- Industrial Machinery

- Refrigeration and Air Conditioning Compressors Market

Refrigeration and Air Conditioning Compressors Market Size, Share, and Growth Forecast, 2025 - 2032

Refrigeration and Air Conditioning Compressors Market By Product Type (Reciprocating, Screw, Centrifugal, Rotary, Scroll), Cooling Capacity (Less than 5 KW, Others), Refrigerant Type (R410A, R407C, Others), Application, and Regional Analysis for 2025 - 2032

Refrigeration and Air Conditioning Compressors Market Size and Trends Analysis

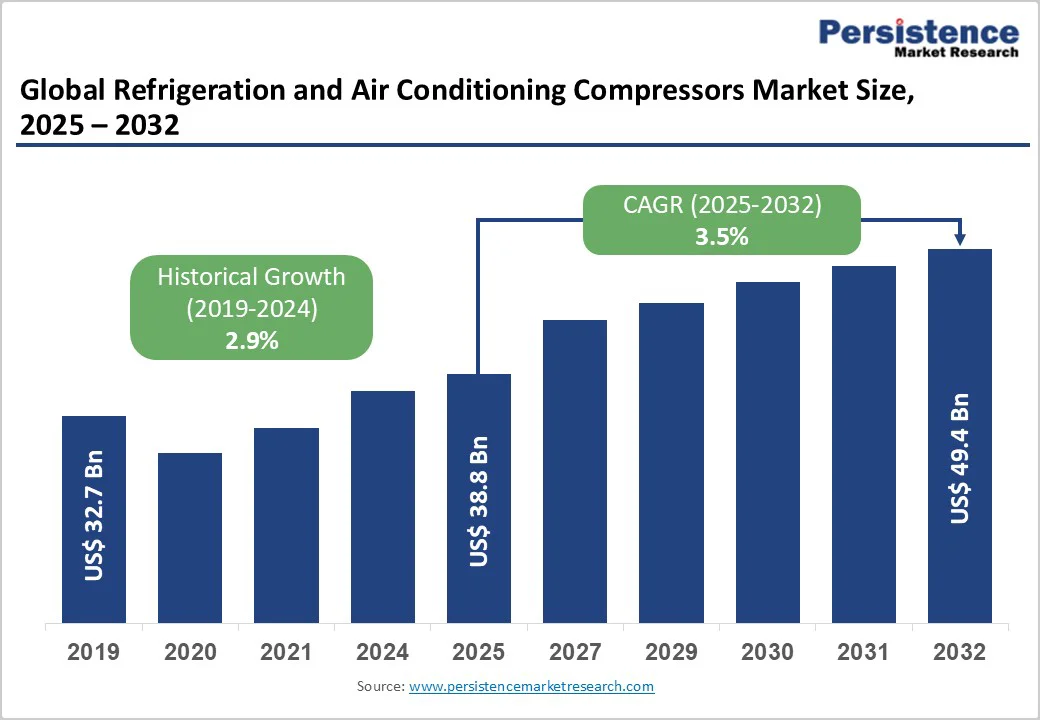

The global refrigeration and air conditioning compressors market size is likely to be valued at US$38.8 Billion in 2025 and is expected to reach US$49.4 Billion by 2032, growing at a CAGR of 3.5% during the forecast period from 2025 to 2032, driven by escalating demand for energy-efficient cooling solutions, rapid urbanization spurring residential air conditioning adoption, and expanding cold chain logistics infrastructure, particularly in Asia Pacific.

Key Industry Highlights:

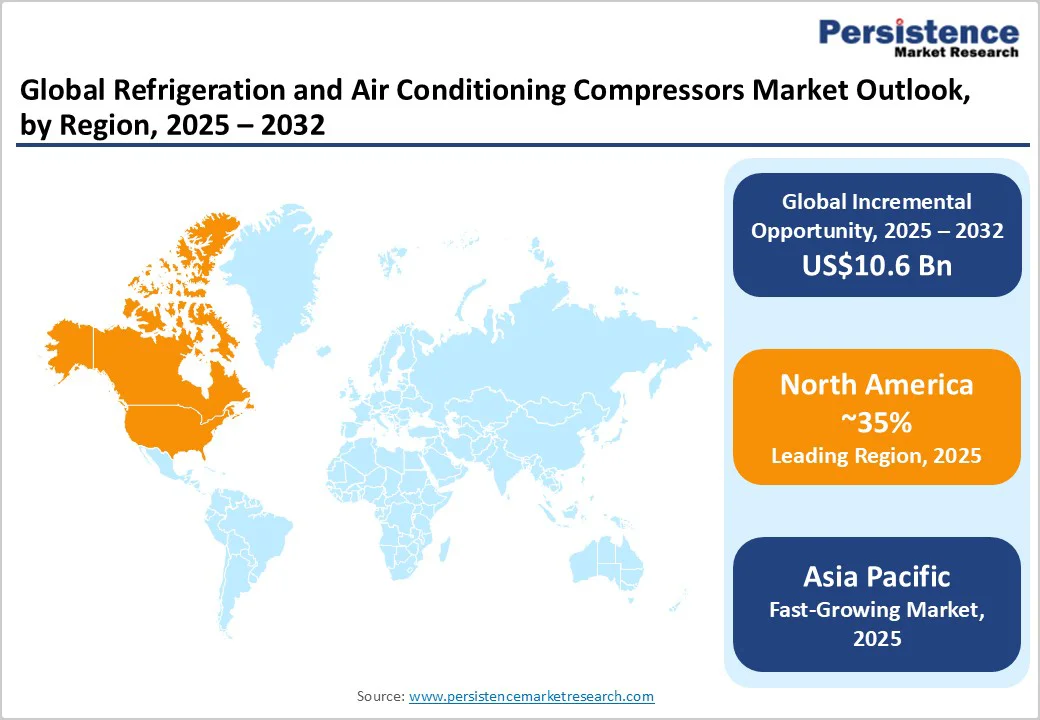

- Regional Leaders: North America emerges as the leading developed region with approximately 32% global market share in 2025, driven by stringent SEER energy efficiency standards, regulatory HFC phase-down compliance, and advanced manufacturing infrastructure.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing region through 2032, propelled by residential air conditioning penetration accelerating in China and India.

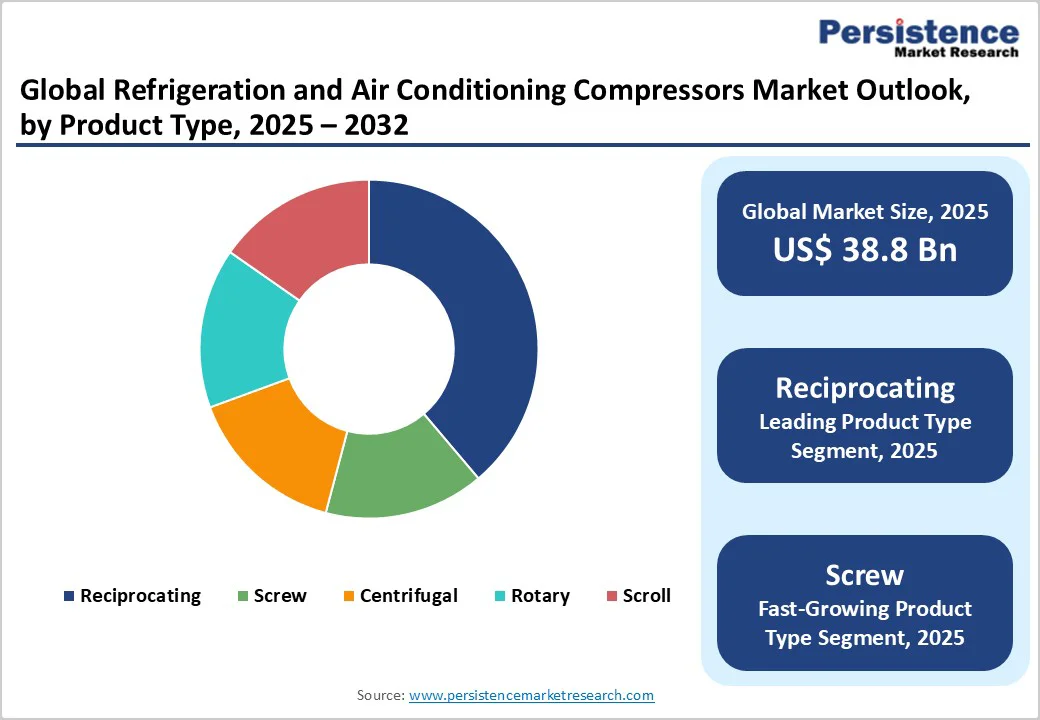

- Leading Product Type: Reciprocating compressors dominate product type with 59% market share in 2025, leveraging established reliability, proven serviceability, and broad applicability across residential, commercial, and industrial cooling capacity ranges from 1 kW household refrigerators to 500+ kW industrial systems.

- Fastest Growing Product Type: Scroll compressors represent the fastest-growing product segment, driven by superior energy efficiency, reduced noise operation, and expanding adoption in residential air conditioning and commercial refrigeration.

- Market Opportunity: The rapid proliferation of electric vehicles (EVs) is creating significant growth opportunities for advanced compressor technologies.

| Report Attribute | Details |

|---|---|

|

Refrigeration and Air Conditioning Compressors Market Size (2025E) |

US$38.8 Bn |

|

Projected Market Value (2032F) |

US$49.4 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

3.5% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

2.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis

Regulatory Transition to Low-GWP Refrigerants and Energy-Efficient Technologies

Global refrigeration and air conditioning compressor demand is experiencing substantial acceleration driven by regulatory mandates targeting the phase-down of high global warming potential (HFC) refrigerants. The U.S. Environmental Protection Agency (EPA), under the American Innovation and Manufacturing (AIM) Act, has implemented progressive restrictions on high-GWP HFC refrigerants, including R410A, R404A, and R134A, with production phase-down targets of 85% by 2036. The European Union's F-Gas Regulation similarly mandates reductions, creating approximately 40% quota reductions by 2018 and 2030 targets of 19% of baseline.

These regulatory frameworks are compelling manufacturers to develop compressors compatible with low-GWP alternatives such as R290 (propane), R744 (carbon dioxide), and R32. Industry data indicate that approximately 60% of compressor design upgrades globally are now driven by low-GWP refrigerant compliance requirements. Technological innovations, including inverter-driven scroll compressors, digital scroll technology with variable speed capabilities, and enhanced efficiency metrics, are enabling manufacturers to meet stringent regulatory timelines while simultaneously improving energy consumption metrics, thereby supporting sustained market expansion through 2032.

Rapid Urbanization and Rising Cooling Demand in Emerging Economies

Emerging economies across Asia Pacific, Latin America, and Africa are experiencing unprecedented urbanization rates and expanding middle-class populations requiring residential cooling infrastructure. According to United Nations projections, approximately 68% of the global population will reside in urban areas by 2050, compared to 55% in 2018. In China, urban population growth coupled with rising disposable incomes has driven residential air conditioning penetration from 45% of households in 2015 to over 72% by 2024. India's burgeoning middle class, projected to expand by 250 million individuals by 2030, is creating explosive demand for residential cooling systems, with air conditioning ownership expected to grow at 15-20% annually.

Commercial refrigeration infrastructure expansion in supermarkets, cold storage facilities, and pharmaceutical warehousing is concurrently accelerating compressor demand. The Asia Pacific Cold Chain Logistics Market is projected to expand at a 15% CAGR through 2032, driven by e-commerce growth in food delivery and pharmaceutical distribution requiring reliable temperature-controlled infrastructure. Compressor manufacturers are ramping up capacity in high-growth regions to capitalize on this sustained demand expansion.

Barrier Analysis - Supply Chain Disruptions and Refrigerant Availability Constraints

The compressor industry faces significant headwinds from refrigerant supply disruptions exacerbated by the transition toward low-GWP alternatives. Historical HFC refrigerant production quotas were deliberately reduced by major producing nations, creating supply bottlenecks for R410A, R404A, and R134A between 2021 and 2023, with price increases reaching 400-600% compared to historical baselines. Manufacturers utilizing legacy refrigerants for existing equipment stock face escalating procurement costs and extended delivery timelines, constraining margins, particularly for smaller compressor producers.

The manufacturing infrastructure for emerging low-GWP refrigerants remains geographically concentrated, predominantly in China, India, and select North American facilities, creating supply chain vulnerabilities and dependency risks. Regulatory restrictions on the disposal of high-pressure refrigerant cylinders, effective from 2025 onward per EPA guidelines, are imposing additional compliance burdens on manufacturers and compounding operational complexity.

Opportunity Analysis

Electrification of Transportation and Electric Vehicle Thermal Management Expansion

The rapid proliferation of electric vehicles (EVs) is creating significant growth opportunities for advanced compressor technologies, particularly electronic compressors optimized for battery thermal management and cabin climate control. Global EV sales exceeded 14 million units in 2024, representing a 25% year-on-year increase, with projections exceeding 50 million units annually by 2032. Unlike conventional internal combustion engine vehicles, EVs require independent electronic compressors that operate continuously regardless of engine status, as they cannot leverage waste engine heat for cabin warming during cold months.

Innovations, including variable capacity electronic compressors, heat pump systems utilizing R744 refrigerant cascades, and battery thermal management integration, represent significant value-add opportunities for manufacturers developing EV-specific compressor solutions. Collaborations between compressor manufacturers and automotive OEMs, including Tesla, BMW, and Mercedes-Benz, are accelerating adoption and technology refinement, positioning specialized compressor suppliers for substantial market share capture in the high-growth electrified vehicle segment.

Development of Smart HVAC Systems and IoT-Enabled Compressor Integration

Intelligent HVAC systems incorporating advanced compressor controls, machine learning algorithms, and real-time performance monitoring represent emerging opportunities capturing premium pricing and expanded addressable markets. Smart compressor systems with variable speed drive technology, digital scroll modulation, and predictive maintenance algorithms can reduce energy consumption by 20-30% compared to fixed-speed alternatives, aligning with stringent energy efficiency regulations mandating compliance with SEER (Seasonal Energy Efficiency Ratio) standards of 16+ in North America and equivalent European benchmarks.

Integration of IoT sensors enabling remote monitoring, predictive failure detection, and automated maintenance scheduling extends equipment service life and optimizes operational efficiency. Leading manufacturers, including Daikin Industries, Carrier Global, and Emerson Electric, are investing in AI-driven diagnostic platforms and cloud-connected compressor management systems. Developing nations' adoption of smart building infrastructure, supported by government incentives and sustainability mandates, creates substantial opportunities for compressor manufacturers developing cost-effective, scalable IoT integration solutions.

Category-wise Analysis

Product Type Insights

Reciprocating compressors dominate the market with approximately 59% share in 2025, reflecting their established market position across residential, commercial, and industrial refrigeration applications. Reciprocating compressors offer exceptional versatility, enabling deployment across diverse cooling capacities from 1 kW household refrigerators to 500+ kW industrial freezing systems. Their straightforward mechanical design, ease of maintenance, and established global supply chains have sustained market leadership despite emerging alternatives.

Scroll compressors are experiencing accelerated adoption at the highest CAGR, driven by superior energy efficiency, reduced noise operation below 70 dB, and compact designs suitable for residential and light commercial systems. Variable frequency drive (VFD) technology integration enhances scroll compressor attractiveness, enabling modulation across operating conditions and reducing energy waste during partial-load scenarios.

Cooling Capacity Analysis

The 5 to 30 kW cooling capacity leads market demand with approximately 39% share, representing the optimal capacity range for residential air conditioning units, small commercial refrigeration installations, and residential freezers. This segment's market dominance reflects the global residential housing stock of approximately 1.8 billion units, with accelerating air conditioning penetration in developing regions.

The 100-300 kW segment is projected to experience the fastest growth at the highest CAGR through 2032, propelled by commercial refrigeration infrastructure expansion in ASEAN nations, Latin America, and sub-Saharan Africa.

Refrigerant Type Insights

R410A refrigerant-compatible compressors hold around 42% of the market share in 2025, largely due to their long-standing use in residential and light commercial air conditioning systems since their introduction in 2002 as a replacement for older, ozone-depleting refrigerants such as R22. R410A became the industry standard as its high energy efficiency, non-ozone-depleting nature, and compatibility with modern HVAC technologies.

Regulatory bodies such as the U.S. Environmental Protection Agency (EPA) and international frameworks such as the Kigali Amendment are now enforcing stricter phasedown schedules for high-GWP (Global Warming Potential) refrigerants. Under these rules, R410A production and import quotas are expected to decline by 70% from baseline levels by 2029, pushing manufacturers and end-users to shift toward next-generation, low-GWP refrigerants such as R32 and R454B. This transition marks a significant technological and environmental shift in the compressor market, encouraging innovation in system design, energy efficiency, and sustainability while reshaping long-term demand dynamics.

Application Insights

Residential cooling applications dominate market consumption with approximately 67% share, reflecting global housing stock cooling needs, rising temperatures from climate change, and accelerating air conditioning penetration in emerging economies. Data from United Nations development programs indicate that residential air conditioning units are expanding at approximately 8% annually in Asia Pacific, Latin America, and Middle East regions, directly proportional to electricity infrastructure development and household income growth.

Commercial refrigeration applications, including supermarkets, food service establishments, and specialty retail, are projected to grow at the highest CAGR through 2032. Expanding retail infrastructure in developing economies, cold chain modernization initiatives, and food safety regulatory compliance are driving commercial segment expansion.

Regional Insights

North America Refrigeration and Air Conditioning Compressors Market Trends

North America maintains a substantial market presence driven by advanced manufacturing infrastructure, stringent energy efficiency regulations, and technology leadership in compressor innovation. The U.S. compressor market was valued at approximately US$4.3 Billion in 2024, with residential air conditioning and commercial refrigeration representing approximately 75% of demand.

Canadian and Mexican markets are experiencing complementary growth driven by construction industry expansion, industrial manufacturing facility upgrades, and cold chain infrastructure development supporting pharmaceutical and specialty food distribution. Smart building trends in Canada are driving the adoption of IoT-enabled compressors with predictive maintenance capabilities, representing emerging profit center opportunities for manufacturers offering integrated control platform solutions.

Europe Refrigeration and Air Conditioning Compressors Market Trends

Europe represents a mature but technologically sophisticated market emphasizing regulatory compliance, energy efficiency optimization, and environmental sustainability. The European Union's F-Gas Regulation mandates achieving 80%+ reductions in HFC refrigerant use by 2036, creating accelerated demand for low-GWP compressor alternatives and driving technology differentiation among manufacturers. Germany, representing Europe's largest industrial base, accounted for approximately 28% of regional compressor consumption in 2024.

France and the U.K. markets are experiencing steady growth in commercial refrigeration modernization, driven by food safety compliance and energy cost reduction initiatives. Spain's industrial refrigeration sector is expanding at approximately 4% annually, supported by agricultural product processing and pharmaceutical cold chain infrastructure development.

Asia Pacific Refrigeration and Air Conditioning Compressors Market Trends

Asia Pacific emerges as the fastest-growing regional market with sustained 6.2% growth rates through 2032, propelled by urbanization, middle-class expansion, and cold chain logistics infrastructure development. China dominates regional consumption, accounting for approximately 48% of Asia Pacific demand, supported by residential air conditioning penetration accelerating from approximately 40% of urban households in 2015 to projected 85%+ by 2032.

India represents the highest-growth market with air conditioning demand expanding 8% annually in urban areas, driven by government initiatives and private sector investments in residential and commercial infrastructure. Tata Chemicals and emerging Indian compressor manufacturers are establishing local production capacity, addressing residential and light commercial segments, while multinational suppliers, including Daikin Industries and Johnson Controls, are establishing regional manufacturing hubs in Pune and Delhi.

Competitive Landscape

The global refrigeration and air conditioning compressors market is moderately consolidated, with the top 10 players holding 60–65% share. Leaders such as Daikin, Carrier, Emerson, and Johnson Controls compete through technology innovation, geographic expansion, and vertically integrated system solutions.

Japanese firms such as Daikin and Mitsubishi Electric excel in inverter and efficiency technologies, while Carrier and Emerson benefit from strong distribution and aftermarket ecosystems. Rising competitors, including Gree and Midea, scale rapidly with cost-efficient manufacturing exceeding 3 million units annually. Key differentiation centers on low-GWP refrigerants, variable-speed drives, IoT monitoring, and noise-reduction features.

Recent Industry Developments

- In January 2025, Wacker Chemie AG announced US$100 Million investments in U.S. polysilicon production capacity, supporting electronic compressor manufacturing for electric vehicle thermal management applications with enhanced R744 refrigerant system integration.

- In November 2024, Daikin Industries and Copeland Partnership announced a joint venture to introduce Daikin's inverter swing rotary compressor technology to the U.S. residential HVAC market, addressing energy efficiency and low-GWP refrigerant requirements through advanced capacity modulation and variable speed control technologies.

- In September 2024, Evonik and Specialty Gas Collaboration expanded compressor manufacturing compatibility across low-GWP refrigerant platforms through enhanced catalyst development supporting R290 and R744 safe handling protocols in compressor design specifications.

Companies Covered in Refrigeration and Air Conditioning Compressors Market

- Daikin Industries, Ltd.

- Carrier Global Corporation

- Emerson Electric Co.

- Mitsubishi Electric Corporation

- Johnson Controls International plc

- LG Electronics Inc.

- Panasonic Corporation

- Danfoss A/S

- Hitachi Ltd.

- Samsung Electronics Co., Ltd.

- Tecumseh Products Company

- Bitzer SE

- Copeland (Emerson subsidiary)

- Gree Electric Appliances Inc.

- Midea Group Co., Ltd.

- Atlas Copco AB

- Sanden Holdings Corporation

- Hanon Systems

- Secop GmbH

- Bristol Compressors International

Frequently Asked Questions

The global refrigeration and air conditioning compressors market was valued at US$38.8 Billion in 2025 and is projected to reach US$49.4 Billion by 2032, growing at a 3.5% CAGR during the forecast period.

The primary drivers for the refrigeration and air conditioning compressors market include rising global demand for energy-efficient cooling systems, expanding cold chain logistics, and growing residential and commercial HVAC installations.

Reciprocating compressors hold a commanding 59% market share in 2025, underscoring their strong presence and widespread use across residential, commercial, and industrial refrigeration systems.

North America leads the refrigeration and air conditioning compressors market with a 32% market share, supported by strong demand for high-efficiency HVAC systems, extensive commercial refrigeration usage, and ongoing technological upgrades across the U.S. and Canada.

Major opportunities include rising demand for energy-efficient and low-GWP compressor technologies and rapid expansion of cold chain logistics, e-commerce food delivery, and HVAC modernization across emerging markets.

The leading companies in the refrigeration and air conditioning compressors market include Daikin Industries, Ltd., Carrier Global Corporation, Emerson Electric Co., Mitsubishi Electric Corporation, Johnson Controls International plc, LG Electronics Inc., and Panasonic Corporation.