- Semiconductor Materials & Components

- Power Supply Unit (PSU) Market

Power Supply Unit (PSU) Market Size, Share, and Growth Forecast, 2025 - 2032

Power Supply Unit (PSU) Market By Device Type (AC-DC Power Supplies, DC-DC Converters, DC-AC Converters, Others), Output Power Range (Less than 50W, Others), Application (Telecommunications, Industrial Automation, Others), and Regional Analysis for 2025 - 2032

Power Supply Unit (PSU) Market Share and Trends Analysis

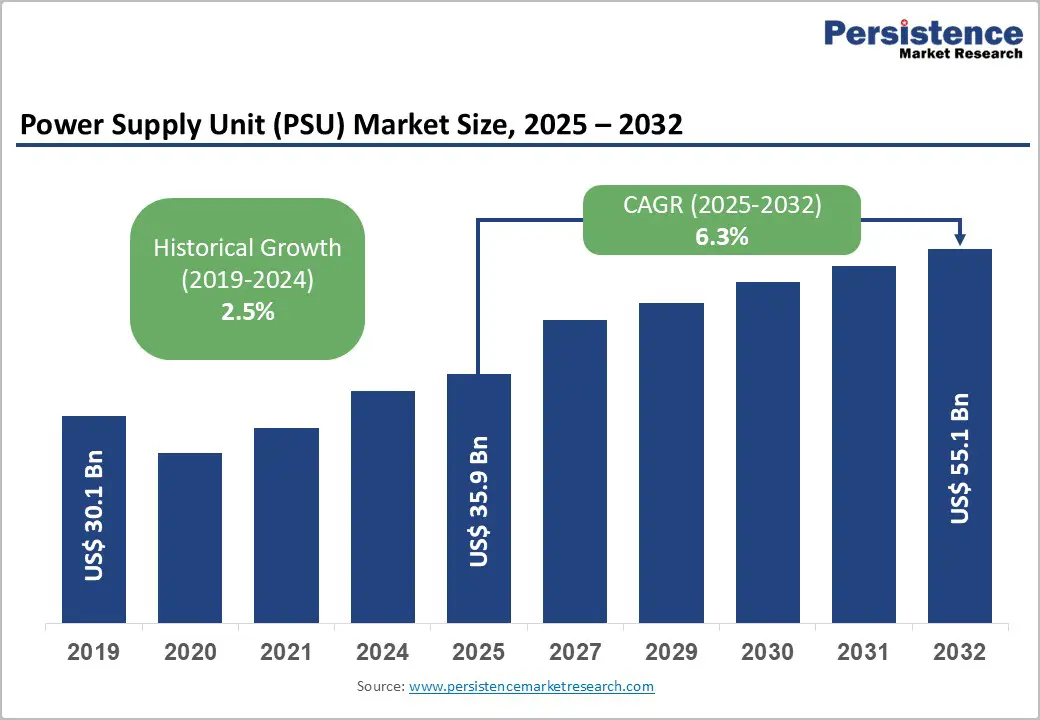

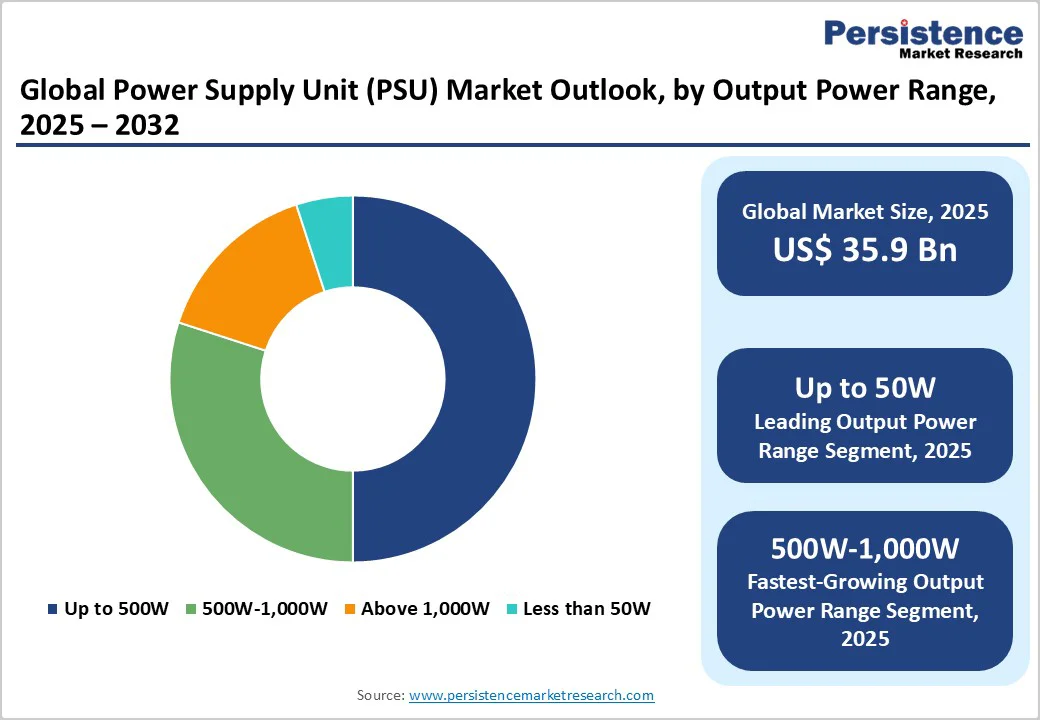

The global power supply unit (PSU) market size is likely to be valued at US$35.9 Billion in 2025, and is estimated to reach US$55.1 Billion by 2032, growing at a CAGR of 6.3% during the forecast period 2025 - 2032, driven by the increasing adoption of energy-efficient power supplies across consumer electronics, industrial automation, and telecommunications, alongside the integration of renewable energy sources and electric vehicle (EV) expansion.

Advances in modular and digitally controlled PSUs, rising data center investments, and the shift to intelligent power systems are driving growth, while energy efficiency regulations and HPC demand further boost the need for scalable, robust PSU solutions.

Key Industry Highlights

- Dominant Device Type: High-wattage AC-DC power supplies hold the leading revenue share of around 45% in 2025.

- Fastest-growing Device Type: DC-DC converters are the fastest-growing segment through 2032, due to soaring demand for EV and renewable energy globally.

- Leading Output Power Range Segments: The up to 500W output power range leads in terms of market share of approximately 50%, while the 500W-1,000W segment is set to grow the fastest between 2025 and 2032.

- Application Scenario: Consumer electronics lead application revenue share with 41% in 2025; industrial automation grows the fastest from 2025 to 2032.

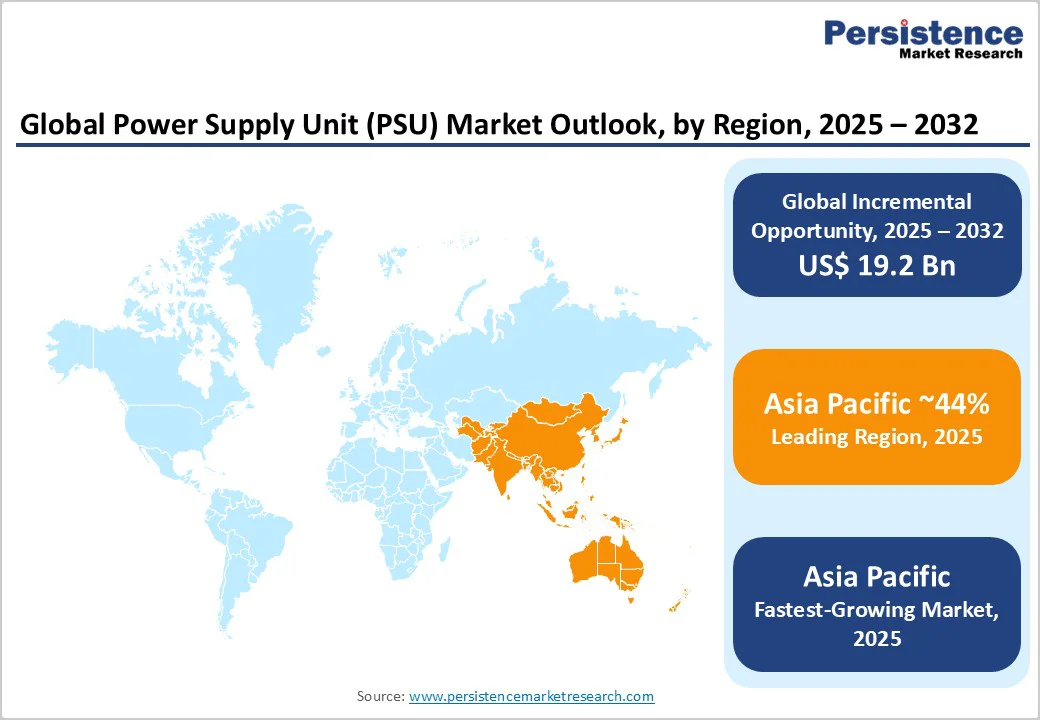

- Regional Dominance: Asia Pacific dominates the global market with a 44% share in 2025, led by China and India.

- Competitive Environment: The market is moderately consolidated, with prominent players competing through innovation in energy-efficient, modular, and AI-integrated PSU technologies to meet increasing demand across data centers, renewable energy, and EV sectors.

- August 2025: NVIDIA unveiled a new AI power supply incorporating Innoscience’s GaN technology, enhancing efficiency and power density for AI workloads, underscoring a growing trend toward advanced semiconductor materials in data center PSUs.

| Key Insights | Details |

|---|---|

| Power Supply Unit (PSU) Market Size (2025E) | US$35.9 Bn |

| Market Value Forecast (2032F) | US$55.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for High-Wattage PSUs in HPC and Gaming Applications

The expanding demand for high-wattage power supply units is fueled profoundly by the growing penetration of high-performance computing, artificial intelligence (AI), and graphics processing units (GPUs) across data centers and consumer gaming markets.

For instance, multi-GPU configurations in gaming rigs and professional workstations necessitate power supply units capable of delivering upwards of 650W with superior efficiency and thermal management. This is further compounded by regulatory emphasis on power efficiency, compelling manufacturers to innovate in modular, 80 PLUS certified designs to meet stringent standards.

With major players enhancing portfolio offerings, including digitally controlled and fully modular PSUs, businesses are responding to both consumer and industrial demand for stable, high-capacity power solutions. The macroeconomic trend of increasing digital infrastructure investments, coupled with sustained growth in the eSports and cloud gaming sectors, underpins significant PSU market expansion opportunities.

Supply Chain Disruptions and Raw Material Volatility

A critical restraint facing the power supply unit market growth stems from supply chain vulnerabilities, particularly volatility in semiconductor and raw material prices, such as copper and rare earth elements essential for transformer and coil manufacturing. Post-pandemic geopolitical tensions and freight challenges have induced a 15-20% cost increase in key components since 2023, squeezing profit margins.

The PSU manufacturing ecosystem also experiences delays due to the complex sourcing of specialized circuitry and certification processes mandated by regulatory bodies such as the U.S. Department of Energy (DOE) and Ecodesign standards of the European Union (EU).

These challenges risk production slowdowns, extending lead times by several weeks, impacting market responsiveness, and limiting the ability to capitalize fully on growing demand. Companies with diversified, localized supply chains and investments in component recycling are better positioned to mitigate these risks, but smaller players face heightened pressure, constraining market expansion.

Renewable Energy Expansion in Developing Markets

Asia Pacific presents one of the most attractive growth opportunities for the PSU market players, driven by robust industrialization and aggressive renewable energy adoption policies in China, India, and ASEAN countries. With China targeting 70 GW of nuclear capacity by 2025 and India accelerating grid modernization, coupled with solar and wind installations surpassing 150 GW, the demand for high-efficiency power supplies in energy generation and distribution infrastructure is surging.

Government incentives aimed at enhancing grid stability and reducing carbon footprints are encouraging the deployment of advanced AC-DC and DC-DC converter technologies, facilitating a shift toward intelligent, remotely managed power supply systems. Business investments focusing on scalable, modular PSUs compatible with smart grids and battery energy storage systems present strategic avenues to capture this expanding market segment.

Category-wise Analysis

Device Type Insights

The AC-DC power supplies segment leads the PSU market with an estimated 45% share in 2025, driven by its widespread use in consumer electronics, industrial machinery, and telecom infrastructure for efficient AC-to-DC conversion.

Stricter regulatory standards, including the U.S. DOE’s MEPS and the EU’s Ecodesign Directive, have prompted manufacturers to innovate with power factor correction, digital controls, and high-efficiency certifications such as 80 PLUS Titanium.

These advancements minimize energy waste, ensure compliance with global energy regulations, and enhance performance, making AC-DC power supplies essential across both mature and emerging markets, supporting the growing demand for reliable and efficient power solutions.

DC-DC converters are poised to be the fastest-growing segment between 2025 and 2032. This rapid growth is primarily driven by the surge in electric vehicles (EVs), renewable energy infrastructure, and data centers that demand efficient voltage regulation and conversion within DC distribution systems.

The advent of battery energy storage systems (BESS), solar photovoltaic (PV) farms, and electrification of transportation fuels the need for compact, modular, and highly efficient DC-DC converters that can handle varying loads while maintaining stability and minimizing losses. Industrial adoption of smart manufacturing techniques also contributes to this growth as factories increasingly rely on precision DC power supplies for automation and robotics.

Output Power Range Insights

The up to 500W segment is likely to lead, holding approximately 50% of the power supply unit market revenue share in 2025, largely due to its relevance to consumer electronics and IoT devices. The proliferation of smartphones, laptops, smart home devices, and wearables ensures consistent volume demand for reliable, low to mid-power PSUs that provide compact form factors and energy savings. The regulatory focus on energy conservation in household and enterprise electronics further consolidates the position of this segment.

The 500W-1,000W output power range is set to be the fastest-growing segment from 2025 to 2032. Growth drivers include expanding industrial applications such as high-power professional gaming PCs, data center server power supplies, and advanced manufacturing equipment requiring higher, stable power delivery.

The need for thermal efficiency and long-term reliability under continuous load conditions compels the development of advanced cooling and modular PSU designs in this power range. The digitization of industrial processes and rising demand for multi-GPU computing clusters additionally accelerate investments in this category.

Application Insights

As of 2025, the consumer electronics segment constitutes the leading application segment with an estimated market share of 41%, fueled by continual innovation and new product introductions in portable devices, home automation, and wearable technologies.

The rising usage of IoT technology across smart cities, connected homes, and personal health accelerates the demand for power supply units for small form factor, energy-efficient models. This segment also benefits from rapid product iterations that require flexible, scalable PSU designs adaptable to diverse use cases.

Industrial automation is projected to be the fastest-growing application through 2032. This growth is attributable to the automation revolution in manufacturing, logistics, and process industries, where reliable and resilient power supplies are critical for robotics, sensors, and control systems.

Investments in Industry 4.0, incorporating real-time monitoring and data analytics, increase reliance on power supplies that ensure minimal downtime and precise electrical performance. The focus on sustainable manufacturing practices also drives demand for energy-saving PSU technologies designed for factory environments.

Regional Insights

North America Power Supply Unit (PSU) Market Trends

North America is expected to command an estimated 30% market share in 2025, primarily backed by the United States’ leadership in digital infrastructure, clean energy initiatives, and advanced manufacturing. A robust regulatory environment, including the Biden Administration’s infrastructure and clean energy plans, has ensured significant investment flows into data centers,

EV charging infrastructure, and military power systems. Innovation ecosystems centered in Silicon Valley and Boston actively foster next-generation PSU technologies, emphasizing modularity, digital control, and AI-driven power management.

The regional competitive landscape features a mix of large multinational power supply unit manufacturers and an increasing number of startups focusing on niche markets such as gaming, aerospace, and health care power solutions.

Investment trends indicate substantial R&D funding directed towards energy-efficient, scalable PSU platforms that support green data centers and smart grid applications. Strategic collaborations between technology providers and electric utilities are expanding to accelerate intelligent power distribution adoption.

Europe Power Supply Unit (PSU) Market Trends

Europe is slated to capture about 22% of the power supply unit market share in 2025, boosted by Germany, the U.K., France, and Spain. Regional market growth is tightly linked to harmonized regulatory policies, most notably the EU’s Ecodesign and Energy Labelling regulations, which enforce minimum efficiency and environmental standards on all power supply units sold within the bloc.

Renewable energy expansion, high rate of EV deployment, and factory automation initiatives drive demand for reliable and green PSU solutions, while government support for decarbonization stimulates the development of next-generation power electronics.

Market competition is characterized by a strong presence of technology providers collaborating with industrial conglomerates, fostering the development of customized power solutions for automotive, manufacturing, and consumer technologies. Investment trends show emphasis on sustainability and compliance technologies to meet upcoming EU regulatory milestones.

Asia Pacific Power Supply Unit (PSU) Market Trends

Asia Pacific is the largest regional market for power supply units with an approximate 44% share of the market in 2025, supported by rapid industrial growth, digital transformation, and vast renewable energy integration.

Leading contributors are China, Japan, India, and the ASEAN nations, where government policies aggressively promote energy-efficient electronics manufacturing and smart grid infrastructure development. China’s push towards renewable energy targets and smart city projects, India’s growing electrification and industrial automation focus, and Japan’s advanced electronics sector create fertile ground for PSU market expansion.

The regional market stands to benefit significantly from a mature manufacturing ecosystem, widespread supply chain capabilities, and cost advantages that attract global investment into PSU design and production. Regional regulatory frameworks are evolving, with increased alignment to international energy efficiency protocols, fostering innovation and competitive product offerings.

Competitive Landscape

The global power supply unit (PSU) market exhibits a moderately consolidated structure, with the top 5 players controlling the majority of the market.

Major leaders include Delta Electronics, Corsair Components, and Seasonic, which leverage their broad product portfolios, robust innovation pipelines, and extensive distribution networks. Market concentration has increased over time as larger firms have acquired smaller players or specialized niche companies to augment their technology capabilities and market reach.

This semi-consolidated scenario leaves room for niche players who focus on specialized segments such as industrial-grade PSUs or gaming power supplies. Barriers to entry remain significant due to high capital investment requirements in manufacturing, international energy certification compliance, and R&D capabilities. Strategic positioning among incumbent players emphasizes energy efficiency, modularity, smart features, and customer-specific power solutions.

Key Industry Developments

- In November 2025, Schaeffler secured a deal to supply a dual inverter featuring onsemi’s silicon carbide (SiC) technology for plug-in hybrid pickup trucks in North America, with nearly one million units planned by the end of 2027. The inverter manages both auxiliary electric drives using conventional IGBTs and the primary traction motor with over 200 kW output via SiC MOSFETs, enhancing efficiency and extending all-electric range.

- In November 2025, Clixroute partnered with China’s TPV Audio and Visual Technology to manufacture AOC projectors starting January 2026 and outdoor power supplies from February at its Noida facility in India. The company plans to invest US$10 Million in the production plant and aims to hire around 200 employees by March, increasing its workforce to over 500. TPV Technology is known for manufacturing display panels and monitors and is the parent firm of AOC International.

- In September 2025, Infineon Technologies introduced a 12 kW high-density power supply unit (PSU) reference design tailored for AI data centers and servers, delivering peak efficiencies above 99% in AC/DC conversion and 98.5% in DC/DC stages using advanced silicon, silicon carbide, and gallium nitride (GaN) technologies. The design features a bidirectional energy buffer that enhances grid stability and reduces capacitance requirements while achieving a power density of up to 113 W/in³.

Companies Covered in Power Supply Unit (PSU) Market

- Delta Electronics

- Corsair Components

- Seasonic

- FSP Group

- Mean Well Enterprises

- TDK-Lambda

- Murata Manufacturing

- Flex Ltd.

- Emerson Electric

- Bel Power Solutions

- Artesyn Embedded Technologies

- Lite-On Technology

- Bel Fuse

- Schneider Electric

Frequently Asked Questions

The global power supply unit (PSU) market is projected to reach US$35.9 Billion in 2025.

Increasing adoption of energy-efficient power supplies across consumer electronics, industrial automation, and telecommunications, combined with the integration of renewable energy sources and electric vehicle (EV) expansion, is driving the market.

The power supply unit (PSU) market is poised to witness a CAGR of 6.3% from 2025 to 2032.

Advancements in power management technologies such as modular and digitally controlled PSUs, growing investments in data centers, the shift toward intelligent power systems, and the proliferation of high-performance computing applications are key market opportunities.

Delta Electronics, Corsair Components, and Seasonic are some of the key players in the power supply unit (PSU) market.