- Plastics, Polymers & Resins

- Plastic Films Market

Plastic Films Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Plastic Films Market By Material Type (Polyethylene Films, Others), Film Type (Stretch Films, Others), Application, End-user, and Regional Analysis for 2025 - 2032

Plastic Films Market Size and Trends Analysis

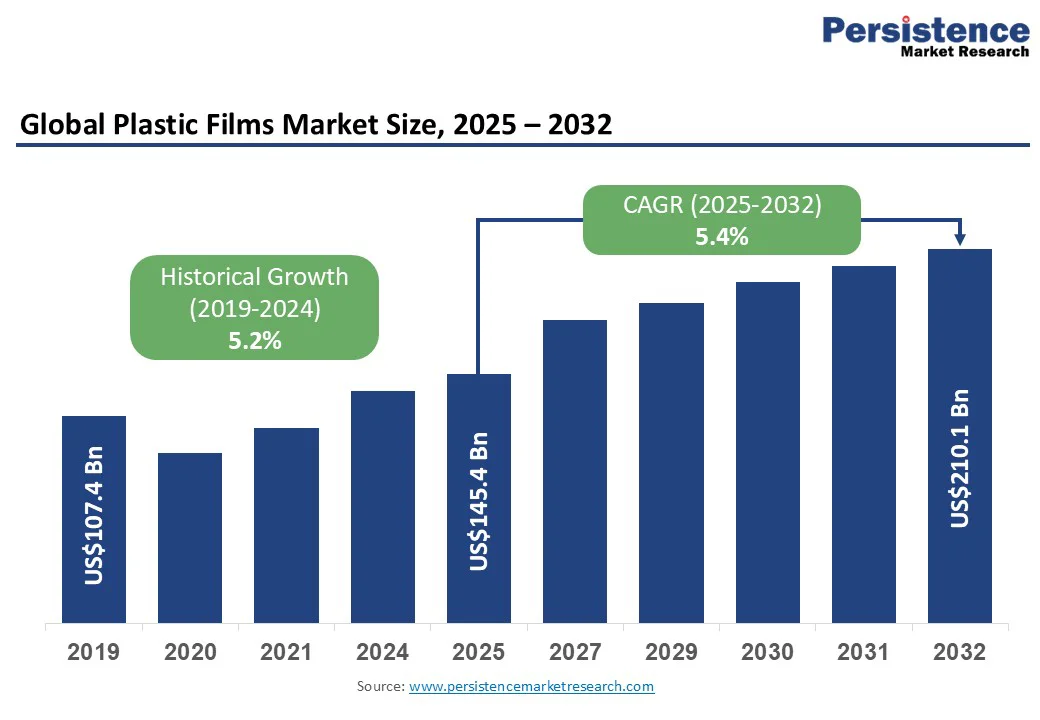

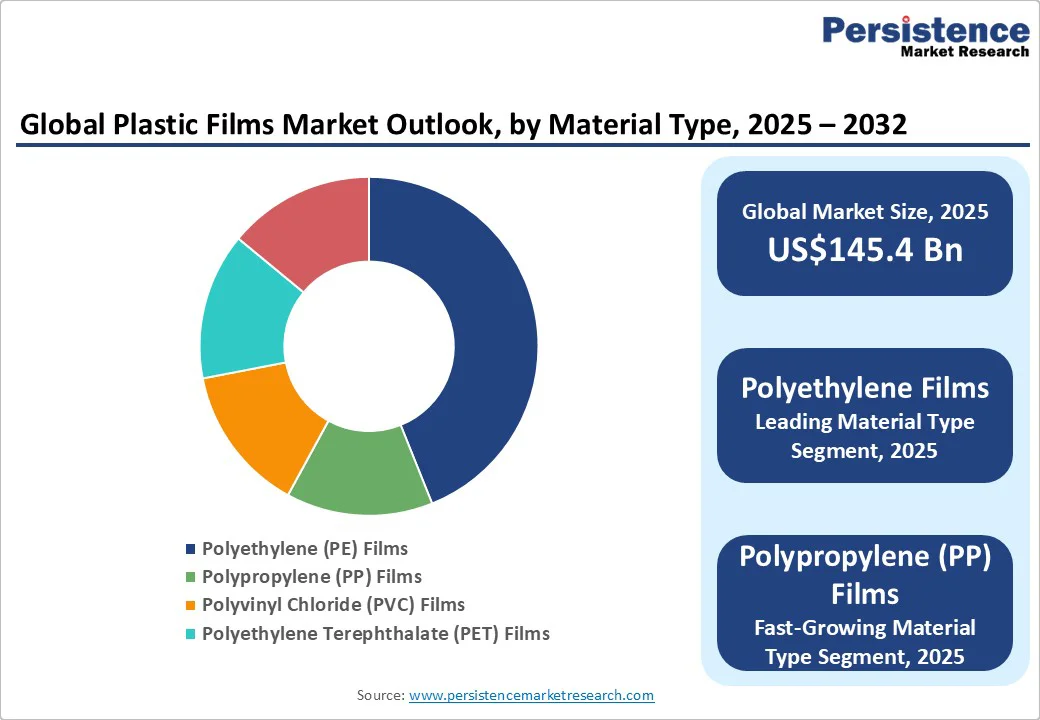

The global plastic films market size is likely to be valued at US$145.4 Bn in 2025 and is expected to reach US$210.1 Bn by 2032, growing at a CAGR of 5.4% during the forecast period from 2025 to 2032, driven by their wide utilization in food and beverage packaging, agriculture, pharmaceuticals, and industrial applications due to their versatility, lightweight properties, and cost efficiency.

Key Industry Highlights:

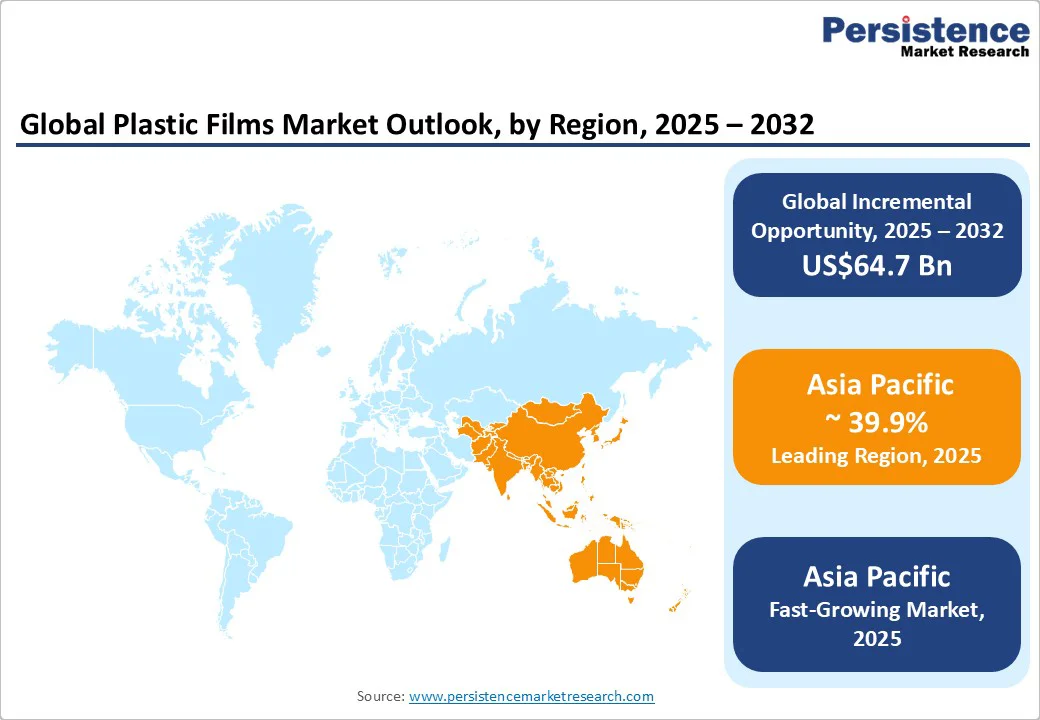

- Leading and fastest-growing Region: Asia Pacific, holding approximately 39.9% share, driven by strong demand in packaging, agriculture, and industrial applications in China and India.

- Investment Plans: Major players are investing in recyclable and bio-based film technologies, chemical recycling plants, and high-performance barrier films. Examples include Dow & Liby’s BOPE film with 10% post-consumer recycled content in China and NOVA Chemicals’ PE film recycling facility in Indiana, U.S.

- Dominant Material Type: Polyethylene (PE) films, accounting for around 47% of the material share, widely used across packaging, agricultural, and stretch/shrink film applications due to flexibility, low cost, and recyclability.

- Leading Film Type: Barrier films, particularly metallized barrier films, capturing approximately 48% share of the film-type market, due to superior protection against moisture, oxygen, and UV for packaged foods and pharmaceuticals.

| Key Insights | Details |

|---|---|

| Market Size (2025E) | US$145.4 Bn |

| Market Value Forecast (2032F) | US$210.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Push Fuels Shift to Recyclable and Biodegradable Films

The plastic films market is experiencing a strong momentum due to the regulatory shift toward recyclable mono-material films and restrictions on non-recyclable laminates. Governments across Europe, North America, and parts of Asia are setting strict targets for packaging waste reduction, which is accelerating the replacement of complex multi-layer laminates with single-polymer alternatives such as polyethylene and polypropylene.

These films are easier to recycle and align with circular economy goals while still offering essential barrier properties. For instance, major food companies are increasingly adopting mono-material high-barrier films for snack packaging to ensure compliance with evolving waste directives without compromising product protection.

Agriculture is also shaping the demand trajectory, particularly with the rising use of biodegradable mulch films in high-value crop cultivation. These films improve soil health, retain moisture, suppress weed growth, and reduce post-harvest labor, while also addressing concerns over plastic waste accumulation in farmland.

Supportive government programs in regions such as China, India, and the European Union are encouraging farmers to switch to biodegradable alternatives, creating new opportunities for suppliers. A recent collaboration in India between Sulzer and Balrampur Chini Mills to establish polylactic acid (PLA) production demonstrates how investments in bio-based feedstocks are directly strengthening the market.

Material Complexity and Recycling Gaps Undermine Sustainability Goals

A key restraint impacting the plastic films market is the complexity of material composition. To achieve barrier protection, durability, and seal strength, many films are engineered as multi-material laminates that combine polyethylene, polypropylene, PET, EVOH, aluminum foil, and adhesives.

While these structures perform well in packaging, they create significant challenges in recycling, as the layers cannot be separated without degrading material quality. Added contamination from printing inks, adhesives, and food residues further reduces the usability of recycled output, often making it unsuitable for food-grade or high-performance applications.

Supply chain inefficiencies also limit the growth potential of plastic films. Thin and lightweight formats, such as shrink wraps or retail bags, are difficult to collect and transport, often becoming entangled in recycling machinery or misclassified in sorting systems.

Current optical sorting technologies struggle to accurately differentiate multilayer, metallized, or dyed films, which leads to high rejection rates and contamination issues. As a result, the supply of clean, sorted post-consumer film feedstock remains inconsistent, preventing large-scale production of recycled plastic films. Without stable upstream collection and reliable sorting infrastructure, manufacturers face significant barriers in scaling sustainable film production.

Emerging Applications in Agricultural and Functional Films

The growing adoption of UV-blocking greenhouse films is creating significant headroom for innovation in the agricultural sector. These films are engineered to control light transmission and spectral selectivity, which directly improves plant yield and reduces stress in controlled environments.

With greenhouse cultivation expanding for high-value crops such as organic vegetables, berries, and floriculture, demand for crop-specific film solutions with improved durability and energy-saving properties is accelerating. This trend enables suppliers to move beyond commodity offerings and position themselves in premium, performance-driven segments of agricultural plastic films.

Functional enhancements in protective films also present strong opportunities across electronics, automotive, and construction markets. The development of films with added features such as UV resistance, scratch protection, anti-microbial coatings, or corrosion inhibition is creating new revenue streams where surface protection is critical.

For instance, vapor corrosion inhibitor stretch films are increasingly used to protect metal coils during transport and storage, addressing a niche industrial need. Similarly, Dow’s collaboration with detergent brand Liby in China to commercialize recyclable BOPE films reinforced with post-consumer recycled content highlights how resin innovation can unlock new opportunities in flexible packaging, blending sustainability with advanced performance.

Category-wise Analysis

Material Type Insights

Polyethylene (PE) films are anticipated to lead, accounting for a market share of 47% in 2025. Their dominance comes from versatility, low production costs, and widespread use in packaging, agriculture, and stretch or shrink applications.

Subtypes such as LDPE, LLDPE, and HDPE make PE films adaptable to different needs, whether providing flexibility for food packaging or durability for industrial wrapping. Another key factor behind their market strength is the well-established recycling infrastructure for PE, which makes them more aligned with sustainability goals compared to other polymers.

Polypropylene (PP) films, on the other hand, are expanding at the fastest pace within this category. The segment is growing, fueled by increasing demand in food packaging, healthcare, and consumer goods. PP films are valued for their clarity, excellent heat resistance, and sealing properties, which make them ideal for applications such as snack wrappers, medical packaging, and sterile coverings.

Their lightweight nature also reduces logistics costs, adding to their appeal for brand owners. As more companies look for advanced barrier properties without significantly increasing costs, PP films are rapidly gaining traction in high-performance packaging.

Film Type Insights

Barrier films are anticipated to account for a dominant position, accounting for nearly 48% share in 2025. These films are favored in industries where protection from oxygen, moisture, UV rays, and other environmental factors is critical, particularly in packaged foods, pharmaceuticals, and high-value consumer products.

The superior shelf-life extension offered by barrier films, combined with cost efficiency in comparison to rigid packaging alternatives, has cemented their position as the largest film type segment.

Transparent barrier films represent the fastest-growing category, reflecting shifting consumer and brand preferences. Unlike opaque or metallized structures, transparent films allow visibility of the product while maintaining strong barrier protection, making them especially attractive for food and beverage brands seeking to combine product appeal with performance.

Advances in co-extrusion and functional coatings are enhancing their oxygen and moisture resistance, further boosting adoption. The demand for recyclable and sustainable flexible packaging solutions is also driving growth in this segment, as transparent barrier films align more closely with mono-material packaging initiatives.

Regional Insights

Asia Pacific Plastic Films Market Trends- Fueled by Urbanization and Sustainable Film Adoption

Asia Pacific dominates the market, accounting for more than 39.9% of total consumption, and continues to expand at a robust pace. Rapid urbanization, a growing middle class, and the surge in e-commerce are fueling demand for flexible and specialty films across packaging, agriculture, and industrial applications.

The packaging sector, in particular, benefits from rising consumption of processed food, beverages, and personal care products, where lightweight and durable films are preferred for cost efficiency and extended shelf life. Sustainability has also emerged as a central theme in the region, with manufacturers investing heavily in recyclable and bio-based films to cater to regulatory frameworks and shifting consumer sentiment.

China stands as the largest market in the region, driven by both its industrial scale and its emphasis on material innovation. Packaging accounts for a substantial share of demand, supported by its dominant position in the consumer goods and electronics sectors.

Notably, Dow partnered with detergent brand Liby to introduce BOPE (biaxially oriented polyethylene) films that include post-consumer recycled content.

India is another rapidly developing market, supported by its agricultural base and strong retail sector. The adoption of mulch and greenhouse films has expanded significantly as farmers seek to improve water conservation, soil quality, and productivity.

At the same time, the growth of organized retail and packaged food consumption is driving robust demand for flexible packaging solutions. The government’s emphasis on biodegradable and compostable alternatives, along with rising investment in recycling infrastructure, is accelerating the adoption of eco-friendly films.

North America Plastic Films Market Trends - Sustainability-Led Innovation in a Mature Packaging Ecosystem

North America represents a mature but steadily evolving market, contributing around one-quarter of global demand. Food and beverage packaging remains the largest application, supported by established supply chains and consumer preference for convenience packaging. At the same time, the healthcare and pharmaceutical industries are expanding their use of barrier and specialty films for medical packaging, sterile wraps, and protective coatings.

The U.S. leads the North America market with a well-developed ecosystem of packaging manufacturers and converters. Demand for recyclable PE films and advanced barrier films is rising sharply, driven by state-level extended producer responsibility laws and corporate sustainability pledges.

For example, bio-based and recyclable lidding films have gained popularity in dairy and ready-to-eat packaging, where brands are under pressure to minimize single-use plastics. This shift is encouraging resin producers and converters to scale innovation in mono-material packaging solutions that can be recycled more easily.

Europe Plastic Films Market Trends - Regulatory Leadership Driving Circular and Compostable Film Solutions

Europe plays a critical role in shaping the future of the plastic films industry due to its stringent regulatory environment and emphasis on circular economy principles. Strong EU-wide regulations, particularly the Packaging and Packaging Waste Regulation (PPWR), are forcing manufacturers to redesign products to ensure full recyclability by 2030.

As a result, innovation in mono-material barrier films and compostable packaging has accelerated, giving European producers a first-mover advantage in sustainable technologies.

Germany remains Europe’s largest producer and consumer of plastic films, though production volumes have recently declined due to high energy costs and stricter compliance requirements. Despite these pressures, German companies continue to lead in research and development, particularly in transparent barrier films and advanced recycling systems.

France has also emerged as a key player, particularly after aligning its national packaging regulations with EU requirements by lifting the ban on certain styrenic materials. This regulatory clarity has encouraged innovation in recyclable and compostable films while maintaining compliance with EU-wide targets.

French retailers have been active in reducing unnecessary plastic packaging, especially in fresh produce and dairy categories, pushing film producers to deliver high-performance solutions that balance functionality with sustainability. Investments in recycling capacity and improved waste sorting systems further strengthen France’s position as an innovation hub for next-generation plastic films.

Competitive Landscape

The global plastic films market is moderately fragmented, with global leaders and regional players competing across material innovation, pricing, and sustainability initiatives. Companies such as Amcor, Berry Global, Sealed Air, Toray Industries, and UFlex dominate through extensive product portfolios in packaging, agriculture, and specialty films, while smaller regional manufacturers strengthen their presence with cost-effective and localized solutions.

The shift toward recyclable, bio-based, and mono-material films has intensified R&D investments and strategic collaborations, as seen in partnerships between resin producers and brand owners to commercialize high-performance recyclable packaging.

Mergers, acquisitions, and capacity expansions remain common strategies, with players leveraging scale and advanced technologies to gain a competitive edge in a market increasingly shaped by sustainability and regulatory compliance.

Key Industry Developments

- In July 2025, Dow and Liby launched one of the first fully recyclable flexible packs in China. Dow’s new INNATE™ TF 220 resin for BOPE films was used in Liby’s “Floral Era” detergent pack, which includes ~10% post-consumer recycled content, showcasing the integration of recycled materials and advanced resins to support circular packaging.

- In May 2025, Jindal Poly Films Ltd. (JPFL) launched India’s first biaxially oriented polyamide (BOPA) nylon films for high-barrier packaging. These films offer superior resistance to gas, oils, and moisture, catering to the stringent requirements of the food and pharmaceutical sectors.

Companies Covered in Plastic Films Market

- Amcor plc

- Berry Global, Inc.

- Toray Industries, Inc.

- Uflex Ltd.

- Jindal Poly Films Ltd.

- SABIC

- Dow Inc.

- Sealed Air Corporation

- Cosmo Films Ltd.

- Taghleef Industries

- Oben Holding Group

- DuPont Teijin Films

- Toyobo Co., Ltd.

- Inteplast Group

- Reynolds Consumer Products

- Polyplex Corporation Ltd.

- Winpak Ltd.

- Klöckner Pentaplast

- Mitsubishi Polyester Film

- Flex Films (USA) Inc.

Frequently Asked Questions

The plastic films market is estimated to be valued at US$145.4 Bn in 2025.

By 2032, the plastic films market is projected to reach US$210.1 Bn, reflecting steady growth across all key regions and applications.

Key trends include the adoption of recyclable and bio-based films, growth in transparent and high-barrier films, increased demand from food and beverage packaging, and innovation driven by regulatory pressure in Europe and sustainability initiatives globally.

By material type, Polyethylene (PE) films are expected to hold 47% market share in 2025, due to their versatility, low cost, and recyclability.

The plastic films market is expected to grow at a CAGR of 5.4% from 2025 to 2032, driven by rising demand for high-performance films, recyclable solutions, and the expansion of packaged food, retail, and agricultural applications globally.

The leading players include Amcor, Berry Global, Sealed Air, Toray Industries, and UFlex.