- Hardware & Software IT Services

- Enterprise Password Management Market

Enterprise Password Management Market Size, Share, and Growth Forecast, 2026 - 2033

Enterprise Password Management market by Component Self-Service Password Management, Privileged User Management, and related Services.), Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode (Cloud/SaaS and On-Premise), End Use Industry (Banking, Financial Services, Insurance, IT and Telecom, Healthcare and Life Sciences, Retail and Distribution, Government and Public Sector, Manufacturing and Industrial, Education, Others), and Regional Analysis for 2026 - 2033

Enterprise Password Management Market Size and Trends Analysis

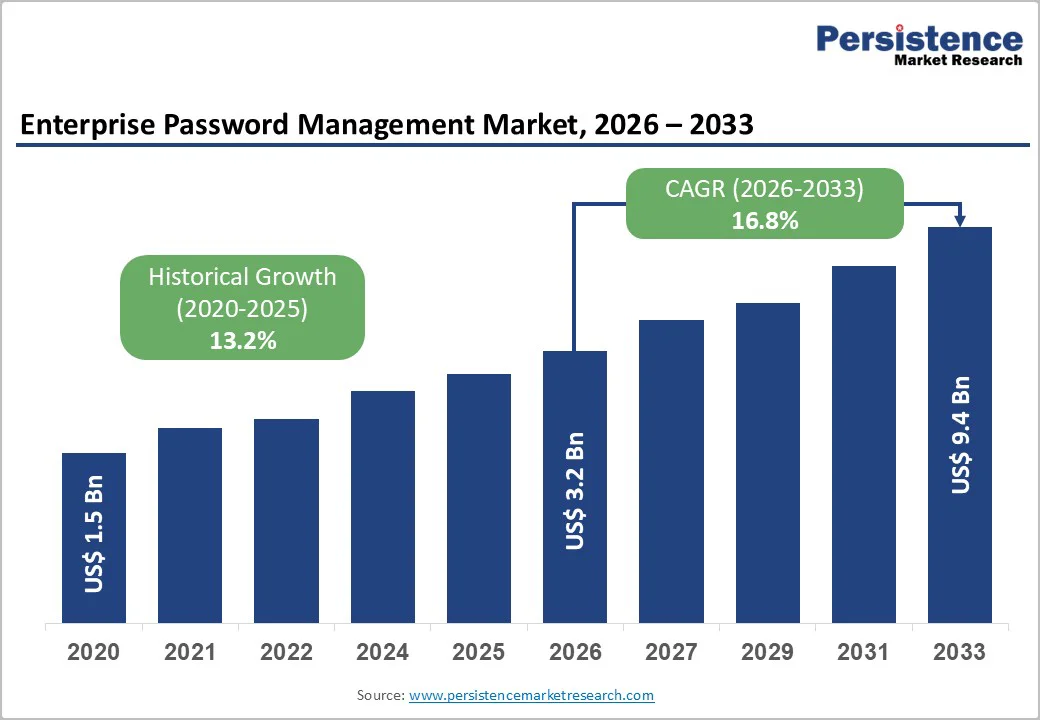

The global enterprise password management market size was valued at US$ 3.2 billion in 2026 and is projected to reach US$9.4 billion by 2033, growing at a CAGR of 16.8% between 2026 and 2033.

The market expansion is driven by three converging forces: escalating cybersecurity threats requiring sophisticated credential protection, stringent regulatory mandates such as GDPR, HIPAA, and PCI DSS enforcing enterprise-wide password governance, and widespread hybrid work adoption necessitating cloud-integrated access solutions.

The market recorded a historical growth of 13.2% CAGR from 2020, with the market size reaching US$1.5 billion in 2020, demonstrating consistent organisational investment in identity security infrastructure. Growth acceleration toward 16.8% CAGR reflects intensifying compliance pressures, data breach costs averaging US$4.45 million globally, and organisational shift toward zero-trust security architectures that position password management as foundational identity infrastructure.

Key Industry Highlights:

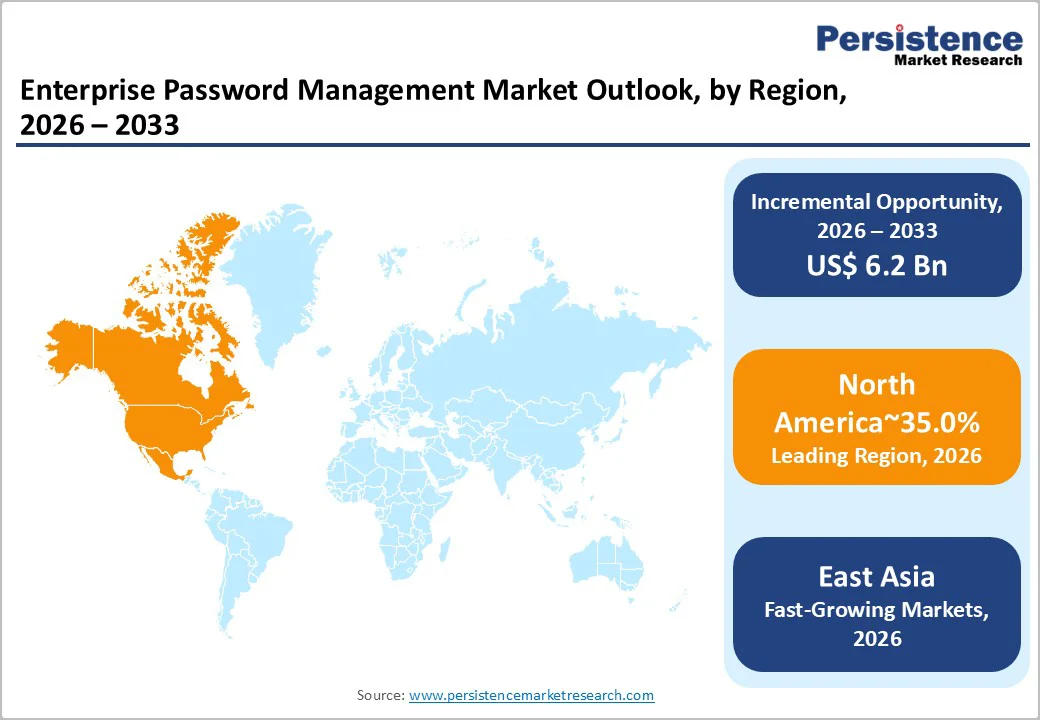

- Regional Leadership: North America leads the global Enterprise Password Management Market with 35% share in 2026, driven by mature identity management infrastructure, extensive cloud adoption, and stringent regulatory compliance requirements.

- Fastest-Growing Region: East Asia captures 15% market share and exhibits high growth due to accelerating digital transformation, mobile-first internet adoption, and emerging compliance-driven demand across financial services and government sectors.

- Leading Segment: Self-Service Password Management dominates with 40% market share in 2026, driven by user-initiated password reset, policy compliance, and help desk burden reduction.

- Rapidly Growing Segment: Services, including managed password administration and professional implementation, represent the fastest-growing segment as organizations outsource password management for efficiency and compliance.

- Primary Market Driver: Escalating cybersecurity threats and regulatory mandates compel the adoption of Enterprise Password Management systems to protect credentials and prevent costly breaches.

- Key Market Opportunity: Passwordless authentication and zero-trust architecture integration create substantial growth potential, enabling continuous authentication, multi-factor enforcement, and mobile/biometric support.

- Notable Developments: CyberArk, 1Password, and Passwork lead innovation with advanced vaulting, automation, API integration, and enterprise-scale deployment enhancements, strengthening market adoption across BFSI, healthcare, and government sectors.

| Global Market Attributes | Key Insights |

|---|---|

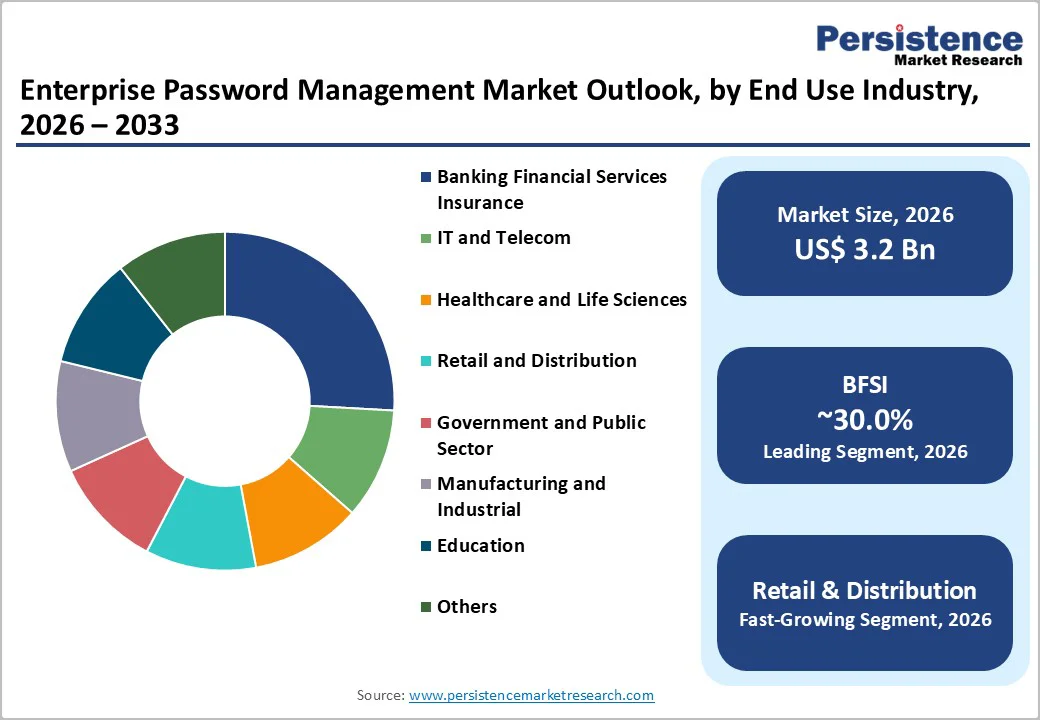

| Enterprise Password Management Market Size (2026E) | US$ 3.2 Bn |

| Market Value Forecast (2033F) | US$ 9.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 16.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.2% |

Market Dynamics

Growth Drivers

Escalating Cybersecurity Threats and Regulatory Compliance Mandates

Organisations face unprecedented pressure to implement enterprise password management systems as cybersecurity threats intensify and regulatory frameworks mandate robust credential governance. The Market demand is fundamentally shaped by the breach landscape: in 2022 alone, approximately 24 billion passwords were exposed in data breaches, a 65% increase in compromised credentials compared to 2020, while 54.8% of breaches resulted from accounts having no passwords or weak password configurations. Beyond exposure volume, the financial consequences of non-compliance drive purchasing decisions: regulatory fines for password-related breaches average US$4.45 million globally, with European enterprises facing potential penalties of up to 20 million or 4% of global annual turnover.

Specific regulatory frameworks intensify compliance requirements, compelling 70% of banks to prioritise Enterprise Password Management solutions with granular access controls, session monitoring, and comprehensive audit trails.

Organisations in regulated industries, BFSI, healthcare, and government, recognise password management not as optional infrastructure but as a mandatory compliance enabler, with 89% of enterprise users integrating password management into identity and access management strategies.

Cloud Migration and Hybrid Work Infrastructure Requirements

Cloud adoption and distributed workforce models fundamentally transform credential management requirements, creating urgent demand for Enterprise Password Management systems capable of operating across distributed infrastructures. Over 94% of enterprises now utilise cloud services, with hybrid cloud adoption accelerating at 19% year-over-year growth, generating complex scenarios where employees simultaneously access multiple SaaS applications, Infrastructure-as-a-Service platforms, and cross-cloud databases.

Legacy on-premises password systems prove obsolete in this environment, unable to scale across distributed networks or integrate with dynamic cloud identity providers. Modern Enterprise Password Management platforms address this requirement through unified credential visibility across AWS, Azure, and Google Cloud Platform environments while enforcing granular access policies and automated password rotation. Integration with centralised identity providers, Microsoft Azure Active Directory with 300+ million commercial users, Okta, and Google Workspace, enables single sign-on capabilities that eliminate reliance on password sharing and reduce password-related security incidents by 41% as documented in multinational logistics operations.

The complexity of cloud password management surfaces in infrastructure audits: when a multinational retailer migrated to Azure Arc, requiring real-time credential rotation across 3,000 hybrid servers, only Enterprise Password Management systems integrated with Privileged Access Management tools completed the task efficiently, reducing human error by 68% compared to manual credential rotation processes. Zero-trust security architecture adoption compounds this demand: password platforms now incorporate behavioural biometrics and risk-based authentication, with organisations reducing breach risks by 63% after implementing context-aware access controls during cloud infrastructure transitions.

Organisational Demand for Passwordless Authentication and Advanced Identity Integration

Enterprise password management evolution toward passwordless and multi-factor authentication architectures drives solution adoption beyond traditional credential vaults. Organisations increasingly specify Enterprise Password Management systems that enable password-less access through Windows Hello, FIDO2 hardware tokens, and mobile biometric authentication while maintaining backward compatibility with legacy systems.

Microsoft's strategic push toward password-less Azure Active Directory authentication demonstrates market momentum. BP migrated 70,000 employees to AAD's passwordless system, eliminating 12,000 monthly password reset tickets while reducing administrative overhead. 63% of social engineering attacks leverage stolen passwords, compelling organisations to prioritise solutions with integrated multi-factor authentication that breaks credential-alone attack vectors.

Industry leaders recognise this shift as Keeper Security achieved four consecutive years as Overall Leader in GigaOm's Enterprise Password Management Radar Report through maturity in passwordless support, Identity Provider integration, fine-grained policy controls, and integrated Privileged Access Management offerings. Securden and CyberArk similarly achieved Leader status through advanced capabilities just-in-time access, dark web monitoring, CI/CD secrets injection, and AI-driven automation that represent the next-generation Enterprise Password Management capabilities, replacing legacy password reset and governance approaches.

Market Restraining Factors

Implementation Complexity and Legacy System Integration Challenges

Enterprise password management adoption faces significant headwinds from implementation complexity and integration costs with established IT infrastructure. Organisations report that 29% of centralised password management implementations initially fail compliance reviews due to inadequate access logging, insufficient multi-factor authentication integration, or incompatibility with existing identity providers.

The challenge intensifies in heterogeneous environments as enterprises managing authentication across Active Directory, Okta, Azure Active Directory, and legacy LDAP systems require Enterprise Password Management platforms capable of synchronising credentials across incompatible systems, a technical hurdle that delays deployment and increases total cost of ownership.

User resistance compounds implementation difficulties: change management for password policy transitions and mandatory authentication workflow modifications generates employee resistance that undermines adoption velocity, particularly when passwordless requirements conflict with legacy application support.

Key Market Opportunities

Passwordless Authentication Integration and Zero-Trust Architecture Alignment

The emerging opportunity for Enterprise Password Management systems lies in positioning password management as a foundational enabler of zero-trust security architectures requiring continuous authentication, context-aware authorisation, and behavioural biometrics integration. Rather than managing passwords as static credentials, next-generation Enterprise Password Management platforms are evolving to orchestrate authentication across multiple factors biometric identifiers, hardware tokens, contextual risk signals, and device posture assessment that collectively replace password reliance.

The technical shift creates substantial market opportunities, such as platforms supporting FIDO2 standards, Windows Hello integration, and mobile biometric authentication address enterprise demand for passwordless access while maintaining policy enforcement and audit capabilities. This architectural evolution positions Enterprise Password Management as a critical orchestration platform rather than a password vault, expanding addressable market opportunity toward organisations migrating to zero-trust models who require unified authentication management across Workforce Identity Access Management and Customer Identity Access Management use cases.

The regulatory environment amplifies this opportunity as the NIST Cybersecurity Framework (CSF) 2.0 and government cybersecurity executive orders increasingly endorse passwordless authentication as best practice, compelling federal contractors and regulated entities to adopt Enterprise Password Management systems supporting passwordless access. This regulatory endorsement creates compliance-driven demand distinct from traditional cost-reduction motivations, supporting premium pricing for Enterprise Password Management solutions with advanced passwordless capabilities.

Secrets Management and DevOps Integration for Cloud-Native Applications

Enterprise password management expansion into secrets management for continuous integration/continuous deployment (CI/CD) pipelines and Infrastructure-as-Code environments represents a significant growth opportunity as organisations accelerate cloud-native application development.

Traditional Enterprise Password Management systems address user credential management; DevOps-focused opportunities involve managing API keys, database credentials, encryption certificates, and SSH keys required for automated infrastructure deployment. This market expansion is driven by organisational shift toward containerization, microservices, and serverless architectures that require dynamic secrets rotation at scale.

The technical opportunity: Passwork 7's launch introduced 100% REST API coverage and CLI tools enabling automated workflows and enterprise system integration while allowing organisations to maintain full data control and reduce total cost of ownership by 30% compared to alternatives. DevOps-focused Enterprise Password Management capabilities address previously underserved market segments in technology companies, fintech platforms, and organisations with sophisticated software development infrastructure, expanding enterprise password management applicability beyond traditional BFSI and healthcare sectors.

Managed Service Provider (MSP) and Managed Security Service Provider (MSSP) Channel Expansion

The managed service provider market represents a significant channel expansion opportunity for Enterprise Password Management vendors seeking to scale customer acquisition while supporting small and medium-sized enterprises lacking in-house security expertise. 1Password's August 2025 launch of 1Password Enterprise Password Manager – MSP Edition on the Pax8 Marketplace, providing 40,000 MSPs access to purpose-built enterprise-grade password management, exemplifies this opportunity.

The MSP channel addresses a market gap where SMEs require enterprise-grade Enterprise Password Management capabilities but cannot justify dedicated security staff or independent vendor relationships. This channel expansion model enables Enterprise Password Management vendors to achieve broader market penetration in underserved SME segments while MSPs differentiate service portfolios through white-labeled or co-branded password management offerings.

Category-wise Analysis

Component Insights

Self-Service Password Management commands 40% market share in 2026, representing the dominant Enterprise Password Management solution module as organisations prioritise user-initiated password reset, policy compliance, and reduced help desk burden. This segment encompasses employee-facing password management portals, account unlock functionality, and password strength guidance that enable users to maintain credential security without IT department intervention. Self-Service Password Management implementations reduce help desk password-related tickets by 40-60%, directly improving operational efficiency while enhancing user experience through rapid credential recovery without support delays. Organisations across all industries, BFSI, healthcare, government, and retail standardize on Self-Service Password Management as a fundamental Enterprise Password Management capability supporting remote work infrastructure and distributed workforce access requirements.

Services segment, encompassing professional implementation services, managed password administration, ongoing managed services, and vendor-provided support, represents the fastest-growing Enterprise Password Management module segment. This acceleration reflects organisational preference for outsourced password management operations to specialised vendors rather than building internal expertise.

Services expansion includes vendor-managed password administration for enterprises lacking dedicated password management personnel, managed monitoring and compliance reporting services, and ongoing optimisation services ensuring password policies align with evolving regulatory requirements. This business model shift benefits Enterprise Password Management vendors through recurring revenue streams and deeper customer relationships while addressing enterprise preference for outsourced security operations.

End Use Industry Insights

Banking, Financial Services, and Insurance industries command 30% market share in the Enterprise Password Management Market in 2026, reflecting regulatory intensity and data security criticality inherent to financial services operations. BFSI organisations operate under particularly stringent requirements: Federal Financial Institutions Examination Council (FFIEC) multifactor authentication mandates force 70% of banks to specify Enterprise Password Management solutions with granular access controls and session monitoring. Payment processing organisations must comply with PCI DSS, which requires minimum password requirements and complex enforcement mechanisms. The regulatory environment directly translates to BFSI market dominance: compliance-driven budgets support Enterprise Password Management spending regardless of economic cycles, with regulatory penalties for non-compliance exceeding customer acquisition costs. BFSI organisations further specify advanced features, dark web monitoring for stolen credential detection, just-in-time privileged access, and continuous authentication that command premium pricing available primarily in BFSI-focused implementations.

Retail and Distribution industries represent the fastest-growing End-Use Industry segment within the Enterprise Password Management Market, driven by accelerating digital commerce transformation, expanding point-of-sale system connectivity, and regulatory compliance with payment card industry standards. Retail operations increasingly extend from physical stores to e-commerce platforms, mobile applications, and customer data management systems, requiring unified credential governance across diverse touchpoints. Distribution supply chain digitisation introduces credential management requirements for supplier network access, logistics system integration, and inventory management platforms.

Deployment Mode

Cloud deployment models command 60% market share in the Enterprise Password Management Market in 2026, reflecting overwhelming organisational preference for SaaS-based password management over on-premises infrastructure. Cloud deployment advantages include scalability across distributed workforces, automatic updates and security patching, reduced capital expenditure for infrastructure, seamless integration with cloud identity providers drive adoption across enterprise segments.

Cloud-deployed Enterprise Password Management enables rapid scaling for growing enterprises and provides built-in disaster recovery and business continuity capabilities without requiring organisations to manage redundant infrastructure. The cloud preference intensifies with hybrid work adoption: organisations managing distributed employees across multiple locations leverage cloud-based Enterprise Password Management for centralised policy enforcement and unified credential visibility independent of office network architecture.

Regional Insights and Trends

North America Market Trend

North America commands 35% of the global Enterprise Password Management Market share, with the region representing the largest mature market for identity and access management infrastructure. The United States enterprise market dominance reflects technological infrastructure sophistication, extensive cloud adoption, and the presence of prominent Enterprise Password Management vendors CyberArk, Okta, 1Password, Keeper Security, LastPass/GoTo, and Bitwarden. North American organisations face particularly stringent regulatory requirements: the Financial Industry Regulatory Authority requires multi-factor authentication for financial advisor access; HIPAA imposes password governance standards on healthcare organisations; state-level privacy regulations mandate password-related access controls and audit capabilities.

The NHTSA Federal Motor Vehicle Safety Standards and Department of Defence cybersecurity requirements establish baseline password management and authentication standards applicable across industries and government contractors.

The regulatory environment directly translates to sustained Enterprise Password Management investment: organisations across healthcare, finance, government, and critical infrastructure prioritise password management compliance ahead of optional technology initiatives. This compliance-first purchasing behaviour maintains stable demand independent of economic conditions, supporting premium pricing for solutions demonstrating comprehensive compliance coverage.

East Asia Market Trend

East Asia represents 15% of the global Enterprise Password Management Market share with substantially higher growth rates compared to North American mature market dynamics. The region encompasses China, Japan, South Korea, and Australia, each with distinct regulatory frameworks and organisational maturity. Japan and Australia demonstrate mature enterprise technology adoption patterns comparable to North America; China and South Korea exhibit accelerating digital transformation, creating emerging market opportunities; Southeast Asia, including Vietnam, Thailand, and Indonesia, represents frontier markets with rapid SME digitalisation.

East Asian regulatory frameworks increasingly mandate cybersecurity governance and password security controls, with Japan's Act on the Protection of Personal Information and China's Personal Information Protection Law establishing regulatory requirements equivalent to GDPR intensity. These regulatory frameworks, combined with government cybersecurity awareness campaigns and fintech and digital payment system expansion, create compliance-driven demand for Enterprise Password Management, particularly acute in financial services and government sectors.

East Asia exhibits the highest mobile internet penetration globally, with more than 4.5 billion mobile subscriptions in APAC, and over 70% of regional internet access occurring through smartphones rather than desktop computers. This mobile-first digital landscape generates unique Enterprise Password Management requirements: solutions must optimise mobile performance, support biometric authentication, including fingerprint and facial recognition, enable offline access, and synchronise securely across devices. Cloud adoption accelerates in the region, with hybrid cloud deployment patterns becoming standard as organizations manage workloads across private data centres and public cloud providers. Over 61% of SMEs across East Asia seek password encryption and multi-factor authentication tools, indicating a substantial addressable market in previously underserved segments.

Europe Market Trend

Europe represents 20% of the global Enterprise Password Management Market share as a mature, highly regulated region with sophisticated enterprise technology adoption and stringent data protection requirements. The European market encompasses developed economies such as the United Kingdom, Germany, France, Scandinavia, and Benelux with mature cybersecurity investments and enterprise information security infrastructure. Europe exhibits measured growth compared to East Asia's acceleration, reflecting market maturity and comprehensive regulatory compliance frameworks already embedded in enterprise purchasing decisions.

The General Data Protection Regulation (GDPR) fundamentally shapes European Enterprise Password Management market dynamics through Article 32 requirements for appropriate technical and organisational measures ensuring password security. GDPR non-compliance penalties up to €20 million or 4% of global annual turnover create powerful compliance incentives influencing purchasing decisions across all industries.

European organisations prioritise Enterprise Password Management solutions demonstrating EU data residency, encryption standards exceeding GDPR minimum requirements, zero-knowledge architecture preventing vendor access to customer credentials, and comprehensive audit trails enabling GDPR compliance documentation. These requirements create a premium pricing opportunity for vendors meeting stringent European compliance standards, with European organisations paying 15-25% price premiums for GDPR-certified solutions compared to standard Enterprise Password Management offerings.

Competitive Landscape

The global Enterprise Password Management (EPM) market exhibits a consolidated yet competitive structure, where a handful of leading players dominate the enterprise segment while numerous smaller vendors serve niche markets and SMEs. Major companies such as CyberArk Software Ltd., Keeper Security, 1Password, Bitwarden, LastPass, and Passwork hold significant market share, leveraging advanced features like privileged access management, MFA/SSO integrations, passwordless authentication, and enterprise-grade vaulting to secure large contracts across highly regulated industries.

Despite this concentration at the top, the market remains somewhat fragmented, as smaller vendors and emerging solutions continue to compete by offering cost-effective, flexible, or specialised password management capabilities. Innovation plays a critical role, with players constantly enhancing API integrations, automation, secrets management, and compliance tools to differentiate themselves.

This mix of strong incumbents and agile challengers keeps the market dynamic, encouraging continuous product evolution and strategic partnerships. As enterprises increasingly prioritise cybersecurity and regulatory compliance, market competition is expected to remain robust, with potential consolidation among smaller players but persistent fragmentation at the mid-tier and niche levels. Overall, the EPM market reflects a partially oligopolistic structure with ongoing competitive pressures driving innovation and adoption.

Key Industry Developments

- September 3, 2025 - CyberArk was named a Leader and Outperformer in the GigaOm Radar Report for Enterprise Password Management, recognized for its advanced Workforce Password Management capabilities, including enterprise-grade vaulting, session monitoring, dark-web risk detection, seamless credential automation, and deep integrations with SSO, MFA, PAM, and secure enterprise browsing, strengthening identity security and reducing password-related vulnerabilities for global enterprises.

- November 18, 2025 - 1Password released major updates to its Enterprise Password Manager (EPM), enhancing usability, governance visibility, and scalable control to simplify enterprise deployment, improve administrative efficiency, and enable security teams to protect all users effectively while maintaining seamless operations across the organisation.

- July 29, 2025 - Passwork launched Passwork 7, introducing 100% REST API coverage, CLI tools, and Python connectors to enable automated workflows, seamless integration with enterprise systems, and enhanced operational efficiency, while allowing organisations to maintain full control over sensitive data and reduce total cost of ownership by 30% compared to competitors.

Companies Covered in Enterprise Password Management Market

- LogMeIn / LastPass

- Keeper Security

- 1Password (AgileBits Inc.)

- Bitwarden

- CyberArk Software Ltd.

- Microsoft Corporation

- IBM Corporation

- SailPoint Technologies Inc.

- Dashlane

- Micro Focus International PLC

Frequently Asked Questions

The global Enterprise Password Management market is projected to be valued at US$ 3.2 Bn in 2026.

The Self-Service Password Management segment is expected to account for approximately 40.0% of the global Enterprise Password Management market by Component/Solution Type in 2026.

The market is expected to witness a CAGR of 16.8% from 2026 to 2033.

The Enterprise Password Management market is driven by escalating cybersecurity threats, stringent regulatory compliance mandates, cloud and hybrid work adoption, and growing demand for passwordless authentication with advanced identity integration.

Key market opportunities in the Enterprise Password Management market lie in passwordless authentication and zero-trust architecture integration, DevOps and secrets management for cloud-native applications, and expansion through MSP and MSSP channels.

The key players in the Enterprise Password Management market include LogMeIn/LastPass, Keeper Security, 1Password, Bitwarden, CyberArk,