- Inks, Coatings, Adhesives & Sealants (ICAS)

- Phenolic Resins Market

Phenolic Resins Market Size, Share, and Growth Forecast 2026 - 2033

Phenolic Resins Market by Product Type (Novolac, Resoles [Liquid Resol Resin, Solid Resol Resin], Modified), by Application (Wood Adhesives, Molding [Molding Compounds, Shell Molding], Paper Impregnation, Coatings, Others), End-user (Automobile, Electric and Electronics, Furniture, Construction, Others), and Regional Analysis, 2026-2033

Phenolic Resins Market Size and Trend Analysis

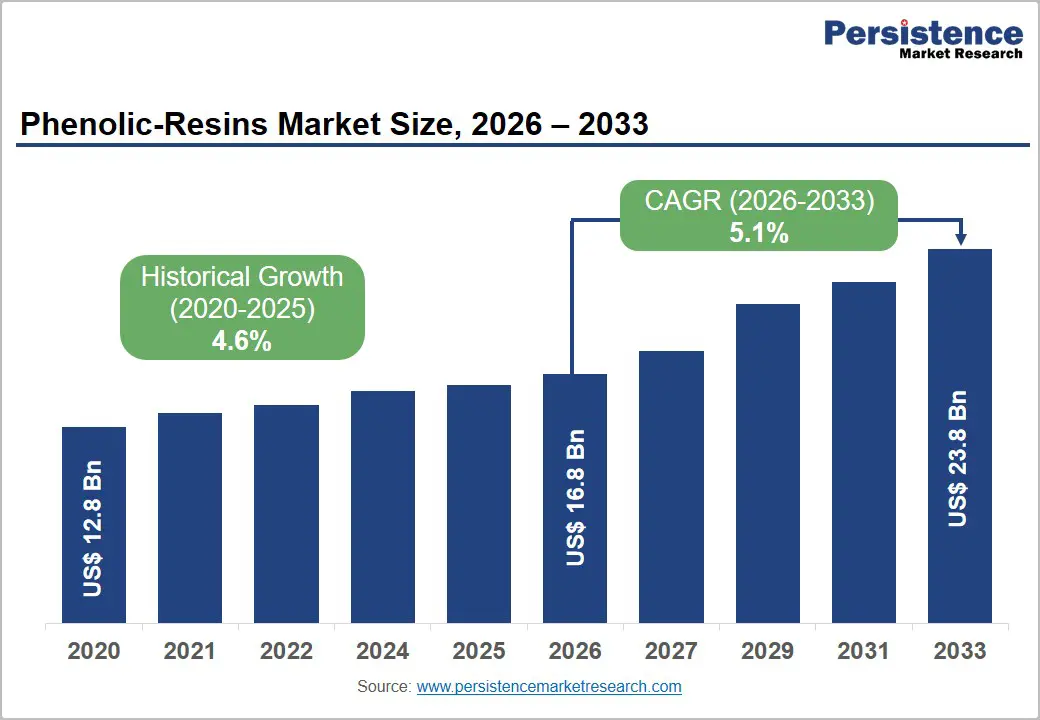

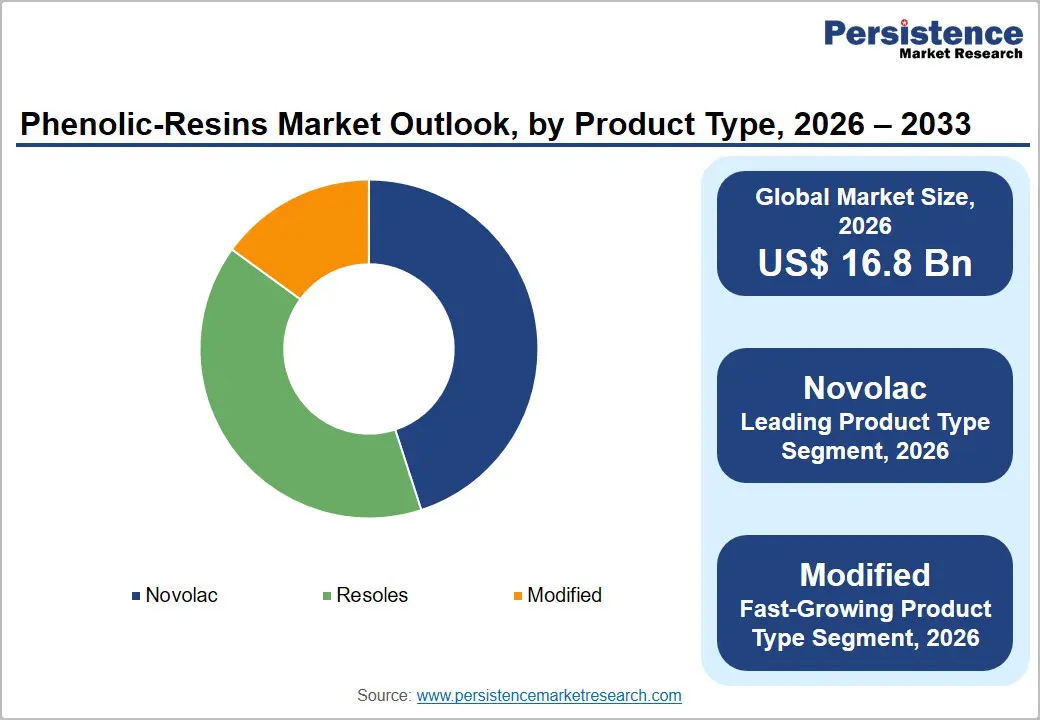

The global phenolic resins market size is expected to be valued at US$ 16.8 billion in 2026 and projected to reach US$ 23.8 billion, growing at a CAGR of 5.1% between 2026 and 2033.

Sustained growth is underpinned by robust demand across the automotive, construction, and electric and electronics industries, where phenolic resins are prized for their superior thermal stability, mechanical strength, and flame-retardant properties.

The accelerating adoption of lightweight composite materials in vehicle manufacturing, expanding engineered wood panel production for green construction, and rising electronic component miniaturization trends together reinforce the strong multi-year demand trajectory for phenolic resin formulations globally.

Key Industry Highlights:

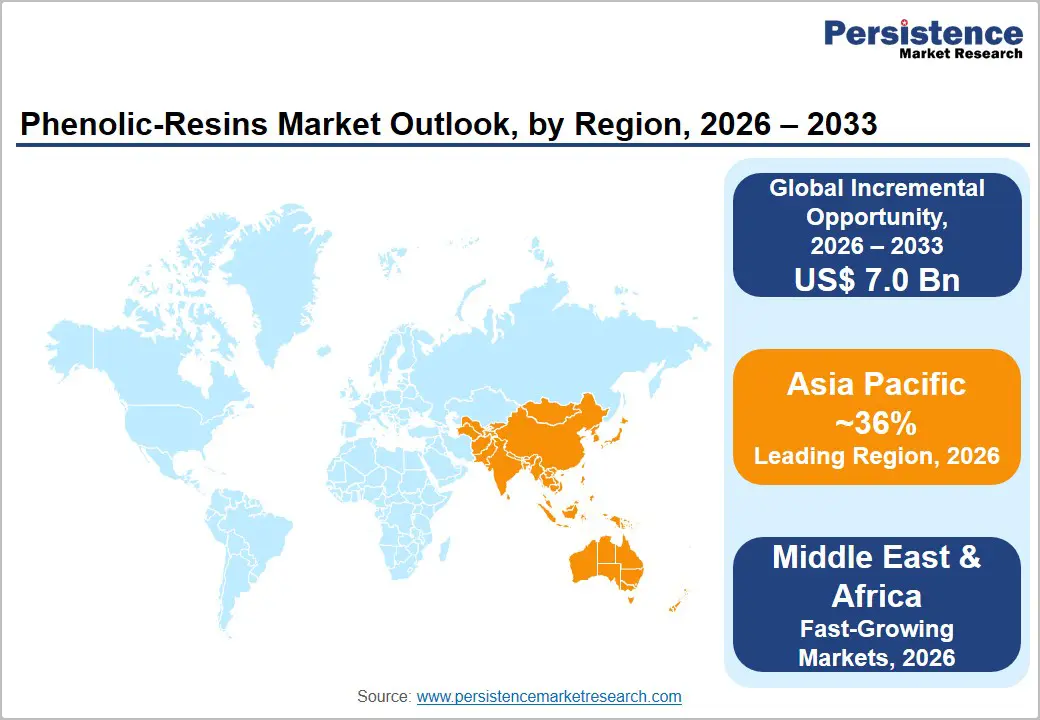

- Leading Region: Asia Pacific dominates global phenolic resin demand with 36% market share in 2026, driven by China's massive wood panel and electronics manufacturing base, alongside India's fast-expanding construction and automotive sectors.

- Fastest Growing Region: Middle East & Africa is the fastest-growing regional market for phenolic resins, fueled by ambitious construction programs, petrochemical industry expansion, and growing demand for engineered wood products driven by urbanization and infrastructure investment.

- Dominant Segment: Novolac leads the Product Type category with approximately 43% market share in 2026, underpinned by its critical role in automotive friction materials, foundry shell molding, and high-performance semiconductor encapsulant applications globally.

- Fast-Growing Product Segment: Modified phenolic resins are the fastest-growing product type at 7% CAGR, driven by demand for bio-based, low-emission formulations compliant with tightening regulatory standards in the EU and North America.

- Key Opportunity: Rapid semiconductor and electronics manufacturing expansion across Asia Pacific, with global semiconductor sales exceeding US$ 526 billion in 2023, creates strong, recurring demand for phenolic resin-based PCB laminates and encapsulant molding compounds.

DRO Analysis

Drivers - Surging Automotive Lightweighting and Composite Materials Demand

The global automotive industry's aggressive transition toward lighter vehicles to meet increasingly stringent fuel efficiency and emissions regulations is generating strong, sustained demand for phenolic resin-based composites and molding compounds. Regulatory frameworks such as the European Union's CO2 emission standards, targeting 0 g CO2/km for new passenger cars by 2035, and U.S. Corporate Average Fuel Economy (CAFE) standards are compelling automakers to replace metal components with high-performance polymer composites.

Phenolic resins, particularly novolac-based thermosets, are widely used in brake linings, under-hood components, and composites due to their exceptional heat resistance above 200°C and dimensional stability. According to the International Energy Agency (IEA), electric vehicle sales surpassed 14 million units globally in 2023, with EV platforms requiring advanced thermal management materials, a key application area for phenolic systems.

Expanding Construction Sector and Engineered Wood Panel Production

Global construction output is projected to reach US$ 15.2 trillion annually by 2030, according to the Global Construction Perspectives and Oxford Economics report, driven by urbanization, infrastructure renewal, and green building initiatives. Phenolic resins, particularly resole-type binders, are essential in the manufacture of oriented strand board (OSB), plywood, medium-density fiberboard (MDF), and laminate flooring, which are core materials in residential and commercial construction.

The Food and Agriculture Organization (FAO) reports that global wood panel production exceeded 430 million m³ in 2022, with engineered wood formats growing at above-average rates. Phenolic resin binders are preferred over urea-formaldehyde in exterior and structural applications due to superior moisture resistance and bond durability, directly expanding market volumes as construction activity intensifies in emerging economies.

Restraints - Regulatory Pressure on Formaldehyde Emissions and Health Concerns

Phenolic resins are synthesized using formaldehyde, a compound classified as a Group 1 carcinogen by the International Agency for Research on Cancer (IARC). Increasingly stringent emission limits under the U.S. EPA's Formaldehyde Emission Standards for Composite Wood Products Act (TSCA Title VI) and equivalent European REACH regulation requirements are raising compliance costs for manufacturers.

These regulations are curtailing application scope in indoor wood panels and interior automotive components, particularly in the EU and North America, constraining volume growth in traditionally high-demand application segments.

Volatility in Phenol and Benzene Feedstock Prices

Phenolic resins are directly dependent on phenol, a petrochemical derivative of benzene and propylene, as the primary raw material, typically constituting 55–65% of total production costs. Phenol prices are highly sensitive to crude oil price fluctuations and refinery operating rates.

The American Chemistry Council (ACC) has documented multi-year price volatility cycles in benzene and cumene chains, with phenol prices swinging by over 30% between 2020 and 2023. Such feedstock price instability compresses manufacturer margins, disrupts long-term contract pricing, and discourages downstream investment in phenolic resin-intensive applications.

Market Opportunities - Growth in Bio-based and Modified Phenolic Resin Formulations

The Modified phenolic resin segment, the fastest-growing at a projected CAGR of 7% from 2026 to 2033, represents a compelling commercial opportunity centered on bio-based, low-emission, and performance-enhanced resin systems. Regulatory pressure on formaldehyde emissions and growing end-user demand for sustainable raw materials is accelerating investment in lignin-modified, cashew nutshell liquid (CNSL)-modified, and epoxy-modified phenolic systems.

The European Chemicals Agency (ECHA) and the U.S. Department of Energy's Bioenergy Technologies Office (BETO) have both funded research programs targeting lignin valorization as a phenol substitute. BASF SE and Hexion LLC have publicly committed to advancing bio-based resin alternatives. Companies capable of scaling bio-modified phenolic platforms can capture premium pricing in regulated markets and attract sustainability-conscious OEM partners across automotive, construction, and electronics sectors.

Rising Demand from Electric and Electronics Sector in Asia Pacific

The rapid proliferation of consumer electronics, printed circuit boards (PCBs), semiconductor packages, and electrical insulation components is generating strong incremental demand for phenolic resin-based laminates and molding compounds across Asia Pacific. According to the Semiconductor Industry Association (SIA), global semiconductor sales exceeded US$ 526 billion in 2023, with fabrication capacity expansions concentrated in Taiwan, South Korea, Japan, and India. Phenolic paper laminates, used extensively as PCB base substrates, are a foundational material in this supply chain.

The India Semiconductor Mission (ISM) and similar national semiconductor strategies in Southeast Asia are catalyzing new electronics manufacturing capacity, directly expanding the addressable market for phenolic resin intermediates. Market participants with established supply chain presence in Asia Pacific are best positioned to capture this accelerating demand wave.

Category-wise Analysis

Product Type Insights

Novolac resins dominate the product type category with approximately 43% share in 2026, establishing their primacy across high-performance thermoset applications. Novolacs, acid-catalyzed, thermoplastic prepolymers cured with hexamethylenetetramine (HMTA), are the resin of choice in abrasive and friction materials, brake linings, foundry shell molds, and semiconductor encapsulants, owing to their superior thermal performance above 300°C and precise processing control. The global automotive aftermarket and the expanding foundry sector in China, India, and South Korea continue to drive strong novolac demand.

Novolac epoxy curing agents are extensively used in high-performance protective coatings, semiconductor photoresists, and advanced composites. The American Foundry Society (AFS) reports consistent growth in resin-bonded sand casting, underpinning sustained novolac market leadership through the forecast period.

Application Insights

Wood adhesives are likely to represent the leading application segment, accounting for approximately 38% share in 2026. Phenolic resin-based wood adhesives, primarily resole-type systems, are the industry standard for exterior-grade plywood, OSB, and structural laminated veneer lumber (LVL), where waterproof bond strength and durability under weather exposure are non-negotiable. The FAO's Global Forest Products Facts and Figures document sustained growth in global plywood and engineered wood production, particularly in China, Indonesia, and Brazil.

Construction sector activity, particularly prefabricated housing, modular construction, and mass timber buildings, is amplifying demand for structural-grade engineered wood panels bonded with phenolic resin. Growing adoption of LEED and BREEAM certified low-emission building products is simultaneously pushing innovation in low-formaldehyde phenolic adhesive formulations.

End-user Insights

The construction sector leads the end-user category, capturing approximately 35% of phenolic resin demand in 2026. Phenolic resins are integral to the construction value chain, from structural engineered wood panels and thermal insulation boards (phenolic foam) to surface laminates and fire-resistant coatings. The United Nations Environment Programme (UNEP) estimates that the construction sector accounts for approximately 36% of global energy consumption and over 37% of CO2 emissions, driving policy-mandated adoption of energy-efficient insulation materials, a key growth vector for phenolic foam boards.

National green building codes in the EU, China, and the U.S. are mandating higher thermal insulation standards, directly expanding consumption of phenolic insulation systems. The sector's leadership is reinforced by sustained global construction spending across residential, commercial, and infrastructure segments.

Regional Analysis

North America Phenolic Resins Market Trends and Insights

North America holds a significant share of the global phenolic resins market, driven by strong demand from the automotive, construction, and electronics industries. The region benefits from well-established resin manufacturing infrastructure, active R&D investment in bio-based and low-emission phenolic systems, and regulatory-driven demand for high-performance, compliant resin formulations under EPA TSCA Title VI frameworks.

U.S. Phenolic Resins Market Size

The United States accounts for approximately 80% of North American phenolic resin revenues in 2026, underpinned by its large automotive manufacturing base, extensive OSB and plywood production sector, and growing electronics manufacturing investments. Federal infrastructure spending under the Bipartisan Infrastructure Law is further stimulating construction-linked phenolic resin demand.

Europe Phenolic Resins Market Trends and Insights

Europe represents a mature, innovation-oriented market with strong regulatory influence on product development. Tightening REACH regulations and ambitious EU Green Deal targets are accelerating the transition toward bio-based and low-formaldehyde resin alternatives. Key demand centers include automotive manufacturing in Germany, France, and the Czech Republic, alongside construction-driven wood adhesive consumption in Scandinavia and Central Europe.

Germany Phenolic Resins Market Size

Germany leads European phenolic resin consumption, contributing approximately 22% of regional revenues in 2026. Home to major automotive OEMs including Volkswagen Group, BMW, and Mercedes-Benz, Germany generates strong demand for phenolic-based friction materials, underbody coatings, and composite structural components, alongside its well-developed construction and engineered wood sectors.

U.K. Phenolic Resins Market Size

The United Kingdom accounts for approximately 12% of European market revenues in 2026. Demand is concentrated in construction insulation, particularly phenolic foam boards used to meet the UK Building Regulations Part L thermal efficiency standards, alongside aerospace composite applications centered around facilities in England and Wales.

France Phenolic Resins Market Size

France contributes approximately 11% to European phenolic resin revenues in 2026. The French market is driven by automotive supply chain activity for major OEM platforms, including Stellantis and Renault Group, which extensively use phenolic-based brake and friction components, alongside demand from the wood panel and construction composites sectors.

Asia Pacific Phenolic Resins Market Trends and Insights

Asia Pacific leads the global phenolic resins market with a 36% share in 2026, anchored by China's massive wood panel, foundry, and electronics manufacturing sectors. China alone accounts for an estimated 50% of regional demand, supported by its world-leading OSB, plywood, and semiconductor packaging industries. Japan, South Korea, and India are also significant consumers, driven by electronics, automotive, and construction end-use demand.

India Phenolic Resins Market Size

India is among the fastest-growing national markets in Asia Pacific, expected to represent approximately 12% of regional revenues by 2027. Rapid expansion of the construction sector under the Pradhan Mantri Awas Yojana (PMAY) housing program and growing domestic automotive production, supported by PLI schemes, are primary demand drivers for phenolic resin-based wood adhesives and molding compounds.

Japan Phenolic Resins Market Size

Japan holds approximately 15% of the Asia Pacific market in 2026. The country is a global technology leader in phenolic resin applications for semiconductor encapsulants and PCB laminates. Sumitomo Bakelite Co. Ltd. and Hitachi Chemical Co. Ltd. are headquartered in Japan and supply critical phenolic-based electronic materials to global OEMs.

Southeast Asia Phenolic Resins Market Size

Southeast Asia contributes approximately 10% of Asia Pacific phenolic resin revenues in 2026, with Indonesia, Malaysia, Vietnam, and Thailand as key markets. The region's large-scale plywood and wood panel export sector, particularly from Indonesia, is a major consumer of resole-type phenolic resin binders, alongside rapidly growing electronics manufacturing clusters attracting semiconductor and PCB supply chain investment.

Competitive Landscape

The global phenolic resins market is moderately consolidated, with leading players including Hexion LLC, BASF SE, Sumitomo Bakelite Co. Ltd., SI Group, and DIC Corporation holding significant market shares through proprietary resin technology and integrated production networks.

Key competitive strategies include investment in bio-based and low-formaldehyde resin R&D, capacity expansion in Asia Pacific to serve local demand, and strategic long-term supply agreements with automotive and wood panel OEMs. Emerging competitors are differentiating through specialty modified phenolic formulations targeting high-value electronics and aerospace applications.

Key Developments

- In March 2025, BASF SE announced advancement of its bio-based phenolic resin development program, targeting lignin-derived substitutes for fossil-based phenol, aiming for commercial-scale production by 2027 under its sustainability strategy.

- In October 2024, Hexion LLC expanded its phenolic resin production capacity at its Louisville, Kentucky facility to meet growing demand from the North American engineered wood panel and construction insulation sectors.

- In June 2024, Sumitomo Bakelite Co. Ltd. launched a new range of ultra-low emission phenolic molding compounds specifically formulated for next-generation EV battery thermal management module applications across the Asia Pacific automotive supply chain.

Global Phenolic Resins Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 12.8 billion |

|

Current Market Value (2026) |

US$ 16.8 billion |

|

Projected Market Value (2033) |

US$ 23.8 billion |

|

CAGR (2026-2033) |

5.1% |

|

Leading Region |

Asia Pacific, 36% market share (2026) |

|

Dominant Product Type |

Novolac, ~43% market share (2026) |

|

Leading Application |

Wood Adhesives, ~38% market share (2026) |

|

Incremental Opportunity |

US$ 7.0 billion (2026-2033) |

Companies Covered in Phenolic Resins Market

- DIC Corporation

- Hexion LLC

- Chang Chun Plastics Co. Ltd.

- Mitsui Chemicals Inc.

- Georgia Pacific Chemicals LLC

- Prefere Resins

- Kolon Industries, Inc.

- SI Group

- Sumitomo Bakelite Co. Ltd

- BASF SE

- Hitachi Chemical Co. Ltd.

- Plastics Engineering Company

- RPM International Inc.

- KCC Corporation

- Altex Coatings Inc.

- Nippon Paint Marine Coatings Co., Ltd.

Frequently Asked Questions

The global phenolic resins market is estimated at US$ 16.8 billion in 2026, projected to reach US$ 23.8 billion by 2033 at a CAGR of 5.1%. Growth is driven by expanding construction activity, automotive lightweighting trends, and rising demand for phenolic resin-based laminates in the global electronics manufacturing supply chain.

Key growth drivers include the automotive industry's shift to lightweight phenolic composites and friction materials to comply with EU CO2 emission standards and U.S. CAFE regulations and expanding global wood panel production supported by sustained construction sector investment, particularly in emerging economies across Asia Pacific, the Middle East, and Africa.

Asia Pacific leads the global phenolic resins market, holding approximately 36% of global market share in 2026. The region's dominance is driven by China's large-scale wood panel manufacturing, Japan's and South Korea's advanced electronics industries, and India's rapidly growing construction and automotive sectors.

Key opportunities include the commercial scaling of bio-based and modified phenolic resin formulations, the fastest-growing segment at 7% CAGR, to meet regulatory demands for low-emission, sustainable materials, and growing demand for phenolic PCB laminates and semiconductor encapsulants driven by global electronics manufacturing capacity expansion, particularly across the Asia Pacific.

Leading companies in the global phenolic resins market include Hexion LLC, BASF SE, Sumitomo Bakelite Co. Ltd., SI Group, DIC Corporation, Mitsui Chemicals Inc., Chang Chun Plastics Co. Ltd., and Georgia Pacific Chemicals LLC.