- Hardware & Software IT Services

- Enterprise Digital Rights Management (EDRM) Market

Enterprise Digital Rights Management (EDRM) Market Size, Share, and Growth Forecast, 2026 - 2033

Enterprise Digital Rights Management (EDRM) market by Solution Type (Document Protection, Email Protection, File Sharing & Collaboration Protection, Endpoint & Mobile Protection, Policy & Access Management / Analytics, Misc), Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode, Industry, and Regional Analysis for 2026 - 2033

Enterprise Digital Rights Management (EDRM) Market Size and Trends Analysis

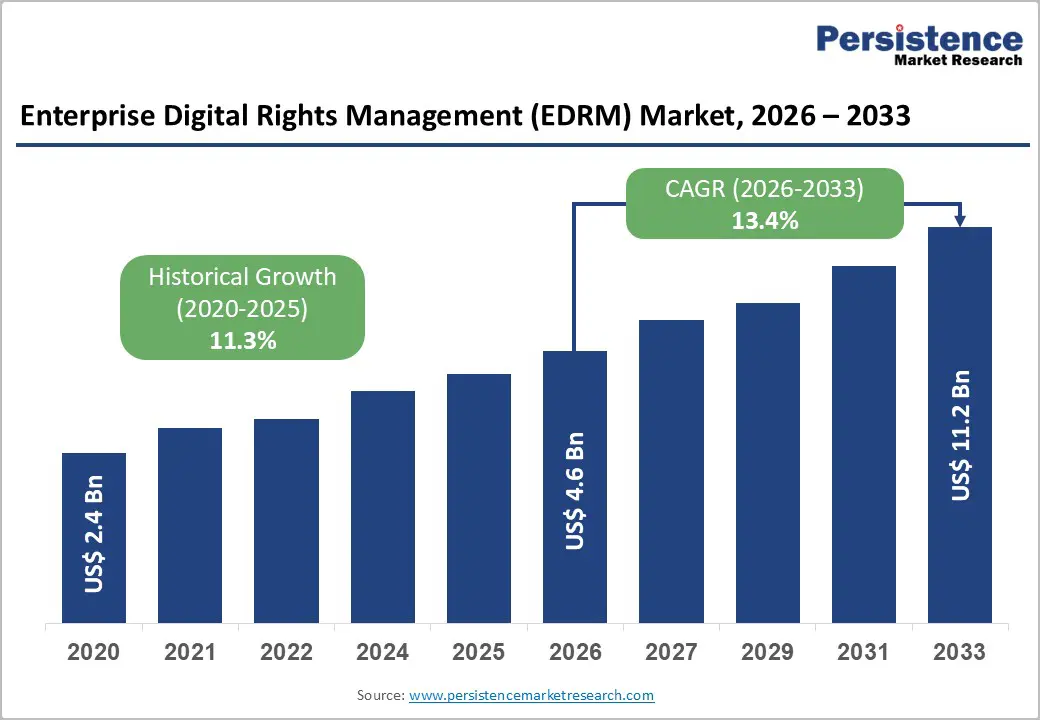

The global enterprise digital rights management (EDRM) market size is likely to be valued at US$ 4.6 billion in 2026 and is projected to reach US$ 11.2 billion by 2033, growing at a CAGR of 13.4% between 2026 and 2033. The EDRM market represents a critical evolution in data protection and intellectual property safeguarding, driven by organisations' growing demand for persistent content control mechanisms that operate across devices and locations.

The market expansion reflects heightened regulatory imperatives spanning GDPR, HIPAA, CCPA, and emerging privacy frameworks, coupled with the surge in supply chain attacks, which doubled to 30% of total breaches in 2024, and the accelerating shift toward remote and hybrid work models. Enterprise adoption of EDRM solutions extends beyond traditional document protection to encompass identity-aware policy enforcement, Zero Trust architectural principles, and AI-driven classification systems that automatically identify and protect sensitive assets, including intellectual property, personally identifiable information (PII), and proprietary business data.

Key Industry Highlights:

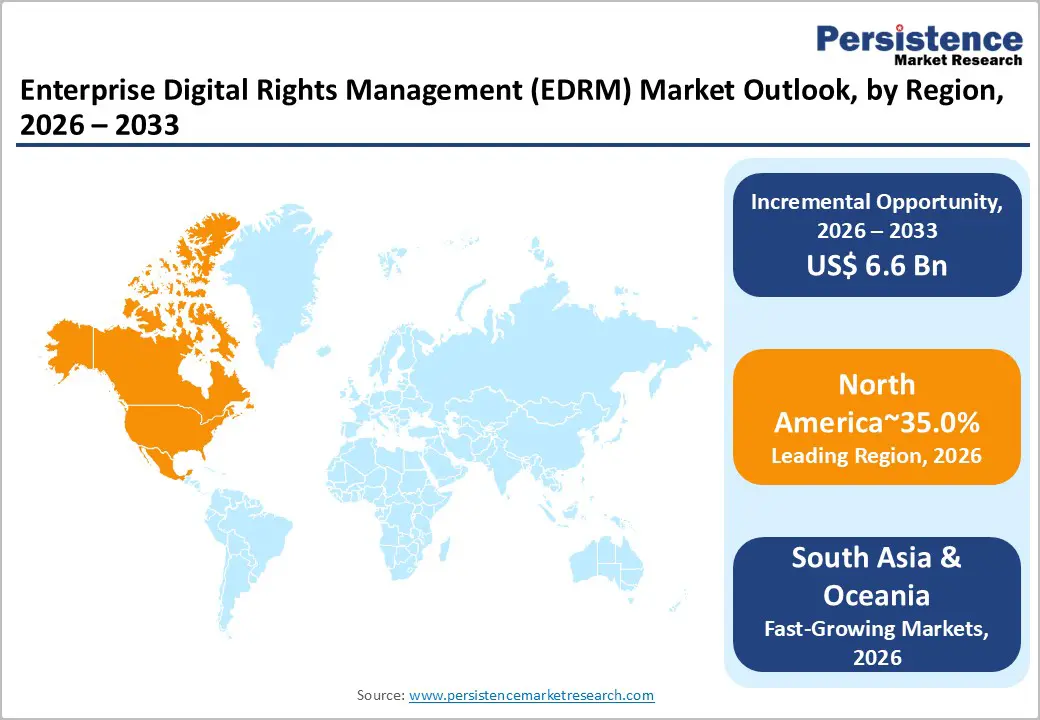

- Regional Leadership: North America dominates the global Enterprise Digital Rights Management (EDRM) Market with a 35% share in 2026, driven by mature IT infrastructure, stringent regulatory frameworks, and high adoption across BFSI, healthcare, and government sectors.

- Fastest-Growing Region: East Asia captures a 20% share in 2026 and is the fastest-growing, supported by digital infrastructure expansion, regulatory mandates, and rising cybersecurity threats in China, India, and emerging economies across the Asia-Pacific.

- Leading End-user: Banking, Financial Services & Insurance (BFSI) leads with a 28% share in 2026, propelled by regulatory compliance pressures, protection of sensitive financial data, and enterprise-wide governance requirements.

- Fastest-Growing End-user: Healthcare & Life Sciences emerges as the fastest-growing segment, driven by intellectual property protection, patient data privacy regulations, and increased digitalisation of research and clinical operations.

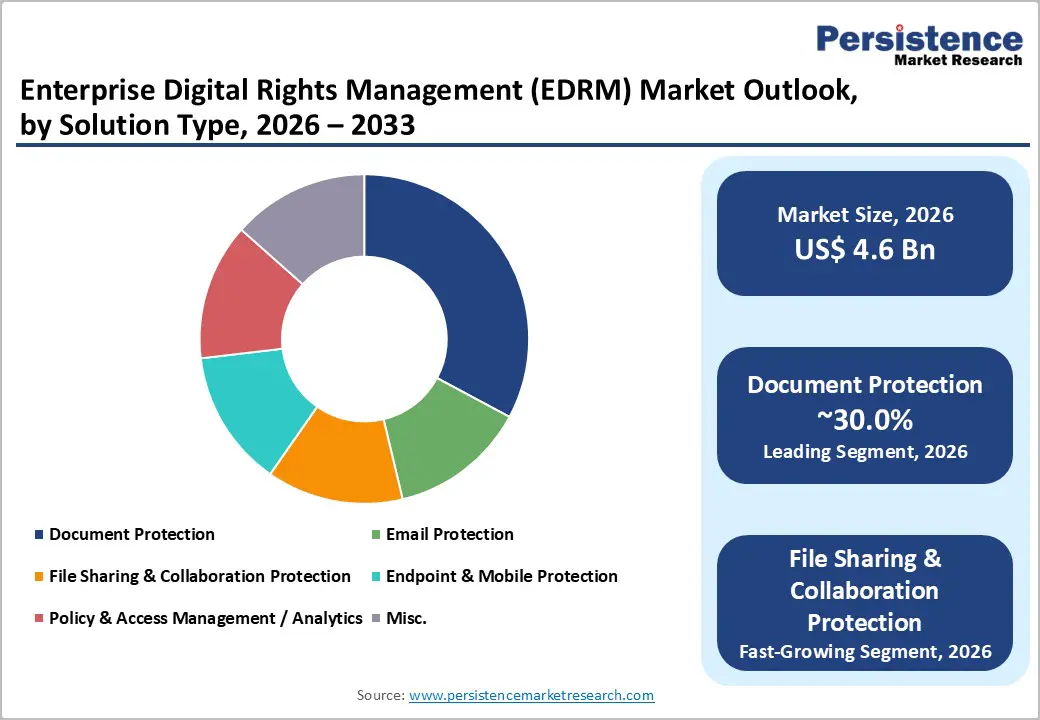

- Leading Solution Type: Document Protection dominates with a 30% share in 2026, reflecting the need to secure PDFs, Microsoft Office files, and other critical corporate records against unauthorised access and manipulation.

- Rapidly Growing Solution Type: File Sharing & Collaboration Protection is the fastest-expanding category, fueled by hybrid work adoption, cross-organisation workflows, and demand for persistent data protection across collaboration platforms.

| Key Insights | Details |

|---|---|

| Enterprise Digital Rights Management (EDRM) Market Size (2026E) | US$ 4.6 Bn |

| Market Value Forecast (2033F) | US$ 11.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.3% |

Market Dynamics

Drivers - Quantified Unplanned Downtime Escalation and Predictive Maintenance Financial Validation

Enterprise Digital Rights Management (EDRM) adoption is fundamentally driven by the proliferation of stringent global data protection regulations that mandate organisational accountability for information security. The European Union's GDPR, effective since 2018, imposes penalties of up to €20 million or 4% of annual global revenue for non-compliance, establishing a regulatory baseline that extends extraterritorially to any organisation processing personal data of EU residents.

The United States' CCPA expanded in 2024 through the California Privacy Rights Act (CPRA), broadening the definition of sensitive personal information to include biometric and genetic data, with fines reaching $7,500 per intentional violation. Asia's regulatory acceleration is equally significant: India's Digital Personal Data Protection Act and China's Cybersecurity Law of 2025 mandate in-country data processing and localised policy orchestration, collectively expanding the addressable EDRM market across jurisdictions.

The HITECH Act amendments require healthcare providers to implement encryption controls for electronic protected health information (ePHI) and mandate breach notifications within 72 hours for incidents affecting 500+ individuals. These regulatory pressures have incentivised organisations to deploy Enterprise Digital Rights Management (EDRM) solutions that enforce persistent, policy-driven controls and generate audit trails demonstrating compliance readiness. Market analysis indicates that regulatory compliance investments account for approximately 18-22% of organisational cybersecurity budgets, directly correlating regulatory tightening with accelerated EDRM deployment across the BFSI, healthcare, and manufacturing sectors.

Exponential Growth in Data Volume and Cyber Threat Sophistication

The global data sphere is projected to reach 175 zettabytes by 2025, and enterprises are facing increasingly sophisticated threat vectors that traditional perimeter-based security architectures can no longer adequately address. Data breaches in 2024 increased sharply year over year, with organisations experiencing an average of 1,876 attacks per quarter. Supply chain compromises exploiting third-party vendor vulnerabilities have become a major breach vector, with significant involvement in ransomware incidents. Nation-state actors continue to intensify their focus on manufacturing intellectual property, with Chinese threat groups accounting for a measurable share of targeting activity against manufacturers between 2024 and early 2025, and the manufacturing sector witnessing a substantial surge in threat actor engagement involving multiple groups conducting espionage and disruption campaigns.

Zero-day vulnerabilities are also proliferating rapidly, with dozens identified in 2024 and more than 30,000 new security vulnerabilities catalogued globally, reflecting a notable year-over-year increase. These evolving threat dynamics have accelerated organisational investment in Enterprise Digital Rights Management (EDRM) solutions, which deliver persistent, identity-aware access controls and real-time usage monitoring to safeguard sensitive data across cloud and on-premises environments.

The convergence of large-scale data proliferation and advanced threat sophistication has positioned EDRM as a critical pillar of Zero Trust Architecture strategies, as cybersecurity leaders increasingly prioritise Zero Trust adoption, and organisations implementing these frameworks report meaningful reductions in security incidents.

Restraint - Integration Complexity and Legacy Infrastructure Incompatibility

Enterprise adoption of Enterprise Digital Rights Management (EDRM) solutions faces significant structural barriers stemming from the prevalence of legacy systems and heterogeneous IT infrastructures within large organisations.

Approximately 35% of organisations cite complex legacy infrastructure as a major barrier to implementing Zero Trust principles, which form the architectural foundation for modern EDRM deployments. Many financial institutions continue operating on outdated banking infrastructure unsuitable for integrating contemporary EDRM systems with advanced Identity and Access Management (IAM) platforms, creating extended and costly deployment cycles that can span 18-36 months.

The absence of standardised data classification frameworks across enterprises necessitates custom policy development, increasing implementation costs, and delaying time-to-value. Additionally, interoperability challenges between EDRM solutions and third-party applications, particularly in Microsoft Office environments where policy enforcement can degrade over software updates, create operational friction, and reduce user adoption rates.

Opportunity - Artificial Intelligence-Powered Automated Classification and Content-Aware Protection

Artificial intelligence and machine learning technologies are revolutionising Enterprise Digital Rights Management (EDRM) market dynamics by enabling automated data classification, sentiment analysis, and behavioral anomaly detection without manual intervention. Advanced algorithms can automatically identify sensitive assets such as PII, financial data, intellectual property, and regulated content, applying appropriate encryption, watermarking, and access restrictions in real-time upon file creation or upload.

Natural language processing (NLP) and image recognition technologies enable EDRM systems to understand document context and content semantics, facilitating intelligent policy application across diverse file types, including PDFs, CAD drawings, source code, and rich media. This AI-driven capability maturation is particularly consequential in Enterprise Digital Rights Management (EDRM) markets serving regulated industries where manual classification creates compliance gaps and operational bottlenecks.

The convergence of AI with EDRM technologies creates compelling value propositions for organisations managing high-volume data flows. Sentiment analysis and automated classification can flag documents exhibiting negative sentiment or risk indicators for prioritised review, while continuous active learning (TAR 3) mechanisms improve classification accuracy to achieve recall rates exceeding 90%, comparable to or surpassing manual review.

Organisations deploying AI-enhanced EDRM solutions report reduced data remediation costs, accelerated compliance certification timelines, and improved incident detection capabilities. This opportunity is particularly pronounced in manufacturing, healthcare, and financial services sectors, where regulatory burdens amplify the value proposition of automating data governance and protection workflows.

Convergence with Zero Trust Architecture and Identity-Centric Security Models

Zero Trust Architecture adoption, mandated by regulatory bodies and executive orders across North America, Europe, and Asia-Pacific, creates systematic demand for identity-aware access controls and continuous verification mechanisms that align with Enterprise Digital Rights Management (EDRM) platforms' core capabilities. Executive Order 14028 requires 95% of U.S. federal agencies to achieve Zero Trust compliance by 2025, while the European Union's NIS2 Directive mandates Zero Trust principles for critical infrastructure operators, and the UK's NCSC Secure Cloud Guidance promotes ZTNA and identity-centric security as baseline standards. These regulatory directives create systematic procurement cycles where organisations integrate EDRM as a foundational component of identity-centric security architecture.

The opportunity is amplified by organisational recognition that Zero Trust principles require persistent, dynamic authorisation based on user identity, device context, location, and behavioral patterns capabilities that Enterprise Digital Rights Management (EDRM) systems uniquely provide.

Organisations deploying EDRM within Zero Trust frameworks report a 65% reduction in incidents attributed to inadequate access controls and improved compliance certification outcomes. The integration of EDRM with advanced Identity and Access Management (IAM) platforms, coupled with the adoption of open standards such as XACML, enables policy portability and reduces vendor lock-in risks. This convergence dynamic positions Enterprise Digital Rights Management (EDRM) vendors as essential partners in organisational Zero Trust implementation initiatives, creating recurring revenue streams and expanded addressable markets across regulated sectors.

Category-wise Analysis

Solution Type Insights

Document Protection commands the largest share of the EDRM market, accounting for 30% in 2026. This dominance is driven by the ubiquity of PDF and Microsoft Office formats as the standard for business contracts, financial reports, and technical specifications. The segment's leadership is reinforced by the critical need to prevent unauthorised editing, printing, and screen capture of high-value corporate records.

As highlighted by Adobe's 2025 focus, modern document protection has evolved to include dynamic watermarking and expiration controls, ensuring that access to a document can be revoked even after it has been downloaded to a user's local device. This segment is foundational to EDRM, serving as the entry point for most organizations initiating a data-centric security strategy.

File Sharing & Collaboration Protection is the fastest-growing segment, fueled by the permanent shift to hybrid work and inter-organisational workflows. As enterprises utilise platforms like SharePoint, OneDrive, and Slack, the perimeter of data security has dissolved, necessitating protection that travels with the file during collaboration. This segment is expanding rapidly because it addresses the "collaboration paradox", the need to share data freely to drive business, while simultaneously restricting access to prevent leakage.

Industry Insights

The Banking, Financial Services & Insurance (BFSI) sector maintains the dominant position in the Enterprise Digital Rights Management (EDRM) Market end-use industry segmentation, commanding approximately 28% market share in 2026, reflecting regulatory intensity, sensitive data volume, and institutional requirement for comprehensive information governance across financial institutions.

BFSI organizations process extraordinarily sensitive information, including customer financial records, transaction data, investment portfolios, credit assessments, and proprietary trading algorithms requiring protection against unauthorized disclosure, unauthorized modification, and competitive intelligence exploitation.

The European Union's Digital Operational Resilience Act (DORA), effective January 17, 2025, establishes mandatory digital resilience testing, including Threat-Led Penetration Testing (TLPT) requirements for critical financial institutions, with explicit supply-chain risk management obligations for external ICT service providers, directly creating regulatory drivers for comprehensive EDRM deployment. India's BFSI sector expansion to US$ 1 trillion market capitalisation (2025) from US$ 20.28 billion (2005), with the sector contributing 27% to national GDP and encompassing rapidly expanding NBFC, insurance, and fintech segments, demonstrates substantial demand for information protection solutions proportional to sector growth.

Healthcare & Life Sciences represents the fastest-growing end-use industry segment for Enterprise Digital Rights Management (EDRM) Market solutions, driven by regulatory acceleration, intellectual property proliferation within pharmaceutical research, and clinical privacy requirements spanning both developed and emerging markets.

The European Union's proposed HIPAA security requirement strengthening, responding to a documented 102% increase in large healthcare data breaches over the preceding five years, directly mandates enhanced encryption, multi-factor authentication (MFA) requirements for sensitive health information access, and mandatory annual penetration testing, creating immediate compliance drivers for EDRM deployment.

Regional Insights and Trends

North America Enterprise Digital Rights Management (EDRM) Market Trends

North America commands the largest global EDRM market share at approximately 35%, reflecting the region's mature enterprise IT infrastructure, high technology adoption rates, and stringent regulatory frameworks spanning financial services, healthcare, and federal government sectors. The United States' established regulatory architecture, including HIPAA, Health Insurance Portability and Accountability Act (HIPAA), Gramm-Leach-Bliley Act (GLBA), and evolving state-level privacy regulations, including California Consumer Privacy Act (CCPA), creates sustained demand for EDRM solutions enabling regulatory compliance demonstrations through comprehensive audit trails and usage documentation.

Federal Information Security Modernization Act (FISMA) requirements mandate information security controls across federal agencies with detailed reporting through Office of Management and Budget (OMB) guidance, creating direct government procurement demand for EDRM solutions supporting classified information protection and controlled unclassified information (CUI) governance.

The maturity of EDRM vendor ecosystems in North America, encompassing established players including Microsoft (leveraging SharePoint and Information Protection capabilities), Adobe, IBM, and specialised vendors including Seclore, NextLabs, and Vitrium, enables enterprise customers to select solutions matching specific architectural preferences, security baselines, and industry-specific compliance requirements.

East Asia Enterprise Digital Rights Management (EDRM) Market Trends

East Asia constitutes approximately 20% of the global EDRM market, representing the fastest-growing regional segment reflecting China's digital infrastructure expansion, India's BFSI sector transformation, and emerging economies' regulatory framework development. China's banking and insurance sectors demonstrated substantial growth through Q2 2025, with total banking assets reaching RMB 467.3 trillion (7.9% year-on-year growth) and insurance assets expanding 9.2% to RMB 39.2 trillion, while maintaining robust asset quality metrics (NPL ratio of 1.49%, capital adequacy ratio of 15.58%), directly correlating with accelerated fintech adoption, digital payment proliferation, and emerging cybersecurity threats necessitating enterprise information protection solutions.

The region exhibits distinctive EDRM implementation patterns reflecting regulatory frameworks emphasizing data localization, state control over critical infrastructure, and mandatory domestic processing for sensitive information categories. East Asia's projected economic growth trajectory, with Asia-Pacific developing nations expanding 4.7% in 2026 and India maintaining 6.5% growth, supports sustained digital infrastructure investment and enterprise IT spending proportional to economic expansion.

Vendor strategies within the region emphasise localised cloud infrastructure, domestic data centre deployments, and partnerships with local technology providers satisfying regulatory requirements regarding data residency and sovereignty. The region's manufacturing sectors, particularly in automotive components, electronics,

Europe Enterprise Digital Rights Management (EDRM) Market Trends

Europe represents approximately 25% of the global EDRM market value, characterised by exceptionally stringent regulatory frameworks establishing de facto global standards and driving premium EDRM solution adoption across enterprise ecosystems.

The European Union's comprehensive regulatory architecture encompassing GDPR (rigorous enforcement with record-breaking penalties, with Meta facing €1.2 billion fine in January 2025 for personal data transfer violations), Digital Operational Resilience Act (DORA) effective January 17, 2025 establishing mandatory digital resilience testing and third-party risk management for financial institutions, Network and Information Security Directive 2 (NIS-2) targeting critical infrastructure cybersecurity, and Cyber Resilience Act (CRA) imposing security-by-design requirements for digital product manufacturers creates comprehensive regulatory demand for EDRM solutions satisfying compliance verification and audit documentation requirements.

The European Union's 2022 financial and insurance activities sector generated €0.9 trillion in value added while employing nearly 5 million people across 867,000 enterprises, with the sector exhibiting substantial wage-adjusted labour productivity and gross operating rate. This establishes Europe as the second-largest BFSI market globally after North America. European healthcare organisations face heightened compliance pressures from GDPR enforcement and sector-specific initiatives, including mandatory security audits, incident reporting requirements, and data processing transparency obligations.

Competitive Landscape

The Global Enterprise Digital Rights Management (EDRM) market is highly competitive, comprising established technology giants and specialised solution providers that focus on protecting sensitive enterprise data across cloud, on-premises, and hybrid environments. Adobe Systems Inc. leads with document security and workflow integration, while Seclore specialises in dynamic data-centric rights management.

Bynder provides digital asset management with integrated content protection, and Oracle Corporation combines EDRM with enterprise software and governance solutions. Vitrium Security secures documents and multimedia with analytics, VeriSign, Inc. offers identity-driven access controls, and FileOpen Systems delivers encryption and audit-trail capabilities for document-centric industries.

Vendors compete on technological innovation, cloud scalability, compliance with global data protection regulations, and ease of integration, making the market fragmented yet dynamic, with continuous advancements through partnerships and acquisitions.

Key Industry Developments:

- On 17 OCT 2025, Adobe for Business Team highlighted the increasing significance of digital rights management (DRM) for enterprises managing high-value digital content. Their overview emphasised how EDRM solutions protect intellectual property, maintain compliance, and preserve brand integrity. The development underlines that modern DRM platforms enforce usage policies, manage licenses, apply encryption, embed watermarks, and provide analytics on content usage. These capabilities allow enterprises to control access, prevent unauthorized sharing, and optimise workflows while ensuring secure collaboration across multiple channels, reflecting the rising adoption of EDRM technologies in corporate digital content management.

- NextLabs, Inc. launched its flagship EDRM solution for SAP, providing policy-driven and automated data protection across both unstructured files and structured transactional data within SAP environments. The solution seamlessly classifies, encrypts, and enforces access controls during data upload, download, and use, ensuring security remains transparent to end users.

Companies Covered in Enterprise Digital Rights Management (EDRM) Market

- Adobe Systems Inc.

- Seclore

- Bynder

- Oracle Corporation

- Vitrium Security

- VeriSign, Inc.

- FileOpen Systems

Frequently Asked Questions

The global Enterprise Digital Rights Management (EDRM) market is projected to be valued at US$ 4.6 Bn in 2026.

The Document Protection segment is expected to account for approximately 33.0% of the global Enterprise Digital Rights Management (EDRM) market by Solution Type in 2026.

The market is expected to witness a CAGR of 13.4% from 2026 to 2033.

The Global Enterprise Digital Rights Management (EDRM) market growth is driven by tightening global data protection regulations, a sharp rise in cyberattacks and intellectual property theft, and the shift toward cloud-based, remote, and zero-trust work environments requiring persistent, identity-aware data protection.

Key market opportunities in the global Enterprise Digital Rights Management (EDRM) market lie in leveraging AI-powered automated data classification and content-aware protection and integrating EDRM with Zero Trust and identity-centric security frameworks to enhance compliance, access control, and operational efficiency.

The key players in the Enterprise Digital Rights Management (EDRM) market include Adobe, Seclore, Oracle, Vitrium Security, Bynder, and FileOpen Systems.