- Industrial Machinery

- Refrigeration Compressor Market

Refrigeration Compressor Market Size, Share, and Growth Forecast 2025 - 2032

Refrigeration Compressor Market By Compressor Type (Reciprocating Compressor, Others), Motor Type (Fixed, Variable), Application (Refrigerator & Freezer), Sales Channel, and Regional Analysis for 2025 - 2032

Refrigeration Compressor Market Size and Trends Analysis

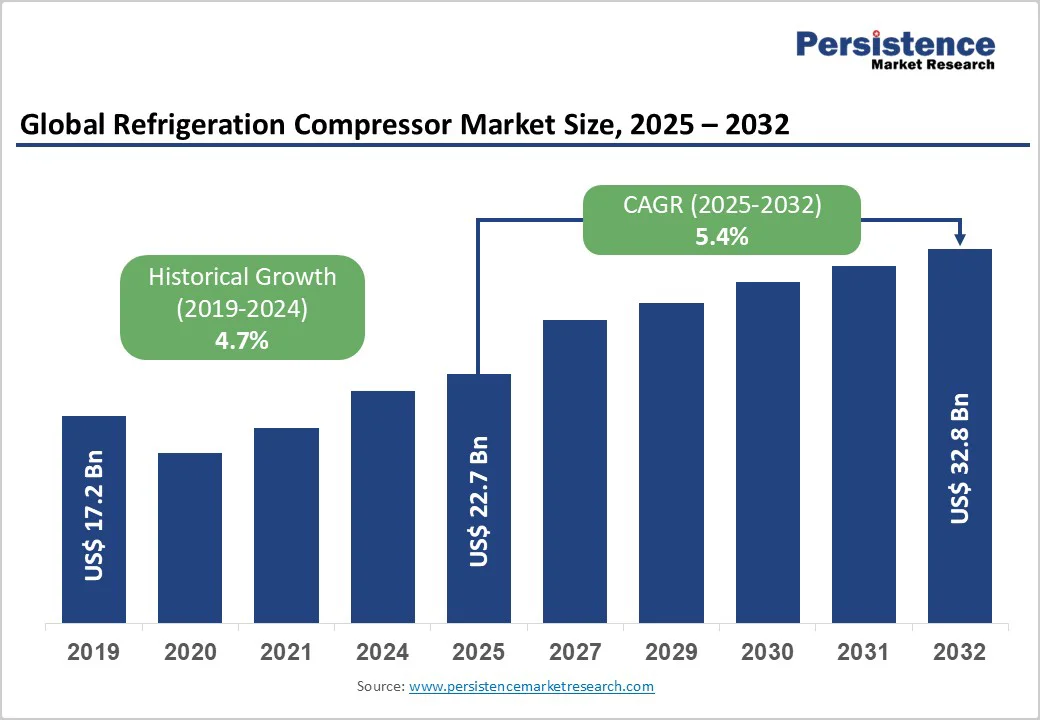

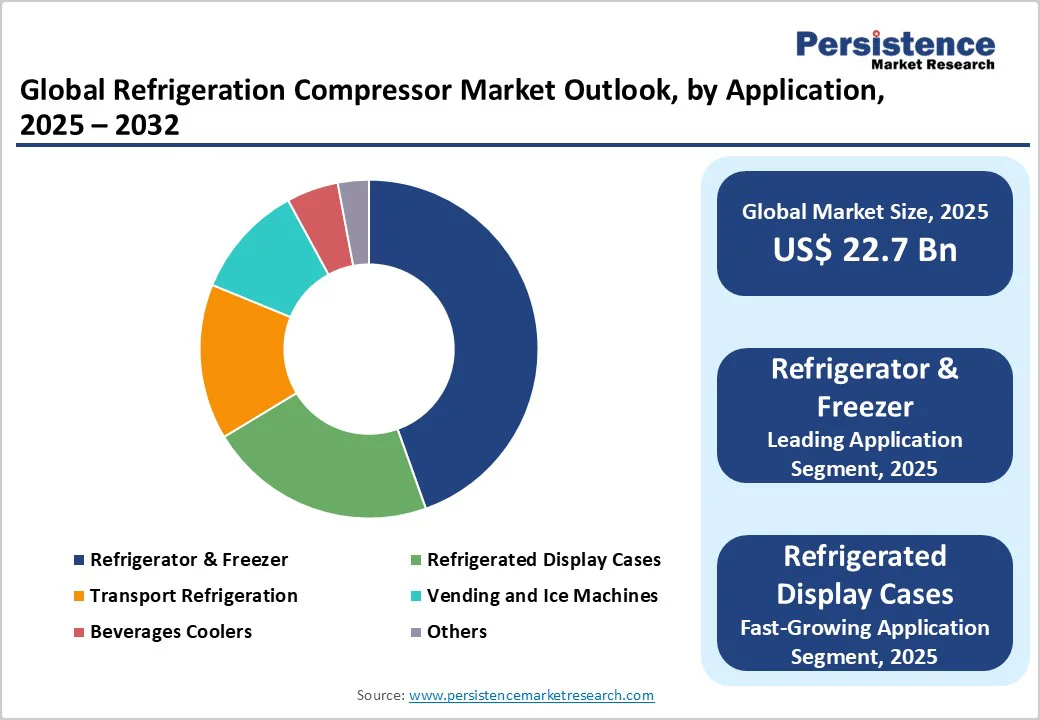

The global refrigeration compressor market size was valued at US$22.7 Billion in 2025 and is projected to reach US$32.8 Billion by 2032, growing at a CAGR of 5.4% during the forecast period from 2025 to 2032, driven by increasing demand for energy-efficient cooling solutions in commercial refrigeration equipment and the rising adoption of variable-speed compressors in HVAC systems to meet stringent regulatory efficiency norms.

Escalating cold chain requirements for food and pharmaceuticals, coupled with growth in liquid-cooled data centers and the burgeoning electric vehicle sector, further bolster market growth and incentivize technological innovation.

Key Industry Highlights

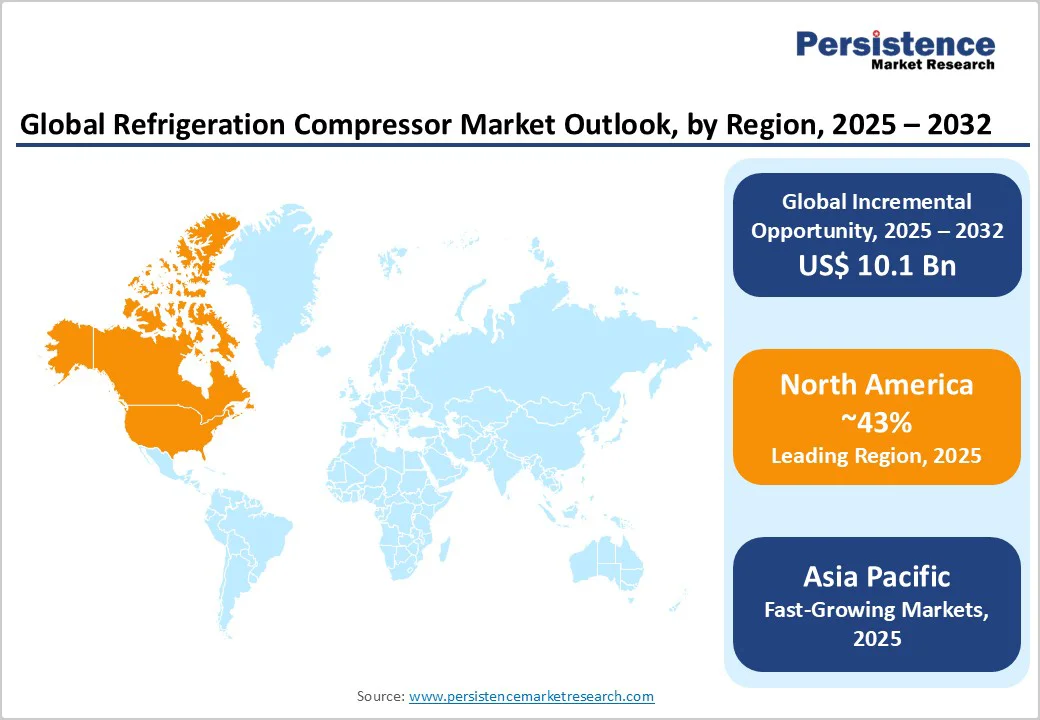

- Leading Region: North America leads the global market, driven by a mature commercial refrigeration sector and stringent energy efficiency regulations that are accelerating the adoption of advanced variable-speed compressors.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a projected CAGR of 7.1%, propelled by rising appliance penetration, cold-chain expansion, and significant manufacturing growth in China and India.

- Leading Compressor Type Segment: Reciprocating compressors dominate the market with a 38% share, valued for their cost-effectiveness and proven robustness in small-scale refrigeration and appliance applications.

- Leading Motor Type Segment: The variable-speed motor segment is showing the fastest growth, with a CAGR of 8.4%, driven by global efficiency mandates and increasing incentives for retrofitting older systems.

- Key Market Opportunity: Smart, IoT-enabled compressors represent the key market opportunity, enabling predictive maintenance services and advanced lifecycle management, thereby unlocking valuable recurring revenue streams for manufacturers.

| Key Insights | Details |

|---|---|

|

Refrigeration Compressor Size (2025E) |

US$22.7 Bn |

|

Market Value Forecast (2032F) |

US$32.8 Bn |

|

Projected Growth CAGR (2025-2032) |

5.4% |

|

Historical Market Growth (2019-2024) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Stricter Energy Efficiency Regulations Driving Variable-Speed Adoption

Stringent global energy efficiency regulations are accelerating the adoption of variable-speed refrigeration compressors. Policies such as the U.S. Department of Energy efficiency mandates and the EU F-Gas Regulation have compelled manufacturers to move away from traditional fixed-speed compressors toward inverter-driven, variable-speed technology. These compressors adjust motor speed to match precise cooling demands, reducing energy consumption by up to 30% and lowering operational costs for end users.

The shift is particularly notable in commercial refrigeration applications, including supermarkets, restaurants, and large cold storage facilities, where total cost of ownership and energy efficiency are critical considerations. Adoption rates for variable-speed compressors rose from 12% in 2019 to an estimated 28% in 2024, reflecting significant OEM investments in advanced technologies. Beyond cost savings, this transition supports global carbon-reduction targets, incentivizes retrofits and new installations, and establishes variable-speed compressors as a cornerstone of energy-efficient refrigeration solutions.

Growth of Cold Chain Infrastructure for Pharmaceuticals and Food

The rapid expansion of the global cold chain sector is a major driver of refrigeration compressor demand. Rising vaccine distribution networks, the growth of perishable e-commerce, and stringent temperature-control requirements have driven demand for high-reliability compressors for refrigerated display units, transport refrigeration, and mobile refrigeration systems. The refrigerated truck fleet segment alone has grown at a global CAGR of 5.9%, supporting the mobile refrigerator market, which exceeded US$3.2 billion in 2023.

Technological advancements, including compact and mobile compressor designs, have enabled seamless integration into trailers and containers, ensuring product integrity and safety across temperature-sensitive supply chains. To meet these requirements, compressor suppliers are increasingly partnering with third-party logistics (3PL) providers to deliver turnkey refrigeration solutions. This trend reinforces compressors as essential components in pharmaceutical, food, and perishable goods logistics, driving sustained market growth and innovation.

Barrier Analysis - High Initial Investments and Retrofit Costs for Advanced Compressors

Although variable-speed and scroll compressors deliver substantial long-term energy savings, their upfront costs are 25–40% higher than conventional reciprocating models. This price premium limits adoption among small-scale end users and in emerging markets, where capital expenditure is constrained. Retrofitting existing refrigeration systems further adds complexity, often requiring redesigning control architectures, upgrading electrical infrastructure, and incurring extended downtime.

These factors increase labor and operational costs, slowing modernization, particularly for local retailers and independent cold storage operators. The combination of high initial investments and retrofit challenges remains a key barrier to widespread deployment of advanced compressor technologies, slowing the transition toward energy-efficient and sustainable refrigeration solutions in cost-sensitive market segments.

Limited Availability and Technical Challenges of Low-GWP Refrigerants

The shift to low-global-warming-potential (GWP) refrigerants such as R-290 and hydrofluoroolefins faces significant technical and regulatory hurdles. Flammable refrigerants, such as propane, require redesigns of compressors with higher pressure ratings, specialized materials, and strict adherence to safety standards such as UL 60335 and EN 378.

These requirements increase design complexity, extend certification timelines by up to 18 months, and raise research and development costs. As a result, the adoption of next-generation, eco-friendly compressors is slower than expected, despite regulatory mandates to phase out high-GWP refrigerants. Limited availability and technical challenges of low-GWP refrigerants thus remain major restraints on market growth.

Opportunity Analysis - Expansion in Electric Vehicle Refrigeration and Battery Cooling

The electrification of the global transport sector is driving a strong demand for compact, high-efficiency refrigeration compressors. These systems are critical not only for passenger comfort but also for battery thermal management in electric buses, trucks, and cars. With the global electric bus fleet surpassing 650,000 units in 2024 and growing over 20% annually, each vehicle requires dedicated cooling to maintain battery performance, safety, and longevity.

Manufacturers are adapting scroll and rotary compressor designs for high-voltage DC integration, incorporating brushless motor drives to reduce electromagnetic interference. Strategic collaborations with EV OEMs and thermal system integrators create high-growth opportunities, enabling suppliers to capitalize on the rapidly expanding automotive refrigeration equipment market while supporting the transition to electrified and sustainable transport solutions.

Integration of IoT-Enabled Smart Compressors for Predictive Maintenance

IoT integration is transforming refrigeration compressors into smart, connected devices capable of predictive maintenance. Embedded sensors monitor vibration, temperature, oil levels, and other performance parameters, enabling analytics that can reduce unplanned downtime by up to 35% and extend equipment life by 20%.

OEMs are increasingly partnering with cloud platform providers to offer subscription-based monitoring services, generating recurring revenue beyond hardware sales. The use of digital twins for performance simulation accelerates R&D, optimizes lifecycle management, and improves customer satisfaction. These innovations allow proactive issue resolution, enhanced system efficiency, and more reliable operations, making IoT-enabled compressors a high-value solution in commercial, industrial, and mobile refrigeration applications.

Category-wise Analysis

Compressor Type Insights

Reciprocating compressors remain the largest segment in 2025, holding an estimated 38% share due to their reliability, cost-effectiveness, and ease of maintenance. They are widely used in residential refrigerators, small freezers, ice machines, and vending machines, where upfront cost and dependable long-term performance are critical.

Scroll compressors, however, are the fastest-growing type with a CAGR of 6.2%, reaching 22% market share by 2024. Their energy efficiency, compact design, and low noise and vibration levels make them increasingly preferred in mid-range commercial HVAC and refrigeration systems, where performance, operational efficiency, and lower lifecycle costs are key purchasing considerations.

Motor Type Insights

Fixed-speed compressors dominate the market with a 62% share, valued for their simplicity, reliability, and cost-effectiveness in residential and light commercial applications. Variable-speed compressors, growing at a CAGR of 8.4%, are rapidly gaining traction due to energy efficiency and precise temperature control advantages.

By 2024, variable-speed adoption reached 28%, supported by integrated inverter modules that allow easier retrofitting with minimal downtime. This reflects an industry-wide trend toward energy optimization and advanced cooling solutions in both commercial and industrial sectors.

Application Insights

The refrigerator & freezer segment leads compressor demand with approximately 45% of the market, driven by household penetration in emerging economies and regular replacement cycles in mature regions. Refrigerated display cases follow at 18%, fueled by modern retail expansion, convenience stores, and supermarkets investing in energy-efficient merchandisers.

Transport refrigeration and beverage coolers each hold roughly 12%, reflecting growth in perishable logistics and retail beverage markets. Vending and ice machines account for 8%, while specialty applications such as medical, laboratory, and data center cooling are included in the "Others" category, highlighting RCA’s diverse usage across consumer and commercial refrigeration.

Sales Channel Insights

The OEM channel dominates with a 74% share, supplying compressors directly to refrigerator, HVAC, and transport refrigeration equipment manufacturers. This ensures product integration at production lines and maintains a streamlined supply chain.

The aftermarket segment accounts for 26% of sales, driven by maintenance, repair, and overhaul services. Extended service life programs and third-party remanufacturing support cost-effective component replacements, enabling end-users to prolong equipment lifespans and enhancing the overall market sustainability.

Regional Insights

North America Refrigeration Compressor Market Trends

North America leads the global refrigeration compressor market, driven primarily by strict energy efficiency regulations enforced by the U.S. Department of Energy (DOE) and the EPA’s SNAP program. These policies are phasing down high-GWP refrigerants while mandating substantial efficiency improvements, compelling manufacturers to adopt advanced compressor technologies. The mature commercial refrigeration sector, valued at US$13.9 Billion in 2024, emphasizes low-energy solutions to reduce operational costs, with major retail chains actively deploying variable-speed compressors to achieve annual energy savings of 15–20%.

The region’s innovation ecosystem, anchored in tech hubs such as Silicon Valley and Boston, fosters cutting-edge R&D in compressor design, including AI-driven control systems and magnetic bearing technologies for ultra-low friction performance. These technological advancements, combined with stringent regulations, reinforce North America’s position as a market leader. The adoption of smart, energy-efficient compressors is expected to remain a key growth driver across commercial, industrial, and transport refrigeration applications.

Europe Refrigeration Compressor Market Trends

Europe is the second-largest refrigeration compressor market, shaped by the ambitious EU F-Gas Regulation, which targets a 79% reduction in GWP-weighted refrigerant use by 2030. Leading markets, including Germany, France, the U.K., and Spain, account for over 60% of regional demand. Germany’s automotive and transport sectors are particularly significant consumers of truck and trailer cooling compressors, while inverter-driven compressors captured 35% of new household refrigerator installations in 2024, highlighting the shift toward energy-efficient solutions.

Regulatory harmonization across EU member states simplifies product approvals and encourages innovation. Directives such as EcoDesign continue to push OEMs to deliver high-efficiency compressors that meet both commercial and consumer requirements. Combined with strong industrial infrastructure and a focus on sustainability, these trends are fostering the adoption of advanced technologies, including variable-speed and smart compressors, across Europe’s commercial and residential refrigeration markets.

Asia Pacific Refrigeration Compressor Market Trends

Asia Pacific is the fastest-growing refrigeration compressor market, projected to expand at a CAGR of 7.1%, driven by rapid industrialization, urbanization, and rising household appliance penetration. China, accounting for around 40% of global compressor production in 2024, dominates both domestic appliance manufacturing and cold-chain logistics. India’s refrigerator penetration has surpassed 80% in urban areas, creating strong demand for residential compressors, while ASEAN countries such as Vietnam and Thailand are emerging as key manufacturing hubs due to lower production costs.

The region’s growth is further supported by expanding mobile refrigeration markets, requiring compact, high-efficiency scroll and rotary compressors for refrigerated transport. Investments by major OEMs in advanced production facilities, coupled with the rising demand for energy-efficient solutions in commercial and industrial applications, are driving significant market expansion. Asia Pacific’s dynamic economies and supportive industrial policies position it as a critical growth region for global refrigeration compressors.

Competitive Landscape

The global refrigeration compressor market is moderately consolidated, with leading manufacturers controlling a significant portion of production capacity. These companies differentiate themselves through vertical integration, providing complete solutions that include compressors, refrigerants, and electronic controls. Heavy investments in R&D focuses on developing compatibility with low-GWP refrigerants, energy-efficient designs, magnetic bearing technology, and oil-free compressors that reduce maintenance requirements.

Emerging regional players are increasing competition by offering cost-effective and customized solutions tailored to local markets. Strategic collaborations with commercial refrigeration equipment manufacturers and aftermarket service providers are essential for strengthening market presence, expanding distribution networks, and enhancing long-term competitiveness.

Key Industry Developments

- In March 2024, Emerson Electric Co. launched its Copeland Scroll UltraTech compressors, compatible with R-32, R-454B, and R-410A refrigerants. These compressors provide up to 18% higher energy efficiency, supporting next-generation low-GWP refrigeration and heat pump applications.

- In September 2025, Danfoss inaugurated its largest global manufacturing facility in Haiyan, China, integrating production for all three business segments. The facility enhances variable-speed compressor capacity and supports green transition initiatives across the Asia Pacific region.

Companies Covered in Refrigeration Compressor Market

- Emerson Electric Co.

- Danfoss

- Tecumseh Products Company

- Mitsubishi Electric Corporation

- LG Electronics

- Samsung Electronics

- Panasonic Corporation

- Embraco

- Bitzer

- Frascold

- Dorin

- Fusheng

- Huayi Compressor Barcelona

- Highly

- Rechi Precision

Frequently Asked Questions

The refrigeration compressor market size is projected to reach a value of US$32.8 Billion by 2032, expanding from US$22.7 Billion in 2025 at a CAGR of 5.4%.

The primary drivers are stringent global energy efficiency regulations that favor advanced technologies and the significant expansion of cold chain infrastructure required for the food & pharmaceutical industries.

Reciprocating compressors continue to lead the market with an estimated 38% share, favored for their robustness and cost-effectiveness in small-capacity and residential refrigeration applications.

North America currently leads the market, a position supported by its mature commercial refrigeration sector and demanding energy regulations that accelerate the adoption of high-efficiency compressor technologies.

The integration of IoT and smart technologies into compressors to enable predictive maintenance services represents a key opportunity, allowing manufacturers to create new, recurring revenue streams and enhance customer value.

Key global players include Emerson Electric Co. (with its Copeland brand), Danfoss, Tecumseh Products Company, Mitsubishi Electric Corporation, LG Electronics, Samsung Electronics, and Panasonic Corporation.