- Smart Packaging

- Reusable Packing Market

Reusable Packing Market Size, Share, and Growth Forecast, 2026 - 2033

Reusable Packing Market by Material (Plastic, Wood, Others), Product Type (Returnable Containers & Pallets, Crates & Pallets, Others), End-use Industry, Distribution Channel, and Regional Analysis for 2026 - 2033

Reusable Packing Market Size and Trends Analysis

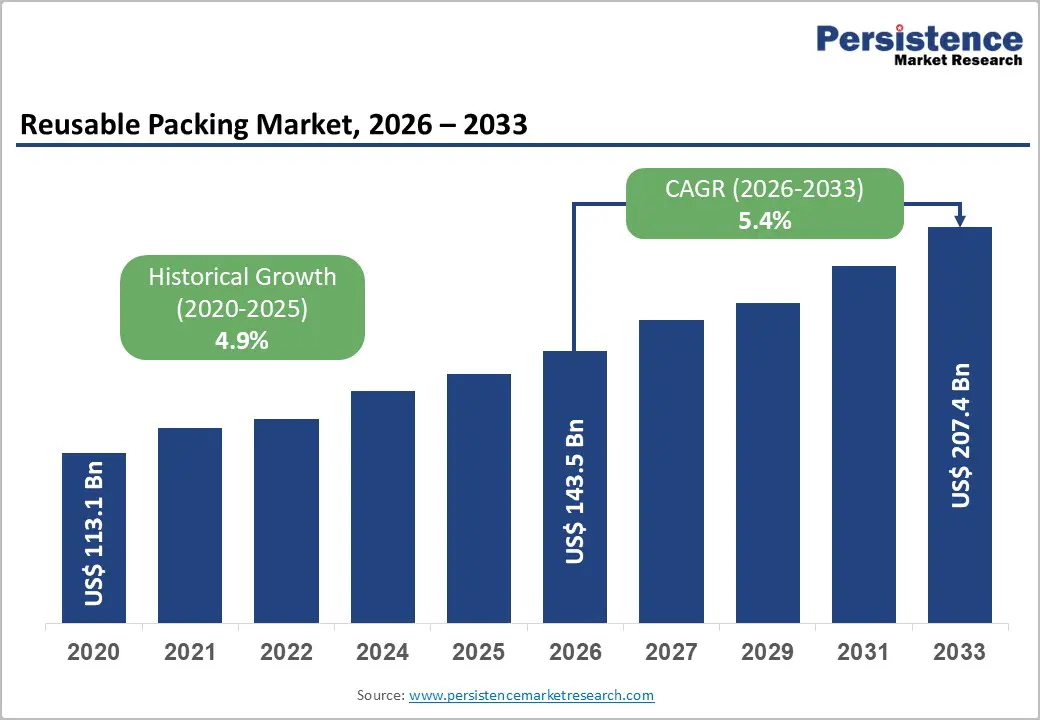

The global reusable packing market size is likely to be valued at US$ 143.5 billion in 2026 and is expected to reach US$207.4 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by the shift from sustainability-focused experimentation to the widespread adoption of reusable packaging within key supply chains.

Factors such as regulatory mandates, lifecycle cost optimization, and the growth of e-commerce and temperature-sensitive logistics are fueling demand. As rotation economics improve and pooling infrastructure expands, reusable packaging systems are increasingly seen as long-term, cost-effective, and compliance-driven solutions, rather than merely optional sustainability initiatives.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to lead the market with approximately 37.4% share, supported by manufacturing concentration and expanding e-commerce logistics networks.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, driven by retail modernization in China and India and automation-led warehouse expansion across Japan and ASEAN.

- Investment Plans: Companies are prioritizing IoT-enabled asset tracking, automated reconditioning centers, and regional pooling hubs to improve turnaround time and asset utilization rates.

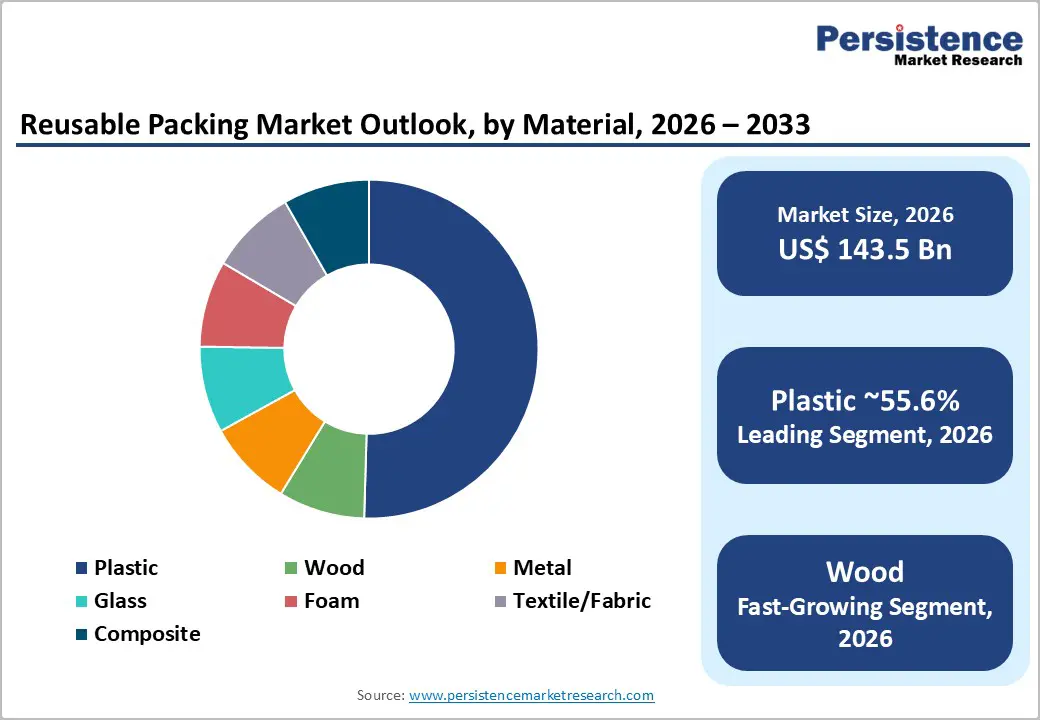

- Dominant Material: Plastic remains dominant with an anticipated 55.6% market share, owing to durability, lightweight structure, and automation compatibility.

- Leading Product Type: Returnable containers & pallets account for an anticipated 46.4% market share, supported by standardized pooling systems and high rotation frequency in retail and industrial logistics.

| Key Insights | Details |

|---|---|

| Reusable Packing Market Size (2026E) | US$143.5 Bn |

| Market Value Forecast (2033F) | US$207.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Push toward Reuse and Stricter Packaging Waste Rules

Governments across North America, Europe, and Asia are strengthening packaging waste regulations, encouraging reuse targets, and extending producer responsibility mechanisms. The European Union’s Packaging and Packaging Waste Regulation establishes binding reuse targets and design-for-recyclability standards, materially shifting procurement decisions toward reusable systems. Regulatory clarity increases the effective cost of disposable packaging and improves payback economics for pooled containers. Companies with established pooling networks and reconditioning capacity benefit from accelerated replacement cycles as retailers and manufacturers transition to compliant packaging formats. Regulation is transforming reuse from a voluntary sustainability initiative into a structural compliance requirement.

Supply Chain Cost Optimization and Pooling Economics

Enterprises are shifting from unit-cost comparisons to total lifecycle cost assessments. When reusable assets achieve sufficient rotation counts, they reduce per-shipment expenses, product damage, landfill fees, and procurement frequency. Large retailers and manufacturers report measurable savings from standardized pallets and returnable containers due to improved fill rates and reduced shrinkage. Pooling models distribute capital expenditures across multiple users, reducing adoption barriers for mid-sized suppliers. Investments in tracking technology and reverse logistics are improving asset visibility and reducing losses. Lifecycle cost transparency and pooling scale are expanding adoption across food & beverage, automotive, and industrial supply chains.

E-Commerce Expansion and Cold Chain Requirements

E-commerce growth, particularly in online grocery and temperature-sensitive goods, increases the need for durable, insulated, and returnable packaging. Multi-stage handling and higher return rates elevate the importance of protective packaging that can withstand repeated cycles. Cold chain logistics for pharmaceuticals, fresh produce, and perishable foods further support reusable insulated containers and bulk transport systems. Sectors with strict temperature control and serious damage sensitivity demonstrate above-average reusable adoption, while 3PLs and retailers pilot subscription-based and pooled return systems to manage last-mile complexity.

Barrier Analysis - Upfront Capital Investment and Operational Complexity

Reusable packaging systems require higher initial capital expenditures for asset pools, digital tracking systems, and reconditioning facilities. For low-rotation SKUs, break-even periods may extend beyond three years. Smaller suppliers with limited cash flow face difficulty funding pooled infrastructure participation. Operational complexity, including reverse logistics coordination and asset tracking, adds administrative burden. Capital intensity and complexity slow adoption in fragmented or price-sensitive supply chains, despite favorable long-term economics.

Regulatory Fragmentation across Jurisdictions

Although reuse mandates are expanding, regulatory interpretation varies by country and region. Differences in labeling, food-contact approvals, hygiene standards, and rotation reporting create compliance friction for multinational operators. Incremental compliance costs can represent several percentage points of packaging-related operating expenses. Regulatory inconsistency reduces scalability for cross-border pooling operations and delays full market harmonization.

Opportunity Analysis - Asia Pacific Industrialization and Retail Modernization

Asia Pacific represents the largest and fastest-growing regional market, holding approximately 37.4% of the global share. Manufacturing concentration, expanding organized retail, and dense trade corridors improve reverse logistics efficiency and rotation economics. Urbanization shortens transport distances, enhancing asset utilization. Establish regional pooling hubs, expand reconditioning capacity, and partner with domestic 3PLs to capture early-mover advantages in high-growth markets such as China, India, and Southeast Asia.

Digital Tracking and Servitization Models

IoT-enabled asset tracking, RFID tagging, and data analytics improve rotation counts and reduce shrinkage. Visibility across supply chains allows operators to optimize asset deployment and reduce loss rates. Reusable packaging providers are increasingly shifting toward asset-as-a-service models, generating recurring revenue streams rather than one-time product sales. Invest in digital infrastructure that increases asset productivity and enables subscription-based pricing models.

Category-wise Analysis

Material Insights

Plastic is anticipated to hold approximately 55.6% share of the reusable packing market, maintaining its leadership position due to its superior durability-to-weight ratio, resistance to moisture and chemicals, and design flexibility. High-density polyethylene (HDPE) and polypropylene (PP) are widely used in reusable plastic crates, pallets, intermediate bulk containers (IBCs), and foldable bins across retail, food & beverage, pharmaceuticals, and industrial logistics. The installed base of reusable plastic containers in grocery and fresh produce supply chains supports recurring pooling revenue for operators such as Brambles Limited (CHEP) and ORBIS Corporation. Lightweight construction lowers freight costs compared with metal alternatives, while RFID-enabled plastic pallets enhance asset tracking and supply chain visibility. Their compatibility with automated storage and retrieval systems (AS/RS) further strengthens adoption in high-throughput distribution centers.

Wood is projected to be the fastest-growing material segment, particularly in heavy-duty pallet and industrial transport applications. Wooden pallets offer strong load-bearing capacity, cost-effective repairability, and standardized global acceptance under ISPM-15 regulations for cross-border trade. They remain dominant in automotive, construction materials, and manufacturing supply chains where high static and dynamic load capacities are required. Regional timber availability and well-established pallet repair ecosystems extend product lifecycles and lower the total cost of ownership. Companies such as UFP Industries support large-scale pallet manufacturing and refurbishment networks. As industries prioritize reparability, recyclability, and localized sourcing, wood gains incremental share in B2B transport applications requiring high load tolerance and operational flexibility.

Product Type Insight

Returnable containers and pallets are anticipated to account for approximately 46.4% of market share, driven by their central role in closed-loop logistics systems. Standardized footprints such as 48x40-inch pallets and Euro pallets ensure compatibility with automated conveyor lines, robotic picking systems, and warehouse management software. High rotation frequency and pooling subscription fees contribute significantly to revenue dominance. Retailers and manufacturers favor interoperable systems that integrate seamlessly with automation platforms deployed by firms such as Daifuku Co., Ltd. Major pooling providers, including Brambles Limited, enable asset optimization, reduced capital expenditure, and improved sustainability reporting through centralized asset tracking models.

Crates and pallets are projected to grow at an anticipated CAGR of approximately 7.5%, supported by e-commerce fulfillment expansion and omni-channel logistics growth. Foldable, collapsible, and nestable crate designs significantly reduce empty backhaul freight costs and warehouse storage space requirements. Automation compatibility and durability across multiple handling touchpoints make these systems attractive for high-volume distribution networks, particularly in grocery retail and last-mile delivery. Retailers such as Walmart Inc. increasingly deploy reusable plastic crates for fresh produce and online grocery orders, while logistics providers integrate stackable pallet systems to improve vehicle cube utilization and reverse logistics efficiency.

Regional Market Insights

North America Reusable Packing Market Trends - Mature Closed-Loop Pooling with IoT-Driven Asset Optimization

North America represents a mature yet steadily expanding reusable packing market, supported by consolidated retail networks, advanced warehouse automation, and established pallet pooling systems. The U.S. leads regional adoption due to the widespread presence of closed-loop logistics models operated by Brambles Limited (CHEP) and PECO Pallet. These pooling providers supply standardized pallets and containers to major retailers such as Walmart Inc. and The Kroger Co., reinforcing recurring asset rotation and reducing one-way packaging waste. High per-capita consumption and extensive grocery distribution networks strengthen the economics of reuse in food and beverage supply chains.

Retail sustainability commitments and private-label expansion further reinforce adoption. For example, Target Corporation has incorporated sustainable packaging goals into its owned-brand strategy, encouraging suppliers to transition toward reusable transport packaging for inbound logistics. While no federal reuse mandate exists in the U.S., state-level packaging EPR frameworks in California and Oregon create indirect incentives for reusable transit packaging. In parallel, Canada’s integrated North American supply chains enable cross-border pooling in fresh produce and automotive components, particularly through logistics providers such as Canadian National Railway that support high-volume freight corridors. Investment trends increasingly focus on IoT-enabled pallet tracking, urban reconditioning centers, and data-driven asset optimization. CHEP’s deployment of digital tracking technologies across North American fleets enhances real-time visibility and reduces shrinkage rates, improving asset utilization. Reverse logistics capabilities are also being integrated within third-party logistics providers such as C.H. Robinson, shortening turnaround cycles and improving container recovery rates across regional distribution hubs.

Europe Reusable Packing Market Trends - Regulatory-Led Reuse Expansion with Standardized Cross-Border Systems

Europe demonstrates strong regulatory momentum favoring reusable packaging systems, creating a predictable framework for investment and cross-border scale. EU-level policy direction under the Packaging and Packaging Waste Regulation (PPWR) establishes binding reuse and recyclability targets, encouraging retailers and manufacturers to shift toward standardized reusable transport packaging. This regulatory clarity reduces long-term uncertainty and supports capital deployment into durable pallet and crate infrastructure.

Germany’s industrial base and automotive exports sustain demand for heavy-duty reusable pallets and containers, supported by firms such as Schoeller Allibert, which operates multiple production and reconditioning facilities across Europe. In the U.K., retailers, including Tesco PLC, have expanded reusable transit packaging programs within fresh produce supply chains to reduce corrugated waste. France has advanced reuse pilots in grocery distribution aligned with its Anti-Waste Law for a Circular Economy (AGEC), accelerating collaboration between retailers and pooling operators.

Consolidation among manufacturers and pooling providers strengthens scale efficiencies and asset standardization. Euro Pool System continues expanding its reusable crate pooling network across continental Europe, improving cross-border interoperability for fresh produce logistics. Automated washing and reconditioning facilities equipped with digital tracking systems enhance compliance reporting and traceability, increasingly serving as competitive differentiators. Companies aligning early with regulatory timelines secure stronger procurement positioning with major European retail chains, where sustainability performance influences supplier selection criteria.

Asia Pacific Reusable Packing Market Trends - Manufacturing Concentration and E-Commerce Driving Reusable Packaging Growth

Asia Pacific is projected to hold approximately 37.4% of the market share and represents the fastest-growing region, driven by manufacturing concentration, rapid e-commerce expansion, and organized retail development. China leads in industrial reusable packaging applications, supported by large-scale manufacturing exports and integrated domestic distribution networks. Logistics giants such as JD Logistics have invested in reusable cold-chain containers and standardized transport packaging to reduce single-use waste in grocery and pharmaceutical deliveries, strengthening closed-loop models in urban centers.

Japan’s high automation standards and advanced robotics adoption favor precision-engineered reusable plastic containers compatible with automated storage systems. Companies such as Daifuku Co., Ltd. integrate reusable pallet systems within automated warehouses, reinforcing demand for durable, dimensionally consistent carriers. In India, retail modernization led by organized players, including Reliance Retail, supports pilot programs using reusable crates in fresh produce distribution across metropolitan areas. Government-led logistics initiatives such as the PM Gati Shakti program further enhance multimodal freight connectivity, improving reverse logistics viability. ASEAN economies benefit from cross-border trade in perishables and automotive components, encouraging standardized reusable pallet flows between Thailand, Vietnam, and Malaysia. Investment priorities across the region include localized pooling hubs, domestic manufacturing of reusable carriers to reduce import dependency, and partnerships with third-party logistics providers to scale reverse logistics networks. As automation penetration and retail formalization increase, Asia Pacific strengthens both its leading market share and its position as the fastest-growing regional segment.

Competitive Landscape

The global reusable packing market is moderately concentrated in pooling services but fragmented among manufacturers and regional reconditioners. A limited number of global operators control significant pooled pallet and crate networks, generating recurring service revenue. Regional manufacturers compete on customization and localized service offerings. Scale advantages are strongest in pooling operations where asset density and logistics orchestration determine profitability.

Leading firms emphasize servitization, digital asset tracking, pooling consolidation, and regional reconditioning expansion. Competitive differentiation centers on network scale, lifecycle analytics, and integrated reverse logistics capabilities.

Key Industry Developments

- In December 2025, Range International’s subsidiary Re>Pal Indonesia secured its first pallet rental orders for 6,000 upcycled plastic pallets from major customers, including Nestlé Indonesia and Sinar Mas Agro Resources and Technology, expanding the company’s reusable pallet footprint in Southeast Asia.

- In April 2025, Brambles (CHEP) initiated a global sustainability program focused on increasing the circularity of its pallet and container pools, with targets to integrate more recycled content into manufacturing and reduce material waste across international reusable packaging operations.

Companies Covered in Reusable Packing Market

- Brambles Limited

- Schoeller Allibert

- ORBIS Corporation

- Euro Pool System

- UFP Industries

- DS Smith

- Menasha Corporation

- SSI Schaefer

- IPL Plastics

- CABKA Group

- Nefab Group

- IFCO Systems

- Greif, Inc.

- Tosca Services

- Rehrig Pacific Company

- Myers Industries

- Buckhorn Inc.

- Craemer Group

Frequently Asked Questions

The global reusable packing market size is estimated at US$143.5 billion in 2026.

The market is projected to reach US$207.4 billion by 2033.

Key trends include IoT-enabled asset tracking, expansion of regional pooling hubs, automation-compatible returnable containers, regulatory push for reuse targets in Europe, and growth of reverse logistics partnerships with 3PL providers.

By material, plastic is the leading segment with an anticipated 55.6% market share, owing to lightweight durability and compatibility with automated handling systems.

The reusable packing market is projected to grow at a CAGR of 5.4%, supported by retail consolidation, manufacturing exports in Asia Pacific, and sustainability-driven supply chain transformation.

Major companies with strong reusable packaging portfolios include Brambles Limited, Schoeller Allibert, ORBIS Corporation, Euro Pool System, and UFP Industries.