- Non-food Packaging

- Pump and Dispenser Market

Pump and Dispenser Market Size, Share, and Growth Forecast, 2026 - 2033

Pump and Dispenser Market By Product Type (Lotion Pumps, Foam Pumps, Others), Material Type (Plastic, Metal, Others), Technology, End-user Industry, and Regional Analysis for 2026 - 2033

Pump and Dispenser Market Size and Trends Analysis

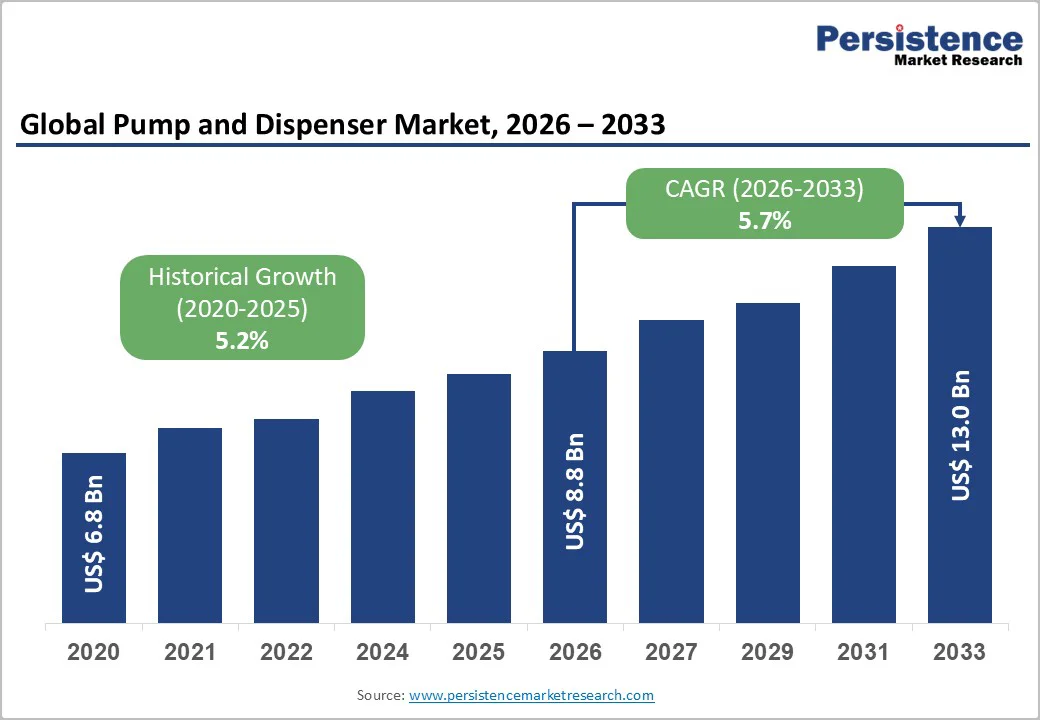

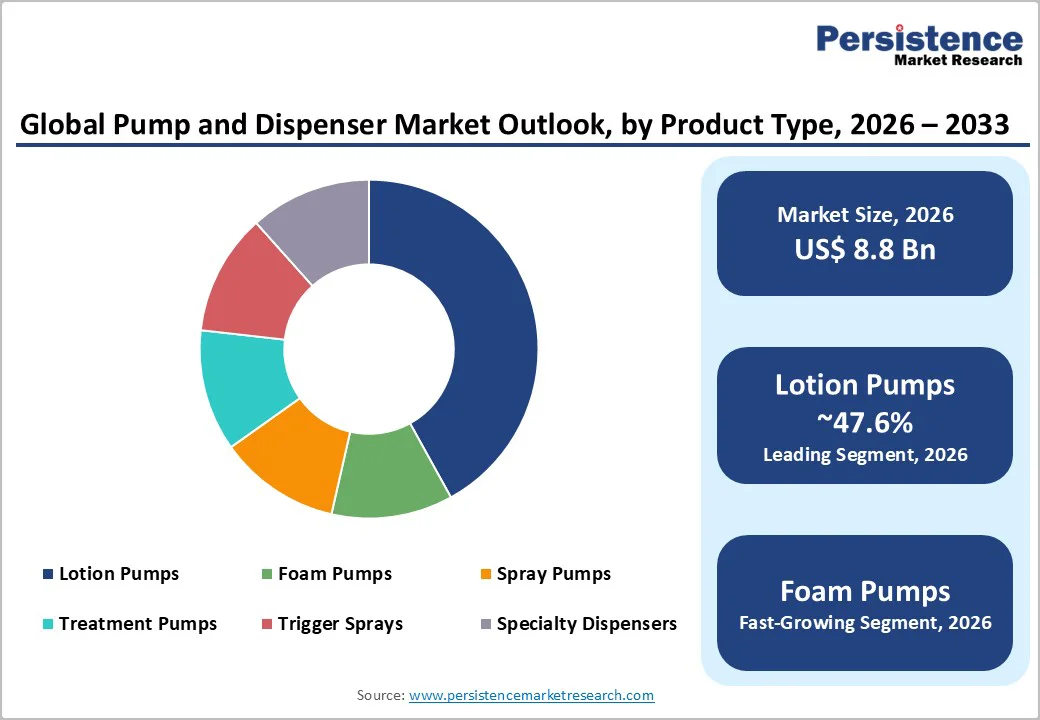

The global pump and dispenser market size is likely to be valued at US$8.8 billion in 2026. It is expected to reach US$13.0 billion by 2033, growing at a CAGR of 5.7% from 2025 to 2032, driven by rising personal-care consumption, the rapid integration of recyclable and PCR materials, and accelerating innovation in airless, soft-actuation, and precision-dosing technologies.

The shift toward premium packaging formats, refill models, and e-commerce-optimized dispensing systems reinforces stable mid-single-digit growth. Regulatory pressure for circularity, strengthening procurement standards, and manufacturing upgrades among global suppliers also support long-term expansion.

Key Industry Highlights

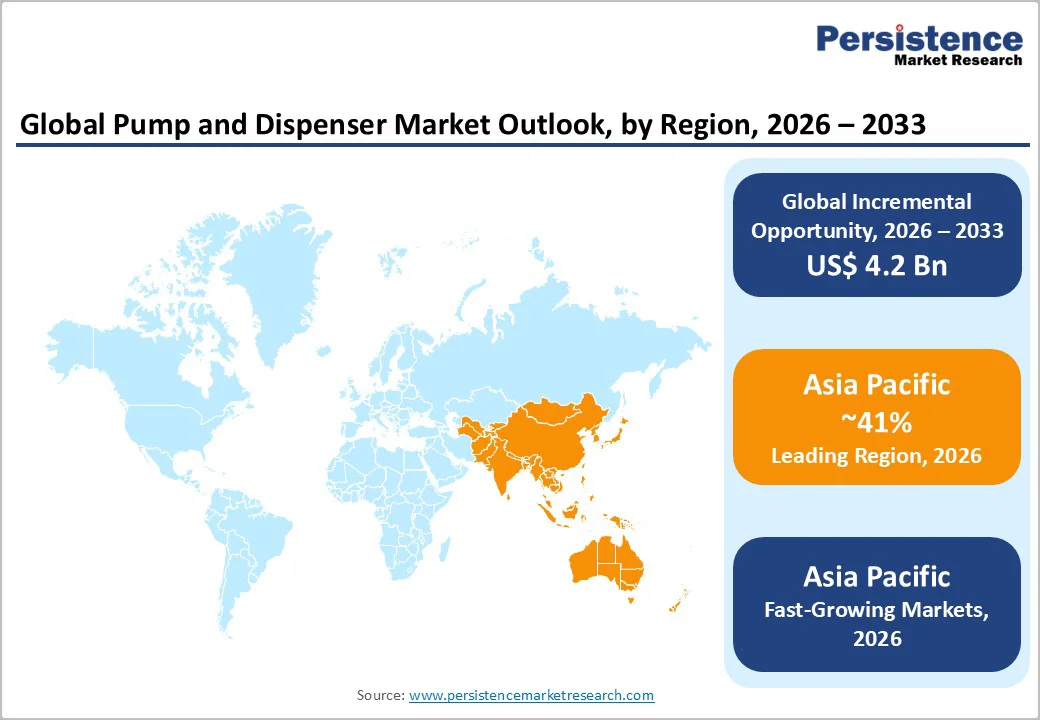

- Leading Region: Asia Pacific, contributing an estimated 41% of global market value in 2026, driven by large-scale personal care manufacturing, strong export capacity, and cost-efficient pump and dispenser production hubs.

- Fastest-growing Region: Asia Pacific leads with the highest projected growth, due to rising consumption of personal hygiene, skincare, and home-care formulations.

- Investment Plans: Global manufacturers are increasing capacity investments in injection molding, metal stamping, PCR integration, and mono-material technologies, with capital expenditure rising by an estimated 18 percent from 2024 to 2026 across key Asia and Europe facilities.

- Dominant Product Type: Lotion pumps, holding approximately 47.6% market share, supported by wide compatibility, low tooling cost, standardized components, and strong penetration in personal care and household liquid applications.

- Leading Material Type: Plastic, with an estimated 62.5% share of total pump and dispenser materials in 2025, driven by moldability, cost efficiency, established supply chains, and increasing use of PCR-enabled mono-material designs.

| Key Insights | Details |

|---|---|

| Pump and Dispenser Market Size (2026E) | US$8.8 Bn |

| Market Value Forecast (2033F) | US$13.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Strong Expansion in Personal Care and Skin-Care Demand

The global personal-care sector remains the largest and most influential demand center for pumps and dispensers. Rising consumption of skincare products, serums, moisturizers, hand sanitizers, and liquid cleansers drives consistent structural demand for lotion pumps, airless dispensers, and precision dosing mechanisms.

Asia Pacific contributes a notably high share of global beauty consumption, and its expanding middle class reinforces the market’s unit and value outlook. This pull effect is evident in both the mass and premium segments, where durable, precision-engineered dispensing components enhance product positioning and reduce formulation waste.

As brands widen their portfolios and increase SKU refresh cycles, pump and dispenser suppliers experience steady incoming volume and multi-year sourcing agreements.

Regulatory and Corporate Commitments to Circularity

Governments and global brands continue introducing stricter requirements for recycled content, recyclability, and extended producer responsibility. These shifts have compelled pump and dispenser manufacturers to redesign multi-material assemblies into mono-material versions, expand PCR integration, and validate compatibility with recycling streams.

Compliance timelines require brands to invest in upgraded tooling, testing, and supplier qualification. As a result, demand for redesigned, all-plastic dispensers and recyclable trigger systems is rising. Suppliers benefit from higher design service revenues, while premium recyclable solutions command improved margins.

Regulatory frameworks accelerate the transition toward sustainable dispensing systems and force industry-wide adoption of new material standards, raising long-term replacement demand.

Innovation in Dosing, Airless Technology, and User Comfort

Suppliers are introducing high-performance, all-plastic pumps, soft-actuation triggers, improved spray ergonomics, and airless systems optimized for formulation stability. These innovations cater to premium skincare, sensitive formulations, natural ingredients, and e-commerce durability requirements.

New high-dose pumps shorten consumer application time, while low-profile designs reduce material use and enhance compatibility with compact packaging formats. Airless systems protect formulations from oxidation and contamination, improving shelf life and brand perception. As brands pursue greater differentiation, the demand for specialty pumps and precision devices increases.

These technological advancements contribute to a shift toward higher-value dispensing formats, supporting the market’s value growth.

Barrier Analysis - Resin Price Volatility and Margin Compression

Fluctuating prices for core resins such as PET, PP, and HDPE increase input-cost unpredictability for pump manufacturers. Price swings can be substantial over short timeframes, often exceeding double-digit percentage changes within a single quarter.

Commodity lotion pumps and high-volume dispensers face the greatest pressure, as manufacturers cannot always pass cost increases to brand owners in competitive bidding cycles. Volatility in freight, energy, and logistics amplifies this margin risk. These dynamics complicate planning, affect profitability, and constrain the ability to invest in new tooling or R&D during periods of instability.

Implementation Burden from Circularity and Compliance Standards

Dispenser redesign to meet recyclability requirements, PCR thresholds, and extended producer responsibility programs carries significant time and capital demands. Manufacturers must invest in engineering validation, supply-chain traceability systems, and new quality-control processes.

Smaller brands often struggle to absorb these redesign costs, slowing their transition to compliant dispensing systems. For suppliers, these adjustments create periods of elevated spending, potential certification delays, and temporary inefficiencies. Compliance failures can lead to penalties or restricted market access, increasing operational and financial risk for manufacturers.

Opportunity Analysis - Asia Pacific Scale, Premiumization, and Manufacturing Localization

Asia Pacific’s expanding consumer base and strong manufacturing capabilities create a multi-billion-dollar opportunity for pump suppliers. As beauty and home-care categories in the region grow at higher rates than global averages, suppliers can capture an incremental opportunity of roughly US$1-2 billion across 2026 - 2033 by expanding tooling capacity, establishing local warehouses, and partnering with regional brands.

The premium skincare shift in China, Japan, India, and Southeast Asia increases demand for advanced, airless, and recyclable dispensers. Suppliers that offer localization, faster lead times, and sustainable material options stand to gain the most.

Refillable and Reuse-Driven Product Models

Refillable packaging formats and modular dispensers create recurring revenue opportunities by increasing dispenser lifecycle value. Brands using refill stations, concentrates, or pouch-plus-dispenser models generate ongoing demand for replacement components.

Converting even 5-10% of a brand’s consumer base to refill subscription models can significantly increase aftermarket dispenser sales and strengthen consumer loyalty. Suppliers that develop standardized, durable, and serviceable dispenser interfaces can lock in multi-cycle revenue and secure long-term contracts with refill-focused brands. This opportunity aligns with sustainability commitments and emerging retail models.

Smart and Connected Dispensing for Pharmaceuticals and High-Value Home-Care

Connected dosing, metered dispensing, child-safe locks, and tamper-proof mechanisms create new pathways for high-margin device uptake in pharmaceutical and specialized home-care applications. These systems allow dosage tracking, compliance monitoring, and safer handling of concentrated or regulated formulations.

Although adoption remains small relative to mass personal care, the premium commanded by connected devices, often 10-30% higher than conventional equivalents, creates a strong diversification avenue for suppliers. Over time, integration with mobile apps and home-health ecosystems will expand revenue potential and attract multi-year supply contracts.

Category-wise Analysis

Product Type Insights

Lotion pumps are expected to retain dominance with about 47.6% of global market share in 2026, driven by widespread use in skincare, personal hygiene, household cleaners, and sanitizers. Their popularity reflects mature supply chains, cost-efficient manufacturing, and compatibility with a range of viscosities.

High-volume production in Asia supports affordability, while standardized neck finishes enable easy integration for global brands. Durable lotion pumps also underpin refill and concentrate systems, with manufacturers advancing spring-less, all-plastic designs to meet recyclability goals.

Foam pumps represent the fastest-growing segment, propelled by increasing demand for controlled dispensing in hand washes, facial cleansers, cosmetics, pet care, and industrial hygiene applications. Consumers favor their dense, sensory-rich texture and efficient product delivery, helping brands meet sustainability and cost-saving targets.

Growth in Asia Pacific’s hygiene markets and e-commerce packaging innovation further boosts adoption. New lightweight, mono-material, and clog-resistant foam pump designs enhance consistency and environmental performance, supporting rapid uptake across market segments.

Material Type Insights

Plastic is expected to dominate the market, with about 62.5% market share in 2026, supported by its cost efficiency, moldability, and compatibility with personal care, home care, OTC, and household chemical products. Materials such as PP, PE, and PET ensure consistent performance and ease of large-scale production.

Asia Pacific’s strong injection-molding infrastructure sustains competitive pricing, while mono-material plastic assemblies enhance recyclability and regulatory compliance. Increasing use of PCR resins and component optimization reinforces plastic’s essential role across both mass-market and premium dispenser categories.

Metal is the fastest-growing material class, fueled by demand in luxury cosmetics, fragrances, high-viscosity skincare, and refillable packaging systems. Aluminum and stainless steel deliver durability, corrosion resistance, and precise dispensing performance.

Expanding refill models in Europe and North America strengthen demand for reusable metal pumps. With high recyclability, recovery value, and distinct aesthetic appeal, metal is positioned as the most dynamic, sustainability-aligned material segment through 2033.

Regional Insights

Asia Pacific Pump and Dispenser Market Trends - Manufacturing Scale, Premiumization, and Eco-Shift

Asia Pacific is projected to remain the largest and fastest-growing region in 2026, accounting for about 41% of global market value. Growth is supported by strong manufacturing ecosystems, competitive cost structures, expanding exports, and rising domestic consumption.

China, India, Japan, and South Korea anchor regional production, serving both global and local brand networks, with China offering unmatched scale in dispenser manufacturing through extensive injection-molding capacity, tooling expertise, and rapid prototyping.

China’s growing demand for premium skincare and beauty products fuels the adoption of airless and precision dispensers. Japan contributes advanced, high-precision solutions for pharmaceuticals, wellness, and high-end home care, while South Korea’s beauty industry drives the use of compact, high-performance pumps.

India and Southeast Asia are expanding rapidly, supported by urbanization, modern retail infrastructure, and increasing access to branded personal-care goods. Sustainability regulations, such as India’s Plastic Waste Management Rules (Amendment 2022) and Thailand’s EPR packaging framework, promote the use of recyclable and PCR-based materials. Japan’s Green Purchasing Law further encourages the procurement of eco-friendly packaging.

The region’s booming e-commerce sector accelerates demand for leak-proof, compact dispensers suited to digital retail logistics. Long-term opportunities lie in premium beauty growth, sustainable materials, and localized manufacturing. Suppliers investing in PCR sourcing, rapid prototyping, and compliance support are best positioned to capture regional market share.

North America Pump and Dispenser Market Trends - Premium Demand, Regulatory Pressure, and Refill Innovation

North America is a high-value market defined by premium packaging adoption, strong personal-care consumption, and advanced dispensing technology. While Asia Pacific leads in volume, North America maintains a significant value share due to higher average selling prices, deep skincare penetration, and regulated pharmaceutical and OTC applications requiring certified dosing systems.

The U.S. anchors regional demand, with consumers favoring high-performance, visually appealing, and recyclable dispensers. Elevated spending on skincare, cosmetics, and wellness products supports strong adoption of airless systems, micro-mist sprayers, and precision pumps, particularly in prestige beauty channels.

E-commerce growth further drives demand for leak-resistant, low-profile designs suited for complex logistics. A notable innovation, Rieke’s Mono™-2e pump, offers a fully recyclable, single-polymer solution aligning with PCR content and sustainability mandates.

Market growth is fueled by retailer-driven sustainability requirements, expanding refill and reuse models, and state-level regulations on recyclability and labeling transparency. These dynamics encourage mono-material adoption and closer supplier-brand collaboration.

Investment priorities include expanding domestic production, upgrading tooling for recyclable lines, and enhancing durability testing. M&A activity among dispensing specialists continues as companies seek broader technical portfolios and stronger partnerships with leading beauty and home-care brands, reinforcing the region’s position as a center for high-performance, sustainable packaging innovation.

Europe Pump and Dispenser Market Trends - Sustainability Leadership and Advanced Material Engineering

Europe serves as both a global innovation hub and a regulatory benchmark for the pump and dispenser industry. The region’s strong focus on circularity, waste reduction, and recyclability has led to stringent packaging standards that influence global product design.

EU packaging policies are accelerating demand for mono-material pumps, recyclable trigger systems, and dispensers incorporating verified recycled content. Germany remains a key engineering and manufacturing center known for precision development and advanced technical partnerships.

France and the U.K. lead the premium beauty segment, driving adoption of sophisticated airless pumps, micro-dosing systems, and custom finishes. In contrast, Spain and Italy show high demand for affordable yet sustainable dispensers used in mass-market personal-care products. Market growth is driven by brand sustainability commitments, the expansion of refill programs, and ongoing premiumization in skincare.

Consumers across Europe are increasingly eco-conscious, prompting brands to prioritize recyclable materials and refillable, lightweight packaging. Innovations such as Aptar Beauty + Home’s “Future Pump” and “Mono Micro” exemplify this trend with fully recyclable mono-material PE designs compliant with RecyClass and Cyclos-HTP standards.

European suppliers lead in material science, developing spring-less pumps, bio-based polymers, and recyclable mechanisms. Investment momentum centers on sustainable materials, advanced tooling, and recyclable technologies that often set the foundation for global dispenser innovation.

Competitive Landscape

The global pump and dispenser market combines fragmented commodity suppliers with a concentrated group of premium manufacturers. Leading players dominate high-value categories such as airless, precision-dosing, and recyclable pumps, supported by strong design expertise and global scalability. Sustainability and innovation now define competitive strength, favoring firms with advanced R&D and multi-region production.

Key strategies include recyclable and mono-material product expansion, ergonomic design, and refill-compatible systems. Emerging models feature subscription-based dispensing and IoT-enabled drug delivery, highlighting the industry’s shift toward smart, sustainable packaging solutions.

Key Industry Developments

- In January 2025, TriMas Packaging launched a new fully recyclable foaming pump under its Singolo product line, replacing the conventional metal spring with an innovative polymeric spring to enable direct recyclability and support a broad range of beauty, personal care and home-care applications.

- In February 2025, AptarGroup unveiled its HDP (High-Dose Pump) in North America, an all-plastic dispenser designed for large-size bottles, delivering a generous 3.5 cc dose per stroke and featuring a metal-free design to enhance recyclability and e-commerce readiness.

Companies Covered in Pump and Dispenser Market

- AptarGroup Inc.

- Silgan Dispensing Systems

- Berry Global

- Albea Group

- Rieke (TriMas Corporation)

- Coster Group

- Mitani Valve Co. Ltd.

- Frapak Packaging

- RPC Group

- Ningbo Jieli Plastics

- WestRock Company

- Calmar Inc.

- Raepak Ltd.

- Yonwoo Korea

- Aptar Beauty + Home

- Tupperware Brands (Pumps Division)

- PZ Cussons (Packaging Division)

- Swallowfield PLC

- Linhardt Group

- Quadpack Industries

Frequently Asked Questions

The market size is estimated to reach US$8.8 billion in 2026.

By 2033, the pump and dispenser market is expected to reach a value of US$13.0 billion.

Key trends include rapid adoption of foam pumps due to rising demand for sensory-rich personal hygiene and skincare applications, and acceleration of mono-material and PCR-integrated designs to meet recyclability and regulatory requirements.

Lotion Pumps are the leading product type, holding approximately 48 percent global market share in 2025.

Plastic is the dominant material class, accounting for around 63% market share in 2025.

Metal is the fastest-growing material category, driven by premium skincare, fragrance packaging, refillable systems, and high durability requirements.

The market is projected to grow at a CAGR of 5.7% from 2026 to 2033.

Major companies include AptarGroup, Inc., Silgan Dispensing Systems, Albea Group, Berry Global, and Rieke (TriMas Corporation).