- Semiconductor Materials & Components

- Power MOSFET Market

Power MOSFET Market Size, Share, and Growth Forecast 2026 - 2033

Power MOSFET Market by Mode (Depletion Mode, Enhancement Mode), Voltage Rating (Low (Below 30 V), Medium (30 V - 200 V), High (Above 200 V)), End Use (Consumer Electronics, Automotive Electronics, Industrial, Energy & Power, Other), and Regional Analysis for 2026 - 2033

Power MOSFET Market Size and Trend Analysis

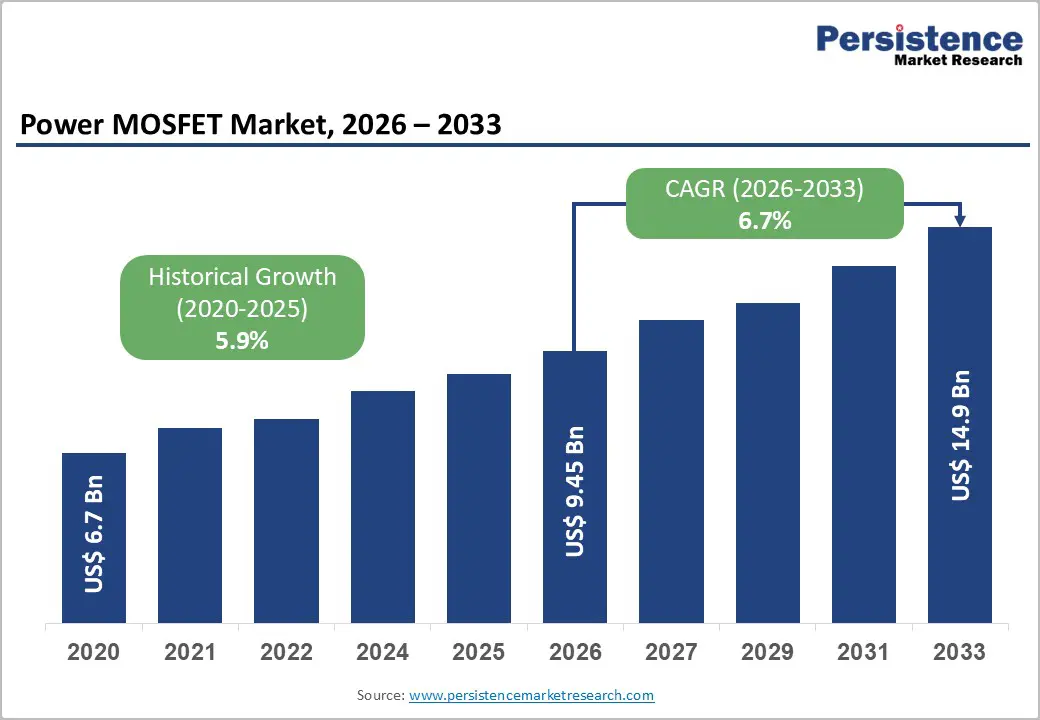

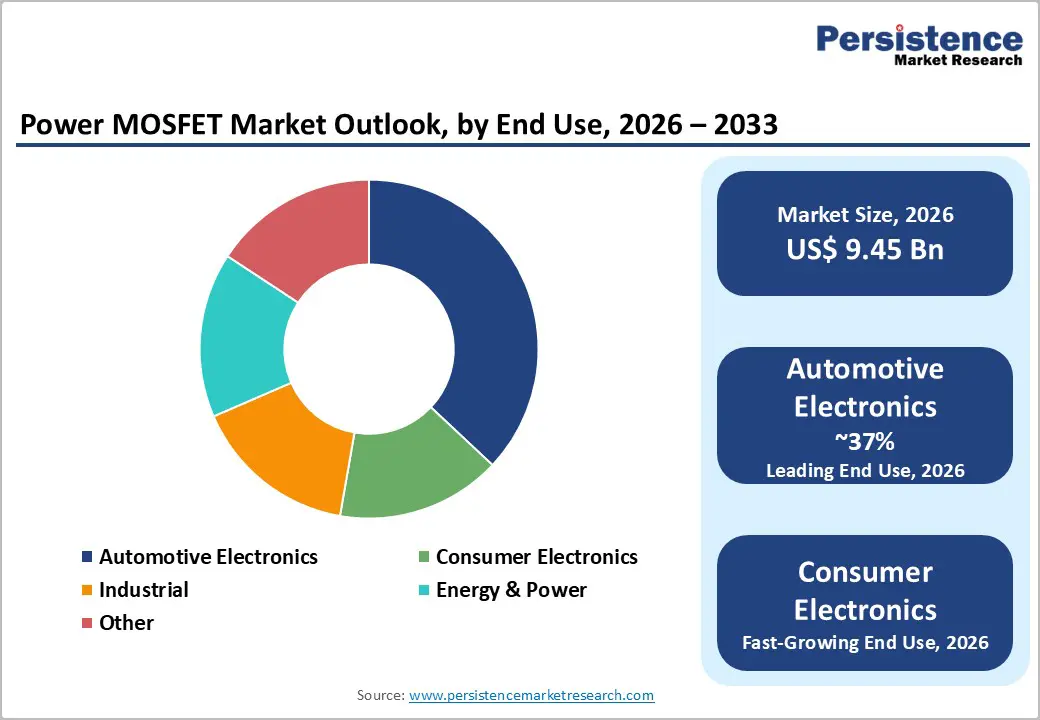

The global power MOSFET market size is supposed to be valued at US$ 9.45 Bn in 2026 and is projected to reach US$ 14.9 Bn by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

The market is experiencing robust growth driven by the escalating demand for energy-efficient power management solutions across automotive, industrial automation, and renewable energy sectors. The rising adoption of electric vehicles, the accelerating deployment of Industry 4.0 technologies, and increasing investments in renewable energy infrastructure are compelling manufacturers to integrate advanced Power MOSFET technologies that deliver superior switching efficiency and thermal performance. This expansion is supported by global EV sales exceeding 17 million units in 2024, driving the adoption of high-efficiency components, as well as by increasing solar and wind installations that necessitate reliable inverters.

Key Industry Highlights:

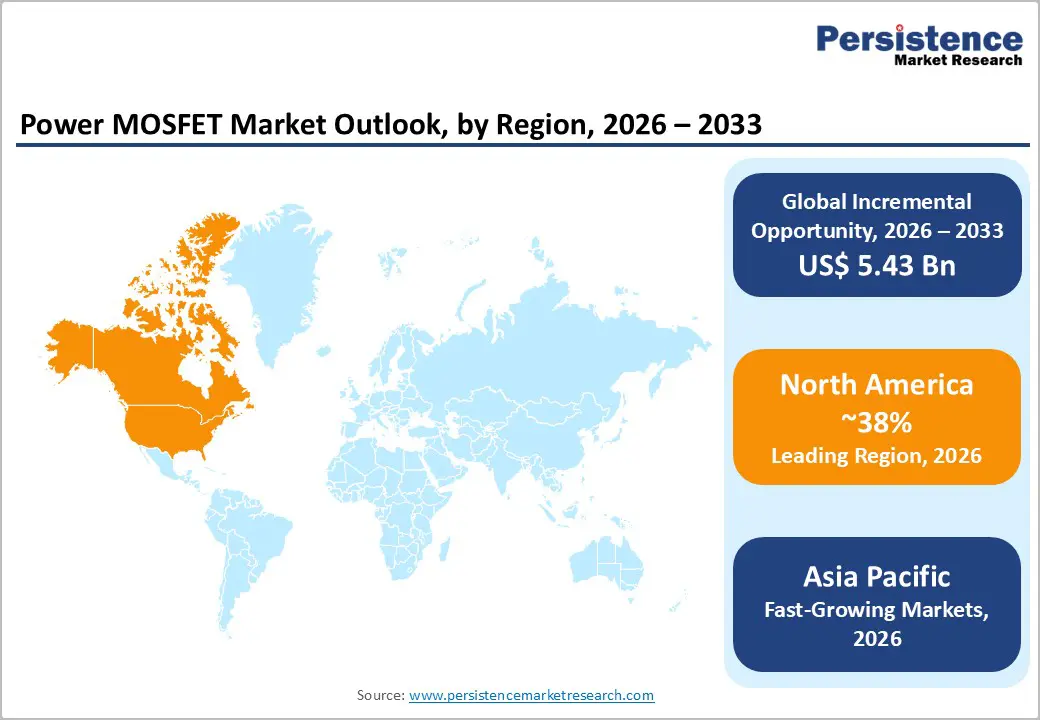

- Regional Leader: North America maintains a strong market position, with 38% market share, driven by CHIPS Act funding, advanced automotive electrification, renewable energy infrastructure investment, and substantial industrial automation adoption, creating sustained demand for sophisticated Power MOSFET solutions.

- Fastest Growing Region: The Asia Pacific region, particularly China, India, and South Korea, demonstrates the highest growth momentum driven by EV production scale-up, electronics manufacturing concentration, government semiconductor initiatives, and renewable energy deployment, expanding the addressable market.

- Leading Segment: Enhancement-Mode MOSFETs command approximately 78% market share due to their inherent fail-safe characteristics, superior switching efficiency, and suitability across the broadest range of power-electronics applications, from automotive to industrial systems.

- Fastest Growing Segment: Medium Voltage MOSFETs (30V-200V) segment experiences fastest growth trajectory driven by IoT device proliferation, 5G infrastructure expansion, smart grid deployment, and fast-charging technology adoption, creating incremental demand for specialized solutions.

- Key Market Opportunity: Silicon Carbide (SiC) technology adoption in the renewable energy and automotive sectors creates a substantial value-creation opportunity as manufacturers transition from traditional silicon devices to advanced SiC MOSFETs that deliver superior efficiency, enable more compact system designs, and support decarbonization objectives.

| Key Insights | Details |

|---|---|

| Power MOSFET Market Size (2026E) | US$ 9.45 Bn |

| Market Value Forecast (2033F) | US$ 14.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.7% |

| Historical Market Growth (2020 - 2025) | 5.9% |

Market Dynamics

Drivers - Electric Vehicle Adoption and Battery Management System Requirements

The rapid adoption of electric vehicles (EVs) is significantly transforming the Power MOSFET market. Global EV sales exceeded 17 million units in 2024, representing over 20% of new vehicle sales, and this growth trend continues to accelerate. Battery management systems in EVs require advanced power switching components to ensure efficient energy transfer from battery packs to motor control units with minimal losses.

Power MOSFETs, particularly enhancement mode variants, are essential for managing high-voltage powertrains operating at 400V, 600V, and 800V. The expansion of ultra-fast charging infrastructure, supporting power levels up to 350 kW, further drives demand for high-performance MOSFETs capable of withstanding extreme thermal and electrical stresses. Additionally, the integration of advanced driver-assistance systems (ADAS) requires reliable, automotive-qualified MOSFETs that meet AEC-Q101 standards.

Industrial Automation and Industry 4.0 Implementation

Industrial automation is advancing rapidly, driven by substantial investments in smart manufacturing systems aligned with Industry 4.0 principles. Modern production environments increasingly rely on robotic systems, conveyor automation, and precision motor controls, all of which demand efficient power switching components to enhance operational performance and minimize energy consumption. Power MOSFETs are critical components in variable-frequency drives, servo motors, and industrial power supplies, ensuring reliable operation in automated processes.

The ongoing shift toward electrification, replacing combustion-based systems with electric alternatives, is broadening the market scope across sectors such as food processing and chemical manufacturing. Furthermore, the integration of uninterruptible power supplies (UPS) and renewable energy inverters within industrial facilities underscores the growing importance of Super Junction MOSFET technologies, offering superior voltage tolerance and switching efficiency.

Restraint - Supply Chain Complexity and Semiconductor Manufacturing Constraints

The semiconductor industry continues to face significant supply chain challenges that limit Power MOSFET production and availability. Wafer fabrication requires highly specialized infrastructure, and the concentration of production in select regions creates bottleneck risks. Geopolitical tensions, trade restrictions, and export restrictions on advanced equipment have disrupted established supply chains, leading to unpredictable component availability. Manufacturing advanced Power MOSFETs, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN) variants, demands 200mm wafer processing capabilities that remain capacity-constrained.

Furthermore, fluctuating raw material costs, including specialty gases and ultra-pure silicon, exert pricing pressures and affect market accessibility. These constraints are especially severe for emerging manufacturers attempting to scale production, thereby reducing competitive intensity and potentially hindering overall market growth.

Price Sensitivity in Cost-Constrained Applications

Price competition continues to pose a significant challenge to market growth in cost-sensitive segments, particularly within consumer electronics, where manufacturers operate under stringent margin constraints. Power MOSFET pricing is heavily influenced by raw material costs, production complexity, and yield performance. Lower-voltage MOSFETs (below 30V), widely used in consumer applications, experience intense pricing pressure from established players leveraging economies of scale.

Original equipment manufacturers (OEMs) in this segment prioritize cost efficiency over performance differentiation, limiting the adoption of premium MOSFET variants that deliver superior energy efficiency but command higher prices. Additionally, the influx of low-cost Chinese suppliers introduces alternative sourcing options, further intensifying price competition for conventional Enhancement Mode MOSFETs and constraining profitability and technological investment capacity for smaller market participants.

Market Opportunities

Silicon Carbide (SiC) Technology Adoption in Power Conversion Systems

Silicon Carbide (SiC) technology presents a pivotal opportunity for market participants aiming to differentiate their portfolios and capture high-value segments. SiC MOSFETs offer superior performance, including higher switching frequencies than conventional silicon devices, enabling compact power conversion systems with enhanced thermal efficiency. Solar inverter manufacturers increasingly adopt SiC MOSFETs to achieve efficiency levels above 96%, surpassing traditional designs.

Driven by stringent decarbonization mandates, the renewable energy sector is deploying extensive solar and wind installations that require advanced power conversion solutions. Infineon’s launch of the CoolSiC MOSFET 400-V portfolio in October 2024, targeting AI servers, solar storage systems, and industrial motor controls, underscores this trend. The SiC MOSFET market is expanding into renewable energy, data centers, and fast-charging infrastructure, creating significant growth prospects for innovators.

Renewable Energy Infrastructure Expansion and Grid Modernization

The global shift toward renewable energy is driving exceptional demand for advanced power conversion components essential for solar inverters, wind systems, and grid-scale energy storage. Solar photovoltaic installations are expanding at double-digit annual rates across major markets, and each kilowatt of renewable capacity requires efficient conversion solutions. Power MOSFETs play a critical role in inverter designs, enabling the transformation of variable DC from renewable sources into stable AC for grid integration.

Grid modernization initiatives worldwide are accelerating the adoption of smart infrastructure incorporating advanced power electronics for load balancing, voltage regulation, and bidirectional energy flow. Solid-state controllers and high-efficiency DC-DC converters increasingly depend on MOSFET technology. Furthermore, government incentives and emerging applications such as vehicle-to-grid (V2G) and bidirectional EV charging create new revenue opportunities for specialized MOSFET solutions.

Category-wise Insights

Mode Analysis

Enhancement Mode MOSFETs hold a dominant position in the global Power MOSFET market, accounting for nearly 78% of total share and delivering the highest revenue contribution across all voltage categories. These devices remain off at zero gate-source voltage and require a positive bias for conduction, making them inherently fail-safe for critical applications where unintended activation could pose operational or safety risks. Their superior switching efficiency compared to Depletion Mode variants minimizes losses and thermal generation, enabling compact power conversion systems with reduced cooling requirements.

Leading manufacturers such as Infineon, STMicroelectronics, and Texas Instruments continue to innovate through advanced trench technology designs that lower on-resistance while ensuring robust avalanche protection. This technical superiority and broad applicability reinforce Enhancement Mode MOSFETs as the preferred choice for automotive, industrial, and consumer electronics applications.

Voltage Rating Analysis

Medium Voltage MOSFETs (30V-200V) constitute the fastest-growing voltage segment, accounting for nearly 45% of market share and exhibiting the strongest growth trajectory. This category serves diverse applications, including consumer electronics, telecommunications infrastructure, industrial automation, and emerging IoT platforms. The rapid proliferation of IoT devices, the expansion of 5G networks, and the development of smart grids are fueling sustained demand for MOSFETs optimized for these applications. Offering an ideal balance between performance and manufacturing complexity, Medium Voltage MOSFETs enable competitive pricing while delivering advanced functionality.

Growth is further supported by miniaturization trends that enhance integration density and efficiency in compact designs. Significant adoption is evident in distributed power architectures for telecom and data centers, alongside rising demand from fast-charging technologies for mobile and portable devices, ensuring continued momentum throughout the forecast period.

End-user Analysis

Automotive electronics constitute the leading end-use segment for Power MOSFETs, accounting for approximately 37% of global demand. This dominance is driven by the rapid electrification of vehicle powertrains and the increasing integration of electronic systems. Electric vehicles require significantly more MOSFETs than internal combustion engine vehicles due to complex battery management systems, multi-stage power converters, and advanced motor control circuits. Traditional automotive functions, such as lighting, heating, window control, and infotainment, are shifting from analog to digital architectures reliant on power semiconductors.

The adoption of Advanced Driver Assistance Systems (ADAS) and autonomous driving technologies further amplifies power management requirements for sensors, actuators, and computational platforms. Stringent automotive qualification standards and long-term supply agreements create high entry barriers, while premium pricing reflects rigorous performance and reliability demands, ensuring sustained market leadership.

Regional Insights

North America Power MOSFET Market Trends

North America holds a dominant position in the Power MOSFET market, supported by significant investments in electric vehicle infrastructure, advanced semiconductor manufacturing, and widespread industrial automation. The U.S. semiconductor sector benefits from strong government backing through the CHIPS and Science Act, which allocated US$39 billion to enhance domestic manufacturing and research capabilities. This initiative is driving production capacity expansion among leading firms such as Infineon, Texas Instruments, and NXP Semiconductors, reinforcing regional technological strength.

The presence of major EV manufacturers and charging infrastructure developers further creates a favorable ecosystem for Power MOSFET innovation. Automotive companies are rapidly scaling EV portfolios to meet regulatory mandates and consumer demand, while Industry 4.0-driven modernization and growing renewable energy deployment, particularly solar installations, continue to fuel demand for efficient power conversion solutions.

Europe Power MOSFET Market Trends

Europe is emerging as a key growth market for Power MOSFETs, driven by stringent decarbonization policies, ambitious EV adoption targets, and significant investments in renewable energy infrastructure. The European Union’s Green Deal mandates aggressive carbon reduction, compelling automotive manufacturers to accelerate electrification and energy utilities to expand renewable capacity. This regulatory framework results in substantial capital expenditure on EV platforms and renewable systems that incorporate Power MOSFET components.

Leading automakers such as Volkswagen, BMW, and Mercedes-Benz are investing heavily in EV development, while Germany maintains leadership in semiconductor manufacturing through advanced fabrication facilities and research institutions. The region’s strong commitment to Industry 4.0 fosters demand for industrial power electronics in smart manufacturing and automation. Additionally, Europe’s emphasis on high-efficiency renewable systems strengthens the Super Junction MOSFET market.

Asia Pacific Power MOSFET Market Trends

Asia Pacific is the fastest-growing region in the Power MOSFET market, driven by manufacturing leadership, large-scale EV production, and concentrated electronics component manufacturing. China dominates global consumption and production, supported by its position as the leading EV manufacturer, electronics producer, and renewable energy installer. The government’s “Made in China 2025” initiative allocates US$150 billion to strengthen semiconductor self-sufficiency and reduce import dependence.

Japanese firms such as Mitsubishi Electric, Toshiba, and Renesas maintain strong market share through advanced portfolios and OEM partnerships, while South Korea’s semiconductor giants, including Samsung and SK Hynix, enhance regional competitiveness. India is emerging as a key player, driven by government-backed initiatives and Tata’s upcoming fabrication facility. Favorable policies, cost advantages, and ASEAN’s role as an assembly hub further reinforce Asia Pacific’s strategic importance in the global Power MOSFET value chain.

Competitive Landscape

The Power MOSFET market demonstrates a moderately consolidated structure, with leading players, Infineon Technologies, STMicroelectronics, and Texas Instruments, collectively holding a significant share through extensive product portfolios, advanced manufacturing capabilities, and strong customer relationships. Infineon leads the market with technological expertise in Silicon Carbide (SiC) devices, Super Junction (SJ) designs, and automotive-qualified solutions, supported by innovative launches such as CoolSiC MOSFET variants. STMicroelectronics competes across the full voltage spectrum, serving both consumer and industrial applications, while Texas Instruments leverages its strength in analog and mixed-signal design to integrate MOSFETs within comprehensive power management systems. Emerging firms, including Nexperia, ROHM Semiconductor, and Toshiba, maintain niche positions through specialized offerings. Competitive differentiation hinges on power density, thermal performance, switching efficiency, and cost-effectiveness, with SiC and GaN technologies driving premium segment growth.

Key Market Developments:

- March 2024: Infineon introduces CoolSiC™ 2000 V MOSFETs in TO-247PLUS-4-HCC package, marking the first discrete silicon carbide device with 2000 V breakdown voltage, designed for high-power solar inverters and EV charging stations.

- July 2025: Nexperia expanded its bipolar junction transistor portfolio through the introduction of twelve new MJD-style BJTs in clip-bonded FlatPower packaging, enhancing thermal dissipation and integration capabilities for industrial and automotive applications.

- January 2025: Renesas Electronics Corporation introduced its first series of 100V high-power N-channel MOSFETs (RBA300N10EANS and RBA300N10EHPF), which were later highlighted in late 2025 for their application in renewable energy systems.

Top Companies in the Power MOSFET Market

- Infineon Technologies AG (Neubiberg, Germany) stands as the global market leader in power semiconductor components, commanding a dominant market position through a comprehensive Power MOSFET portfolio encompassing OptiMOS, StrongIRFET, CoolMOS, and CoolSiC technology families. The company's sustained investment in Silicon Carbide (SiC) technology advancement and recent expansion of 200mm wafer capacity position it for sustained leadership.

- STMicroelectronics N.V. (Geneva, Switzerland) leverages a comprehensive product portfolio spanning from low-voltage devices to high-voltage solutions, supported by multiple manufacturing facilities and established customer relationships across automotive, industrial, and consumer electronics sectors. STMicroelectronics' MDmesh and STMESH trench technology platforms deliver competitive on-resistance characteristics and thermal performance. The company's integration of Power MOSFETs within broader power management solutions creates cross-selling opportunities and customer lock-in benefits.

- Texas Instruments Inc. (Dallas, Texas, U.S.) maintains a strong competitive position through its innovative NexFET technology platform that delivers exceptional figure-of-merit performance through low-charge device architecture. Texas Instruments' strength in analog and mixed-signal semiconductor design enables integration of Power MOSFETs within sophisticated power management and control solutions for automotive, industrial, and consumer applications. The company's robust distribution network and technical support infrastructure support sustained customer relationships.

Companies Covered in Power MOSFET Market

- Infineon Technologies AG

- STMicroelectronics N.V.

- Texas Instruments Inc.

- Toshiba Corporation

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- Mitsubishi Electric Corporation

- ROHM Semiconductor

- Alpha & Omega Semiconductor Limited

- Microchip Technology Inc.

- Power Integration Inc.

Frequently Asked Questions

The power MOSFET market is valued at US$ 9.45 Bn in 2026, reaching US$ 14.9 Bn by 2033 at 6.7% CAGR.

The power MOSFET market is driven by accelerating electric vehicle adoption, with EV sales exceeding 17 million units in 2024, expanding Industry 4.0 automation implementation, escalating renewable energy infrastructure deployment, and increasing demand for energy-efficient power management solutions across consumer electronics and industrial applications.

Enhancement Mode leads with 78% share due to fast switching in automotive and consumer applications.

North America maintains a strong market position driven by CHIPS Act funding, advanced automotive electrification, renewable energy infrastructure investment, and substantial industrial automation adoption.

Silicon Carbide (SiC) technology adoption represents the most significant market opportunity, offering superior switching efficiency, enabling more compact power conversion systems, and supporting renewable energy.

Infineon Technologies AG maintains market leadership through advanced SiC technology and comprehensive product portfolios, followed by STMicroelectronics N.V., Texas Instruments Inc., Toshiba Corporation, Renesas Electronics, NXP Semiconductors, and Mitsubishi Electric Corporation.