- Animal Feed & Additives

- Plant-based Pet food Market

Plant-based Pet food Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Plant-based Pet food Market by Product Type (Kibble/Dry Food, Wet Food / Canned, Treats & Supplements, Fresh/Refrigerated), Pet Type (Cat, Dog, Others), End-user (Hypermarkets/Supermarkets, Convenience Stores, Pet Stores, Drugstores, Online Retail, Others), and Regional Analysis, 2026 - 2033

Plant-based Pet Food Market Share and Trends Analysis

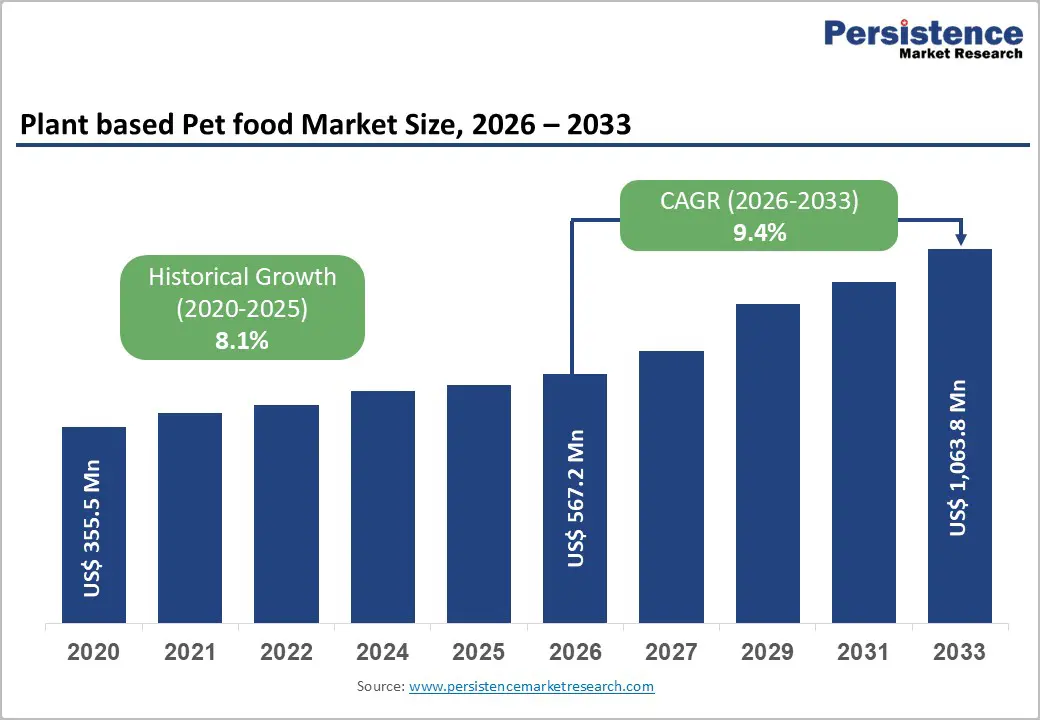

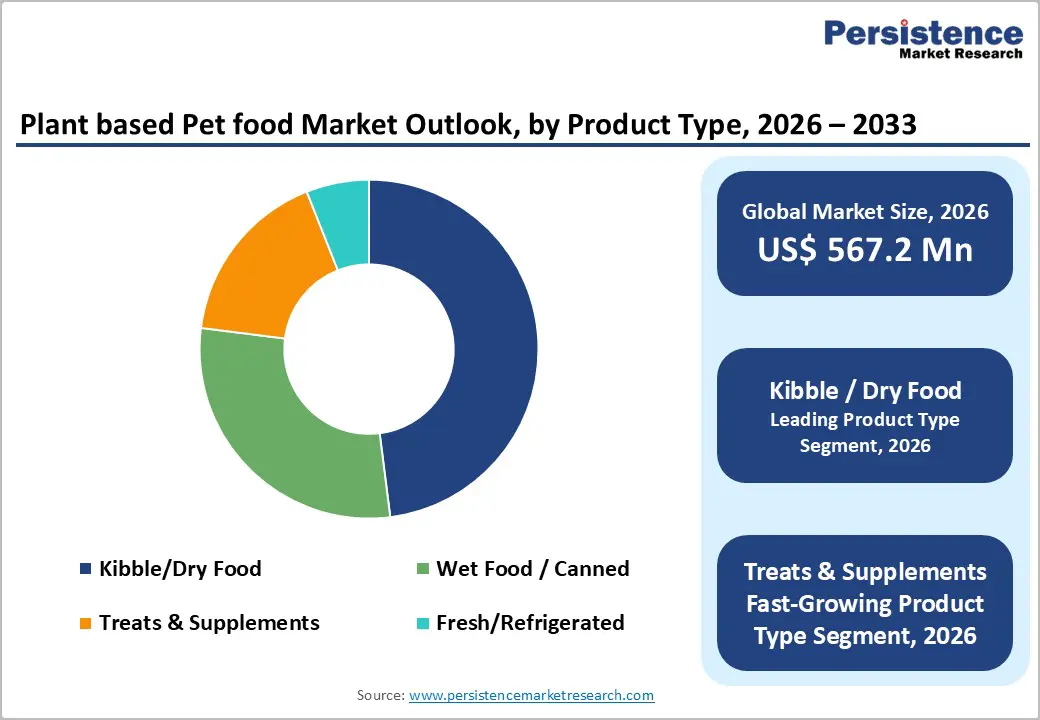

The global plant-based pet food market size is expected to be valued at US$ 567.2 million in 2026 and projected to reach US$ 1,063.8 million by 2033, growing at a CAGR of 9.4% between 2026 and 2033.

Plant-based nutrition for pets is no longer a niche trend as it’s redefining how owners think about health, sustainability, and ethical feeding practices. As awareness of animal welfare, ingredient transparency, and functional nutrition grows, plant-based diets are rapidly gaining traction across global markets, appealing to both dogs and cats.

Key Industry Highlights:

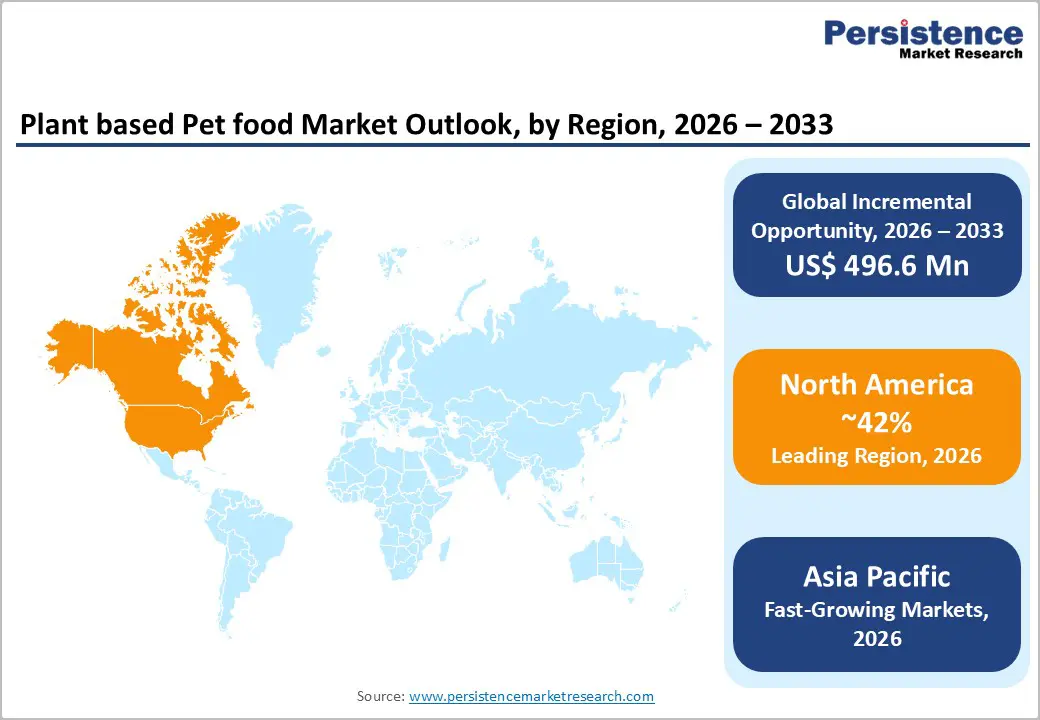

- Leading Region: North America, holding 42% market share, driven by high pet ownership, ethical and sustainability-conscious feeding, and strong adoption of clean-label and functional plant-based diets.

- Fastest-Growing Region: Asia Pacific, fueled by rising disposable incomes, urbanized lifestyles, e-commerce penetration, and digitally savvy pet owners seeking premium plant-based nutrition.

- Fastest-Growing Product Type Segment: Kibble / Dry Food, driven by convenience, long shelf life, fortification opportunities, and suitability for everyday feeding across multi-pet households.

- Market Drivers: Increasing concerns around animal protein sourcing, food safety, traceability, and environmental impact are expanding the appeal to health-conscious and ethically minded pet owners worldwide.

- Opportunities: Partnerships with veterinary nutritionists for clinical-grade diets, expansion of plant-based premium snacks and treats, and development of palatability-enhanced formulations for dogs and cats.

- Key Developments: In November 2025, PawCo Foods launched a dog-specific salad emphasizing plant-based innovation. In March 2025, Colgate-Palmolive acquired the Prime100 fresh pet food brand, strengthening its premium plant-based portfolio.

| Key Insights | Details |

|---|---|

| Plant-based Pet Food Market Size (2026E) | US$ 567.2 Mn |

| Market Value Forecast (2033F) | US$ 1,063.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.1% |

Market Dynamics

Driver - Growing concerns about animal protein sourcing, traceability, and food safety are prompting interest in plant-derived diets

More pet owners are scrutinizing where ingredients come from and how they were produced, elevating ethical and safety concerns to the forefront of purchasing decisions. Stories about contaminated supply chains and unsustainable farming practices have made animal protein sourcing a sensitive topic. By contrast, plant-derived diets offer clearer traceability from field to bowl, reassuring owners who want transparent ingredient journeys and reduced exposure to food safety risks.

Manufacturers are responding with formulations that emphasize traceability, third-party audits, and supply chain transparency. Plant-based recipes reduce reliance on complex animal protein networks while supporting sustainability messaging. As these concerns spread through social and conventional media, interest in plant-based pet food accelerates. The shift reflects a desire for better-understood ingredients and enhanced confidence in everyday pet nutrition choices, making plant-based diets more mainstream and trusted among conscientious pet owners worldwide.

Restraints - Taste acceptance challenges among pets accustomed to meat flavors, requiring advanced palatability research

For many pets, the flavor and texture of traditional meat-based foods are deeply ingrained preferences, creating a barrier to the wide adoption of plant-based formulas. Dogs may reject unfamiliar profiles altogether, and cats, natural carnivores, are especially sensitive to protein sources they perceive as non-meat. These sensory gaps constrain growth, as owners struggle to find plant-based diets that meet both nutritional needs and flavor expectations.

Pet food developers must navigate complex palatability challenges by experimenting with natural flavor enhancers, aroma masking, and texture modulation to create an acceptable eating experience. Without breakthroughs in taste and mouthfeel, plant-based diets may remain a niche for pets with strong meat preferences. Sustained research and testing are essential to making plant-based nutrition broadly appealing, bridging the gap between functional benefits and flavor satisfaction for more animals.

Opportunity - Partnerships with veterinary nutritionists to co-develop clinical-grade plant-based diets for allergy-sensitive and therapeutic segments

Collaborations with veterinary nutritionists open a new frontier for plant-based pet food by elevating formulations to clinical-grade standards. Veterinary experts bring deep expertise in nutrient requirements, digestive physiology, and therapeutic diet design. Partnering with them enables brands to develop plant-based recipes suitable for allergy-sensitive pets, pets with metabolic conditions, and weight-management support, areas traditionally dominated by animal protein diets.

For key players and startups, such partnerships signal credibility and scientific rigor, making functional claims more compelling to both pet owners and veterinary professionals. Co-developed diets can target specific health outcomes while adhering to plant-based and clean-label principles, feeding demand in premium veterinary and specialty nutrition channels. As pet health expenditures rise and preventive care gains emphasis, clinical collaboration offers differentiation, premiumization opportunities, and stronger veterinary endorsement, accelerating adoption among discerning consumers seeking plant-based options with verified nutritional efficacy.

Category-wise Analysis

By Product Type Insights

Kibble / Dry Food holds approx. 48% market share as of 2025, anchored by convenience and everyday practicality. Dry formats are easy to portion, store, and serve, aligning with busy lifestyles and multi-pet households. Their long shelf life and packaging efficiency make them a preferred option for routine feeding, particularly for dog owners who prioritize sensible feeding habits and cost-effectiveness.

In addition, kibble technology allows fortification with balanced nutrients, vitamins, and fiber, making it easier to formulate complete plant-based diets that meet life-stage requirements. The broad adoption of dry food across retail, club stores, and online channels sustains its dominance. While wet foods and treats add variety, the integration of dry kibble into daily feeding routines and its strong presence across price points ensure it remains the cornerstone of plant-based pet nutrition worldwide.

Online retail of Plant based Pet food is anticipated to register strong growth during the forecast period

Online retail in Pet food is projected to grow at a 11.8% CAGR over the forecast period, driven by convenience, direct-to-consumer outreach, and subscription options that simplify repeat purchases. Pet owners are increasingly comfortable sourcing specialized nutrition online, where a broader range of plant-based products is accessible with detailed ingredient, sourcing, and feeding information.

Digital platforms enable personalized recommendations, auto-replenishment, and community reviews that build confidence in plant-based choices. E-commerce also enables smaller brands and startups to reach niche audiences globally, without the traditional retail barriers. Retailers are expanding omnichannel experiences, linking mobile apps, social media, and loyalty programs to strengthen engagement. As interactive shopping grows, online channels become vital for education, comparison, and trial, particularly for plant-based pet food, where trust and transparency drive purchase decisions. This shift enhances market penetration and supports sustained revenue growth across therapeutic, premium, and everyday nutrition segments.

Regional Insights

North America Plant-Based Pet Food Market Trends

North America holds approximately 42% of the global plant-based pet food Market, supported by high pet ownership and strong wellness-oriented feeding trends. In the U.S., demand is driven by ethical consumption and sustainability concerns, encouraging the adoption of plant-based recipes for dogs and cats. Retailers respond with expanded plant-based aisles, education campaigns, and clearer labeling to support owner confidence.

Canada shows rising interest in holistic nutrition, with plant-based formulas marketed for sensitive digestion and allergy concerns. Foodservice partnerships with veterinary clinics create visibility for therapeutic options, while online communities amplify the sharing of feeding experiences. Subscription meal plans and customized nutrition insights further drive adoption. Across both countries, consumer expectations for ingredient transparency, environmental impact, and functional benefits shape product development. This mature market continues to lead global trends, blending convenience with premiumization and fueling broader category growth.

Asia Pacific Plant-Based Pet Food Market Trends

The Asia-Pacific plant-based pet food market is expected to grow at a CAGR of 12.7%, driven by rising pet ownership and higher disposable incomes, which support premium nutrition spending. In India, urban pet parents are exploring plant-based diets for digestive wellness and allergy flexibility. China shows strong growth in premium pet food segments, with plant-based options promoted through digital channels and influencer communities.

Japan emphasizes quality and functional benefits, favoring formulations that support joint health and gentle digestion for aging pets. South Korea’s trend-savvy consumers seek on-trend nutrition options, including plant-based treats and hybrid diets. E-commerce penetration and social media advocacy accelerate trial and education, especially around natural ingredients and sustainability. Across the Asia Pacific, regional flavor adaptation and culturally familiar ingredient blends help plant-based pet foods resonate with local preferences, expanding acceptance beyond early adopters.

Competitive Landscape

The global plant-based pet food market is moderately fragmented, with multinational brands and agile startups shaping competitive dynamics. Leading companies emphasize clean-label ingredients, sustainable sourcing, and advanced packaging technologies such as biodegradable pouches and resealable designs that preserve freshness. Product innovation prioritizes plant proteins, functional botanicals, and balanced nutrient systems tailored to life stages.

Certifications for organic, non-GMO, and hypoallergenic standards enhance credibility across health-oriented buyers. Sustainability initiatives focus on reducing carbon footprint, ethical sourcing, and transparent supply chains. B2B partnerships expand co-development with veterinary nutritionists and pet health professionals. Export strategies target emerging markets by adapting products to local markets and ensuring regulatory compliance with food safety standards. Government regulations around pet food labeling, ingredient safety, and nutrition profiles further shape product positioning and market entry. Combined, these forces drive innovation, quality differentiation, and broader global adoption for plant based pet nutrition.

Key Developments:

- In November 2025, PawCo Foods announced the launch of what it claims is the world’s first salad designed specifically for dogs. Led by former Impossible Foods scientist Dr. Mahsa Vazin, the move reinforces PawCo’s focus on plant-based innovation in pet nutrition.

- In March 2025, Colgate-Palmolive agreed to acquire Care TopCo, an Australia-based company that owns the Prime100 fresh pet food brand. The move strengthens Colgate-Palmolive’s presence in premium, fresh pet nutrition and supports growth in science-led pet care.

- In August 2024, Wild Earth launched its first-ever vegan cat food, branded as ‘Unicorn Pâté’. The product marks the company’s expansion beyond dog nutrition into plant-based feline diets.

Companies Covered in Plant-based Pet food Market

- Nestlé S.A.

- Mars, Incorporated

- General Mills, Inc.

- Colgate-Palmolive Company

- The J.M. Smucker Company

- Freshpet, Inc.

- Evanger’s

- Nature's Recipe

- Central Garden & Pet Company

- Benevo

- PawCo Foods

- Wild Earth

- v-dog

- Others

Frequently Asked Questions

The global plant based pet food market is projected to be valued at US$ 567.2 Mn in 2026.

Growing concerns about animal protein sourcing, traceability, and food safety interest are major drivers for the global plant based pet food market.

The global plant based pet food market is poised to witness a CAGR of 9.4% between 2026 and 2033.

Partnerships with veterinary nutritionists to co-develop clinical-grade plant-based diets for allergy-sensitive and therapeutic segments is a key opportunity.

Major players in the global Plant based Pet food market include Nestlé S.A., Mars, Incorporated, General Mills, Inc., Colgate-Palmolive Company, The J.M. Smucker Company, Freshpet, Inc, Evanger’s, Nature's Recipe, and others.