- Medical Devices

- Pressure Relief Devices Market

Pressure Relief Devices Market Size, Share, and Growth Forecast for 2025 - 2032

Pressure Relief Devices Market by Product Type (High-tech Pressure Relief Devices, Low-tech Pressure Relief Devices), By End-user (Hospitals, Long Term Care Centers, Rehabilitation Centers, Home Care Settings), and Regional Analysis for 2025 - 2032

Pressure Relief Devices Market Size and Trends

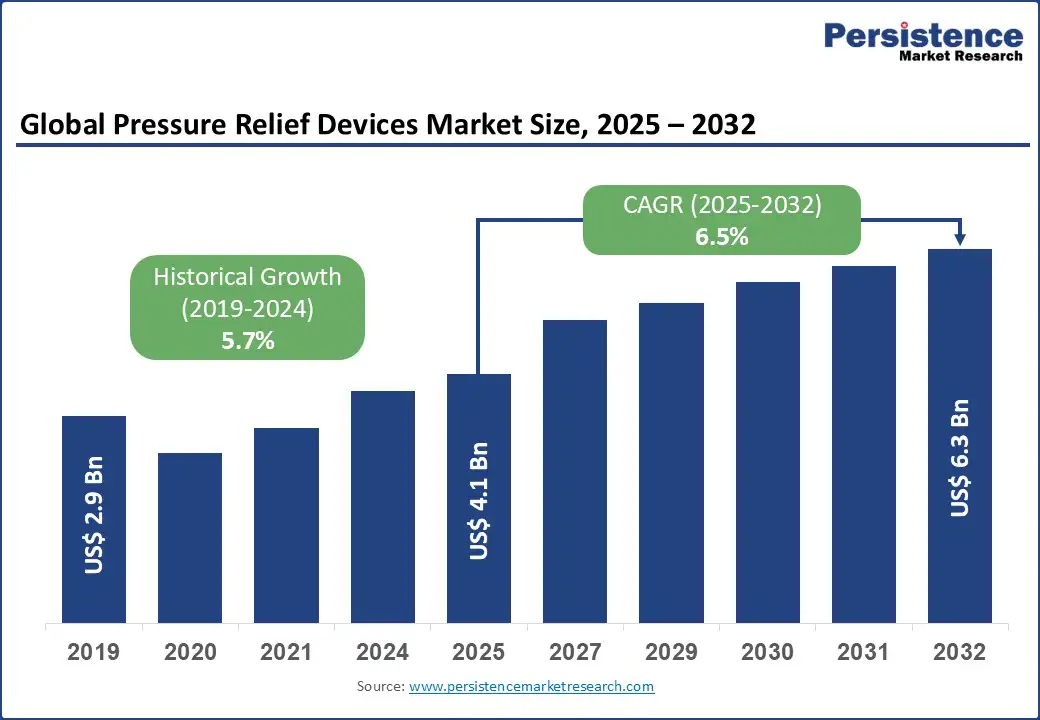

The global pressure relief devices market size is likely to value at US$ 4.1 Bn in 2025 and is projected to reach US$ 6.3 Bn by 2032, expanding at a CAGR of 6.5% during the forecast period 2025 - 2032, driven by rising prevalence of pressure ulcers, stricter healthcare regulations promoting patient safety, and increasing adoption of advanced therapeutic surfaces across hospitals and long-term care centers.

Key Industry Highlights:

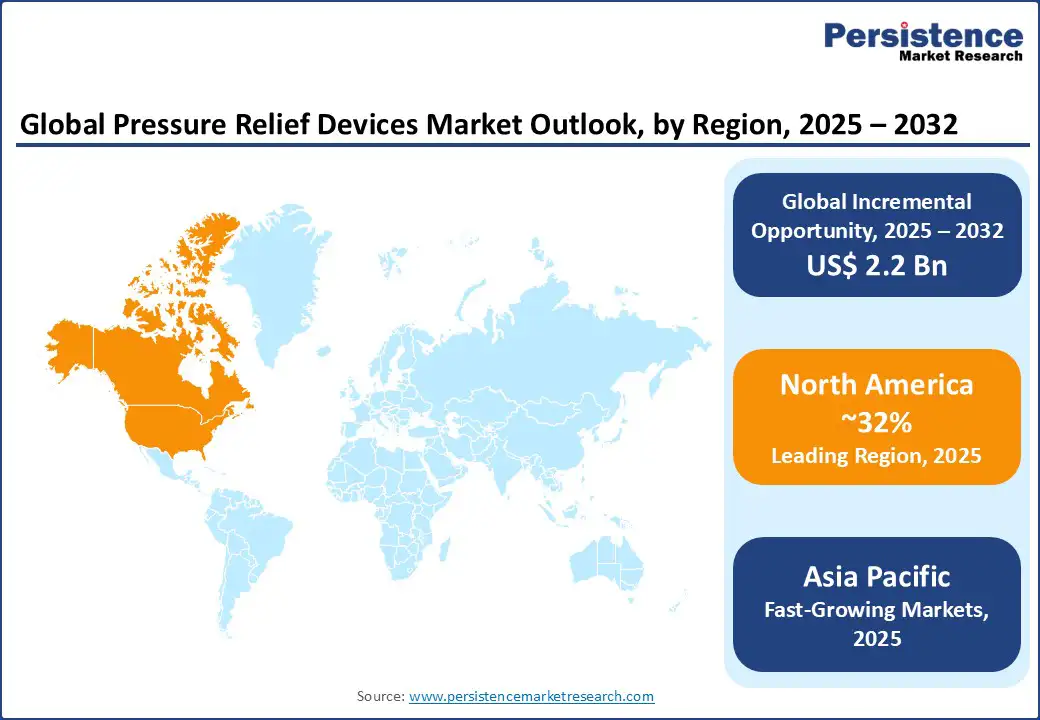

- Leading Region: North America leads with a 32% share in 2025, driven by advanced healthcare infrastructure, higher awareness of pressure ulcer prevention, and strong reimbursement policies that encourage adoption of both high-tech and low-tech devices.

- Fast-growing Region: Asia Pacific is the fastest-growing region, projected at over 7.8% CAGR, fueled by rising geriatric populations, increasing healthcare investments, and expanding home care adoption, particularly in China, India, and Japan, where cost-effective low-tech solutions remain dominant.

- Leading Product: Low-tech pressure relief devices hold the major share at around 65% in 2025, with foam-based mattresses as the fastest-growing sub-segment at a 7.2% CAGR. Their affordability, ease of use, and alignment with standard care protocols drive widespread adoption across hospitals, long-term care centers, and home care, while high-tech beds gradually gain traction.

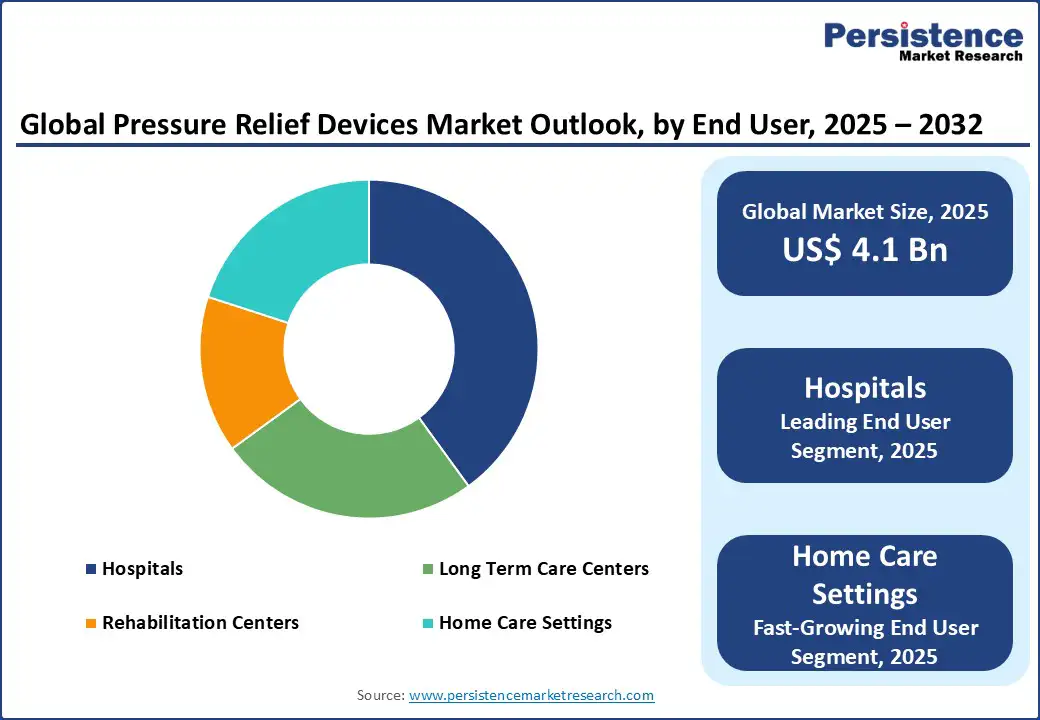

- Fast-growing End-user segment: Hospitals remain the dominant application segment, contributing over 40% of demand, supported by stringent patient safety protocols, mandatory use of pressure-relieving surfaces in ICUs, and rising surgical volumes requiring long-duration post-operative care solutions.

- Air-fluidized beds are the fastest-growing sub-segment of high-tech pressure relief devices, registering a CAGR of 5.8% in the forecast period. Growth is driven by technological innovation and improved clinical outcomes in critical care.

| Key Insights | Details |

|---|---|

|

Pressure Relief Devices Market Size (2025E) |

US$ 4.1 Bn |

|

Market Value Forecast (2032F) |

US$ 6.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.7% |

Market Factors - Growth, Barrier, and Opportunity Analysis

Growing Pressure Ulcer Cases and Smarter Therapeutic Surfaces Boost Device Demand Worldwide

The growing burden of pressure ulcers worldwide has become a critical factor shaping demand for pressure relief devices. Hospitals, long-term care centers, and home care providers are increasingly prioritizing effective prevention and management solutions, as untreated pressure injuries significantly extend recovery time and elevate healthcare costs. Advances in therapeutic surfaces, including air-fluidized systems, low-air-loss mattresses, and hybrid smart devices, are improving patient outcomes while also easing caregiver workload. These innovations, combined with stricter safety standards in clinical settings, are steadily expanding the global adoption base.

Evidence from international health organizations underscores the urgency of this demand. The World Health Organization (WHO) estimates that pressure ulcers affect around 8–10% of hospitalized patients globally, highlighting the scale of the issue. In the United States alone, the Agency for Healthcare Research and Quality (AHRQ) reports that 2.5 million patients develop pressure ulcers annually, generating treatment costs exceeding US$11 billion. Meanwhile, European Pressure Ulcer Advisory Panel (EPUAP) guidelines emphasize the use of specialized support surfaces in at-risk populations, reinforcing the regulatory and clinical momentum behind the adoption of advanced pressure relief technologies.

Restraint - Uneven Guidelines and Patchy Reimbursements Slow Adoption and Sales

Limited standardization across clinical guidelines and variability in reimbursement policies remain two major barriers restraining market expansion. In many regions, particularly in the Asia Pacific and parts of Latin America, pressure ulcer prevention protocols are inconsistently applied, leading to uneven demand for advanced devices across healthcare facilities. This lack of uniform adoption slows scaling opportunities for manufacturers and reduces incentives for investment in innovation.

Reimbursement structures for pressure relief devices differ significantly between countries, with some systems covering only basic mattresses and excluding higher-value technologies such as air-fluidized or low-air-loss systems. These policy gaps not only limit hospital purchasing power but also discourage long-term care and home care providers from investing in premium solutions, directly impacting global sales growth despite rising clinical need.

Opportunity - Smart, Sensor-Enabled Mattresses Unlock Better Care and Efficiency Across Healthcare Settings

Increasing digitalization and integration of smart technologies in healthcare unlocks significant growth opportunity for the pressure relief devices market. Sensor-enabled mattresses and overlays that monitor patient movement, pressure distribution, and alert caregivers in real time are transforming preventive care. Such innovations not only improve clinical outcomes but also optimize staff efficiency and resource allocation in hospitals and long-term care facilities. The convergence of IoT, AI-driven analytics, and cloud-based monitoring is expected to drive broader adoption, particularly in regions emphasizing value-based healthcare and patient safety.

Governments and healthcare authorities are actively supporting this shift. For instance, the U.S. Centers for Medicare & Medicaid Services (CMS) incentivizes hospitals for reduced pressure ulcer incidence, indirectly encouraging investment in smart therapeutic surfaces. Leading manufacturers, including Hill-Rom and Invacare, are expanding their portfolios to include sensor-integrated mattresses and connected care platforms, demonstrating the commercial viability of digital solutions. These combined policy and industry initiatives signal a clear pathway for accelerated market growth, especially in technologically advanced and cost-conscious care environments.

Category-wise Analysis

Product Type Insights - Low-Tech Devices Dominate, but Foam-Based Mattresses Set the Pace for Growth

Low-tech pressure relief devices lead with a 65% share in 2025, supported by strong adoption in hospitals, long-term care centers, and home care due to affordability and ease of use. Foam-based mattresses are the fastest-growing sub-segment. This growth is driven by their compatibility with standard care protocols and an increasing use in home care settings. Gel- and fiber-filled mattresses maintain steady demand as healthcare providers focus on patient comfort and moderate pressure redistribution.

The air fluidized beds sub-segment of High-tech Pressure Relief Devices is experiencing a growth rate of 5.8% CAGR in the forecast period. These devices are getting adopted in critical care and rehabilitation settings as manufacturers incorporate smart pressure monitoring and low-air-loss technologies. These advancements enhance preventive care and operational efficiency. By integrating these innovations, healthcare providers can better meet regulatory standards and improve patient outcomes across all care settings.

End-user Insights - Hospitals Anchor Demand, While Home Care Emerges as the Fastest Expanding End-Use Segment

Hospitals remain the largest end-user segment in 2025, holding around 40% market share, driven by high patient volumes, advanced wound care protocols, and institutional budgets that prioritize pressure ulcer prevention. Their adoption is further supported by government quality mandates and hospital-acquired pressure injury reduction programs. Home care settings, however, are the fastest-growing segment fueled by the rising geriatric population, increasing chronic illness management at home, and reimbursement policies favoring cost-effective care.

Long-term care centers continue to demonstrate steady expansion, as aging populations and nursing home networks integrate low-tech mattresses for preventive care. Rehabilitation centers are gradually incorporating advanced beds to improve recovery outcomes, holding comparatively less share. This balanced adoption across End-users reflects shifting healthcare models where institutional strength and home-based innovation both play critical roles in shaping demand.

Regional Insights

Asia Pacific Pressure Relief Devices Market Trends - Leader in Global Growth with Expanding Healthcare Infrastructure and Policy Support

Asia Pacific represents 27% of the global pressure relief devices market in 2025 and continues to expand at the fastest CAGR of 7.8% in the forecast period. China leads with strong government backing for hospital upgrades and advanced wound management initiatives. In 2024, Baxter (Hillrom) introduced its Centrella® Smart+ bed and advanced mattress systems in Chinese healthcare facilities, designed to meet local patient mobility challenges, showcasing how global players are tailoring solutions to regional needs. India is emerging as the next growth hub, with the Ayushman Bharat program enabling wider access to pressure ulcer prevention devices, while domestic manufacturers are scaling up foam- and gel-based mattress production to match rising demand.

Japan and South Korea highlight the premium end of the spectrum, where regulatory emphasis on quality and digital healthcare integration has spurred early adoption of high-tech air-fluidized and kinetic beds. Southeast Asia, particularly Indonesia and Malaysia, is increasingly investing in cost-efficient devices for private hospitals and home care, with procurement programs encouraging wider uptake. This layered demand, from critical care beds in developed markets to affordable overlays in emerging economies, demonstrates Asia Pacific’s unique role as both a volume-driven and innovation-led growth engine.

North America Pressure Relief Devices Market Trends - Market Leadership with Strong Clinical Adoption and Advanced Care Standards

North America accounts for 32% of the global pressure relief devices market in 2025, advancing at a steady CAGR of 6.3%. The United States dominates regional demand, driven by strict prevention protocols for hospital-acquired pressure injuries and significant healthcare spending. In 2023, Arjo launched its Citadel™ patient care system across U.S. hospitals, integrating smart monitoring to enhance patient safety and operational efficiency, underscoring the region’s leadership in digitalized care solutions.

Canada is steadily emerging as a growth contributor, supported by federal investments in elderly care and nationwide pressure injury prevention programs within long-term care facilities. Rising obesity rates and chronic illness prevalence further accelerate the need for advanced pressure redistribution technologies. With strong regulatory oversight, patient-centric care standards, and continuous product rollouts from global leaders, North America maintains its role as a strategic hub for high-tech innovation and large-scale adoption in the pressure relief devices market.

Europe Pressure Relief Devices Market - Policy Support and Technological Upgrades

Europe is poised to represent a 29% in 2025, underscoring its strong role in shaping industry progress. Germany leads the region, supported by advanced healthcare infrastructure and comprehensive reimbursement frameworks that prioritize pressure ulcer prevention. In 2024, LINET Group expanded its German portfolio with enhanced therapeutic beds designed for improved patient mobility and safety, reflecting the region’s push toward embedding innovation into routine hospital care. The United Kingdom continues to stand out through NHS-led initiatives, where national guidelines encourage early pressure injury intervention and favor cost-efficient low-tech mattresses across hospitals and care homes.

France and Italy’s aging populations sustain demand in long-term and home care, while Scandinavian countries demonstrate higher adoption of high-tech air-fluidized and kinetic beds in specialized facilities, supported by strict quality standards. With structured reimbursement policies and consistent investment in eldercare services, Europe maintains a balanced growth trajectory that combines affordability, accessibility, and innovation-driven adoption.

Market Competitive Landscape

Manufacturers of global pressure relief devices market are innovating with smart monitoring beds, hybrid mattresses, and ergonomic designs that adhere to strict clinical standards. Growth strategies are focusing on emerging markets with rising healthcare investments, encouraging healthy competition aimed at improving outcomes rather than competing on price. Reliable sourcing of specialized materials and the expansion of digital platforms and regional alliances enhance product availability, positioning the market for sustainable, patient-centered growth.

Key Industry Developments

- In June 2023, Baxter International (Hillrom brand) launched the Progressa+ ICU bed in the U.S., offering enhanced skin protection and support surfaces designed to reduce pressure injuries and ease caregiver workflow. The system integrates advanced mobility and monitoring features, making it one of the most comprehensive ICU beds on the market.

- In Sep 2021, Baxter International completed a US$10.5 billion acquisition of Hillrom, expanding its capabilities in connected care and pressure relief innovations across the healthcare continuum. This acquisition positioned Baxter as a global leader in advanced hospital beds and therapeutic surfaces, strengthening its product portfolio for critical and chronic care.

Companies Covered in Pressure Relief Devices Market

- Arjo (formerly ArjoHuntleigh)

- Hill-Rom Holdings (Baxter International)

- Invacare Corporation

- Paramount Bed Co., Ltd.

- 3M Health Care

- Essity Health & Medical (Essity AB)

- Smith & Nephew

- Stryker Corporation

- Talley Group Ltd.

- Acelity

- Drive DeVilbiss Healthcare

- French Medical

- Roho

- Medtronic

- B. Braun SE

Frequently Asked Questions

The pressure relief devices market is set to reach US$ 4.1 Bn in 2025.

Rising incidence of pressure ulcers, coupled with advancements in smarter therapeutic surfaces, is driving significant global demand for pressure relief devices.

The industry is estimated to rise at a CAGR of 6.5% from 2025 to 2032.

Smart, sensor-enabled mattresses and connected care solutions are unlocking better patient outcomes and operational efficiency across diverse healthcare settings.

The major players dominating the pressure relief devices market are Arjo, Hill-Rom Holdings, Invacare Corporation, Paramount Bed Co., Ltd., 3M Health Care, Essity Health & Medical, Smith & Nephew.