- Specialty & Fine Chemicals

- Propylene Glycol Methyl Ether Acetate Market

Propylene Glycol Methyl Ether Acetate Market Size, Share, and Growth Forecast 2026 - 2033

Propylene Glycol Methyl Ether Acetate (PGMEA) by Grade (Industrial Grade, Reagent Grade, Electronic Grade, Pharmaceutical Grade, Specialty Grade), by Sales Channel (Direct Sales, Distributors, Online Channels, Retail), by End-Use Industry (Automotive, Construction, Industrial Manufacturing, Electronics & Electrical, Aerospace, Pharmaceuticals, Others), by Regional Analysis, 2026 - 2033

Propylene Glycol Methyl Ether Acetate Market Size and Trend Analysis

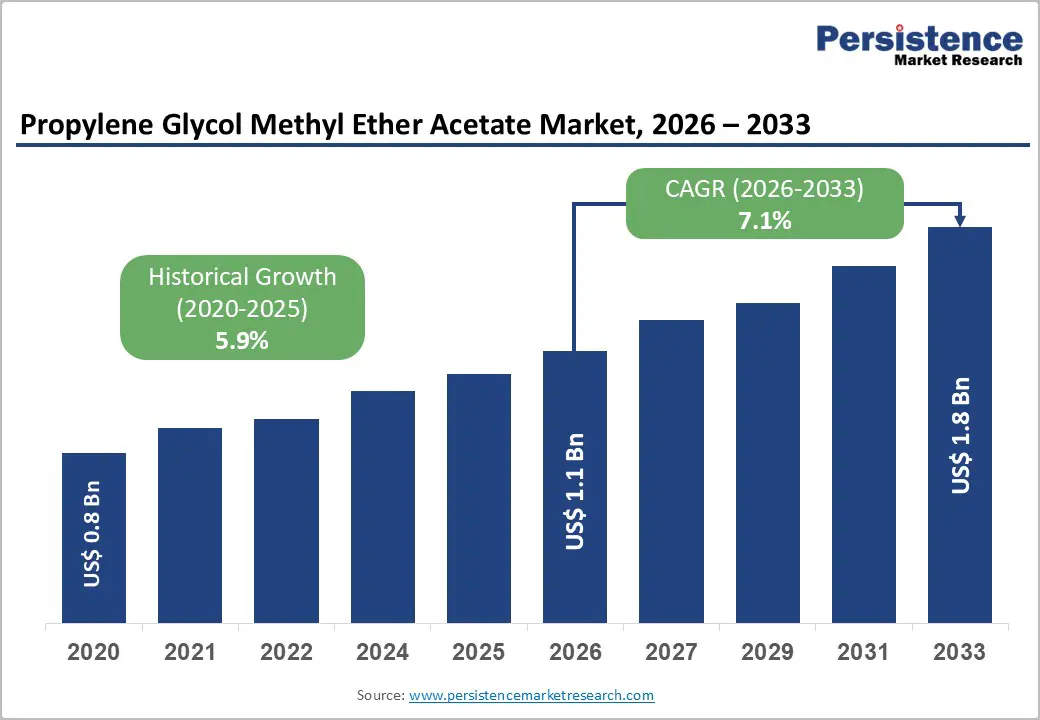

The global propylene glycol methyl ether acetate market size is likely to be valued at US$ 1.1 billion in 2026 and is expected to reach US$ 1.8 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033.

Market growth is driven by rising semiconductor demand for high-purity PGMEA, stricter environmental regulations that promote low-VOC solvents, and the expansion of pharmaceutical, automotive coatings, and specialty industrial applications that require high-performance liquid formulations.

Key Market Highlights

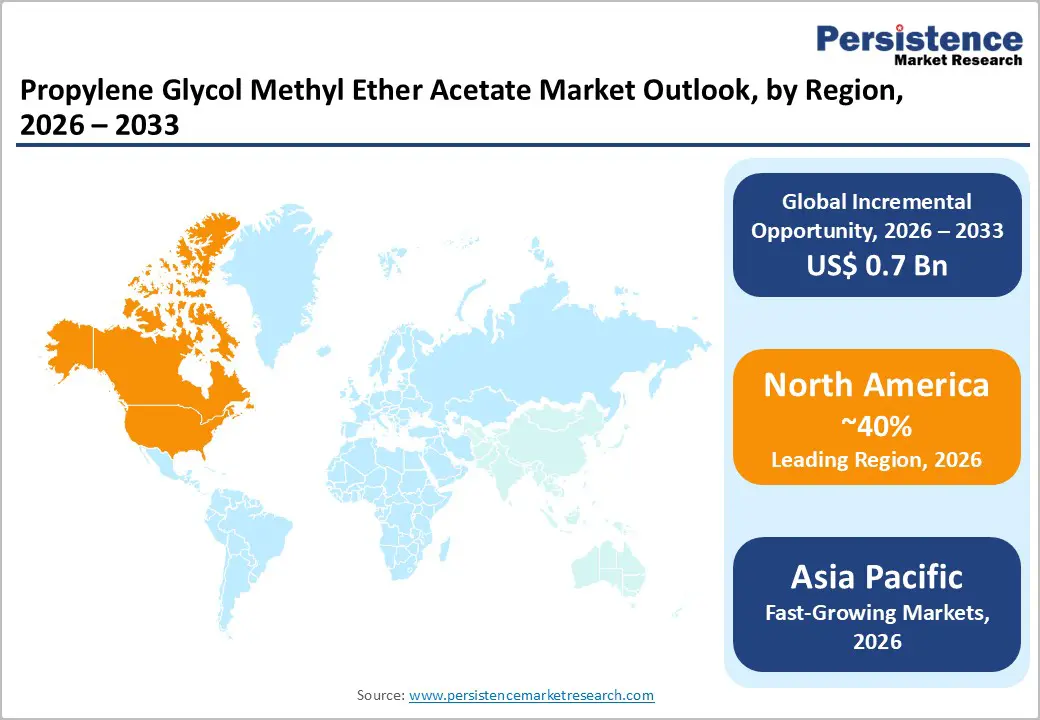

- Leading Region: North America is the dominant market holding 40% share, supported by mature electronics manufacturing, stringent regulatory compliance frameworks, and substantial investment in sustainable PGMEA formulations and premium product development.

- Fastest-Growing Region: Asia Pacific experiences the fastest regional growth, with a 9.8% CAGR, as China consumes 22,000 metric tons annually and Taiwan Semiconductor Manufacturing dominates electronic-grade consumption, supporting exceptional market expansion.

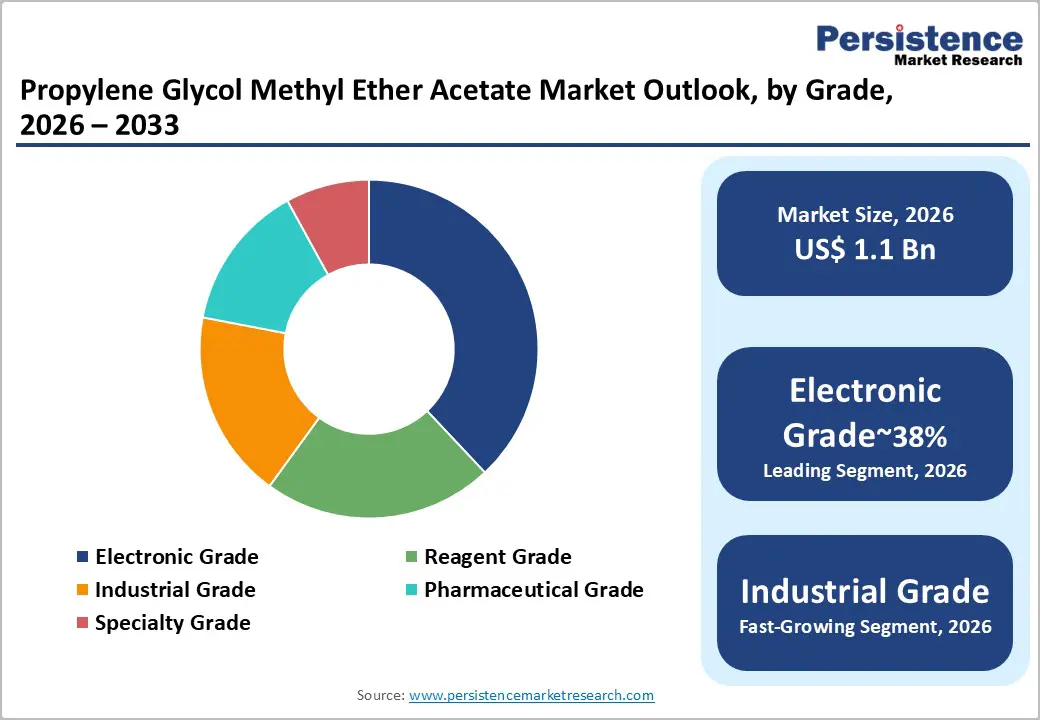

- Leading Segment: Electronic-grade formulations command ~38% market share, driven by semiconductor manufacturing requirements exceeding 99.9% purity, supporting premium pricing and exceptional profitability.

- Fastest-Growing Segment: Electronics and semiconductor applications represent the fastest-growing segment at 31% market share, driven by photoresist solvents and manufacturing processes supporting 5G and AI chip production expansion.

- Key Growth Opportunity: Pharmaceutical industry expansion across emerging markets with 9.8% annual PGMEA consumption growth and specialty industrial applications create substantial growth opportunities supporting market diversification.

| Key Insights | Details |

|---|---|

| Propylene Glycol Methyl Ether Acetate Market Size (2026E) | US$ 1.1 Billion |

| Market Value Forecast (2033F) | US$ 1.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 5.9% |

Market Dynamics

Drivers - Rapid global semiconductor capacity expansion and advanced node development are significantly increasing demand for ultra-pure electronic-grade PGMEA solvents

The rapid expansion of global semiconductor manufacturing capacity is significantly driving demand for high-purity electronic-grade PGMEA solvents, which are essential in photoresist formulations used during chip fabrication. The increasing adoption of 5G networks, artificial intelligence platforms, and advanced computing architectures has accelerated investments in semiconductor production worldwide. Taiwan Semiconductor Manufacturing Company alone consumed nearly 12,000 metric tons of electronic-grade PGMEA in 2024 across its global fabrication facilities, highlighting strong volume demand for premium solvent grades.

Advanced technology nodes such as 5nm and 3nm require extremely high material purity, with PGMEA specifications exceeding 99.9% purity and metal contamination controlled below 100 ppb. These stringent standards allow suppliers to command premium pricing. Asia continues to dominate semiconductor manufacturing, with China consuming approximately 22,000 metric tons of PGMEA in 2024, of which nearly 65% was used for electronic-grade applications. Combined consumption by Samsung and SK Hynix exceeding 8,500 metric tons annually further strengthens market growth. Additionally, government initiatives such as China’s Made in China 2025 strategy, promoting semiconductor self-sufficiency, continue to support long-term demand for specialized manufacturing solvents.

Tightening environmental regulations and sustainability goals are accelerating the shift toward eco-friendly, low-toxicity PGMEA solvent formulations

Increasing environmental regulations related to volatile organic compound emissions, chemical safety, and sustainable manufacturing practices are accelerating the shift toward PGMEA-based solvent systems. Manufacturers across the coatings, paints, and adhesives industries are replacing traditional high-toxicity solvents with environmentally safer alternatives to meet regulatory requirements. In North America and Europe, strict VOC emission standards have created a strong preference for PGMEA-based formulations, as they offer improved environmental compliance without compromising performance. This regulatory pressure is also aligned with growing corporate sustainability commitments, pushing companies to adopt low-toxicity and eco-friendly materials.

PGMEA’s favorable biodegradability profile and lower environmental impact compared to legacy solvents make it a preferred choice for formulators aiming to balance performance and sustainability. As consumers and regulators increasingly favor greener chemical solutions, PGMEA continues to gain traction across multiple applications. This transition creates premium-pricing opportunities for manufacturers that emphasize sustainable production methods, environmental stewardship, and compliance-driven innovation, thereby further strengthening the market’s long-term growth outlook.

Restraints - High purification costs, complex manufacturing processes, and raw material price volatility continue to restrain broader PGMEA market adoption

The production of advanced electronic-grade PGMEA involves highly sophisticated purification processes, including vacuum distillation, multistage filtration, and rigorous quality-control systems. These requirements significantly increase capital investment and operational costs for manufacturers. Achieving ultra-high purity levels demanded by semiconductor applications requires continuous monitoring and specialized infrastructure, creating strong entry barriers for new or smaller producers. In addition, fluctuations in raw material prices, particularly propylene and methyl acetate feedstocks, contribute to cost volatility and margin pressure.

Manufacturers without vertically integrated supply chains are especially exposed to rising procurement costs, limiting their pricing flexibility. These high production costs limit adoption in cost-sensitive applications and in emerging economies, where budget constraints influence purchasing decisions. As a result, although demand remains strong in premium segments, overall market penetration can be constrained by affordability challenges, particularly for industrial users seeking lower-cost solvent alternatives.

Increasing regulatory complexity and rising compliance costs create operational challenges and slow product commercialization across global PGMEA markets

Manufacturers operating in developed markets face increasing regulatory complexity related to chemical safety, environmental protection, and occupational health standards. Compliance with frameworks such as the European REACH regulations, VOC emission controls, and region-specific chemical registration requirements significantly increases operational costs. These regulatory obligations require extensive documentation, ongoing audits, and frequent product testing, thereby extending development timelines and delaying commercialization.

Fragmented regulatory systems across regions require manufacturers to customize formulations and compliance strategies for different markets, increasing administrative and operational burdens. Smaller manufacturers often struggle to meet these evolving standards, limiting their competitiveness and expansion capabilities. As regulations continue to tighten, companies must invest heavily in compliance infrastructure, safety systems, and regulatory expertise. While these measures improve environmental performance, they also act as barriers to rapid market growth and reduce flexibility in responding quickly to changing customer or technology demands.

Opportunities - Next-generation semiconductor technologies and advanced lithography processes present strong growth opportunities for high-purity electronic-grade PGMEA producers

The emergence of next-generation semiconductor technologies presents significant growth opportunities for electronic-grade PGMEA manufacturers. Advanced processes such as extreme ultraviolet lithography, chiplet-based architectures, and expansion of 3nm and 5nm nodes require ultra-pure solvents with extremely low contamination levels. This creates strong demand for specialized PGMEA formulations that meet stringent performance and reliability standards.

In addition, the rise of flexible and printed electronics applications, including wearable devices, smart packaging, and printed sensors, creates new high-growth segments that require customized solvent solutions. Increasing production of artificial intelligence accelerators and high-performance computing chips further supports sustained demand for premium electronic-grade PGMEA. As semiconductor fabrication capacity expands across the Asia-Pacific and North America, manufacturers that focus on purity enhancement, advanced formulation development, and close collaboration with chipmakers are well positioned to capture long-term value in this technologically driven market.

Expanding pharmaceutical production and rising specialty chemical applications are opening new high-value growth avenues for PGMEA manufacturers globally

The expanding pharmaceutical industry in emerging economies such as India and China represents a major growth opportunity for PGMEA manufacturers. Pharmaceutical companies increasingly use PGMEA in advanced drug synthesis, purification, and formulation processes due to its strong solvent properties and controlled impurity profile. Leading companies, including Dr. Reddy’s Laboratories, have expanded usage, while Chinese pharmaceutical manufacturers report nearly 9.8% annual growth in PGMEA consumption.

This rising demand supports development of pharmaceutical-grade formulations that meet strict pharmacopeia and regulatory standards. Beyond pharmaceuticals, specialty chemical applications such as high-performance coatings, precision cleaning agents, and advanced adhesive systems are emerging as attractive revenue streams. These applications require tailored solvent solutions optimized for specific performance parameters. Manufacturers that invest in customized product development and application-specific solutions can strengthen customer relationships and diversify revenue, positioning themselves for stable long-term growth across professional and institutional markets.

Category-wise Analysis

Grade Insights

Electronic-grade PGMEA holds approximately 38% of the total market share, primarily driven by strong demand from semiconductor and electronics manufacturing. These applications require ultra-high purity levels of 99.9% or higher, with metal contamination maintained below 100 ppb to ensure device reliability and production efficiency. The complex purification processes involved justify premium pricing and contribute to higher profitability. Industrial-grade PGMEA accounts for approximately 35% of the market, supported by widespread use in coatings, inks, adhesives, and industrial cleaning applications, where cost efficiency and consistent performance are critical.

Pharmaceutical and specialty grades together represent nearly 27% of the market, serving niche applications that demand strict quality standards, regulatory compliance, and customized formulations. These segments command premium positioning due to their specialized requirements. Overall, the balanced demand across grades supports market stability while allowing manufacturers to target both high-volume and high-margin opportunities.

Sales Channel Insights

Direct sales dominate the PGMEA market, accounting for approximately 52% of the market, driven by long-term supply agreements with large semiconductor manufacturers, pharmaceutical companies, and industrial coating producers. These customers prefer direct procurement to ensure consistent quality, reliable supply, and technical collaboration. Distributor networks account for approximately 32% of the market, serving mid-sized and regional customers through established chemical distribution channels.

Distributors offer logistical flexibility, localized support, and faster delivery, making them essential for regional market penetration. Online and retail channels together represent nearly 16% of the market and are experiencing steady growth. The expansion of e-commerce platforms and digital procurement models enables small manufacturers and emerging enterprises to access PGMEA more easily. This evolving distribution structure improves market accessibility, enhances supply chain efficiency, and supports broader customer reach across industrial and specialty segments.

Industry Insights

The electronics and semiconductors segment accounts for approximately 31% of the total market and remains the fastest-growing application area. Demand is driven by photoresist solvents, wafer processing, and precision cleaning applications that require high-purity PGMEA formulations. Automotive coatings account for nearly 22% of the market, supported by OEM paint systems, refinishing applications, and performance-driven coating technologies. PGMEA provides excellent flow, finish quality, and environmental compliance, making it well-suited for automotive use.

Construction and industrial coatings collectively account for approximately 28% of the market, driven by architectural paints, protective coatings, and industrial maintenance solutions. PGMEA’s strong solvency and film-forming characteristics allow broad applicability across multiple coating systems. Together, these end-use industries ensure diversified demand, supporting consistent market expansion across both industrial and high-technology sectors.

Regional Insights

North America Propylene Glycol Methyl Ether Acetate Trends

North America holds a strong market position supported by advanced electronics manufacturing infrastructure and significant investment in semiconductor fabrication facilities. The United States plays a central role due to its robust semiconductor ecosystem, which combines leading fabrication plants with innovation-driven chip design. This environment generates steady demand for high-performance solvents used in precision manufacturing processes.

In addition, stringent environmental regulations related to VOC emissions and chemical safety encourage the adoption of PGMEA-based formulations over traditional solvents. The automotive and aerospace industries also contribute substantially to regional demand, utilizing PGMEA in high-performance coating systems that require durability, surface quality, and regulatory compliance. Ongoing modernization of manufacturing facilities and increasing focus on domestic semiconductor production further support sustained market growth across premium industrial and electronic applications in the region.

Europe Propylene Glycol Methyl Ether Acetate Trends

European markets, including Germany, France, the United Kingdom, and Spain, maintain a stable and technologically advanced PGMEA market. Strong automotive manufacturing, industrial coatings production, and strict environmental regulations drive steady demand for sustainable solvent solutions. The European Union’s emphasis on chemical safety, environmental protection, and VOC reduction strongly favors PGMEA-based formulations that comply with REACH standards.

Germany’s leadership in automotive engineering and advanced coating technologies drives consistent demand for high-performance solvents. Additionally, Europe’s commitment to circular economy principles encourages innovation in sustainable chemical manufacturing. This focus creates opportunities for bio-based PGMEA alternatives and advanced purification technologies. As sustainability becomes a central purchasing criterion, manufacturers offering environmentally responsible solutions are well positioned to strengthen their market presence and achieve long-term growth across the European region.

Asia Pacific Propylene Glycol Methyl Ether Acetate Trends

Asia Pacific dominates the global PGMEA market, accounting for approximately 48% of total demand. This leadership is driven by rapid expansion in semiconductor manufacturing, strong automotive production, and growth in the pharmaceutical industry across China, Taiwan, Japan, South Korea, and the ASEAN economies. China remains the largest consumer, with annual PGMEA consumption of nearly 22,000 metric tons, of which around 65% is electronic-grade.

Government initiatives promoting semiconductor self-sufficiency further strengthen demand for high-purity solvents. Taiwan serves as a critical hub, with TSMC consuming over 12,000 metric tons annually to support advanced chip manufacturing. Additionally, growth in the pharmaceutical industry in India and China is increasing PGMEA usage in drug synthesis and purification processes. These combined factors position Asia Pacific as the primary engine of global market growth.

Competitive Landscape

The global polypropylene glycol methyl ether market exhibits moderate consolidation, with a mix of multinational chemical corporations and regional specialists. Tier-1 manufacturers such as LyondellBasell Industries, Royal Dutch Shell, DowDuPont, BASF SE, and Eastman Chemical Company collectively account for approximately 68% of global market share. Their dominance is supported by large-scale production capacity, advanced purification technologies, and long-standing customer relationships.

Tier-2 players, including KH Neochem, Daicel, and regional Asian manufacturers, hold around 20-25% share through cost-competitive operations and strong regional focus. Competitive differentiation increasingly centers on product purity enhancement, sustainable manufacturing practices, and specialty grade development. Continuous investment in research and development remains critical as manufacturers strive to meet evolving semiconductor and environmental requirements, ensuring ongoing innovation and long-term market competitiveness.

Key Developments:

- In December 2024: LyondellBasell Industries completed a major expansion of its electronic-grade PGMEA production capacity to support rising semiconductor manufacturing demand. The expansion strengthens global supply security for high-purity solvents used in advanced lithography and wafer fabrication processes.

- In September 2024: Eastman Chemical Company introduced new sustainable PGMEA formulations incorporating bio-derived raw materials. This initiative supports environmental compliance goals while maintaining high solvency performance, helping customers meet stricter VOC regulations and sustainability targets across coatings and electronics applications.

- In June 2024: BASF SE announced expansion of its manufacturing infrastructure across the Asia Pacific region to address rising demand from semiconductor, electronics, and industrial coatings sectors. The expansion improves regional supply reliability and strengthens BASF’s strategic presence in high-growth Asian markets.

Companies Covered in Propylene Glycol Methyl Ether Acetate Market

- LyondellBasell Industries Holdings N.V.

- Royal Dutch Shell plc

- DowDuPont Inc. (Dow Chemical)

- BASF SE

- Eastman Chemical Company

- Chang Chan Group

- Manali Petrochemicals Limited

- KH Neochem Co. Ltd.

- Shiny Chemical Industrial Company Limited

- Jiangsu Baichuan High-tech New Materials Co. Ltd.

- Jiangsu Hualun Chemical Industry Co. Ltd.

- Jiangsu Dynamic Chemical Co. Ltd.

- Daicel Corporation

- Nippon Nyukazai Company

- SKC Co. Ltd.

- INEOS Oxide

Frequently Asked Questions

The global PGMEA market is projected to reach US$ 1.8 billion by 2033, growing at a 7.1% CAGR driven by semiconductor, eco-friendly solvent, and industrial application demand.

Market growth is driven by semiconductor manufacturing expansion, stringent environmental regulations promoting low-VOC solvents, and rising pharmaceutical and specialty chemical applications.

Electronic-grade PGMEA leads the market with approximately 38% share, supported by ultra-high purity requirements in advanced semiconductor fabrication.

Asia Pacific dominates the global market, accounting for around 48% demand, led by strong semiconductor manufacturing in China, Taiwan, and South Korea.

Major opportunities include advanced semiconductor nodes, EUV lithography, pharmaceutical expansion in emerging markets, and growth in flexible electronics applications.

The market is led by LyondellBasell, Shell, Dow, BASF, and Eastman Chemical, supported by strong production capacity, technology leadership, and global supply networks.