- Semiconductor Materials & Components

- Optical Transceivers Market

Optical Transceivers Market Size, Share, and Growth Forecast, 2026 - 2033

Optical Transceivers Market by Form Factor (SFP, SFP+, SFP28; QSFP, QSFP+, QSFP28, QSFP-DD; OSFP; CFP; XFP; Others), by Transmission Rate (Less than 25G, 25G to 100G, 100G to 400G, 400G to 800G, Above 800G), by Application (Data Centers, Telecom, Enterprise, Others), and Regional Analysis for 2026 - 2033

Optical Transceivers Market Size and Trends

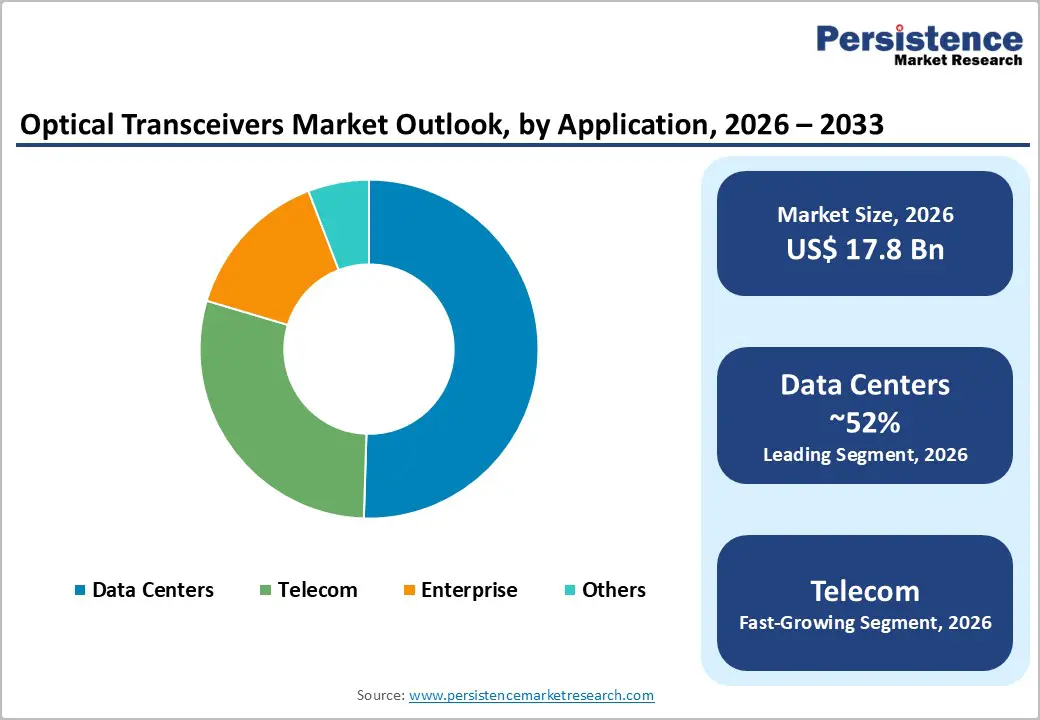

The global optical transceivers market size is projected to rise from US$17.8 billion in 2026 to US$46.5 billion by 2033. It is anticipated to witness a CAGR of 14.7% during the forecast period from 2026 to 2033, driven by the surging demand for high-speed data transmission and bandwidth-intensive applications.

The exponential growth of hyperscale data centers, widespread rollout of 5G networks, and accelerating cloud computing adoption are collectively driving unprecedented requirements for high-capacity optical interconnects. According to the International Telecommunication Union (ITU), global internet traffic is projected to more than triple by 2030, necessitating robust optical networking infrastructure.

Key Industry Highlights:

- Leading Offering: SFP, SFP+, SFP28 dominate with over 46% share in 2026, valued at more than US$ 8.2 Bn, due to their high-speed, flexible, and cost-efficient network connectivity. QSFP, QSFP+, QSFP28, QSFP-DD are the fastest-growing form factors at a CAGR of 17.8%, driven by ultra-dense port configurations, higher bandwidth requirements, and energy-efficient deployment in modern networks.

- Leading Transmission Rate: 100G–400G holds over 36% share in 2026, valued at more than US$ 6.4 Bn, offering a balance of bandwidth, energy efficiency, and scalability. 400G–800G is the fastest-growing segment at a CAGR of 18.2%, fueled by AI workloads, high-bandwidth applications, and multi-GPU cluster requirements.

- Leading Application: Data Centers command the largest market share at over 52% in 2026, valued at more than US$ 9.3 Bn, driven by cloud computing, AI, big data analytics, and demand for high-density, low-latency interconnects. Telecom is the fastest-growing application at a CAGR of 18.7%, supported by 5G rollout, fiber upgrades, and the need for scalable, high-speed connectivity.

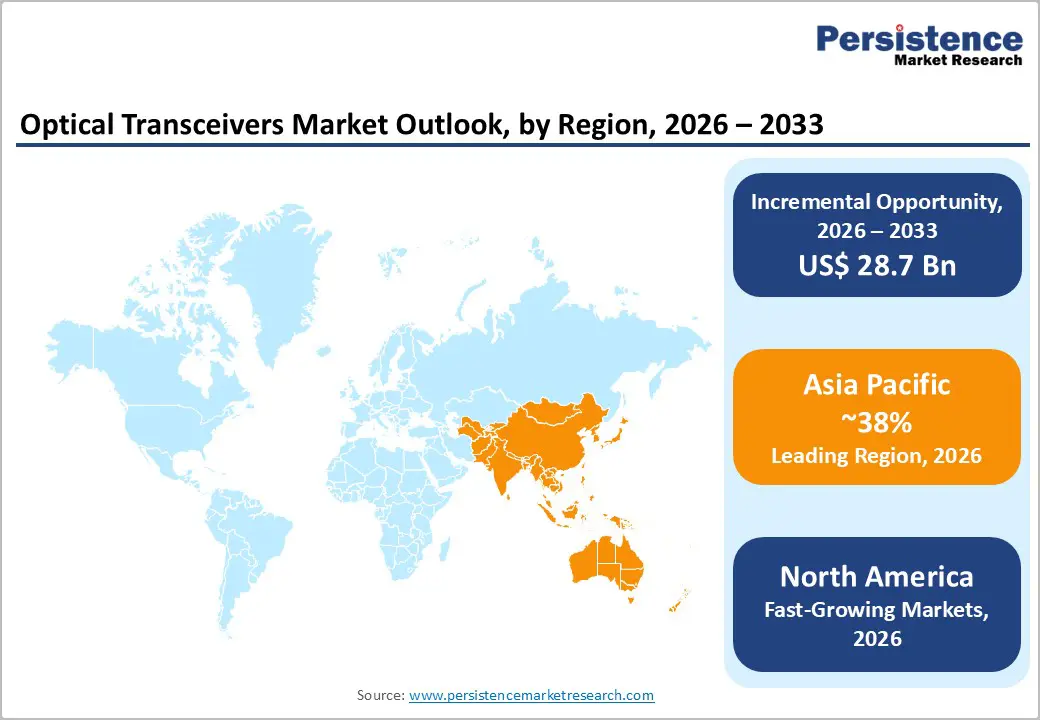

- Leading Region: North America leads with a CAGR of 13.9%, supported by hyperscale cloud hubs, early 5G adoption, federal broadband initiatives, and domestic photonics innovation. Asia Pacific holds over 38% share in 2026, reaching US$ 6.8 Bn, driven by China’s telecom expansion, rapid 5G deployment, and growing data center construction. Europe accounts for more than 21% share, propelled by coordinated 5G rollouts, digital transformation programs, and data center densification across Germany, the UK, France, and the Netherlands.

| Key Insights | Details |

|---|---|

|

Optical Transceivers Market Size (2026E) |

US$17.8 Bn |

|

Market Value Forecast (2033F) |

US$46.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.9% |

Market Dynamics

Driver - Rapid Growth of Hyperscale Data Centers and Cloud Infrastructure

The rapid expansion of hyperscale data centers worldwide is a key driver for the optical transceivers market. Leading cloud service providers, including Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, are continuously scaling their infrastructure to meet growing demands from artificial intelligence, machine learning, and big data applications. This growth requires high-density, low-latency optical interconnects, which in turn boosts the adoption of advanced transceiver technologies. There are now approximately 1,300 large data centers operated by hyperscale providers globally, with AWS, Google, and Microsoft collectively controlling more than 50% of all data center capacity. As a result of this rapid growth and utilization, global data center electricity consumption is projected to reach ~1,000 terawatt-hours (TWh) by 2026, highlighting the scale and energy demands of the expanding infrastructure.

Rising GPU Cluster Requirements Boost Optical Transceiver Market Growth

The surge in AI training requiring massive multi-GPU collaborative computing is a major factor driving demand. Traditional servers use only 2–4 ports per machine, whereas AI servers with 8 GPUs demand 24–32 ports, a 6–8× increase, to support high-frequency GPU data interaction. As clusters scale to 100,000 GPUs, the optical transceiver-to-GPU ratio rises from 1:1 to 1:4, tripling or quadrupling per-cabinet demand. This expansion also necessitates higher-speed transceivers, as rates of 400G and below cannot meet the low-latency, high-bandwidth requirements of large AI clusters, making advanced optical transceivers essential for training efficiency.

Restraint - High Manufacturing Costs and Component Supply Chain Vulnerabilities

The production of optical transceivers involves precision photonic components including laser diodes, photodetectors, and optical lenses that require stringent manufacturing tolerances and specialized fabrication processes. This results in elevated unit costs, particularly for 400G and 800G modules, which range from US$ 500 to over US$ 2,000 per unit depending on specifications. Supply chain disruptions, as evidenced during the COVID-19 pandemic and ongoing semiconductor shortages, have further complicated procurement timelines. Dependence on a limited number of high-purity substrate suppliers, particularly for Indium Phosphide (InP) and Gallium Arsenide (GaAs), creates concentration risks that constrain production scalability and inflate overall product costs for end-users.

Technical Complexity of Interoperability and Standardization Gaps

The optical transceivers ecosystem is fragmented across a wide array of form factors, protocols, and vendor-specific implementations, creating significant interoperability challenges for network operators. Despite efforts by industry bodies such as Multi-Source Agreement (MSA) groups and the IEEE 802.3 standards committee, variations in implementation across QSFP-DD, OSFP, and CFP8 platforms continue to impede seamless network interoperability. Migration from legacy 10G and 100G infrastructure to next generation 400G+ architectures requires substantial capital investment and technical expertise. This requirement limits adoption velocity among small and mid-sized enterprise operators.

Opportunity - CPO Technology Unlocks Extreme Density and Business Model Innovation

CPO (Co-Packaged Optics) technology offers a major growth avenue by supporting ultra-high-speed data rates of 3.2T and above while cutting package size by 50%. This is driving closer collaboration between optical transceiver manufacturers and switch chip developers, requiring joint design, R&D, and optimization of interfaces, architecture, and thermal solutions. Companies that embrace this integrated approach secure strategic partnerships, deliver high-performance optoelectronic systems, and expand their presence in hyperscale data centers and AI-focused networking infrastructure. The evolution toward co-designed systems also opens opportunities for innovative business models and premium product offerings.

Telecom Upgrades and Form Factor Advances

The global shift toward 5G and high-speed fiber networks demands higher bandwidth, lower latency, and more reliable connectivity, increasing the need for advanced optical transceivers. Standardization across protocols and form factors, promoted by organizations like IEEE and MSA groups, simplifies integration and reduces interoperability issues, enabling faster deployment. Innovations in compact and high-density form factors such as QSFP-DD, OSFP, and CFP8 allow network operators to scale capacity while saving space and power. This convergence of network upgrades, standardization, and form factor innovation creates opportunities for transceiver manufacturers to develop next-generation solutions that meet the evolving demands of telecom operators worldwide.

Category-wise Insights

By Form Factor

SFP, SFP+, SFP28 dominate the global market, capturing more than 46% market share in 2026 with a value exceeding US$ 8.2 Bn, due to their ability to meet the growing demand for high-speed, flexible, and cost-efficient network connectivity. These form factors support a range of data rates from 1G to 25G, making them ideal for enterprise networks, data centers, and metro networks. Their compact size and hot-swappable design simplify network upgrades and expansions, while broad vendor support ensures interoperability and easy deployment. This combination of scalability, efficiency, and reliability drives their widespread adoption.

QSFP, QSFP+, QSFP28, QSFP-DD are expected to grow at the highest rate, with a CAGR of 17.8%, as modern networks demand higher bandwidth and faster data rates to handle massive traffic. Their compact design supports ultra-dense port configurations, reducing space and power requirements in switches and servers. Network operators prioritize scalable, high-performance, and energy-efficient solutions. Their versatility makes them essential for next-generation connectivity.

By Transmission Rate

100G to 400G hold over 36% market share in 2026, with a value exceeding US$ 6.4 Bn, as modern networks demand ultra-high-speed data transfer to handle massive volumes of cloud computing, AI workloads, and video streaming. These transceivers offer a cost-effective balance between bandwidth, energy efficiency, and scalability, supporting multi-terabit links without frequent hardware upgrades. Their compatibility with existing infrastructure and ability to future-proof networks for next-generation applications make them the preferred choice for operators.

400G to 800G is expected to grow at the highest rate, with a CAGR of 18.2%, due to surging demand for high-bandwidth applications and ultra-low latency connections. Operators need faster links to handle massive traffic from AI, streaming, and real-time analytics. Enterprises are upgrading networks to support denser computing and multi-GPU configurations, which require higher-speed transceivers. Network operators are consolidating links to reduce port counts while increasing throughput, making 400G–800G modules essential.

By Application

Data Centers command the largest market share at over 52% in 2026, with a value exceeding US$ 9.3 Bn, due to their growing need for ultra-high-speed data transmission and low-latency connectivity. The surge in cloud computing, big data analytics, and AI workloads drives massive demand for high-density interconnects. Optical transceivers enable efficient scaling of server-to-server and server-to-switch communication. Energy-efficient and compact solutions are critical for modern hyperscale data centers, further boosting their adoption.

Telecom is expected to grow at a CAGR of 18.7% due to rapid expansion to support higher data traffic from 5G, fiber-to-the-home, and broadband services, driving the need for faster, more reliable connections. Upgrades to backbone and metro networks demand higher-capacity optical transceivers to handle increased bandwidth efficiently. The push for low-latency and energy-efficient communication also fuels adoption. Standardization of newer form factors and protocols enables smoother integration, meeting operators’ urgent need for scalable, high-speed infrastructure.

Regional Insights

North America Optical Transceivers Market Trends

North America is expected to grow at a significant rate with a CAGR of 13.9%, led by hyperscale cloud hubs in Northern Virginia, Dallas, Chicago, and Silicon Valley, alongside early 5G adoption and strong enterprise tech investment. The U.S. CHIPS and Science Act, allocating over US$52 billion to semiconductor manufacturing and R&D, is boosting domestic photonics innovation and supporting transceiver supply chains. Federal initiatives like the FCC and NTIA’s BEAD Program, committing US$42 billion to broadband expansion, are accelerating fiber deployment and driving transceiver demand. In Canada, the Universal Broadband Fund similarly fuels optical networking investments, collectively expanding the regional market opportunity.

Asia Pacific Optical Transceivers Market Trends

Asia Pacific holds over 38% share in 2026, reaching US$ 6.8 Bn value, due to China’s extensive telecom infrastructure and rapid 5G deployment. Japan’s NTT Group and South Korea’s KT Corporation are upgrading core networks to support 400G optical transport, boosting demand for high-capacity transceivers. The region’s manufacturing hubs in China, Taiwan, and South Korea further strengthen its position in global transceiver supply chains. Growing data center construction in ASEAN countries, including Singapore, Indonesia, and Vietnam, is supporting increased optical component demand.

Europe Optical Transceivers Market Trends

Europe is expected to hold more than 21% share by 2026, fueled by coordinated 5G rollouts, digital transformation initiatives, and rising data center investments across Germany, the UK, France, and the Netherlands. The EU Digital Decade 2030 framework continues to push for gigabit-capable connectivity and ubiquitous 5G coverage by 2030, prompting operators like Deutsche Telekom, Orange, and BT Group to accelerate fiber and optical network densification. Harmonized regulation under the European Electronic Communications Code (EECC) is streamlining spectrum allocation and infrastructure deployment approvals, reducing rollout times. At DE-CIX Frankfurt Europe’s largest internet exchange annual traffic reached 48 exabytes in 2025, and peak throughput hit 18.73 Tbps, highlighting surging data demand and the need for high-density optical transceivers across telecom and enterprise applications.

Competitive Landscape

The global optical transceivers market exhibits a moderately consolidated structure, with a combination of vertically integrated photonics conglomerates and specialized transceiver manufacturers competing for market share. Leading players pursue aggressive R&D investment in silicon photonics, co-packaged optics (CPO), and pluggable 800G module development. Chinese manufacturers compete on cost efficiency and scale, capturing significant market share in hyperscale deployments.

Key Industry Developments

- In March 2025, Broadcom Inc. expanded its optical interconnect portfolio for AI infrastructure, showcasing innovations in 200G/lane DSPs, 400G optics, co-packaged optics (CPO), and PCIe Gen6 over optics. These solutions enable high-bandwidth, low-power, and low-latency connectivity for next-generation AI clusters.

- In March 2025, Coherent Corp. launched its 800G ZR/ZR+ transceiver in QSFP-DD form factor, enabling high-speed, scalable metro, regional, and data center interconnects. The module supports up to 2000 km transmission without additional amplification, offering cost-efficient integration for IP-over-DWDM networks.

Companies Covered in Optical Transceivers Market

- Cisco Systems, Inc.

- Coherent Corp.

- Broadcom Inc.

- Lumentum Holdings Inc.

- Sumitomo Electric Industries Ltd.

- InnoLight Technology

- Accelink Technologies Co., Ltd.

- NeoPhotonics Corporation

- Fujitsu Optical Components Ltd.

- ATOP Technologies Co., Ltd.

- Huawei Technologies Co., Ltd.

- Others

Frequently Asked Questions

The global optical transceivers market is projected to be valued at US$17.8 Bn in 2026.

The need for faster, high-capacity, and energy-efficient data transmission to support growing internet traffic, 5G networks, and expanding data center connectivity are key driver of the market.

The market is expected to witness a CAGR of 14.7% from 2026 to 2033.

Leveraging CPO technology and high-density form factors to deliver ultra-fast, compact, and energy-efficient transceivers for 5G and next-generation fiber networks is creating strong growth opportunities.

Cisco Systems, Inc., Coherent Corp., Broadcom Inc., Lumentum Holdings Inc., Sumitomo Electric Industries Ltd., InnoLight Technology, Accelink Technologies Co., Ltd. are among the leading key players.