- Specialty & Fine Chemicals

- Polypropylene Packaging Market

Polypropylene Packaging Market Size, Share, and Growth Forecast, 2025 - 2032

Polypropylene Packaging Market By Product Format (Rigid Packaging and Flexible Packaging), Polymer Type (Homopolymer Polypropylene (PP-H), Impact Copolymer Polypropylene (PP-B), Others), End-user, and Regional Analysis for 2025 - 2032

Polypropylene Packaging Market Size and Trends Analysis

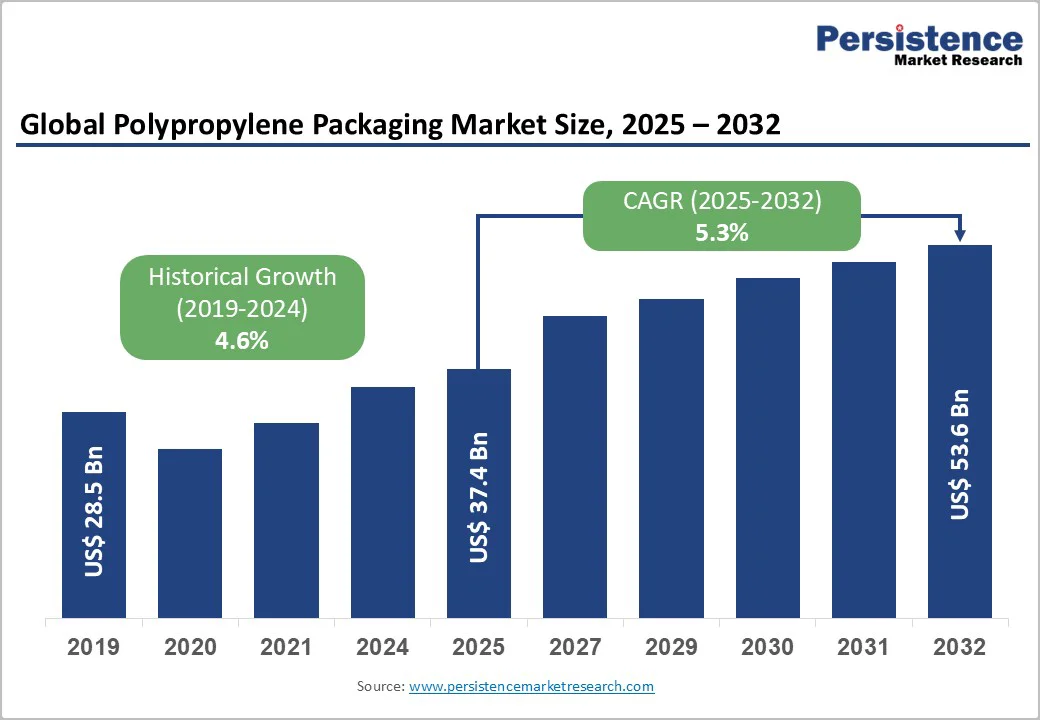

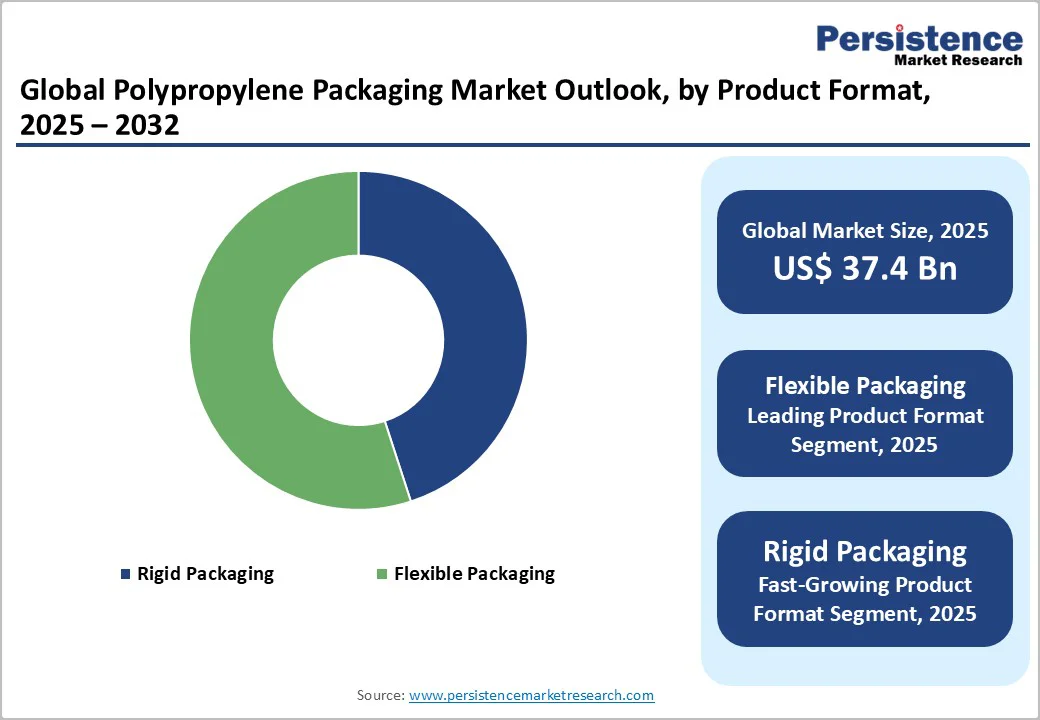

The global polypropylene packaging market size is likely to be valued at US$37.4 billion in 2025. It is projected to reach US$53.6 billion by 2032, growing at a CAGR of 5.3% during the forecast period from 2025 to 2032, driven by surging demand for lightweight and durable packaging solutions in the food and beverage sector, where polypropylene's barrier properties extend shelf life and reduce transportation costs.

Advancements in recycling technologies and regulatory pushes for sustainable materials are accelerating adoption, particularly in automotive and healthcare applications, supported by a 15% increase in global packaging production reported in 2024. These factors, when combined, enhance efficiency and align with circular-economy goals, thereby propelling market expansion.

Key Market Highlights

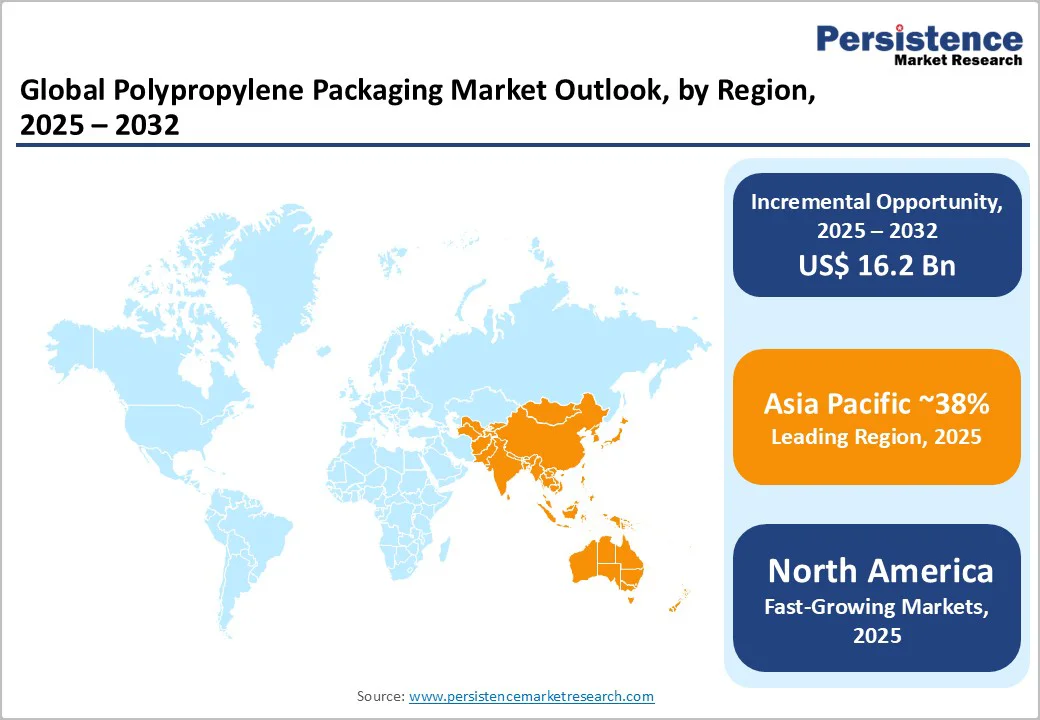

- Leading Region: Asia Pacific leads as the dominant region with a 38% share, driven by manufacturing hubs in China and India, which together account for nearly half of the global share through packaging and automotive demand.

- Fastest-Growing Region: North America emerges as the fastest-growing region, with a robust innovation ecosystem and evolving regulatory frameworks that emphasize sustainability and circularity.

- Leading Segment: Flexible packaging dominates product format segments, with over 55% share, driven by lightweight e-commerce applications.

- Fastest-Growing Segment: Food & beverage is the fastest-growing end-user segment, surging annually from processed foods.

- Key Opportunity: Sustainable recycling offers substantial potential through bio-based advancements.

| Key Insights | Details |

|---|---|

| Polypropylene Packaging Market Size (2025E) | US$37.4 Bn |

| Market Value Forecast (2032F) | US$53.6 Bn |

| Projected Growth CAGR (2025 - 2032) | 5.3% |

| Historical Market Growth (2019 - 2024) | 4.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Future Analysis - Growing Consumption of Packaged Foods

The polypropylene packaging market is witnessing robust growth driven by the surging demand for packaged food and beverages. Changing consumer lifestyles, rapid urbanization, and the expansion of e-commerce food delivery services are accelerating the need for efficient and durable packaging. Polypropylene (PP) packaging offers superior moisture, chemical, and heat resistance, making it ideal for preserving freshness and extending product shelf life.

Companies such as Toray Plastics have launched the Torayfan PLS film series, enhancing oxygen and moisture barrier protection for snacks and bakery items. Taghleef Industries and UFlex Limited are introducing advanced BOPP films packaging that prevents contamination while improving recyclability.

3B Films Limited has expanded production to meet the growing demand from the FMCG sector. These developments emphasize how PP’s versatility, lightweight nature, and sustainability make it the preferred choice for food and beverage packaging worldwide.

Rising Preference for Lightweight, Recyclable, and Cost-Efficient Flexible Packaging

The rising demand for flexible, cost-effective, and eco-friendly packaging is a major driver of the polypropylene packaging market. PP’s high clarity, strength, and barrier properties make it suitable for a wide range of applications, from pouches and wraps to labels and containers. Manufacturers are focusing on developing recyclable and mono-material PP packaging solutions to meet global sustainability goals.

Taghleef Industries and Copol International are innovating mono-layer BOPP films, while Borealis AG and UFlex Limited are investing in circular recycling technologies. The growing preference for lightweight packaging that reduces transportation costs and carbon emissions is further supporting PP’s adoption.

As industries increasingly replace traditional materials with recyclable PP formats, the market continues to expand due to its balance of functionality, cost-efficiency, and environmental benefits.

Barrier Analysis - Unstable Crude Oil Prices Remain a Major Restraint Impacting Polypropylene Packaging Production Costs

Fluctuations in crude oil prices remain a key restraint in the polypropylene packaging market, as PP is produced from petroleum-based feedstocks such as propylene. Any sharp increase in oil prices directly raises manufacturing costs and compresses profit margins for packaging producers. Leading companies such as LyondellBasell and Borealis have reported cost pressures that have led to production slowdowns and cautious expansion.

Smaller converters are particularly affected, facing competitiveness challenges when raw material prices spike. To reduce exposure to oil price volatility, firms are adopting hedging strategies and investing in bio-based propylene sources. Despite these efforts, ongoing instability in crude oil markets continues to affect supply chain predictability, cost management, and long-term investment planning across the global polypropylene packaging sector.

Global Plastic Regulations are Driving Innovation toward Recyclable and Bio-Based Polypropylene Packaging

Tightening environmental regulations continue to pressure polypropylene packaging manufacturers. Many countries are enforcing bans on single-use plastics and mandating recycled content in packaging products. Producers now face rising compliance costs and the need to upgrade production lines for recyclability.

Taghleef Industries and UFlex Limited have responded by developing films made from post-consumer recycled and bio-based polypropylene to meet sustainability standards.

In regions such as Europe and North America, new extended producer responsibility (EPR) laws require packaging companies to include specific percentages of recycled material, further driving costs. While these measures encourage innovation, they also limit flexibility for low-cost applications and smaller enterprises. As a result, compliance with evolving sustainability mandates remains a key challenge for polypropylene producers seeking long-term market growth.

Opportunity Analysis - Increasing Focus on Circular Economy is Creating Strong Growth Prospects for Recycled and Bio-Based PP Packaging

The global shift toward sustainability is unlocking major opportunities in recycled and bio-based polypropylene packaging. Companies such as Taghleef Industries and Copol International have developed recyclable, mono-material PP films that maintain performance without compromising environmental goals.

Borealis AG and UFlex Limited are investing heavily in advanced recycling technologies to convert plastic waste into high-quality PP resins. Plastchim-T has expanded its sustainable packaging production capacity to meet surging demand across Europe.

These innovations align with consumer preferences for eco-friendly packaging and help brands meet corporate sustainability targets. As governments and corporations push for the adoption of the circular economy, demand for recycled and bio-based PP materials is expected to rise sharply, driving a new growth phase for forward-looking packaging manufacturers.

Expanding Healthcare and Hygiene Sectors

Polypropylene’s chemical resistance, clarity, and sterilization compatibility make it ideal for healthcare and personal care packaging. Rising global healthcare spending and post-pandemic hygiene awareness have accelerated its use in pharmaceutical bottles, syringes, and labware.

Mitsui Chemicals’ TPX™ resin and similar PP-based materials are increasingly adopted for sterile and transparent packaging applications. Alpha Marathon Technologies and Polyplex are expanding their extrusion and film production lines to meet high demand in the medical and hygiene markets.

In personal care, random copolymer PP films are preferred for their premium clarity and flexibility, appealing to cosmetic brands. Growing adoption in Asia-Pacific, driven by rapid expansion of healthcare infrastructure and rising disposable incomes, positions PP as a key material for next-generation medical and personal care packaging.

Category-wise Analysis

Product Format Insights

Flexible packaging leads the product format category with approximately 55% market share, driven by its versatility in films, wraps, and pouches that cater to e-commerce and consumer goods. This dominance stems from lightweight properties reducing shipping costs, making it preferable for food and retail applications. Industry data highlights its use in over half of flexible formats, underscoring superior moisture resistance and recyclability.

Polymer Type Insights

Homopolymer Polypropylene (PP-H) holds the leading position with about 60% share in the polymer type category, owing to its high rigidity and cost-effectiveness for rigid containers and bottles. Its uniform structure provides excellent chemical resistance, making it ideal for industrial and food packaging, supported by production data showing that most global PP output is homopolymer. This preference is justified by lower processing costs, enhancing adoption in high-volume sectors.

End-user Insights

Food & beverage dominates the end-use category with roughly 40% market share, driven by polypropylene's barrier properties, which help preserve freshness in containers and films. This leadership is supported by a significant revenue share in related packaging sectors amid rising annual processed food consumption. Its compliant grades ensure safety for beverages and meals, solidifying demand amid urbanization trends.

Regional Insights

North America Polypropylene Packaging Trends

In North America, the polypropylene packaging market is gaining strength due to a robust innovation ecosystem and evolving regulatory frameworks that emphasize sustainability and circularity. In the U.S., in particular, federal and state mandates under extended producer responsibility (EPR) rules are driving brands to adopt recycled polypropylene in bottles, caps, and flexible packaging.

LyondellBasell Industries has joined a circular initiative that allows food-grade recycled polypropylene derived from post-consumer waste, positioning its “Circulen” range for consumer goods and packaging applications.

This movement is supported by a well-developed recycling infrastructure, which allows converters such as Inteplast Group to plan for increased use of recycled content in domestic flexible packaging, reducing reliance on virgin material. The combination of regulation, infrastructure, and brand demand is steadily expanding the polypropylene packaging opportunity in North America.

Europe Polypropylene Packaging Trends

In Europe, polypropylene packaging trends are strongly influenced by harmonized regulations that mandate recycled content across major markets, including Germany, the U.K., France, and Spain. Companies such as Taghleef Industries are responding by launching their “reLIFE™” recycled polypropylene film range, which maintains technical performance while boosting circularity. European converters such as 3B Films Limited are shifting to mono-material film designs to improve recyclability as mandated by the EU’s Green Deal and Packaging Waste Regulation.

France and Spain are particularly active, encouraging additive reduction and promoting reusable packaging formats. Sustainability programs in the region promote renewal of polypropylene with bio-based feedstocks, enabling film producers such as Plastchim-T to expand capacity for circular packaging solutions. Together, regulatory push and industry innovation are accelerating the move toward more sustainable polypropylene packaging in Europe.

Asia Pacific Polypropylene Packaging Trends

Asia Pacific is emerging as a powerhouse for polypropylene packaging growth, driven by rapid manufacturing expansion in China, Japan, India, and ASEAN countries, and capturing a major share of the global volume. For example, India-based UFlex Limited has reported growth in flexible packaging demand linked to e-commerce and the rising middle class.

In China and ASEAN, companies such as Thai Film Industries Public Company Limited and Polyplex are ramping up polypropylene film capacity for food, beverage, and personal care packaging. Japan and South Korea continue to innovate in high-barrier and specialty films, while urbanisation across Southeast Asia adds to the consumption base. With cost-competitive production, expanding consumer markets, and a shift toward value-added polypropylene grades, the Asia Pacific region is well positioned for sustained packaging growth in the coming years.

Competitive Landscape

The global polypropylene packaging market is moderately consolidated, with top players controlling a substantial share through strategic expansions and R&D in sustainable grades. Companies focus on mergers for capacity growth, such as petrochemical integrations, and differentiate via bio-based innovations meeting regulatory demands. Emerging models emphasize circular supply chains, with leaders investing significantly in recycling technology to capture eco-premiums.

Key Industry Developments

- In April 2024, BASF SE launched food-grade polypropylene products with enhanced recyclability targeted at sustainable packaging markets, enabling food-contact safety while promoting circular packaging solutions and reducing reliance on virgin PP.

- In March 2024, Reliance Industries announced a boost to polypropylene output at its Jamnagar complex in India to meet strong domestic demand for PP in packaging, automotive, and consumer goods segments.

Companies Covered in Polypropylene Packaging Market

- Treofan Group

- Toray Plastics, Inc.

- Inteplast Group

- Plastchim-T

- Alpha Marathon Technologies Inc.

- Polyplex

- UFlex Limited

- 3B Films Limited

- Taghleef Industries

- Schur International Holding a/s

- Oben Group

- Thai Film Industries Public Company Limited

- Profol GmbH

- MITSUI CHEMICALS AMERICA, INC.

- Copol International Ltd.

- Borealis AG

- LyondellBasell Industries

Frequently Asked Questions

The polypropylene packaging market is expected to reach US$53.6 Billion by 2032, growing from US$37.4 Billion in 2025 at a 5.3% CAGR.

Rising food and beverage consumption drives demand, with polypropylene's barrier properties extending shelf life amid annual packaging growth.

Flexible Packaging leads with over half a share, favored for e-commerce due to its lightweight and recyclable traits.

Asia Pacific dominates with nearly half a share, propelled by China's manufacturing and India's infrastructure boom.

Sustainable recycling presents growth, with bio-based PP capturing a significant share via global policies and tech advancements.

Leading companies include Treofan Group, UFlex Limited, and Borealis AG.