- Automation & Robotics

- Safety Interlock Switches Market

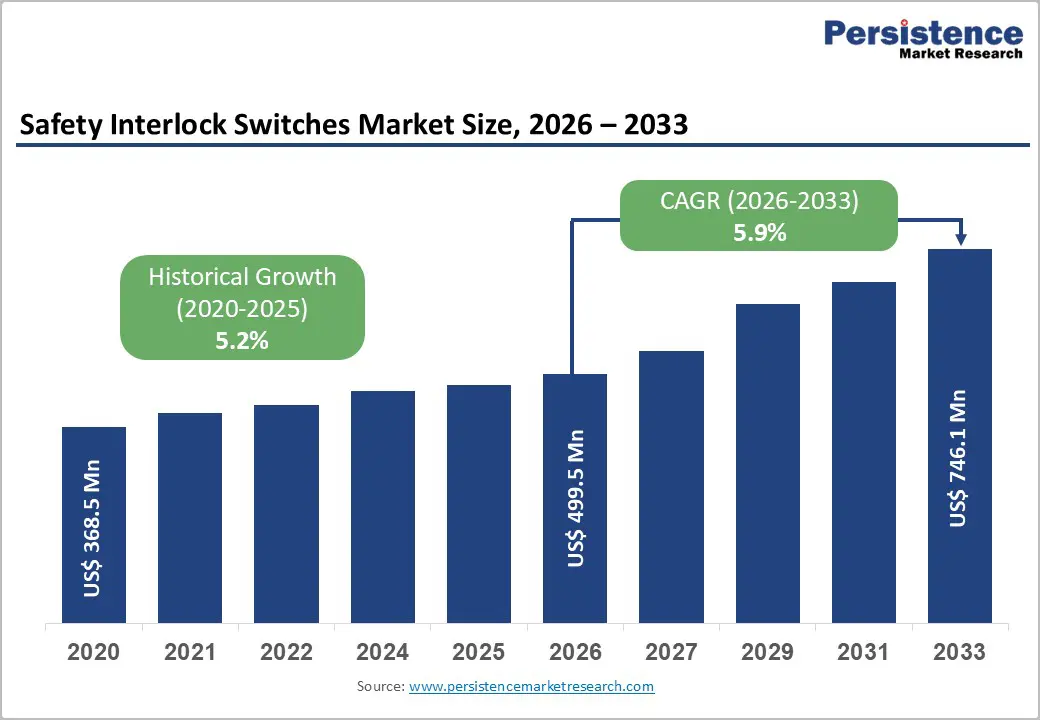

Safety Interlock Switches Market Size, Share, and Growth Forecast 2026 - 2033

Safety Interlock Switches Market by Switch Type (Electromechanical Interlock Switches, Non-Contact Interlock Switches, Tongue-Operated Interlock Switches, Key Interlock Switches, Hinge Interlock Switches, Others), Actuation Mechanism, Industry, Regional Analysis, 2026 - 2033

Safety Interlock Switches Market Size and Trend Analysis

The global safety interlock switches market size is expected to be valued at US$ 499.5 million in 2026 and projected to reach US$ 746.1 million by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

Stringent global safety regulations and rapid industrial automation are major drivers of growth. OSHA recorded 1,675 citations for machine guarding violations in 2024, underscoring the need for reliable interlock systems to reduce workplace accidents. Additionally, the International Federation of Robotics (IFR) reported that industrial robot installations reached 4,664,000 units in 2024, a 9% year-over-year increase, thereby boosting demand for advanced safety interlocks in automated and collaborative industrial environments.

Key Industry Highlights:

- Leading Region: Asia Pacific leads with 39.6% share in 2025, driven by industrialization, automation, and robotics adoption.

- Fastest-Growing Region: Europe is the fastest-growing region with a CAGR of 6.1%, fueled by Industry 4.0 adoption and the modernization of manufacturing infrastructure.

- Leading Switch Type: Non-Contact Interlock Switches dominate the market with a 34.6% market share in 2025, preferred for reliability in harsh environments and compliance with ISO 14119.

- Leading Actuation Mechanism: Guard/Door Actuated Switches hold 35.8% share in 2025, critical for machine guarding and fail-safe operations.

- Key Opportunity Segment: RFID and coded non-contact interlock technology present major opportunities in Industry 4.0 for predictive maintenance and smart factory integration.

| Key Insights | Details |

|---|---|

| Safety Interlock Switches Size (2026E) | US$ 499.5 million |

| Market Value Forecast (2033F) | US$ 746.1 million |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 5.2% |

Market Dynamics

Drivers - Stringent Global Safety Regulations and Industrial Compliance Standards Driving Adoption

Worldwide regulatory frameworks are increasingly mandating rigorous machine safety standards, significantly influencing the adoption of safety interlock switches. In regions such as North America and Europe, organizations must comply with strict machine guarding guidelines, ensuring industrial equipment cannot operate without proper access control. This push toward regulatory compliance has made interlocks essential for minimizing workplace hazards and ensuring legal adherence in manufacturing environments.

Safety interlocks help organizations achieve high-performance safety standards, prevent unauthorized access to hazardous areas, and reduce accident risk. Standards such as ISO 14119 and EN ISO 13849 emphasize interlocking devices and performance levels, encouraging industries across automotive, pharmaceuticals, and general manufacturing to implement these systems. This regulatory focus fosters consistent adoption and investment in advanced interlock technologies.

Accelerated Industrial Automation and Rapid Growth of Robotics Fueling Demand

The fast-paced adoption of industrial automation and robotics has intensified the need for sophisticated safety interlock systems. As factories deploy collaborative robots and integrate automated production lines, interlocks ensure safe human-machine interaction, preventing accidents during operations. Real-time monitoring, access control, and integration with IoT platforms are increasingly critical to maintaining operational safety in smart manufacturing environments.

Automotive, electronics, and general manufacturing sectors increasingly rely on interlocks to optimize efficiency while safeguarding workers. Collaborative robots, sensor-driven machinery, and Industry 4.0-enabled production lines require interlocks that are reliable and flexible. This technological trend drives innovation in safety devices, encouraging manufacturers to invest in R&D to enhance interlock functionality, connectivity, and resilience in highly automated workplaces.

Restraints - High Initial Costs and Equipment Compatibility Challenges Limiting Adoption

Advanced safety interlock systems often require significant upfront investment, which can hinder adoption, particularly in cost-sensitive regions and small-scale manufacturing. Smart interlocks with RFID or IoT features are considerably more expensive than basic electromechanical types, and retrofitting existing machinery can present compatibility issues, leading to project delays and increased planning requirements for manufacturers upgrading legacy systems.

Economic fluctuations also impact capital expenditure, delaying the implementation of modern safety solutions in emerging markets. These high costs and integration challenges can slow adoption, forcing organizations to prioritize other operational investments. As a result, some manufacturers continue using less advanced interlocks or postpone upgrades, limiting market penetration despite regulatory and automation pressures.

Complex Installation Requirements and Shortage of Skilled Safety Technicians

Installing advanced safety interlocks requires specialized knowledge and technical expertise, creating adoption barriers in regions facing labor shortages. Improper installation can compromise safety; unreported incidents are often linked to inexperienced handling, underscoring the need for certified technicians trained in ISO 14119 and related standards to ensure proper setup and operation.

Maintenance for non-contact and IoT-enabled interlocks also demands diagnostic tools and technical skills, increasing operational complexity and ongoing costs. SMEs and small manufacturers that lack in-house safety engineers face challenges in deploying and maintaining these systems, slowing market growth in certain regions despite rising automation and regulatory compliance requirements.

Opportunity - Expansion into Emerging Markets Driven by Rapid Industrialization

Rapid industrialization across the Asia Pacific, particularly in China and India, presents significant opportunities for safety interlock switch adoption. As factories modernize and integrate automated production lines, governments enforce standards such as ANSI and UL compliance, pushing manufacturers to install advanced interlocks. EV production and electronics manufacturing also increase demand for high-voltage and reliable safety solutions.

Strategic partnerships for local production and supply chain optimization can help companies capture substantial market share. The modernization of industrial infrastructure, coupled with government incentives for automation, is driving a growing market for safety interlocks in emerging economies, creating long-term growth potential across the automotive, electronics, and general manufacturing sectors.

Adoption of Non-Contact and Smart Interlock Technologies Offering High Growth Potential

Non-contact interlock switches, including RFID and magnetic types, are emerging as high-growth opportunities due to tamper-resistant designs and maintenance-free operation. These smart devices integrate seamlessly with Industry 4.0 systems, offering PL e-compliance and enhanced safety for collaborative robotics and pharmaceuticals. AI-enabled diagnostics further reduce downtime, making them ideal for automated, high-precision manufacturing environments.

Updated ISO 14119:2025 standards favor coded and smart sensors, encouraging widespread adoption. The combination of enhanced safety, predictive maintenance, and seamless integration with IoT platforms positions non-contact and smart interlocks as a fast-growing segment, with strong potential for both developed and emerging industrial markets.

Category-wise Analysis

Switch Type Insights

Non-Contact Interlock Switches lead the market with 34.6% share in 2025, driven by their superior reliability in harsh and high-risk environments. RFID and coded variants are tamper-resistant and comply with ISO 14119, making them suitable for robotics, pharmaceuticals, and food processing. Magnetic types tolerate misalignment up to 10mm, reducing false trips by nearly 40% compared to electromechanical switches. The automotive and pharmaceutical sectors value them for their hygiene and durability, in line with EHEDG standards.

The fastest-growing segment is smart and IoT-enabled interlock switches, which integrate predictive diagnostics and real-time monitoring. These devices enhance operational safety, reduce downtime, and support Industry 4.0 environments. Their adoption is accelerating across automated production lines, collaborative robots, and high-precision manufacturing due to the combination of tamper resistance, maintenance-free operation, and seamless connectivity with modern industrial systems.

Actuation Mechanism Insights

Guard/Door Actuated Switches dominate the market, accounting for 35.8% of the market in 2025 and are essential for machine guarding under OSHA 1910.212. They ensure fail-safe operation, preventing unauthorized access to hazardous zones. With IP69K ratings, these switches are widely used in food processing, pharmaceuticals, and automotive applications. EN ISO 13849 mandates their integration into PL d/e safety systems, while stringent enforcement helps ensure compliance and reduce accidents.

The fastest-growing actuation segment is two-hand control and sensor-driven switches, favored in automated and robotic setups. These mechanisms provide additional safety in collaborative operations, ensuring both operator protection and continuous machine efficiency. Their flexibility, compatibility with IoT systems, and suitability for high-speed processes are driving adoption in automotive, electronics, and industrial automation applications.

Industry Insights

Automotive Manufacturing holds the largest market share at 30% in 2025, driven by EV assembly lines, high-voltage safety requirements, and robotics integration. Germany alone produced 15.6 million vehicles in 2021, increasing demand for interlocks to safeguard assembly operations. IFR data indicate an automotive robot density of 1,500 units per 10,000 workers, underscoring the need for non-contact interlocks. ANSI/UL compliance reduces workplace accidents by nearly 50%, further encouraging adoption.

The fastest-growing end-use segment is pharmaceuticals and life sciences, where stringent hygiene, safety, and regulatory requirements drive the deployment of non-contact and coded interlocks. High-precision manufacturing, cleanroom environments, and automation integration require switches that minimize contamination risk while supporting Industry 4.0 diagnostics, making this sector a rapidly expanding market for advanced safety interlock technologies.

Regional Insights

North America Safety Interlock Switches Market Trends

North America demonstrates mature adoption of safety interlock switches, largely driven by stringent OSHA enforcement. The US reported 1,675 machine guarding citations in 2024, resulting in $13.7 million in fines, prompting widespread interlock upgrades across automotive, aerospace, and industrial sectors. Compliance with ANSI/UL standards also encourages IoT-enabled solutions, enhancing predictive maintenance and reducing downtime by around 25%.

The market in North America held a 31.7% share in 2025, reflecting strong regulatory adherence and early automation integration. Industry certifications, such as TUV, foster innovation and support Industry 4.0 adoption in pharmaceuticals, robotics, and high-tech manufacturing. This region continues to lead in advanced safety systems while driving best practices for human-machine interaction in automated environments.

Europe Safety Interlock Switches Market Trends

Europe’s safety interlock switch market benefits from harmonized Machinery Directive regulations and proactive adoption of Industry 4.0. Automotive hubs such as Germany's integrate PL e-rated and RFID-enabled interlocks, particularly in EV production lines, reducing violations by 30%. The UK, France, and Spain emphasize CE marking under ISO 14119:2025 to ensure consistent safety standards across the region.

The European market is projected to grow at a CAGR of 6.1%, driven by the modernization of manufacturing infrastructure, increased automation, and the adoption of collaborative robotics. High-tech sectors prioritize predictive maintenance, IoT-enabled interlocks, and compliance, making Europe a hub for innovation in safety devices and advanced industrial safety solutions.

Asia Pacific Safety Interlock Switches Market Trends

Asia Pacific leads global adoption of safety interlock switches, driven by rapid industrialization in China, Japan, and India. The region accounted for a 39.6% global share in 2025, with IFR reporting that 74% of new industrial robot installations occurred here. Coded and RFID-enabled interlocks are in high demand to ensure safe human-machine interaction on automated production lines.

Cost advantages in ASEAN manufacturing reduce deployment costs by approximately 20%, whereas India’s policies encourage local production and technology adoption. The automotive, electronics, and pharmaceutical sectors are major growth drivers, and widespread implementation of Industry 4.0, smart factories, and automated robotics continues to boost interlock adoption across the region.

Competitive Landscape

The safety interlock switches market is moderately consolidated, with leading players collectively holding a significant share of the market. Companies focus heavily on R&D, particularly in IoT-enabled and smart interlock solutions, to enhance connectivity, predictive maintenance, and real-time monitoring for automated production environments.

Strategies focus on geographic expansion, acquisitions, and the development of specialized products for high-demand sectors such as food, pharmaceuticals, and automotive. Key differentiators include high durability, IP-rated designs for harsh conditions, tamper-resistant technologies such as RFID, and subscription-based diagnostics, positioning manufacturers to meet evolving industrial safety requirements.

Key Developments:

- In March 2024, ABB introduced the Busch-art linear® series of safety-integrated switches, designed for enhanced automation applications. These switches offer improved reliability, seamless integration with industrial systems, and support for predictive maintenance, addressing growing demand for smart safety solutions in automated environments.

- In April 2025, IDEM Safety launched its 2025 catalogue featuring stainless steel interlocks tailored for the pharmaceutical sector. These high-durability switches meet strict hygiene and safety standards, enabling secure access control in cleanroom operations and supporting compliance with global regulatory requirements.

- In September 2025, Rockwell Automation expanded its portfolio of guardlocking interlocks for robotics applications. The new models enhance operator safety in collaborative robotic environments, provide IP-rated durability, and integrate with IoT-enabled monitoring systems to improve operational efficiency and accident prevention.

Companies Covered in Safety Interlock Switches Market

- Schneider Electric SE

- Rockwell Automation, Inc.

- Siemens AG

- ABB Ltd.

- Honeywell International Inc.

- Omron Corporation

- Eaton Corporation plc

- SICK AG

- Banner Engineering Corp.

- IDEC Corporation

- Pilz GmbH & Co. KG

- Keyence Corporation

- Schmersal GmbH & Co. KG

- Balluff GmbH

- Pepperl+Fuchs SE

Frequently Asked Questions

The global safety interlock switches market is projected to reach US$ 499.5 million in 2026.

Stringent OSHA and ISO regulations, with 1,675 US violations in 2024, drive adoption for accident prevention.

Asia Pacific leads with 39.6% share in 2025, fueled by industrialization, robotics, and automation.

RFID and coded non-contact interlocks offer growth potential in Industry 4.0, IoT-enabled factories, and predictive maintenance.

Leading players include Schneider Electric, ABB, Rockwell Automation, and IDEM Safety Switches.