- Industrial Machinery

- Gas Pressure Regulator Market

Gas Pressure Regulator Market Size, Share, and Growth Forecast for 2025 - 2032

Gas Pressure Regulator Market By Product type (Low Pressure (0-20 psi), Medium Pressure (20-100 psi) and High Pressure (100-1000 psi), Gas Type (Brass, Stainless Steel, Cast Iron and Plastic), End-user (Industrial Manufacturing, Oil & Gas Production, Healthcare, Water Treatment), and Regional Analysis from 2025 to 2032

Gas Pressure Regulator Market Size and Share Analysis

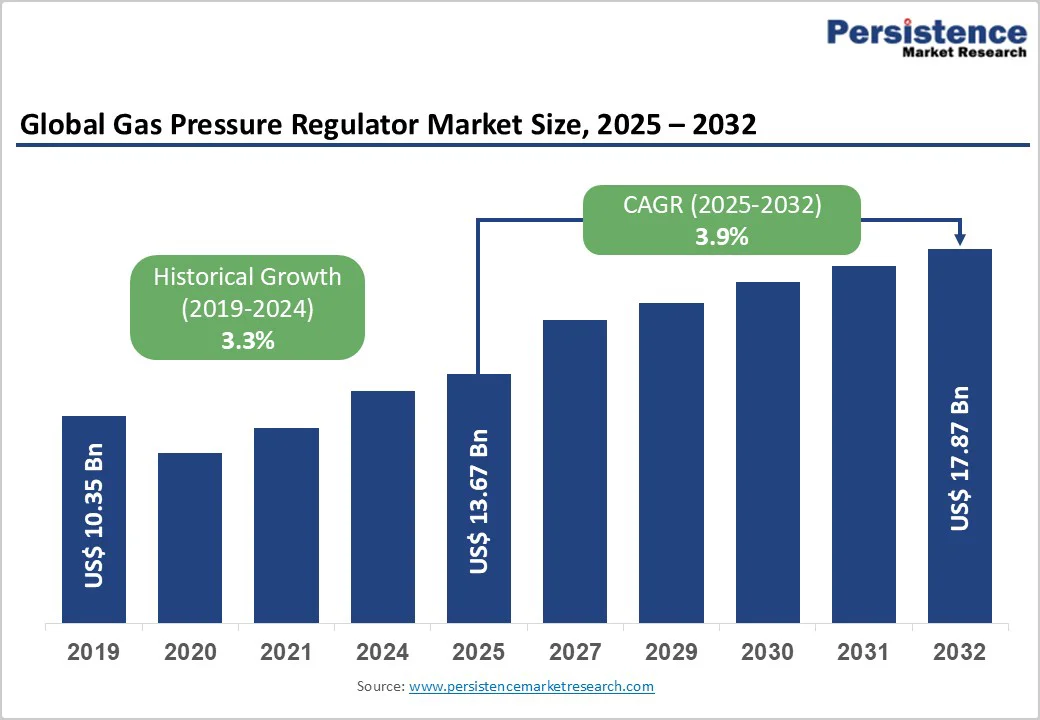

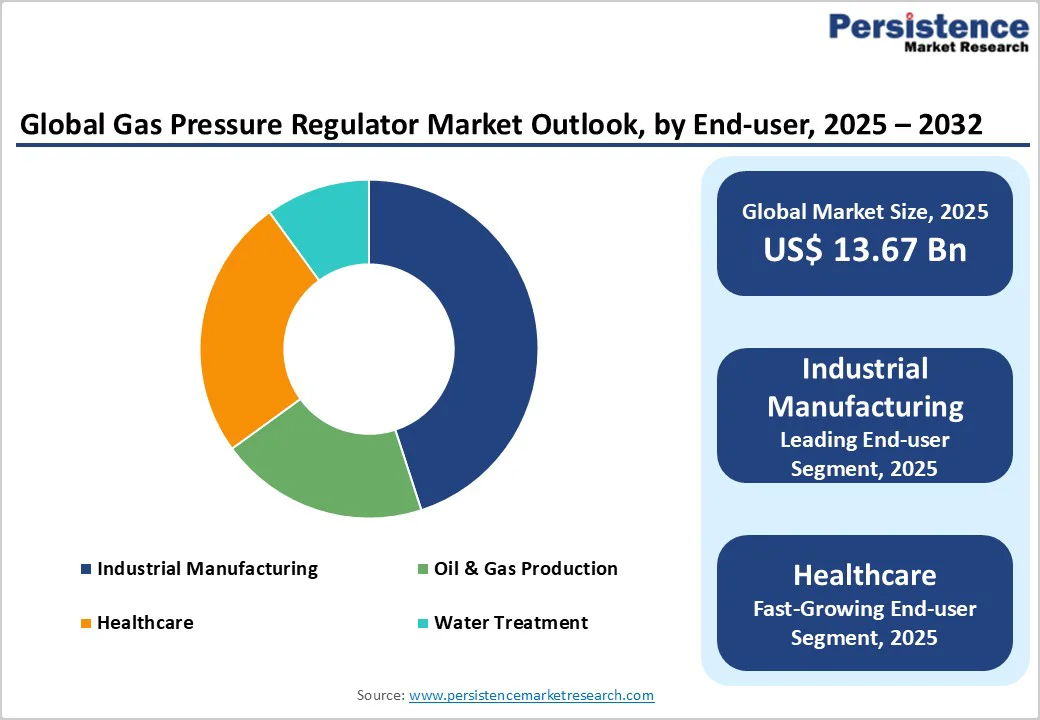

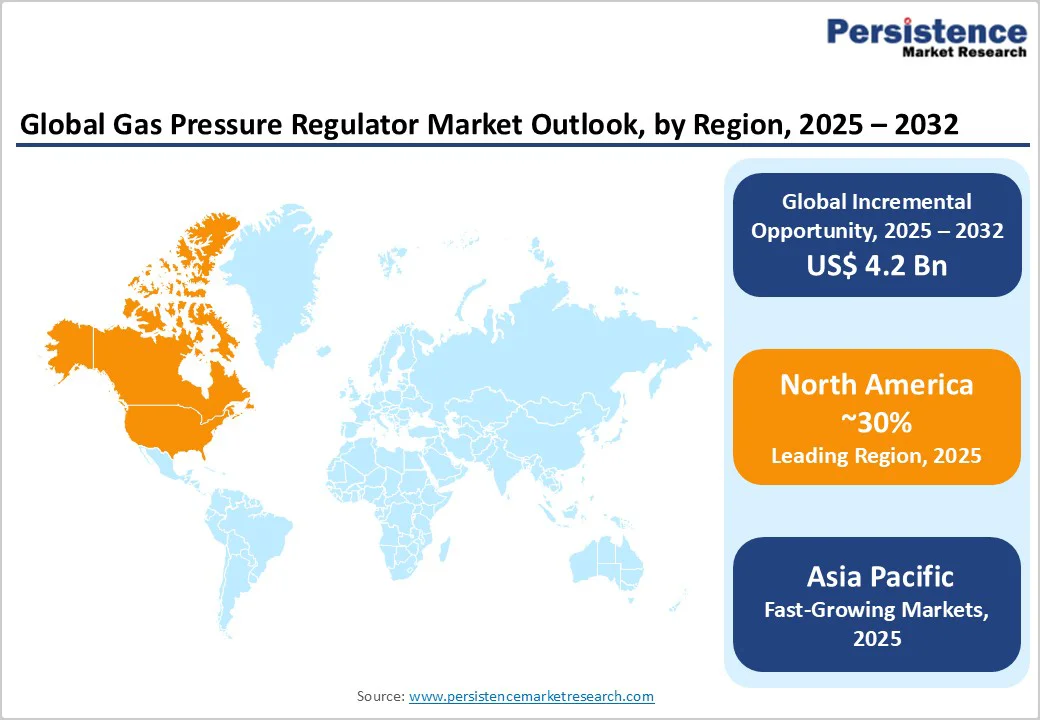

The global gas pressure regulator market size is likely to be valued at US$13.67 billion in 2025 and is projected to reach US$17.87 billion by 2032, growing at a CAGR of 3.9% between 2025 and 2032. The demand grows due to investments in new gas infrastructure, expanding industrial base in Asia-Pacific, and regulatory requirements for process safety. Key growth enablers include technological innovation, uptake across healthcare and water treatment, and transition to low-carbon energy sources.

Key Industry Highlights:

- Leading Region: North America leads the global gas pressure regulators market with an estimated 26.3% share in 2025, supported by strong demand from industrial manufacturing, oil & gas, and healthcare sectors. The region’s emphasis on process safety, high-performance materials, and precision control systems continues to drive adoption across critical applications such as chemical processing, energy distribution, and medical gas supply.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, accounting for over 39% of new unit installations during the forecast period. Rapid industrialization, infrastructure expansion, and growing healthcare investments in China, India, and Southeast Asia are fueling market acceleration. Government-backed initiatives promoting clean energy and hydrogen infrastructure further enhance regional growth prospects.

- Dominant Pressure Range: Low-pressure regulators dominate the market with a 37.3% share in 2025, driven by widespread use in residential, laboratory, and low-flow industrial applications where stability and accuracy are essential. Meanwhile, the high-pressure regulator segment is projected to post the fastest growth rate due to increasing adoption in energy, aerospace, and industrial gas systems requiring superior performance and safety.

- Material Leadership: Brass regulators hold approximately 34.1% of the global share, favoured for their cost-effectiveness and compatibility with a wide range of gases. However, the stainless-steel regulator segment is anticipated to grow at the fastest rate, propelled by rising demand for corrosion-resistant, high-purity, and hydrogen-compatible systems in semiconductor and healthcare applications.

- End-Use Industry Leadership: The industrial manufacturing sector maintains dominance with a 45.3% market share, driven by process control applications in metalworking, chemical production, and equipment manufacturing. The healthcare sector is forecast to record the highest CAGR of 5.1%, supported by expanding medical gas infrastructure and increased demand for precision flow control in hospitals and laboratories.

- Technological Advancement: The market is advancing through smart regulator technologies, digital pressure control systems, and hydrogen-ready designs. Key developments include Emerson’s ER5000 electronic regulator launch, Linde’s ultra-high-purity (UHP) product expansion, and the Greenfuel–Ventrex partnership in India (2023–2025), reflecting industry momentum toward automation, sustainability, and clean energy transition.

| Key Insights | Details |

|---|---|

| Gas Pressure Regulator Market Size (2025E) | US$ 13.67 Bn |

| Projected Market Value (2032F) | US$ 17.87 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 3.9% |

| Historical Market Growth Rate (CAGR 2019 to 2023) | 3.3% |

Market Dynamics

Driver - Rising Demand for Innovative Machines Drives the North America Gas Pressure Regulator Market

Global urbanization and industrialization directly increase the need for safe, reliable gas distribution. In 2025, more than 45% of total installations were attributed to new factories and urban projects, notably in China, India, and Southeast Asia. Regulatory mandates established by agencies—including the U.S. Department of Energy (DOE) and China's National Development and Reform Commission—require advanced gas pressure regulators in all new energy and utility development projects, effectively driving year-over-year growth.

Energy Transition & Clean Fuel Initiatives

International efforts to reduce emissions propel natural gas and LPG adoption, with OECD and IEA-backed policies supporting cleaner fuel infrastructure. In 2024, the EU’s “Green Gas Support Scheme” and India’s LPG expansion program contributed to greater market penetration. Approximately 53% of new residential energy connections now utilize regulated natural gas, underscoring sustained demand for pressure management solutions.

Advancements in Digital and Smart Regulator Technology

Technological progress—in AI-driven diagnostics, IoT-enabled remote monitoring, and smart sensors—has transformed reliability and responsiveness. By 2025, nearly 37% of new market entrants will have launched products equipped for digital integration and real-time leak/fault detection. Such features are crucial for compliance in hazardous environments and medical gas delivery.

Restraint - High Upfront Costs and Skilled Workforce Shortfalls

Advanced regulator systems, especially those with smart features, entail considerable initial investment and require specialized installation skills. The shortage of trained technicians and engineers in emerging markets impedes adoption, particularly in rural and small enterprise sectors, resulting in slower rate of technology penetration and higher maintenance costs.

Infrastructure Retrofitting and Regulatory Complexity

Aged pipeline infrastructure in mature markets poses retrofitting challenges, increasing project costs and complicating compliance with diverse international standards. Retrofits of legacy networks in North America and Europe can inflate regulator system costs by up to 15-20%, influencing replacement cycles and leading to delays in large municipal upgrades.

Opportunity - High-Pressure and Hydrogen-Ready Regulators

Fast-growth is expected in the high-pressure segment and for hydrogen-ready devices as new industries (green hydrogen plants, refueling stations) come online. Investments and subsidies are driving a 6.2% CAGR in these segments, which represent actionable opportunities for product differentiation and market capture.

Asia Pacific accounts for more than 39% of gas regulator installations, with rapid deployment in both urban residential and clustered industrial parks. Local governments grant incentives for LPG/CNG conversion, smart metering, and modular pressure control systems—representing scalable opportunity for manufacturers.

Healthcare and Smart Home Adoption

The healthcare segment posts a 5.1% CAGR, spurred by hospital expansions and regulatory standards for medical gas supply. Smart homes increasingly require pressure regulators integrated with home automation, driving new product launches into mainstream consumer electronics and utilities markets.

Category-wise Analysis

Product Type Insights

Low-pressure regulators dominate the market, capturing a 37.3% share in 2025. Their core role is safe home, commercial kitchen, and utility gas delivery. Large-scale adoption is supported by ongoing replacement cycles and regulatory incentives for new builds; resilience and user-friendliness ensure steady volume growth.

High-pressure regulators are the fastest growing segment, reflecting demand for industrial, energy plant, and hydrogen applications. This segment benefits from the expansion of manufacturing and chemical plants using gases under high pressure. Growth is anticipated at over 6.2% CAGR, with industry stakeholders investing in R&D to optimize regulator design for hydrogen and other specialty gases.[2][1]

Gas Type (Material) Analysis

Brass Regulators

Brass regulators are the market share leaders, accounting for 34.1% in 2025. Preferred for their strength, corrosion resistance, and broad applicability in industrial and residential systems, brass remains the standard in multi-gas supply pipelines and utility connections.

Stainless steel, as the fastest growing material segment, is driven by stringent safety and hygiene requirements in healthcare, pharmaceuticals, and chemical manufacturing. Enhanced durability and expanded compatibility push CAGR in this segment above the industry average, notably for clean-room and critical environment installations.

End-use Analysis

Industrial manufacturing represents the largest end-use category, claiming a 45.3% share in 2025. With factories and process industries depending upon controlled gas supply for operational and occupational safety, manufacturers are scaling up regulator installations for diverse production lines.

Healthcare is the fastest growing end-use segment, with a CAGR of 5.1%. The requirement for precise pressure management in oxygen delivery, anesthesia, and laboratory gases is augmented by post-pandemic infrastructure investment and regulatory updates, especially across Southeast Asia and Europe.

Regional Market Insights

North America Gas Pressure Regulator Market Trends

North America is the market leader, attributed to advanced gas distribution network maturity and strict implementation of safety standards (e.g., ANSI Z21, OSHA regulations). The U.S. occupies over 21.3% of global market share, propelled by ongoing infrastructure upgrades, residential conversions to gas heating, and strong industrial output. Canada and Mexico are also experiencing growth, albeit from a smaller base, aided by cross-border regulatory harmonization and trade in gas equipment. Investment in hydrogen blending pilots and smart regulator deployment further underpin future expansion. The region’s competitive landscape is marked by highly consolidated supply chains, with major manufacturers such as Emerson and Honeywell spearheading innovation.

Europe Gas Pressure Regulator Market Trends

Europe follows North America in market size, led by Germany, France, the UK, and Spain. The region’s driving forces are government mandates on energy transition, national incentives for upgrading natural gas grids, and phasing out legacy boilers for hydrogen-ready systems. Germany’s Energiewende program and EU-wide sustainability goals stimulate demand for high-performance, eco-friendly regulators. The healthcare segment is robust, and modular designs for industrial SMEs (small and medium-sized enterprises) are gaining traction. Regulatory advances ensure strong compliance and facilitate transnational market presence, especially in high-value end markets.

Asia Pacific Gas Pressure Regulator Market Trends

Asia Pacific emerges as the fastest growing region, responsible for more than 39% of installations in 2025. China, India, Japan, and ASEAN economies benefit from rapid urbanization, aggressive government incentives for LPG/CNG conversion, and new industrial cluster developments. Growth in smart cities, infrastructure expansion, and robust water treatment investments contribute to record regulator unit installations. The competitive landscape is fragmented, with global leaders focusing on strategic partnerships and local manufacturing to address regulator customization preferences and regulatory diversity.

Competitive Landscape

The Gas Pressure Regulator Market is moderately consolidated, with the top five player Emerson Electric, The Linde Group, Air Liquide, Cavagna Group, and Itron Inc. accounting for about 60-65% of global revenue. The remainder is split among regional specialists and niche market entrants. Leading companies maintain strong competitive positioning via product innovation, comprehensive service contracts, and investment in digital integration. Smaller and new entrants are increasing market fragmentation in selected Asia Pacific and European countries.

Recent Industry Developments:

- In 2024, Emerson Electric, Launched TESCOM ER5000 series, featuring wireless diagnostics and remote setpoint control, targeting industrial and utility segments.

- In 2024, Linde Group, Expanded SPECTRA product line for UHP compatibility; partnered with OEMs for dual-stage regulator rollouts in hydrogen infrastructure projects across Europe and APAC.

- In 2024, Air Liquide, introduced smart regulators for medical and industrial use, including real-time leak detection and performed hospital network retrofits in Southeast Asia.

Companies Covered in Gas Pressure Regulator Market

- Honeywell International

- Air Liquide SA

- Itron Inc.

- Emerson Electric Co.

- Xylem

- Air Products and Chemicals, Inc.

- Rotarex SA

- ESAB

- Watts Water Technologies, Inc.

- Linde plc.

- Matheson Tri-Gas, Inc.

- Medenus Gas-Druckregeltechnik GmbH

- Pietro Fiorentini S.p.a

- Essex Industries, Inc.

- Greggersen Gasetechnik GmbH

Frequently Asked Questions

The Gas Pressure Regulator market is estimated to be valued at US$ 13.67 Bn in 2025.

The key demand driver for the Gas Pressure Regulator market is the rising need for precise pressure control and safety in industrial, energy, and healthcare applications.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the global Gas Pressure Regulator market.

Among the Pressure Range, Low Pressure (0-20 psi) hold the highest preference, capturing beyond 37.3% of the market revenue share in 2025, surpassing other products.

The key players in the Gas Pressure Regulator market are Kennametal Inc., Flow International Corporation, OMAX Corporation, CERATIZIT S.A. and GMA Garnet Pty. Ltd.