- Hardware & Software IT Services

- Enterprise Performance Management Software Market

Enterprise Performance Management Software Market Size, Share, and Growth Forecast, 2026 – 2033

Enterprise Performance Management Software Market by Component (Software, Services [Consulting, Integration & Implementation, Training & Support, Managed Services]), Deployment (On-Premises, Cloud / SaaS, Hybrid), Application, Industry, and Regional Analysis for 2026 – 2033

Enterprise Performance Management Software Market Size and Trends

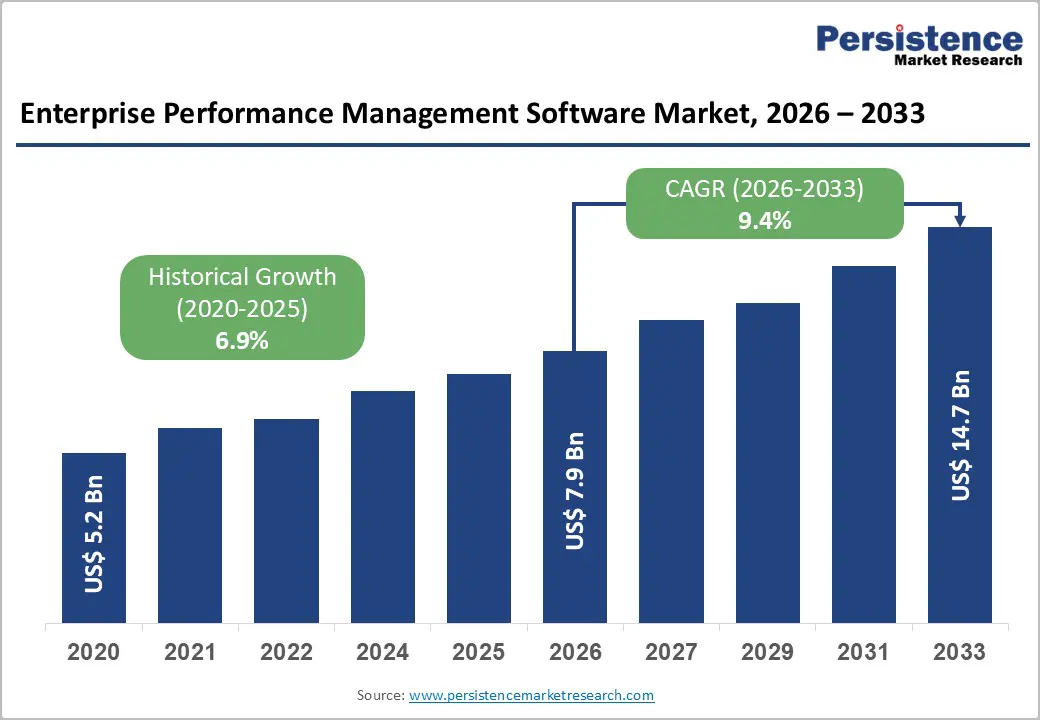

The global Enterprise Performance Management Software Market size is projected to rise from US$7.9 Bn in 2026 to US$14.7 Bn by 2033. It is anticipated to witness a CAGR of 9.4% during the forecast period from 2026 to 2033, driven by the growing complexity of business planning, budgeting, forecasting, and performance measurements across large and mid-sized organizations. As companies seek greater visibility into financial and operational metrics, EPM solutions help streamline strategic planning, enhance decision-making, and align resources with corporate goals. The shift toward automated workflows and the reduction of manual processes drives investment in advanced EPM capabilities.

Key Industry Highlights:

- Leading Component: Software dominates with over 67% market share in 2026, valued at more than US$ 5.3 Bn, driven by the need for real-time visibility into financial and operational performance, scenario modeling, and predictive insights. Services are the fastest-growing segment due to increasing demand for implementation, integration, customization, and ongoing change management support.

- Leading Deployment: On-Premises leads with over 40% market share in 2026, valued at more than US$ 3.2 Bn, due to data control, security, and regulatory compliance needs. Cloud/SaaS is the fastest-growing deployment with a CAGR of 14.9%, driven by agility, real-time collaboration, embedded AI, and lower upfront costs.

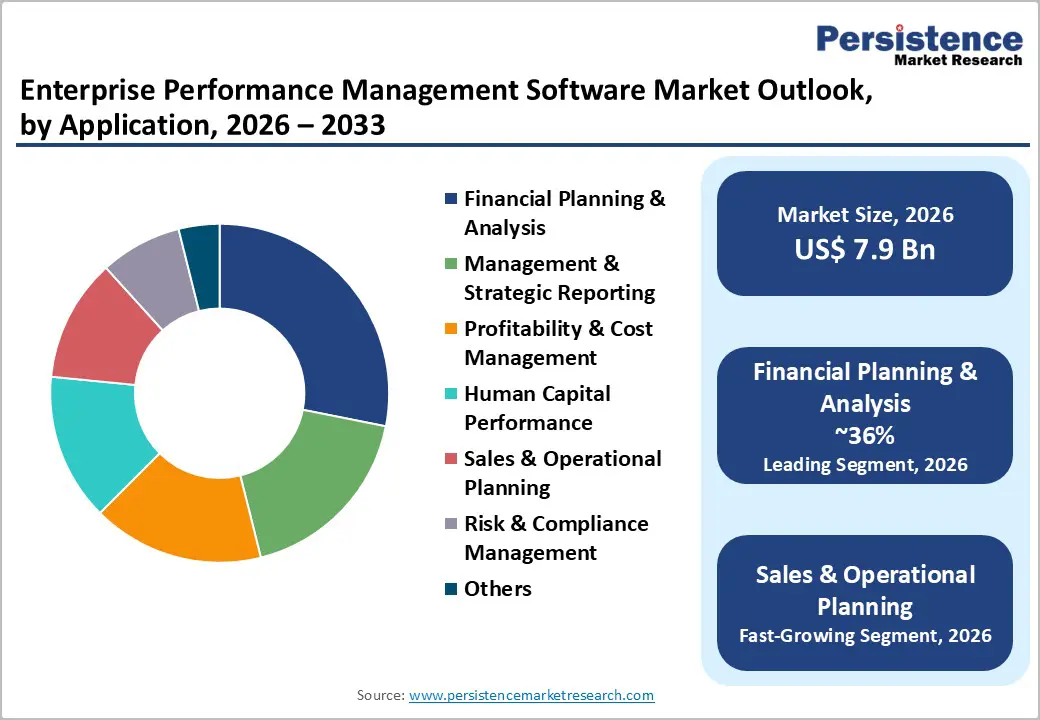

- Leading Application: Financial Planning & Analysis (FP&A) holds over 36% market share in 2026, valued at more than US$ 2.8 Bn, addressing budgeting, forecasting, scenario planning, and profitability analysis. Sales & Operational Planning (S&OP) is the fastest-growing application, driven by demand-supply alignment, rapid what-if analysis, and cross-functional collaboration.

- Leading Industry: BFSI commands the largest share at over 28% in 2026, valued at more than US$ 2.2 Bn, due to real-time forecasting, risk management, and regulatory compliance needs. Healthcare is the fastest-growing industry, driven by cost control, operational efficiency, and resource optimization requirements.

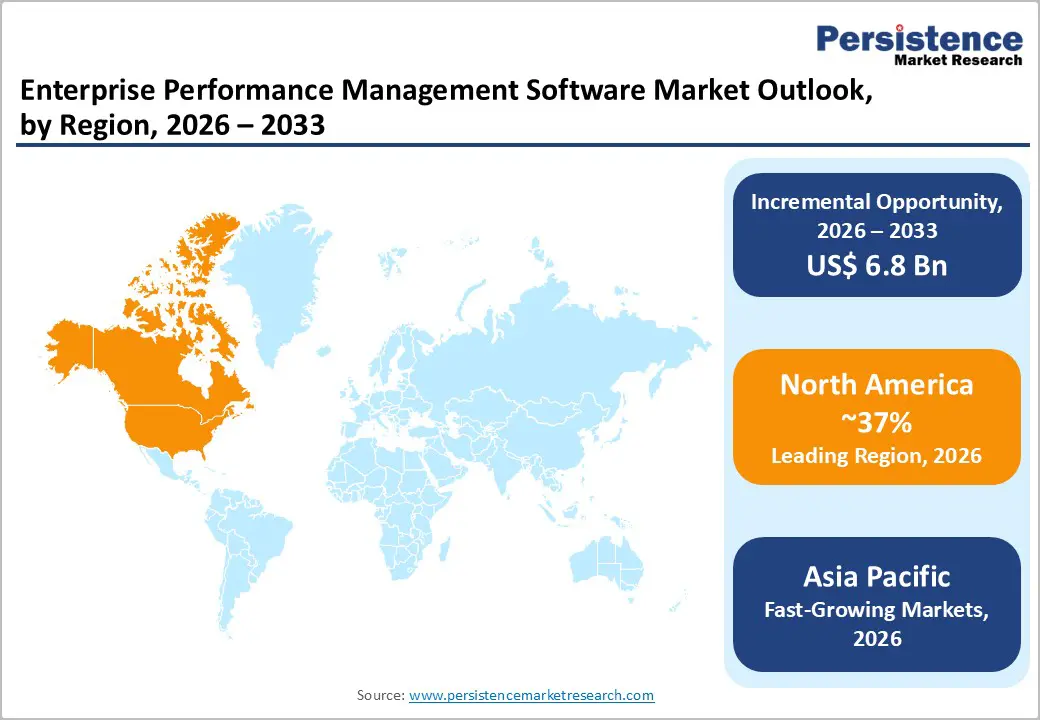

- Leading Region: North America leads with over 37% market share in 2026, valued at approximately US$ 2.9 Bn, supported by mature financial ecosystems, cloud and AI adoption, and regulatory compliance requirements. Asia Pacific is the fastest-growing region with a CAGR of 15.2%, driven by digital transformation, organizational complexity, and government-led initiatives. Europe holds over 21% share, propelled by ESG mandates, regulatory harmonization, and digitalization across industries.

| Global Market Attribute | Key Insights |

|---|---|

| Enterprise Performance Management Software Market Size (2026E) | US$7.9 Bn |

| Market Value Forecast (2033F) | US$14.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.9% |

Market Dynamics

Driver

Escalating Demand for Real-Time Financial Insights and Decision-Making Automation

Business environments become increasingly volatile, and organizations require continuous performance visibility to support faster, data-driven decisions, with over 70% of executives in data-driven enterprises relying on analytics for decision-making. EPM platforms automate core finance functions such as budgeting, forecasting, and consolidation, reducing manual effort while improving accuracy and timeliness. Real-time KPIs and integrated analytics enhance financial transparency and operational control. This enables finance teams to shift focus from transactional tasks to strategic planning and high-value analysis. The demand is especially strong across BFSI, manufacturing, and retail sectors where financial agility is critical.

Operational Efficiency and Performance Optimization

Operational efficiency and performance optimization are central factors accelerating demand for EPM software as organizations seek tighter control over costs, resources, and outcomes. EPM solutions enable enterprises to automate budgeting, forecasting, and financial consolidation, significantly reducing manual effort and cycle times. By integrating financial and operational data into a single performance framework, organizations gain real-time visibility into KPIs, variances, and productivity gaps. EPM platforms also standardize planning and performance processes across business units, minimizing inefficiencies caused by siloed operations. As competitive pressure intensifies, enterprises increasingly rely on EPM tools to continuously monitor performance, improve agility, and drive sustainable operational excellence.

Restraint

High Implementation Complexity and Integration Challenges with Legacy Systems

Organizations rely on legacy on-premises ERP and financial systems, making integration with modern cloud-based EPM platforms technically demanding and costly. Deployment often requires specialized expertise for data migration, system customization, and workflow redesign, particularly in regulated sectors such as BFSI, healthcare, and government, with strict data governance needs. Implementation timelines frequently exceed expectations due to data quality issues and customization requirements. Extensive user training further increases costs. These factors make EPM adoption especially difficult for small and mid-sized enterprises with limited IT resources and capital.

Organizational Change Management and Skills Gap Challenges

Organizations rely on long-standing, spreadsheet-driven planning and reporting practices, making the shift to integrated, analytics-driven EPM platforms culturally and operationally challenging. Limited familiarity with advanced analytics, scenario modeling, and predictive forecasting creates a steep learning curve and internal resistance to change. The shortage of skilled professionals with expertise in EPM platforms, AI-enabled analytics, and system administration raises implementation costs and delays value realization. These challenges are more pronounced in mid-market enterprises, where constrained budgets and limited resources reduce the ability to invest in structured change management and workforce upskilling initiatives.

Opportunity

Regulatory Compliance and Environmental, Social, and Governance (ESG) Reporting Mandates

Global regulations such as the EU’s CSRD under ESRS, alongside TCFD, ISSB standards, and region-specific mandates like those in California, are compelling enterprises to integrate sustainability metrics with financial reporting. This shift is increasing demand for EPM platforms that unify financial, operational, and ESG data within a single governance framework. The rapid expansion of the ESG reporting software space, supported by strong adoption in regulated sectors such as BFSI, further reinforces this demand. Modern EPM solutions enable multi-framework reporting, audit readiness, and real-time performance tracking. As stakeholders seek greater transparency on risk, compliance, and sustainability outcomes, integrated platforms are becoming critical enterprise infrastructure.

Artificial Intelligence and Machine Learning Integration for Predictive Analytics

The integration of AI, machine learning, and generative AI into EPM platforms is creating a significant market opportunity by enabling smarter, faster, and more predictive decision-making. AI-driven EPM solutions improve forecasting accuracy by nearly 20-25% over traditional models, support autonomous anomaly detection, and automate routine analytical tasks. Leading vendors are embedding generative AI for dynamic reporting, natural language queries, and collaboration, enhancing user productivity and decision velocity. Advanced predictive modeling allows enterprises to simulate complex business scenarios with minimal manual effort. Vendors offering intelligent automation and predictive insights are well-positioned to capture strong demand.

Category-wise Analysis

Component Analysis,

Software dominates the global market, capturing more than 67% market share in 2026 with a value exceeding US$ 5.3 Bn, as organizations increasingly need real-time visibility into financial and operational performance to make faster, data-driven decisions. It automates complex planning, budgeting, forecasting, and reporting, reducing manual effort and errors. Enterprises also demand scenario modeling and predictive insights to navigate uncertain business environments. Integrated software supports collaboration across departments, aligning goals and improving strategic execution.

Services demonstrate significant growth as organizations increasingly need expert support to implement, integrate, and customize complex EPM platforms across finance, HR, and operations. As EPM solutions become more cloud-based and AI-driven, enterprises require ongoing advisory, data modeling, and change management services to align systems with evolving business strategies. Continuous regulatory updates, performance optimization, and user training further drive demand for managed and professional services. Companies prefer outcome-based service engagements to ensure faster ROI and sustained performance improvements.

Deployment Analysis,

On-Premises dominate the market, capturing over 40% market share in 2026 with a value exceeding US$ 3.2 Bn, due to enterprise needs around data control, security, and regulatory compliance. Large organizations prefer keeping sensitive financial, budgeting, and forecasting data within their own infrastructure to meet internal governance and audit requirements. On-premises systems also offer deep customization and tighter integration with legacy ERP, finance, and core IT systems that are difficult to migrate to the cloud. Predictable performance, lower long-term costs for high-volume users, and resistance to vendor lock-in continue to reinforce on-premises adoption among mature enterprises.

Cloud / SaaS demonstrate highest growth with a CAGR of 14.9% due to the need for agility, speed, and cost efficiency in planning and reporting. Businesses increasingly require real-time performance visibility, rapid scenario modeling, and collaboration across distributed teams, which cloud platforms enable more effectively. SaaS reduces IT complexity and upfront capital spend, allowing finance teams to focus on insights rather than infrastructure. Continuous updates, embedded AI, and easier integration with ERP and data sources further align cloud EPM with evolving business needs.

Application Analysis,

Financial planning & analysis holds over 36% of the market share in 2026, with a value exceeding US$ 2.8 Bn, as organizations urgently need continuous visibility into revenues, costs, and cash flows amid economic uncertainty and margin pressure. FP&A solutions address core enterprise needs such as budgeting, rolling forecasts, scenario planning, and profitability analysis, which are used across all industries and company sizes. The shift from static annual budgets to dynamic, real-time forecasting has further increased reliance on FP&A platforms.

Sales & operational planning are expected to grow at the highest rate as organizations urgently need better demand–supply alignment in highly volatile markets. Frequent disruptions, shorter planning cycles, and unpredictable customer demand are forcing enterprises to move from static forecasts to continuous, scenario-based planning. Businesses also need cross-functional visibility between sales, operations, finance, and supply chain to improve decision speed and accountability. EPM-based S&OP tools meet these needs by enabling real-time collaboration, predictive forecasting, and rapid what-if analysis across the enterprise.

Industry Analysis,

BFSI commands the largest market share at over 28% in 2026 with a value exceeding US$ 2.2 Bn, due to its need for continuous financial planning, risk management, and regulatory compliance across complex, multi-entity operations. Banks and insurers operate in highly volatile and data-intensive environments, requiring real-time forecasting, stress testing, capital adequacy modeling, and profitability analysis. Frequent regulatory changes demand accurate, auditable, and scenario-based reporting, which EPM platforms are designed to deliver. Intense competition and margin pressure push BFSI firms to rely on EPM solutions for enterprise-wide cost control, performance tracking, and strategic decision-making.

Healthcare is expected to grow at a significant rate due to urgent needs around cost control and operational efficiency. Hospitals and healthcare systems manage complex budgets, reimbursement models, and margin pressures, requiring real-time financial planning and forecasting. Increasing regulatory scrutiny and value-based care models demand accurate performance tracking, outcome measurement, and accountability. Workforce shortages and rising patient demand push healthcare organizations to adopt EPM tools to optimize resource allocation and long-term capacity planning.

Regional Insights

North America Enterprise Performance Management Software Market Trends

North America accounts for over 37% of the Enterprise Performance Management Software market share in 2026, reaching approximately US$ 2.9 Bn, driven by high technology adoption, a mature financial ecosystem, and strong regulatory emphasis on transparency and accountability. The United States anchors regional demand due to the presence of large multinational enterprises, complex financial structures, and strict compliance requirements such as GAAP and evolving IFRS alignment. Adoption is increasingly shifting toward cloud-based and AI-enabled platforms to improve real-time decision-making and operational efficiency. Rising ESG and sustainability reporting requirements are pushing enterprises to adopt integrated EPM solutions that combine financial and non-financial performance management across the organization.

Asia Pacific Enterprise Performance Management Software Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 15.2%, due to accelerating digital transformation, increasing organizational complexity, and government-led digitalization initiatives. China leads adoption as enterprises standardize performance management systems, while Japan shifts from traditional management practices to merit-based evaluation requiring advanced analytics. India shows strong potential with growing enterprise adoption among both domestic and multinational organizations. The sectors such as IT, telecom, and manufacturing drive adoption for real-time operational visibility, supply chain management, and rapid scaling, while Southeast Asian economies are increasingly embracing sophisticated planning and financial management practices.

Europe Enterprise Performance Management Software Market Trends

Europe is expected to hold more than 21% share by 2026, driven by tightening regulatory requirements and accelerating digital transformation across industries. The introduction of mandatory sustainability and integrated reporting regulations is pushing enterprises to adopt platforms that align financial performance with ESG metrics. Adoption varies across key markets such as Germany, the UK, France, and Spain, reflecting differences in regulatory environments and organizational maturity. Manufacturing-led economies like Germany use EPM for cost control, profitability analysis, and supply chain optimization, while financial institutions focus on compliance and consolidated reporting. Regulatory harmonization around IFRS and ESG frameworks is increasing demand for multi-compliance capabilities.

Competitive Landscape

The enterprise performance management software market is moderately consolidated, with a few global platform providers and several specialized vendors competing across regions and use cases. Manufacturers primarily compete by offering end-to-end, cloud-native EPM suites that integrate planning, budgeting, forecasting, and analytics to increase customer stickiness. Continuous innovation in AI-driven forecasting, scenario modeling, and real-time insights is used to differentiate products beyond core financial management.

Key Industry Developments

- In September 2025, Lumel announced the general availability of its Enterprise Performance Management (EPM) solution natively built on Microsoft Fabric, enabling organizations to perform budgeting, forecasting, and scenario planning directly within a unified data environment.

- In April 2025, Oracle NetSuite launched NetSuite Enterprise Performance Management (EPM) in Singapore, enabling organisations to unify planning, budgeting, forecasting, account reconciliation, financial close, reporting, and tax processes on a single AI-powered platform. Built on Oracle Fusion Cloud EPM, the solution helps finance teams automate manual tasks, improve accuracy, and gain predictive insights to support faster, data-driven decision-making and business growth.

Companies Covered in Enterprise Performance Management Software Market

- Oracle Corporation

- SAP SE

- IBM Corporation

- Workday, Inc.

- Anaplan, Inc.

- Microsoft Corporation

- OneStream Software LLC

- Workiva Inc.

- Infor Inc.

- Vena Solutions Inc.

- SAS Institute, Inc.

- Longview Solutions

- BOARD International S.A.

Frequently Asked Questions

The global market is projected to be valued at US$7.9 Bn in 2026.

The need for real-time financial visibility, accurate forecasting, and data-driven decision-making across enterprises is a key driver of the market.

The market is expected to witness a CAGR of 9.4% from 2026 to 2033.

AI-driven analytics, cloud-based planning, and integrated financial and operational insights help organizations optimize performance and make faster, data-backed decisions, creating strong market expansion potential.

Oracle Corporation, SAP SE, IBM Corporation, Workday, Inc., Anaplan, Inc., Microsoft Corporation, OneStream Software LLC, Workiva Inc. are among the leading key players.