- Plastics, Polymers & Resins

- Resin Moulds Market

Resin Moulds Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Resin Moulds Market by Material Type (Silicone, Latex, Polyurethane, Plastic, Other), Resin Compatibility (Epoxy Resin, UV Resin, Polyurethane Resin, Other), Application (Jewelry, Decorative Art, Automotive Components, Architectural Parts, Industrial Components, Other), and Regional Analysis for 2025 - 2032

Resin Moulds Market Size and Trend Analysis

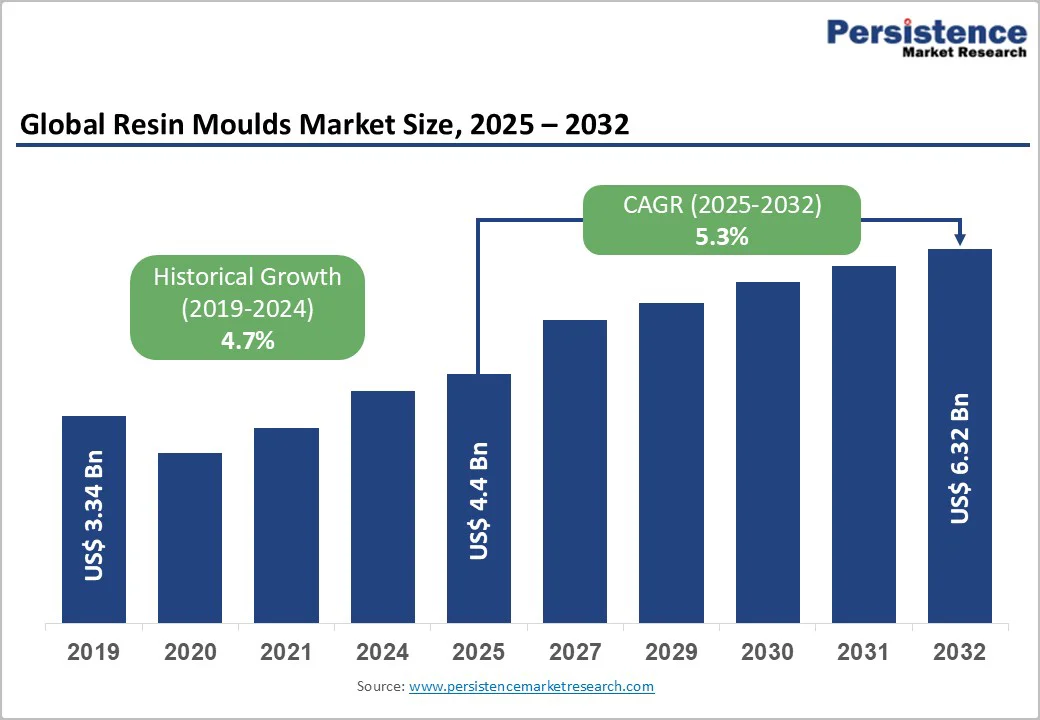

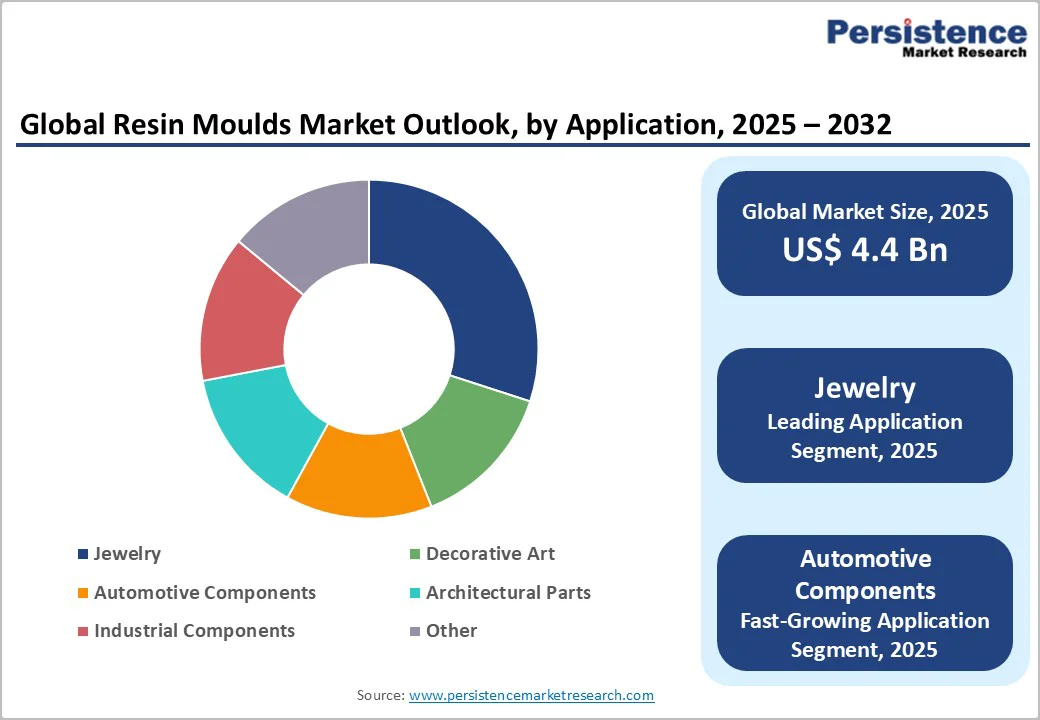

The global resin moulds market size is valued at US$4.4 billion in 2025 and is projected to reach US$6.3 billion by 2032, growing at a CAGR of 5.3% between 2025 and 2032.

The major drivers include rising demand for customized products across industries such as jewelry and automotive, supported by advancements in material flexibility and precision manufacturing.

Key market dynamics include the increasing adoption of resin moulds in lightweight component manufacturing, particularly in the automotive sector, where fuel-efficiency regulations mandate material innovation.

Key Market highlights

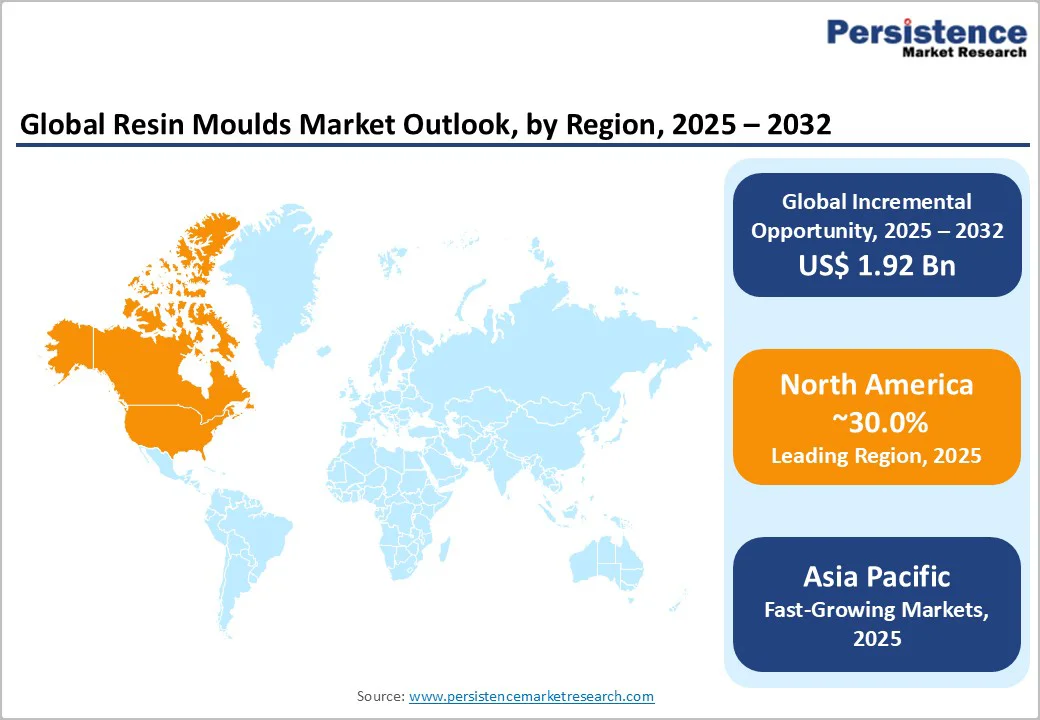

- Regional Leader: North America leads the resin moulds market, with 30% of the market, due to advanced innovation ecosystems and regulatory support from the EPA and FAA, ensuring high adoption in aerospace and automotive sectors.

- Fastest Growing Region: Asia Pacific is driven by accelerating industrialization in China, India, manufacturing expansion through government initiatives, and substantial infrastructure development projects, creating sustained composite material demand.

- Leading Segment: Silicone dominates material type segments with 40% share, offering flexibility for jewelry and decorative applications.

- Fastest Growing Segment: Epoxy Resin compatibility grows fastest at 35% share, driven by industrial durability needs in automotive components.

- Growth Opportunities: Key opportunity lies in bio-based resins, aligning with EU sustainability policies for 30% renewable content by 2030.

| Key Insights | Details |

|---|---|

| Resin Moulds Market Size (2025E) | US$4.4 Bn |

| Market Value Forecast (2032F) | US$6.3 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.3% |

| Historical Market Growth (2019 - 2024) | 4.7% |

Market Dynamics

Drivers - Rising Demand for Customization

The increasing consumer preference for unique and customized products is fundamentally transforming manufacturing approaches across jewelry, automotive, and consumer goods sectors, with resin moulds emerging as critical enablers of this trend.

The global jewelry market has witnessed a significant shift toward bespoke pieces, with jewelry casting resins enabling faster production times and the creation of highly detailed designs that traditional metal casting cannot achieve, thereby meeting the growing demand for personalized ornaments at competitive price points.

Furthermore, innovations in resin chemistry have led to formulations that mimic the appearance and texture of precious metals such as gold, silver, and platinum, enabling designers to produce visually appealing jewelry at lower production costs.

This customization capability extends to decorative articles and architectural elements, where advanced resin formulations enable the replication of complex patterns and textures previously achievable only through expensive traditional methods.

Advancements in Lightweight Materials

Technological progress in lightweight resin composites, particularly for automotive and aerospace applications, propels the market by offering superior strength-to-weight ratios, improving fuel efficiency and reducing emissions. Modern vehicles require components that reduce overall weight without compromising structural integrity or safety performance.

The integration of resin moulds in electric vehicle components has grown by 20% in recent years, driven by regulatory pushes for sustainability.

The integration of advanced simulation tools, such as finite element analysis (FEA) and computational fluid dynamics (CFD), has revolutionized mould design optimization, enabling engineers to predict performance characteristics and identify potential defects before physical production begins.

These technological advancements have particularly benefited the production of complex automotive and electronics components, where precision requirements are stringent and even minor dimensional variations can compromise product performance.

Restraints - High Initial Investment and Equipment Costs for Advanced Mould Production

The substantial capital investment required to establish advanced resin mould manufacturing facilities is a significant barrier to market entry, particularly for small and medium-sized enterprises seeking to compete with established players.

Modern mould production systems incorporating automation, precision machining equipment, and quality control technologies demand considerable upfront expenditure, with additional ongoing costs for maintenance, calibration, and operator training programs.

Furthermore, the specialized nature of certain resin formulations and curing equipment necessitates technical expertise that may not be readily available in all geographic markets, potentially limiting the expansion of production capacity in emerging economies despite strong demand growth. Economic uncertainty and fluctuating raw material prices, particularly for petroleum-based resin components, create additional financial pressures that can affect profitability margins and investment decisions.

Environmental Concerns and Regulatory Compliance Challenges

Growing environmental awareness and increasingly stringent regulations regarding VOC emissions and non-biodegradable waste disposal are creating operational challenges for traditional resin mould manufacturers. Conventional petroleum-based epoxy and polyurethane resins contribute to greenhouse gas emissions during production and often pose difficulties for end-of-life disposal, as these materials can take years to decompose in landfills.

Regulatory frameworks in developed markets such as the EPA in the U.S. and the EU’s REACH are progressively tightening emission standards and mandating the use of sustainable materials, compelling manufacturers to invest in cleaner production technologies and reformulate existing products.

The transition to eco-friendly alternatives, such as Bio-Based Epoxy Resins and recyclable composites, requires substantial research and development investments, and performance validation often extends product development timelines.

Opportunities - Adoption of Bio-Based Resins

The accelerating shift toward sustainable manufacturing practices presents substantial growth opportunities for manufacturers developing environmentally friendly resin mould solutions that reduce carbon footprints while maintaining performance standards. The bio-based epoxy resins market is experiencing rapid growth, supported by EU policies mandating 30% bio-content in composites by 2030, creating demand for compatible moulds.

Many bio-based resin formulations are designed to be compostable or more easily recyclable, addressing end-of-life disposal challenges and contributing to circular economy initiatives that are becoming increasingly important to environmentally conscious consumers and regulatory authorities.

The growing emphasis on sustainability certifications and green building standards, particularly in the construction and architectural applications sector, is driving the specification of eco-friendly resin moulding solutions that meet stringent environmental performance criteria while delivering exceptional durability.

Growing Applications in Electric Vehicle Components

The shift to electric mobility and device miniaturization is driving demand for resin moulding solutions that deliver strength, durability, and thermal stability. EV makers use these moulds to produce lightweight composite parts for batteries, chargers, and sensors, ensuring reliability at extreme temperatures.

Advanced technologies now produce compact motor components that withstand temperatures from -40°C to 80 °C and withstand 1,000 cycles, solving challenges of thermal expansion in multi-material designs.

The development of heat-resistant resins for connectors, switches, and insulators on circuit boards, combined with growing demand for precision insert moulding in medical devices, aerospace, and defense applications, represents substantial revenue opportunities for manufacturers with advanced technical capabilities.

Category-wise Analysis

Material Type Insights

Silicone leads the material type category with approximately 40% market share, attributed to its exceptional flexibility, durability, and ease of use in creating detailed moulds for various applications.

Silicone's superior flexibility, tear resistance, and durability enable multiple casting cycles without significant degradation, providing greater long-term value than alternative materials. The material's excellent release properties eliminate the need for frequent application of external release agents, streamlining production workflows and reducing operational costs.

The expansion of Dow Inc.'s global silicone resin capacity, including new facilities in Zhangjiagang, China, reflects growing demand for specialty silicone products in home and personal care, pressure-sensitive adhesives, and moldable optics applications.

The innovations, such as DOWSIL™ 2080 Resin, recognized in the 2024 R&D 100 Awards, demonstrate ongoing technological advancement in solventless silicone resin formulations that enhance heat resistance and durability for powder coating applications.

Resin Compatibility Insights

Epoxy Resin holds the leading position in resin compatibility with around 35% share. Epoxy resins offer exceptional adhesion to diverse substrates, outstanding dimensional stability during curing, and excellent resistance to environmental degradation, making them preferred choices for applications demanding long-term durability under challenging conditions.

The bio-based epoxy resins market is experiencing accelerated growth as manufacturers respond to environmental regulations and consumer preferences for sustainable materials, with innovations in plant-derived formulations from vegetable oils and lignin offering performance comparable to petroleum-based alternatives.

The growing adoption of epoxy resin moulds in the decorative laminates market reflects the material's ability to produce high-pressure laminates with enhanced abrasion resistance, improved dimensional stability, and superior aesthetics for furniture, countertops, and wall paneling applications.

Application Insights

Jewelry Manufacturing dominates the application segment, with about 30% market share, fueled by the need for intricate, customizable designs that resin moulds facilitate at a lower cost than metal casting.

The transformation of the global Jewelry market toward customized designs has positioned resin casting as a cost-effective alternative to traditional metal casting methods, with modern formulations capable of simulating the appearance of precious metals while enabling intricate detail reproduction that is impossible with conventional techniques.

The DIY jewelry-making movement, particularly among younger demographics, creates expanding opportunities for end users as hobbyists develop commercial capabilities through accessible online platforms.

Social media platforms, including Instagram and TikTok, amplify demand through viral jewelry design trends and influencer-driven product discovery. The global jewelry market continues to expand, supported by rising consumer spending, gifting occasions, and personalization preferences, driving sustained demand for resin molding solutions.

Regional Insights

North America Resin Moulds Market Trends

North America demonstrates strong market leadership, with 30% of the market, through substantial research and development investments, particularly in the U.S., where well-established automotive and aerospace industries drive continuous innovation in advanced resin moulding technologies.

The region's emphasis on fuel-efficient and electric vehicle development, combined with growing adoption of lightweight composite materials in aerospace applications, has significantly accelerated demand for precision resin moulds capable of producing complex geometries with exceptional dimensional accuracy.

Major manufacturers, including Dow Inc., Huntsman Corporation, and other integrated chemical producers, maintain significant North American production capacity, with ongoing investments in automation and smart manufacturing systems enhancing operational efficiency and product quality.

Europe Resin Moulds Market Trends

Europe's market is characterized by strong performance in Germany, the U.K., France, and Spain, bolstered by harmonized EU REACH regulations that emphasize eco-friendly production and material traceability.

The region's robust automotive industry, particularly in Germany, maintains high demand for precision resin moulds used to produce lightweight components that meet increasingly strict vehicle emission standards while enhancing fuel efficiency and performance.

Germany's engineering prowess drives adoption in automotive, with BMW and Volkswagen integrating resin moulds for lightweight parts, achieving 10% emission reductions. The U.K.'s creative industries contribute through artisanal growth, supported by post-Brexit incentives for local manufacturing.

Collaborative initiatives between Univar Solutions and Dow to distribute construction silicone products across Central and Eastern Europe exemplify industry efforts to expand market reach while providing durable, water-repellent materials for demanding building applications.

Asia Pacific Resin Moulds Market Trends

Asia Pacific is the fastest-growing regional market, with rapid industrialization, urbanization, and economic expansion in China, India, Japan, and the ASEAN nations driving unprecedented demand for resin moulding solutions across multiple end-use sectors.

China's dominance as a production hub has led to a 25% capacity expansion in 2024, supported by government plans such as the 14th Five-Year Plan. India's Make in India initiative has spurred infrastructure projects, increasing mould usage in construction by 20%.

Government incentives promoting the adoption of low-VOC technologies and sustainable manufacturing practices are accelerating market transition toward environmentally friendly resin formulations, particularly in developed markets such as Japan and emerging economies implementing stricter environmental standards.

The region's dynamic e-commerce ecosystem, with online retail channels experiencing rapid growth, is democratizing access to specialized resin moulding products and enabling small-scale manufacturers and artisans to source professional-quality materials at cost-effective prices.

Competitive Landscape

The global resin moulds market is moderately fragmented, with top players holding about 40% share while numerous regional suppliers compete in niche segments. Companies pursue expansion through R&D investments in sustainable materials and strategic partnerships for technology transfer.

Key market differentiators include technological innovation in resin formulations, proprietary curing systems, integrated chemical backbones across product segments, and extensive application development capabilities supported by global innovation hubs in strategic locations.

Market participants are increasingly investing in smart manufacturing technologies, sensor-equipped production systems, and digital transformation initiatives to enhance quality control, reduce lead times, and enable predictive maintenance.

Key Market Developments

- August 2024: Dow Inc. received recognition in the 2024 R&D 100 Awards for five innovative products, including DOWSIL™ 2080 Resin, a solventless liquid silicone resin that chemically reacts with organic resins to create high-quality binders for heat-resistant powder coatings with improved appearance and durability.

- April 2024: Univar Solutions and Dow announced expansion of their strategic partnership to distribute construction silicone products across Central and Eastern Europe, providing builders with durable, water-repellent, and protective materials utilizing Dow's silicone resins and eco-friendly building solutions.

- December 2024: BASF opened a new Catalyst Development and Solids Processing Center focused on bringing process innovations and new chemical technologies to market, and on supporting the ongoing development of advanced resin formulations and sustainable manufacturing solutions.

Top Companies in the Resin Moulds Market

- Dow Inc. (Headquarters: Midland, Michigan, USA) maintains global leadership through extensive silicone resin production capacity, continuous innovation in specialty chemical formulations, and strategic investments in emerging markets, including major manufacturing facilities in China serving Asia Pacific demand growth.

- BASF SE (Headquarters: Ludwigshafen, Germany) leverages integrated chemical production capabilities, extensive research and development infrastructure, and a broad portfolio spanning polyurethane, epoxy, and specialty resin systems to serve diverse end-use applications across automotive, construction, and industrial sectors.

- Huntsman Corporation (Headquarters: The Woodlands, Texas, USA) maintains a strong market position through its polyurethane systems expertise, global manufacturing footprint, and focus on high-performance applications in the automotive, construction, and industrial markets that require advanced material properties.

Companies Covered in Resin Moulds Market

- Dow Inc.

- Huntsman Corporation

- Solvay S.A.

- Hexcel Corporation

- BASF SE

- Covestro AG

- Alchemie Ltd.

- AOC Resins, LLC

- Sasol Ltd.

- DSM Engineering Materials

- Evonik Industries

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

Frequently Asked Questions

The global resin moulds market is valued at US$4.4 Bn in 2025 and expected to reach US$6.3 Bn by 2032, reflecting steady expansion.

Key drivers include customization demands and lightweight material advancements, boosting adoption in jewelry and automotive sectors by 15-20% annually.

Silicone leads with 40% share due to its flexibility and durability in detailed applications like decorative articles.

North America leads, driven by U.S. innovation and regulatory support from the EPA, fostering aerospace and electronics growth.

Bio-based resins offer significant potential, aligning with EU mandates for 30% renewable content by 2030 in sustainable applications.

Leading players include Dow Inc., Huntsman Corporation, and BASF SE, focusing on R&D and sustainability for market dominance.