- Automotive Components & Materials

- Plastic Ignition Holders Market

Plastic Ignition Holders Market Size, Share, and Growth Forecast, 2026 – 2033

Plastic Ignition Holders Market by Material Type (Polyamide (PA), Polyphenylene Sulfide (PPS), Polybutylene Terephthalate (PBT), Polypropylene (PP), Others), End-User (Automotive, Aerospace, Industrial Machinery, Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), and Regional Analysis for 2026-2033

Plastic Ignition Holders Market Share and Trends Analysis

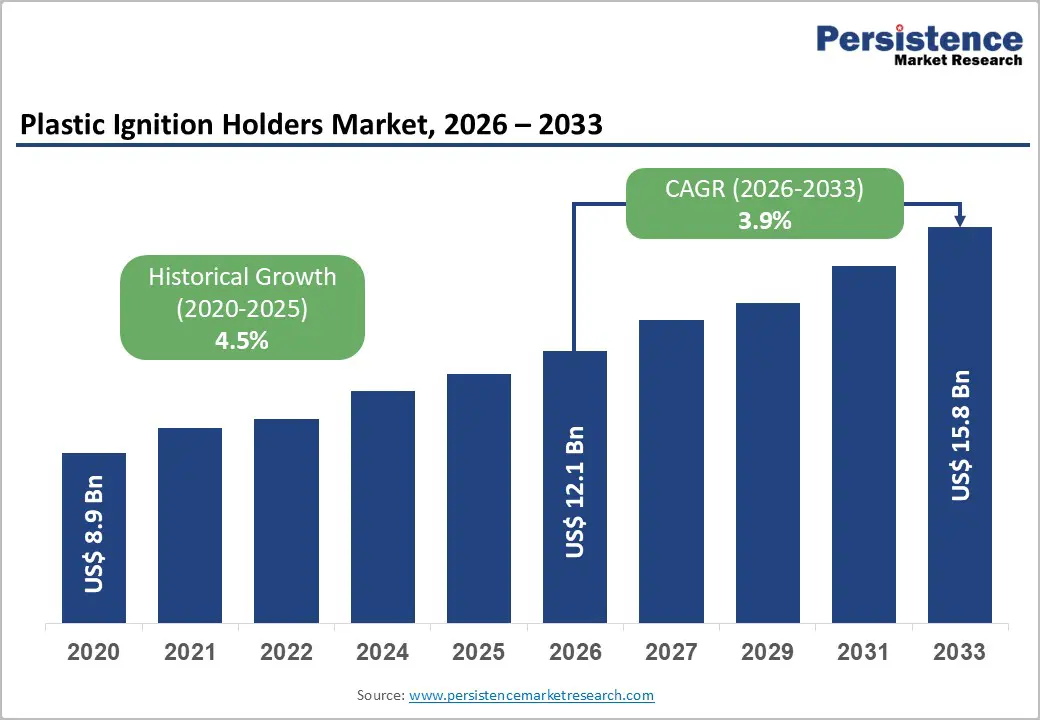

The global plastic ignition holders market size is likely to be valued at US$ 12.1 billion in 2026, and is projected to reach US$ 15.8 billion by 2033, growing at a CAGR of 3.9% during the forecast period 2026−2033.

Expansion of automotive production and increasing adoption of high-performance polymer components are expected to sustain steady market growth during the forecast period. Plastic ignition holders function as structural and electrical insulation components within ignition coil assemblies and spark plug systems. Automotive manufacturers emphasize lightweight materials to improve fuel efficiency and reduce emissions, leading to broader integration of advanced polymer components within engine and electrical subsystems. Polymer materials offer thermal stability, electrical insulation capability, corrosion resistance, and dimensional precision, which supports long-term reliability in ignition systems. Rising vehicle electrification and integration of complex electronic control systems contribute to design changes in ignition architectures.

Key Industry Highlights

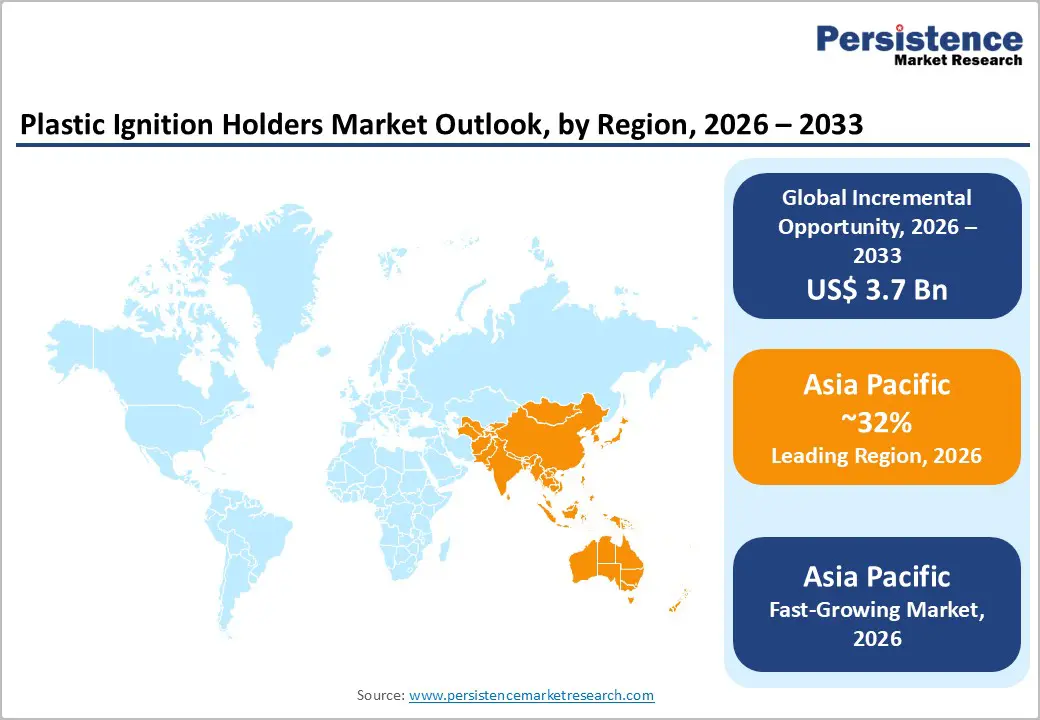

- Dominant Region: Asia Pacific is poised to lead with a projected 32% market share, driven by high automotive production.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, stimulated by expanding vehicle manufacturing.

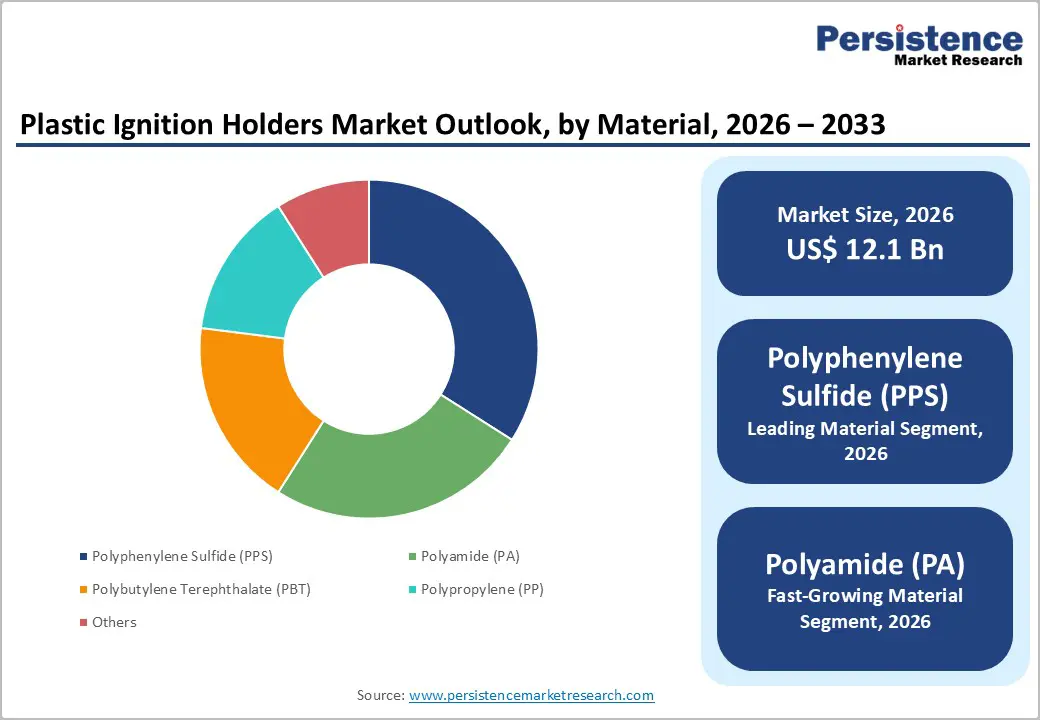

- Leading Material: Polyphenylene sulfide (PPS) is expected to hold about 34% revenue share in 2026, driven by high thermal stability and strong electrical insulation for ignition systems.

- Fastest-growing Material: Polyamide (PA) is slated to be the fastest-growing segment during 2026–2033, stimulated by cost efficiency and durability.

| Key Insights | Details |

|---|---|

|

Key Insights |

Details |

|

Plastic Ignition Holders Market Size (2026E) |

US$ 12.1 Bn |

|

Market Value Forecast (2033F) |

US$ 15.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Lightweight Automotive Components

Automotive engineering strategies emphasize weight optimization across powertrain and ignition system assemblies. Polymer-based components support this objective through lower density, design flexibility, and electrical insulation capability compared with traditional metals. Engineers integrate plastic holders within ignition modules to maintain dimensional stability while lowering component mass. Vehicle architecture programs focus on incremental gram-level reductions across hundreds of small parts, producing measurable improvements in fuel efficiency and emissions compliance. Data from the United States Department of Energy indicates that a 10% reduction in vehicle weight can improve fuel economy by approximately 6–8%, illustrating the operational value of lightweight materials within modern automotive engineering strategies.

Regulatory pressure on fuel efficiency and emission performance reinforces adoption of lightweight components throughout ignition assemblies and surrounding electrical subsystems. Automotive manufacturers evaluate each subsystem for mass reduction opportunities while maintaining thermal resistance and structural integrity near engine compartments. Polymer materials enable compact designs that reduce assembly weight while supporting insulation performance for high-voltage ignition circuits. Design engineers increasingly replace heavier metal holders with reinforced thermoplastics in order to balance cost efficiency, manufacturability, and durability under vibration and heat exposure.

Increasing Demand for Reliable Electrical Insulation Components

Reliable electrical insulation remains fundamental in ignition assemblies that transfer high-voltage energy from the battery and ignition coil toward the spark plug. Electrical energy inside the ignition circuit rises to very high voltage levels in order to ignite the air–fuel mixture within the combustion chamber at the correct timing. Insulation components therefore protect surrounding circuits, structural housings, and electronic modules from electrical leakage, short circuits, and heat-induced degradation. Materials engineered for insulation create a stable barrier that prevents voltage escape while maintaining structural support within the engine environment.

Demand for advanced insulating structures grows in parallel with increasing integration of electronic ignition technologies across modern vehicles. Precise combustion control, emission compliance, and improved engine performance depend on stable electrical pathways that prevent voltage leakage or electromagnetic interference within ignition modules. Growth of electronically controlled powertrain systems increases the number of conductive circuits, connectors, and sensors operating inside compact engine compartments.

Availability of Metal Alternatives with Higher Strength

Higher-strength metal components create a structural challenge for plastic ignition holders in demanding engine environments. Internal combustion engines generate continuous vibration, thermal cycling, and mechanical stress around the ignition assembly. Metal alloys such as steel and aluminum deliver greater load-bearing capacity and dimensional stability under these operating conditions, which supports consistent alignment and durability of ignition system components. Engineering studies indicate that polymers demonstrate lower working temperature tolerance and reduced thermal conductivity compared with metals, limiting performance in areas exposed to sustained engine heat.

Engineering studies from the United States Department of Energy (DOE) highlight the durability advantage of metallic alloys in automotive systems exposed to mechanical stress and heat. Metals demonstrate strong fatigue resistance, structural rigidity, and dimensional stability under repeated thermal cycles. Such performance characteristics support use of aluminum and steel alloys in vehicle components located near the engine block, ignition assembly, and other heat-intensive zones. Established manufacturing processes such as die casting, stamping, and precision machining enable consistent production quality for metal holders used in automotive systems.

Volatility in Polymer Raw Material Prices

Fluctuating polymer feedstock prices create structural cost instability across automotive component supply chains. Most engineering plastics used in ignition-related components originate from petrochemical feedstock such as ethylene, propylene, and other hydrocarbon derivatives. These inputs depend heavily on crude oil and natural gas markets, which respond quickly to geopolitical tensions, refinery shutdowns, transportation disruptions, and energy market speculation. When feedstock prices shift, resin producers revise polymer pricing across the petrochemical chain, leading to frequent changes in thermoplastic costs for automotive component manufacturers. Industry procurement teams experience difficulty maintaining stable production budgets or long-term supplier contracts.

Supply chain sensitivity intensifies this cost instability. Polymer resins travel through a multi-stage production network involving petrochemical cracking units, polymerization plants, compounders, and molding facilities. Each stage introduces exposure to logistics costs, energy tariffs, trade duties, and transportation bottlenecks. Small and mid-scale component manufacturers often operate under fixed automotive contracts with limited capacity to transfer raw-material price increases to downstream buyers. Resin cost spikes therefore compress profitability and discourage investment in production expansion or tooling upgrades. Automotive original equipment manufacturer (OEM) procurement departments also seek predictable component pricing to maintain stable vehicle production planning.

Adoption of Advanced Engineering Polymers

High-temperature electrical environments within ignition assemblies require materials that maintain dimensional stability, electrical insulation, and structural integrity under continuous thermal exposure and mechanical vibration. Advanced engineering polymers such as polyphenylene sulfide (PPS) and polyether ether ketone (PEEK) provide high heat resistance, strong dielectric strength, and chemical stability suitable for demanding automotive electrical systems. These materials tolerate prolonged exposure to engine heat, oil vapors, and chemical contaminants while preserving shape and mechanical performance.

Material innovation within engineering polymers strengthens reliability and production efficiency for ignition components. Reinforced polymer grades incorporating glass fibers or mineral fillers deliver improved stiffness, dimensional stability, and vibration resistance suitable for high-load engine environments. Injection molding technologies enable high-volume manufacturing with consistent tolerances and integrated structural features, reducing assembly complexity and improving production efficiency. Thermal stability and flame resistance of advanced polymers support compliance with automotive safety and electrical performance standards.

Development of Sustainable and Recyclable Plastics

Sustainability policies and circular-economy regulations encourage automotive suppliers to integrate recyclable polymers in component manufacturing. Vehicle design strategies now emphasize material recovery and waste reduction across the entire product lifecycle, creating strong incentives for recyclable engineering plastics in electrical and ignition assemblies. Government regulations increasingly require integration of recycled materials in vehicles, influencing procurement strategies and component material selection. A 2025 policy agreement from the European Parliament introduced targets requiring 15% recycled plastic in new vehicles within six years and 25% within ten years, reinforcing regulatory pressure for recyclable polymer adoption in automotive components.

Resource efficiency and waste-management priorities further support adoption of recyclable plastics in small electrical and ignition system components. End-of-life vehicle processing generates significant volumes of polymer waste that historically entered landfill or incineration streams, creating pressure for material circularity across automotive components. Government environmental programs in regions including the United States and the European Commission promote recycling frameworks and sustainable manufacturing practices for transportation industries.

Category-wise Analysis

Material Type Insights

Polyphenylene sulfide is anticipated to secure around 34% of the plastic ignition holders market revenue share in 2026, reflecting strong demand for high-temperature engineering plastics within automotive ignition systems. Polyphenylene sulfide demonstrates exceptional thermal stability, chemical resistance, and electrical insulation capability, which are essential properties for ignition system components exposed to high engine temperatures. PPS materials maintain structural rigidity under thermal cycling conditions while preventing deformation that could affect ignition coil alignment or spark plug connection stability.

Polyamide (PA) is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by versatility, cost efficiency, and expanding use in automotive electrical components. Polyamide materials provide a balanced combination of mechanical strength, thermal resistance, and electrical insulation, making them suitable for ignition holder manufacturing. Automotive component suppliers use glass-reinforced polyamide formulations to improve structural rigidity and dimensional stability in engine environments. Polyamide materials demonstrate high impact resistance and fatigue durability, which enhances component longevity under mechanical vibration conditions within engine compartments.

End-User Insights

Automotive extracts are poised to dominate with a forecasted market share of over 68% in 2026, powered by extensive use of ignition components in gasoline engine systems. The automotive sector represents the primary application area for plastic ignition holders because internal combustion engines require reliable ignition coil and spark plug assemblies. Plastic holders stabilize electrical connectors and provide insulation to prevent electrical leakage within ignition systems. Passenger vehicles, commercial vehicles, and hybrid engine platforms utilize ignition components that incorporate specialized plastic holders designed for high-temperature environments.

Industrial machinery is estimated to be the fastest-growing segment from 2026 to 2033, fueled by expansion of internal combustion engines used in industrial equipment and power generation systems. Industrial machinery applications utilize combustion engines in equipment such as generators, construction machinery, agricultural machinery, and marine propulsion systems. These engines require reliable ignition assemblies capable of operating under continuous load conditions and variable environmental environments. Plastic ignition holders provide electrical insulation and mechanical stability for ignition coil components used in industrial engines.

Regional Insights

North America Plastic Ignition Holders Market Trends

North America represents a technologically advanced automotive component manufacturing environment supported by strong vehicle production capacity, high adoption of engineering polymers, and well-established supplier networks. Automotive manufacturers emphasize durability, thermal resistance, and electrical insulation for ignition system components operating within high-temperature engine environments. Large vehicle production volumes across the United States generate sustained demand for ignition assemblies and associated plastic holders used in passenger vehicles, light trucks, and commercial vehicles. Extensive adoption of advanced polymer materials such as reinforced polyamide and polybutylene terephthalate supports production of components capable of maintaining dimensional stability and resistance to vibration and chemical exposure.

Automotive technology development and large aftermarket demand support stable growth of ignition-related plastic components across the region. Significant vehicle ownership levels increase replacement demand for ignition assemblies and associated holders used in aging vehicle fleets. Automotive component manufacturers invest in automation, robotics-assisted molding systems, and advanced polymer compounding technologies to improve manufacturing precision and production efficiency. Mexico strengthens regional manufacturing capacity through expanding vehicle assembly plants and growing automotive component supplier clusters integrated with cross-border supply chains.

Europe Plastic Ignition Holders Market Trends

Europe is home to a mature automotive manufacturing ecosystem characterized by advanced vehicle engineering capability, high-precision component production, and strict automotive quality standards. Strong integration between vehicle manufacturers and Tier-1 suppliers supports continuous demand for precision ignition system components produced using engineering thermoplastics. Automotive manufacturers across Germany, France, and Italy emphasize durability, heat resistance, and electrical insulation performance in ignition assemblies used in internal combustion and hybrid vehicles. Advanced polymer processing capability enables large-scale manufacturing of glass-reinforced polyamide and polybutylene terephthalate components designed to withstand vibration, thermal stress, and chemical exposure within engine compartments.

Technological sophistication and regulatory emphasis on manufacturing quality continue shaping demand for high-performance plastic ignition components across major automotive production economies. Automotive component manufacturers invest in automated injection molding systems, robotics-enabled quality inspection, and advanced polymer compounding technologies to maintain production efficiency and product reliability. United Kingdom vehicle manufacturing facilities support demand for durable ignition assemblies in passenger vehicles and light commercial vehicles. Spain strengthens automotive component supply chains through expanding vehicle assembly capacity and growing supplier clusters supporting European automotive production networks.

Asia Pacific Plastic Ignition Holders Market Trends

Asia pacific is expected to lead with an estimated 32% of the plastic ignition holders market share, supported by concentrated automotive manufacturing capacity, mature polymer processing industries, and strong integration between component suppliers and vehicle assembly plants. High-volume vehicle production requires consistent supply of ignition system components that maintain dimensional stability, electrical insulation performance, and resistance to engine heat exposure. Extensive thermoplastic injection-molding infrastructure enables cost-efficient mass production of precision automotive parts such as ignition holders. Automotive manufacturers emphasize lightweight polymer components to improve vehicle efficiency and streamline assembly processes, strengthening demand for engineered plastics including glass-reinforced nylon and polybutylene terephthalate.

Asia Pacific is forecasted to be the fastest-growing market for plastic ignition holders between 2026 and 2033, stimulated by expansion of vehicle manufacturing capacity, increasing hybrid vehicle output, and rising mobility demand across developing economies. Automotive component suppliers continue expanding manufacturing facilities to support higher vehicle production volumes and strengthen localized supply chains for ignition system components. Technological improvements in engineering polymers improve resistance to thermal stress, vibration, and chemical exposure, enabling broader application in modern ignition assemblies. China and India continue expanding automotive manufacturing output through investments in production infrastructure, supplier parks, and advanced component fabrication technologies.

Competitive Landscape

The global plastic ignition holders market demonstrates a moderately fragmented structure shaped by participation from large global automotive component manufacturers and specialized polymer engineering companies. Leading automotive suppliers maintain strong positions within ignition system supply chains through long-term integration with vehicle manufacturing platforms and advanced component design capability. Denso Corporation, Magna International Inc., and Bosch Automotive Solutions operate extensive automotive electronics and ignition system development programs that incorporate precision polymer components designed for durability and electrical insulation.

Competitive positioning also reflects innovation in polymer engineering, cost-efficient manufacturing strategies, and close collaboration with automotive original equipment manufacturers. Lear Corporation and Valeo SA contribute through development of advanced electrical distribution systems and integrated ignition components designed to improve reliability under demanding engine conditions. Market participants emphasize research in reinforced engineering plastics capable of maintaining structural integrity under continuous thermal exposure and vibration.

Key Industry Developments

- In March 2026, LG Chem unveiled thermal-runaway-delaying engineering plastics at InterBattery 2026 that form a dense protective barrier when exposed to flames, slowing the spread of heat, fire, and pressure between battery cells. The lightweight thermoplastic materials improve battery pack design flexibility while enhancing safety for electric vehicles and energy storage systems.

Companies Covered in Plastic Ignition Holders Market

- Denso Corporation

- Magna International Inc.

- Bosch Automotive Solutions

- Lear Corporation

- Valeo SA

- Yazaki Corporation

- Borg Warner Inc.

- Mahle GmbH

- Continental AG

- HELLA GmbH & Co. KGaA

- Hitachi Automotive Systems, Ltd.

Frequently Asked Questions

The global plastic ignition holders market is projected to reach US$ 12.1 billion in 2026.

Surging global automotive production and increasing demand for lightweight, heat-resistant polymer components in ignition system assemblies are driving growth of the market.

The market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Adoption of advanced heat-resistant engineering plastics and expansion of automotive aftermarket replacement demand create key market opportunities.

Some of the key market players include Denso Corporation, Magna International Inc., Bosch Automotive Solutions, and Lear Corporation.