- Specialty & Fine Chemicals

- Propylene Glycol Ether Market

Propylene Glycol Ether Market Size, Share, and Growth Forecast 2026 - 2033

Propylene Glycol Ether Market by Product Type (Propylene Glycol Mono Methyl Ether (PM), Dipropylene Glycol Mono Methyl Ether (DPM), Tripropylene Glycol Mono Methyl Ether (TPM)), by Application (Chemical intermediate, Solvent, Coalescing agent, Electronics (Semiconductor, TFT-LCD), Coatings, Others), by Industry (Construction, Automotive, Electronics, Printing & Packaging, Pharmaceuticals, Others), by Regional Analysis, 2026 - 2033

Propylene Glycol Ether Market Size and Trend Analysis

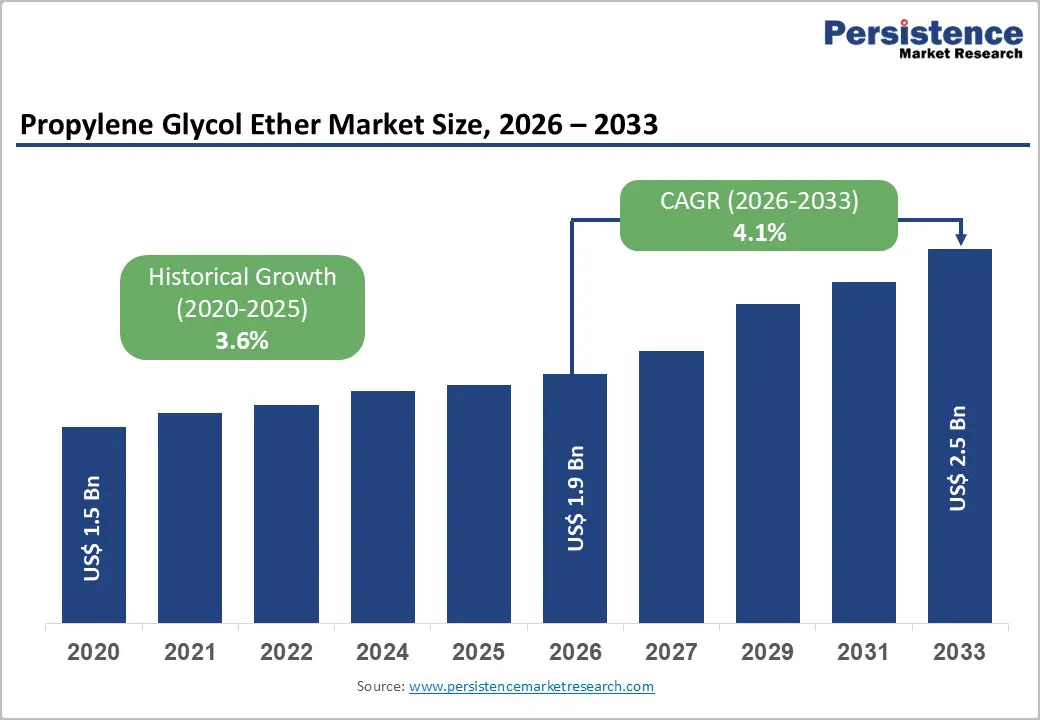

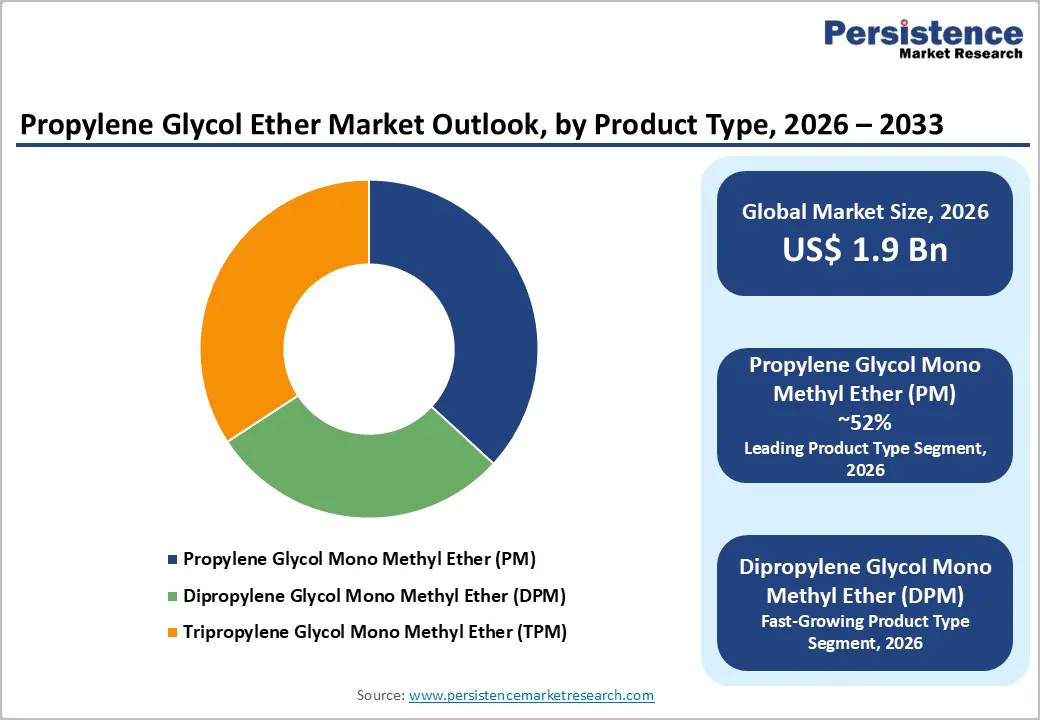

The global Propylene Glycol Ether Market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 4.1% between 2026 and 2033.

Market growth is driven by expanding electronics manufacturing and increasing adoption of sustainable coating solutions. Rising semiconductor fabrication capacity continues to boost demand for high-purity solvents used in advanced electronic processes. In parallel, regulatory shifts toward low-toxicity and environmentally safer solvents are accelerating substitution trends across coatings, inks, and industrial applications. Increased emphasis on green compliance and process efficiency supports steady consumption growth, positioning propylene glycol ethers as preferred solvents across multiple high-value end-use industries.

Key Industry Highlights:

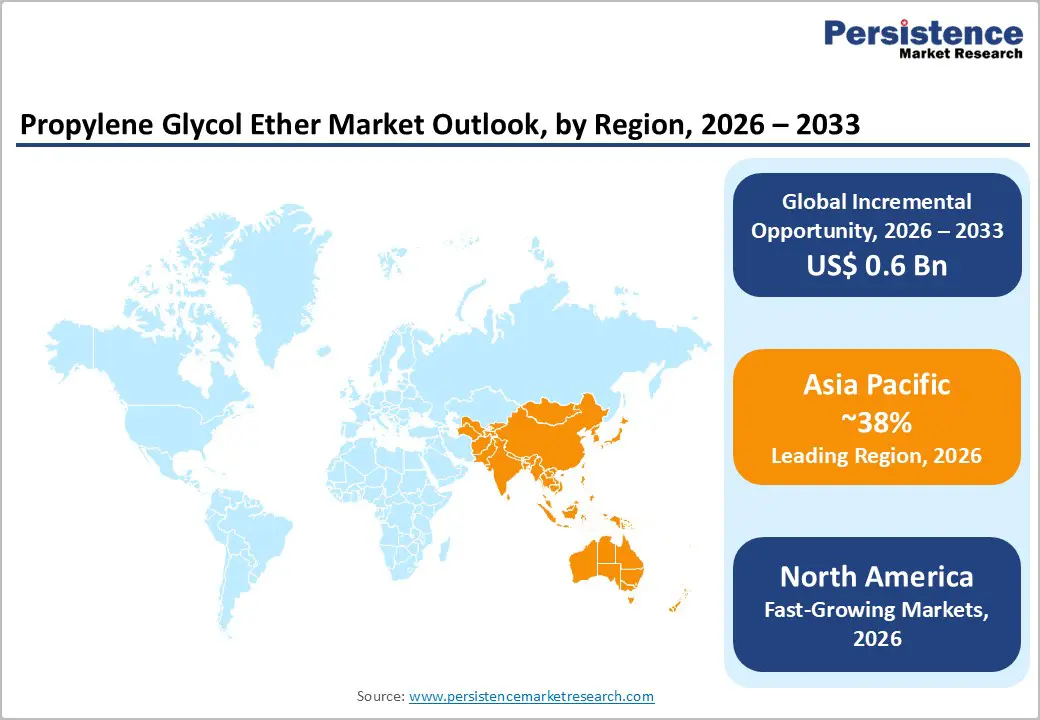

- Leading Region: Asia Pacific leads the propylene glycol ether market with a 38% share in 2025, supported by strong semiconductor manufacturing in China and advanced display production in Japan.

- Fastest-Growing Region: Europe is the fastest-growing regional market, expanding at a ~4.3% CAGR, driven by REACH-led solvent substitution, sustainable coatings adoption, and steady demand from automotive and pharmaceutical industries.

- Leading Product Category: Propylene Glycol Monomethyl Ether (PM) dominates the product landscape with a 52% share in 2025, favored for its balanced evaporation rate and high purity in semiconductor and precision cleaning applications.

- Leading & Fastest-Growing End-Use Category: Electronics remains the largest end-use segment with a 38% share in 2025 and is also the fastest-growing category, supported by advanced semiconductor fabrication, display technologies, and electronics miniaturization.

- Key Market Opportunity: Bio-based propylene glycol ethers represent a major growth opportunity, aligned with renewable chemistry initiatives and long-term sustainability targets driving low-carbon solvent adoption.

| Key Insights | Details |

|---|---|

|

Propylene Glycol Ether Size (2026E) |

US$ 1.9 billion |

|

Market Value Forecast (2033F) |

US$ 2.5 billion |

|

Projected Growth CAGR(2026-2033) |

4.1% |

|

Historical Market Growth (2020-2025) |

3.6% |

Market Dynamics

Drivers - Rising Semiconductor Production and Advanced Electronics Manufacturing Demand

Global semiconductor investments are accelerating demand for propylene glycol ethers, particularly for precision cleaning and photoresist applications. Expanding fabrication capacity, especially in Asia, is increasing consumption of high-purity solvents required for advanced lithography and etching processes. Their low residue, controlled evaporation, and compatibility with sensitive substrates make them critical inputs in next-generation semiconductor nodes.

Continued growth in electronics manufacturing, including TFT-LCD panels, memory chips, and logic devices, further reinforces solvent demand. As device architectures shrink and process complexity rises, manufacturers prioritize solvents that ensure yield optimization and defect reduction. This positions propylene glycol ethers as indispensable materials supporting sustained volume growth across the evolving global semiconductor and electronics value chain.

Stringent Low-VOC Regulations and Shift Toward Sustainable Coatings

Tightening VOC emission regulations are driving widespread adoption of propylene glycol ethers in paints, coatings, and printing inks. Regulatory frameworks in Europe and North America are pushing formulators toward low-toxicity, low-VOC solvent systems. Propylene glycol ethers function effectively as coalescing agents, enabling water-borne coatings to achieve uniform film formation without compromising performance.

The transition toward environmentally compliant coatings is accelerating across architectural, industrial, and automotive applications. Rapid urbanization and construction activity in emerging economies further amplify demand for sustainable coating solutions. As manufacturers increasingly reformulate products to meet regulatory and environmental standards, propylene glycol ethers continue to gain preference, ensuring steady demand growth driven by sustainability and compliance requirements.

Restraints - Raw Material Price Volatility and Petrochemical Feedstock Dependence

Propylene glycol ether production is highly dependent on petrochemical feedstocks, particularly propylene, making the market vulnerable to crude oil price swings and supply disruptions. Geopolitical tensions, refinery outages, and logistics constraints directly translate into feedstock cost volatility, increasing production uncertainty. Sudden price spikes significantly affect procurement planning and long-term supply contracts across the value chain.

Rising raw material costs compress margins, especially for small and mid-sized manufacturers with limited pricing power. Volatility also discourages capacity expansion and investment in price-sensitive end-use sectors such as packaging, cleaners, and general industrial formulations. As a result, cost instability acts as a structural restraint, limiting wider adoption and slowing growth in emerging and cost-conscious markets.

Environmental and Health Scrutiny on Glycol Ether Derivatives

Despite a safer profile compared to ethylene glycol ethers, certain propylene glycol ether derivatives remain under regulatory and toxicological scrutiny. Environmental and chemical safety authorities require extensive testing, registration, and documentation to assess reproductive and long-term exposure risks. Compliance with these frameworks significantly increases time-to-market and regulatory costs for manufacturers.

Additional expenses related to reformulation, labeling, and toxicological validation discourage adoption in highly regulated sectors such as pharmaceuticals and personal care. Smaller producers, in particular, face financial strain from compliance investments, limiting innovation and portfolio expansion. This ongoing regulatory pressure restrains broader market penetration, even as demand shifts toward comparatively safer solvent alternatives.

Opportunity - Shift Toward Bio-Based Feedstocks and Sustainable Solvent Solutions

Growing emphasis on sustainability is creating opportunities for bio-based propylene glycol ethers derived from renewable feedstocks. Advances in bio-propylene and glycerin-based production routes significantly reduce carbon emissions while aligning with global decarbonization targets. Policy support and incentive programs are accelerating pilot-scale and commercial adoption of renewable solvent technologies across key regions.

Electronics, coatings, and specialty chemical manufacturers increasingly seek traceable, low-carbon solvents to meet corporate ESG goals and circular economy requirements. Bio-based propylene glycol ethers offer differentiation through reduced environmental impact without compromising performance. As regulatory and customer pressure for sustainable inputs intensifies, renewable feedstock integration presents a compelling growth avenue for market participants.

Rising Demand from Advanced Display and Next-Generation Electronics Technologies

Expansion of advanced display technologies such as TFT-LCD and OLED is generating strong demand for high-purity propylene glycol ether grades. These solvents are essential in photoresist stripping, developing, and precision cleaning processes where contamination control and yield optimization are critical. Increasing panel complexity and resolution further elevate purity and performance requirements.

Growth in 5G infrastructure, smart devices, and connected electronics is reinforcing demand across the display supply chain. Manufacturing capacity expansion in emerging Asian hubs supports long-term consumption growth. This creates premium market opportunities for suppliers capable of delivering ultra-high-purity, application-specific solvent grades tailored to advanced electronics manufacturing needs.

Category-wise Analysis

Product Type Insights

Propylene Glycol Monomethyl Ether (PM) emerged as the leading product type, accounting for 52% market share in 2025. Its balanced evaporation rate and high solvency make it particularly suitable for electronics cleaning and precision processes. High-purity grades support sub-micron residue removal, reinforcing strong adoption across semiconductor and advanced manufacturing applications.

The fastest-growing product segment includes higher-purity and specialty propylene glycol ether variants tailored for advanced electronics and environmentally compliant formulations. Rising demand for application-specific solvents in semiconductor fabrication, display manufacturing, and sustainable coatings is driving innovation beyond conventional grades, supporting accelerated uptake of next-generation and customized ether products.

Application Insights

Solvent applications dominated the market with a 48% share in 2025, driven by extensive use across coatings, inks, and industrial cleaners. Their versatility, compatibility with waterborne systems, and lower toxicity profile compared to ethylene glycol ethers have strengthened adoption across regulated and high-volume industrial applications.

The fastest-growing application area is electronics and specialty processing, where propylene glycol ethers are increasingly used in precision cleaning, photoresist processing, and surface preparation. Advancements in semiconductor nodes, display technologies, and electronics miniaturization continue to expand solvent performance requirements, accelerating demand in high-value, technology-driven applications.

Industry Insights

The electronics industry led the market with a 38% share in 2025, supported by rising semiconductor fabrication and display manufacturing activity. Propylene glycol ethers play a critical role in lithography, etching, and cleaning processes, making them indispensable inputs across integrated circuit and panel production facilities.

The fastest-growing end-use segment is advanced electronics manufacturing, including next-generation semiconductors, displays, and communication devices. Increasing process complexity, higher purity requirements, and expansion of electronics manufacturing capacity in emerging hubs are driving sustained demand, reinforcing strong growth potential across technology-intensive end-use industries.

Regional Insights

North America Propylene Glycol Ether Market Trends

North America accounted for approximately 34% of the global propylene glycol ether market share in 2025, led by the United States. Strong semiconductor investments supported by federal incentives are expanding fabrication capacity, while stringent VOC regulations are accelerating the shift toward waterborne coatings. Demand remains concentrated in electronics, industrial coatings, and high-performance solvent applications.

The region also benefits from continuous innovation and capacity expansions by major chemical producers supplying high-purity grades. Advanced R&D ecosystems, particularly in technology hubs, are driving development of application-specific solvents for AI chips and next-generation electronics. This combination of regulatory support, technology leadership, and domestic manufacturing strengthens North America’s sustained market position.

Europe Propylene Glycol Ether Market Trends

Europe represents a mature yet steadily expanding market, supported by strong demand from automotive coatings, pharmaceuticals, and construction applications. Germany remains a key contributor due to high vehicle production, while France’s pharmaceutical manufacturing growth supports solvent demand in regulated formulations. The region’s focus on sustainability strongly influences solvent selection.

The European propylene glycol ether market is projected to grow at a CAGR of around 4.3% during the forecast period, driven by REACH compliance and the EU Green Deal. Increasing substitution of conventional solvents with low-toxicity alternatives and continued infrastructure development across Southern Europe underpin consistent growth prospects across multiple end-use industries.

Asia Pacific Propylene Glycol Ether Market Trends

Asia Pacific dominated the global market with an estimated 38% share in 2025, driven by rapid expansion in semiconductor manufacturing, display technologies, and industrial production. China leads regional demand due to strong electronics output, while Japan’s advanced TFT-LCD and semiconductor industries sustain high consumption of high-purity solvent grades.

The region continues to benefit from manufacturing cost advantages, government incentives, and expanding electronics supply chains. India’s production-linked incentive programs and the rise of ASEAN manufacturing hubs are strengthening downstream demand. These dynamics position Asia Pacific as the fastest-expanding and most strategically important region for propylene glycol ether consumption.

Competitive Landscape

The propylene glycol ether market is moderately consolidated, characterized by strong vertical integration across feedstock sourcing, production, and downstream distribution. Leading participants focus on operational efficiency, scale advantages, and long-term supply agreements to serve electronics, coatings, and industrial customers. Strategic investments increasingly prioritize process optimization and portfolio alignment with low-toxicity and environmentally compliant solvent systems.

Competitive differentiation is driven by the ability to deliver ultra-high-purity grades for electronics applications and customized solvent blends meeting specific VOC regulations. Capacity expansion in Asia, renewable feedstock integration, and digitalized supply chain management are emerging as key strategic trends. Collaborative ventures and technology partnerships further support innovation, resilience, and long-term market positioning.

Key Developments:

- In April 2025, Dow opened a new bio-based propylene glycol ether production facility in Texas, strengthening its sustainable solvent portfolio. The plant leverages renewable feedstocks to reduce lifecycle carbon emissions by nearly 40%, supporting low-VOC coatings and electronics applications.

- In June 2024, LyondellBasell expanded its propylene glycol ether production capacity in Asia by 15% to meet rising demand from display and semiconductor manufacturers. The expansion enhances supply reliability for high-purity solvent grades used in advanced TFT-LCD and OLED fabrication.

- In February 2024, INEOS introduced a new pharmaceutical-grade propylene glycol monomethyl ether compliant with stringent REACH requirements. The launch targets regulated pharmaceutical and personal care formulations, addressing demand for low-toxicity, high-purity solvents in sensitive applications.

Companies Covered in Propylene Glycol Ether Market

- Dow Inc.

- BASF SE

- LyondellBasell Industries

- Eastman Chemical Company

- Shell Chemicals

- Huntsman Corporation

- INEOS Group

- Sasol Limited

- SKC Co., Ltd.

- KH Neochem Co., Ltd.

- Chang Chun Group

- LG Chem Ltd.

- Mitsubishi Chemical Corporation

- India Glycols Limited

- Jiangsu Dynamic Chemical Co., Ltd.

Frequently Asked Questions

The propylene glycol ether market is expected to reach US$ 1.9 billion in 2026 and grow to US$ 2.5 billion by 2033, registering a 4.1% CAGR, driven mainly by electronics and sustainable solvent demand.

Key drivers include expanding semiconductor fabrication, advanced display manufacturing, and rising adoption of low-VOC coatings enabled by regulatory-led solvent substitution.

Asia Pacific leads with a 38% market share in 2025, supported by strong semiconductor manufacturing in China and advanced TFT-LCD and electronics production in Japan.

Bio-based propylene glycol ethers offer a major opportunity, aligning with renewable chemistry initiatives and supporting low-carbon, sustainable solvent demand in electronics and coatings.

Dow, LyondellBasell, INEOS, Shell, Eastman, BASF, KH Neochem lead via expansions and innovations.