- Sensors & Controls

- Optical Encoders Market

Optical Encoders Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Optical Encoders Market by Product (Absolute Encoders, Incremental Encoders), Output (Digital, Analog), Form Factor (Shafted Encoders, Hollow Shaft Encoders, Kit Encoders, Others), Application, and Regional Analysis for 2026 - 2033

Optical Encoders Market Size and Trends Analysis

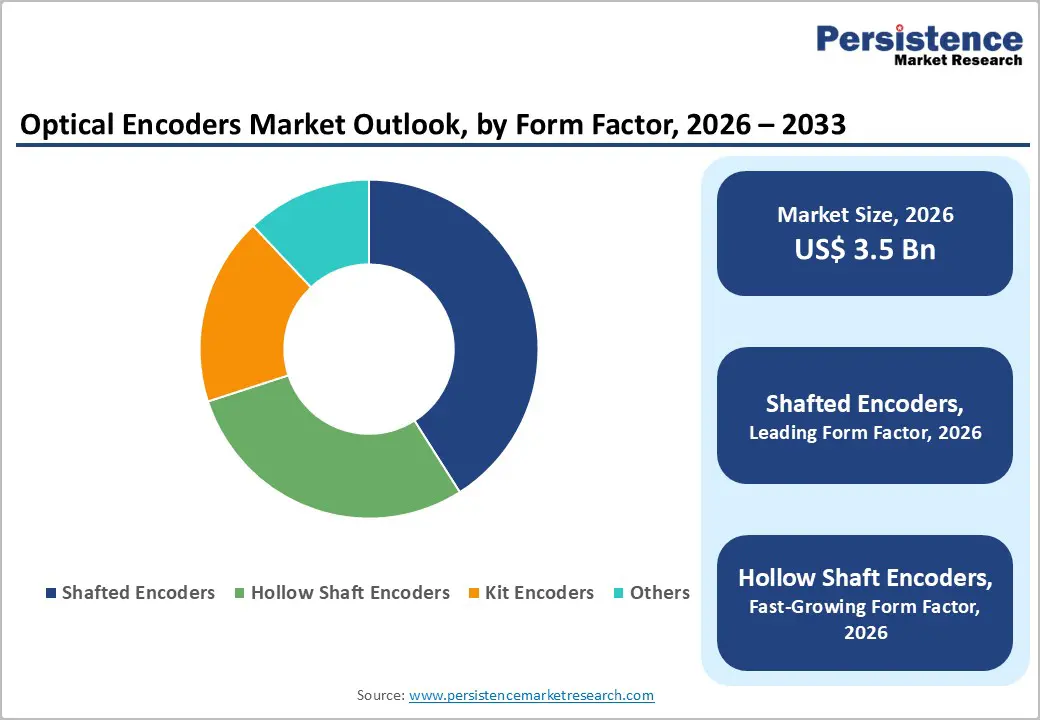

The global optical encoders market size is projected to rise from US$3.5 billion in 2026 to US$7.1 billion by 2033. It is anticipated to witness a CAGR of 10.4% during the forecast period from 2026 to 2033.

This robust expansion is driven by growth in industrial automation, Industry 4.0 initiatives, and rising adoption of collaborative robotics and advanced automation systems across manufacturing ecosystems. The surge in electric vehicle production and the increasing demand for high-precision motion control and real-time position feedback have made optical encoders essential for monitoring rotational and linear motion. Advances in miniaturized, high-resolution encoder designs are further enhancing performance while reducing costs.

Key Industry Highlights:

- Leading Product: Absolute encoders dominate with over 60% market share in 2026, valued at more than US$ 2.1 Bn, driven by unambiguous position tracking, multi-turn memory retention, and critical applications in EV powertrains, industrial automation, and robotics. Incremental encoders are expanding rapidly, with a 9.4% CAGR, driven by their cost-effectiveness, simplicity, and versatility in speed and position measurement.

- Leading Output: Digital output encoders hold the largest share, over 62% in 2026, valued at more than US$ 2.2 Bn, due to their high accuracy, noise immunity, and compatibility with IoT-enabled and smart manufacturing systems. Analog output encoders maintain a significant presence for legacy and cost-sensitive applications, projected to exceed US$ 2.3 Bn by 2033.

- Leading Form Factor: Shafted encoders lead with over 41% share in 2026, valued at over US$ 1.4 Bn, preferred for robust, high-accuracy motion feedback in motors, robotics, and conveyor systems. Hollow shaft encoders are growing at the fastest rate of CAGR 14.9% due to demand for compact, space-saving, and easily integrated solutions in automotive, CNC, and robotic applications.

- Leading Application: Industrial automation accounts for over 28% market share in 2026, valued at more than US$ 986.2 Mn, driven by the need for precise motion control, high-speed accuracy, and reduced human error in production lines. Robotics and cobots are the fastest-growing applications, projected to exceed US$ 1.6 Bn by 2033, fueled by AI-enabled robots, multi-axis motion feedback, and collaborative manufacturing demands.

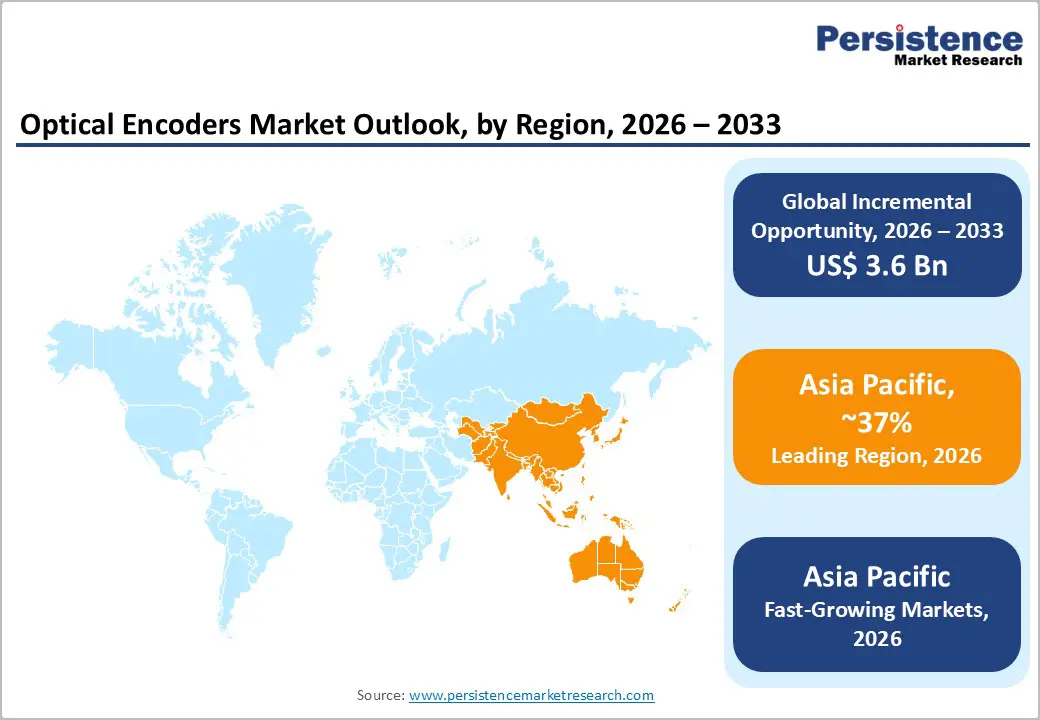

- Leading Region: Asia Pacific dominates with over 37% market share in 2026, valued at US$ 1.3 Bn, led by China’s adoption of industrial automation and robotics, Japan’s precision encoder technology, and South Korea’s semiconductor expansion. North America holds over 30% share in 2026, valued at US$ 1.1 Bn, driven by U.S. investments in semiconductor manufacturing, automotive electrification, and AI-driven positioning systems. Europe accounts for over 22% of the market in 2026, valued at US$ 535.1 Mn, led by automotive electrification, industrial automation, and EU-wide energy-efficiency initiatives.

| Key Insights | Details |

|---|---|

|

Optical Encoders Market Size (2026E) |

US$3.5 Bn |

|

Market Value Forecast (2033F) |

US$7.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.2% |

Market Dynamics

Driver - Electric Vehicle Manufacturing and Electrification Momentum

Global electric vehicle adoption is rapidly expanding, with electric car sales topping 17 million worldwide in 2024, rising by more than 25%. This growth is driving strong demand for high-precision motion control and position sensing technologies across battery production, motor control systems, and advanced driver assistance systems (ADAS). EV battery fabrication requires precise feedback for quality and dimensional consistency, while powertrain systems depend on absolute encoder feedback for torque modulation, regenerative braking coordination, and multi-motor synchronization. Regulatory efficiency and emissions standards across North America, Europe, and Asia-Pacific further reinforce the need for sophisticated encoder solutions in modern vehicles.

Semiconductor Manufacturing and Advanced Processing

Semiconductor manufacturing is a high-precision domain where optical encoders ensure accurate equipment positioning and wafer handling. The industry rebounded post-2023, with semiconductor sales of $69.5 billion in September 2025, increasing to $72.7 billion in October 2025, up 4.7% month-on-month and 27.2% compared to October 2024 ($57.2 billion). Advanced chip fabrication relies on encoder-driven precision in lithography equipment, wafer steppers, and automated assembly systems. Its capital-intensive nature and ongoing technological advancements sustain demand for high-performance encoders, while regional incentives, such as the U.S. CHIPS Act and European semiconductor initiatives, further drive equipment procurement.

Restraint - Premium Pricing and Economic Capital Constraints

High-end optical encoders carry significant price premiums, often 3–5× higher than equivalent magnetic encoder solutions from manufacturers like Renishaw and Heidenhain. Limited capital budgets, particularly in SMEs, restrict adoption to essential applications, segmenting the market and slowing growth. In developing regions, adoption cycles are further delayed due to cumulative factory modernization costs. Legacy system compatibility also poses challenges, as retrofitting high-resolution optical encoders often requires modifications to existing machinery, extending replacement cycles to 7–10 years compared to 3–4 years for greenfield automation projects.

Technical Standardization Gaps and Integration Complexity

Disparate communication protocols across industrial applications (Ethernet/IP, EtherCAT, Profibus, SSI, CANopen) fragment the optical encoder market and complicate multi-vendor system integration. Sealed encoders designed for harsh environments, extreme temperatures, moisture, and vibration add design complexity and increase manufacturing costs, limiting adoption in cost-sensitive segments. Emerging data security and cybersecurity regulations, such as the EU Cyber Resilience Act, effective December 2024, require integrated security architectures, introducing engineering challenges and extended certification timelines that can delay product commercialization.

Opportunity - Miniaturization and IoT-Integrated Encoder Solutions

The growing demand for compact, IoT-enabled sensing technologies creates market expansion opportunities for miniaturized optical encoders with wireless connectivity and cloud-capable data transmission. These advanced encoders enable real-time performance monitoring, predictive maintenance, and autonomous system adjustments, commanding significant value premiums over conventional devices. Healthcare applications, including surgical robotics and diagnostic imaging systems, increasingly require precision encoders. Smart city initiatives in Asia Pacific region are fueling demand for position sensing in autonomous vehicles, smart traffic management, and logistics automation.

AI-Powered Encoder Optimization and Predictive Analytics

AI-powered encoder optimization and predictive analytics are driving growth in the optical encoders market. Advanced diagnostics enable condition-based maintenance, reducing unplanned downtime by around 20% and optimizing spare parts logistics. AI-enhanced monitoring systems can cut maintenance costs by 25–35%, delivering strong ROI and accelerating adoption. Integration with IoT and cloud platforms allows real-time performance monitoring and autonomous decision-making, positioning optical encoders as intelligent, self-optimizing components in high-precision industries.

Category-wise Analysis

Product Insights

Absolute encoders command over 60% share in 2026 with a market value exceeding US$ 2.1 Bn. Absolute encoder architecture enables unambiguous position tracking across entire rotation ranges without requiring initialization sequences, providing critical advantages in applications experiencing power interruptions or emergency shutdown scenarios. It benefits from advancing integration capabilities; modern multi-turn absolute encoders incorporate battery-backed memory systems enabling position retention across extended power outages, addressing reliability requirements in mission-critical infrastructure.

Incremental encoders are expanding at a CAGR of 9.4% through the forecast period, due to their simplicity, cost-effectiveness, and versatility in measuring speed, position, and direction in real time. Industries increasingly require precise motion control in automation, robotics, and industrial machinery, where compact and reliable feedback systems are essential. Their ease of integration with modern PLCs and IoT-enabled systems meets the rising demand for scalable, accurate, and maintainable sensing solutions across manufacturing and automation applications.

Output Insights

Digital output encoders are expected to hold over 62% market share in 2026 and have a value exceeding US$ 2.2 Bn, due to their high accuracy, noise immunity, and reliable signal output. Their compatibility with modern control systems and ability to support real-time data processing meet the growing demand for smart, connected devices. Digital encoders reduce error accumulation compared to analog types, making them the preferred choice for industries requiring consistent performance and low maintenance. Digital output demonstrates accelerated growth at CAGR of 15.1%, reflecting structural technology migration toward connected, data-centric manufacturing paradigms.

Analog output encoders retain a significant market presence, projected to exceed US$ 2.3 Bn by 2033, supporting legacy system maintenance and cost-sensitive industrial applications. It continues serving motor speed feedback, position tracking, and simple automation machinery, where digital signal processing integration lacks justification due to application simplicity or equipment age profiles. Technological convergence initiatives increasingly integrate analog output encoders into hybrid architectures that combine analog feedback with digital supervisory systems, extending the technology lifecycle while establishing upgrade pathways toward fully digital architectures.

Form Factor Insights

Shafted encoders dominate with over 41% market share in 2026 and a value exceeding US$ 1.4 Bn, driven by their ability to provide precise rotational position and speed feedback across a wide range of applications. They meet the demand for robust, high-accuracy motion control in motors, robotics, and conveyor systems. The compatibility of shafted encoders with existing mechanical setups and their ease of integration across diverse machinery further drive their adoption. Industries increasingly prefer shafted designs for reliability in harsh environments, supporting consistent performance and low maintenance needs.

Hollow shaft encoders are expanding at the fastest rate, with a CAGR of 14.9%, due to the increasing demand for compact, lightweight, and space-saving solutions. Their design allows direct mounting on motor shafts, reducing coupling errors and improving accuracy, which is critical for precision machinery. Industries such as automotive, robotics, and CNC machinery increasingly require high-speed, maintenance-free, and easily integrated sensing solutions, driving adoption. The rise of smart manufacturing and IoT-enabled equipment further boosts the need for hollow shaft designs that support seamless connectivity and real-time monitoring.

Application Insights

Industrial automation commands over 28% market share in 2026 with a value exceeding US$ 986.2 Mn, due to the rising need for precise motion control, real-time position feedback, and high-speed accuracy in automated production lines. Manufacturers increasingly require encoders to improve productivity, reduce human error, and ensure consistent quality across robotics, CNC machines, and material handling systems. Labor shortages and cost pressures are accelerating the shift toward fully automated and digitally monitored industrial operations.

Robotics & cobots are the fastest-growing application with value exceeding US$ 1.6 Bn by 2033, driven by their critical need for high-precision position, speed, and torque feedback. Cobots require safe, accurate, and real-time motion control to operate alongside humans, increasing demand for high-resolution and low-latency encoders. The rise of flexible manufacturing, warehouse automation, and AI-enabled robots further amplifies the need for compact, reliable encoders. Multi-axis robots require encoders on every joint, significantly boosting unit demand per system.

Regional Insights

North America Optical Encoders Market Trends

North America holds a strong position in the optical encoders market, with value exceeding US$ 1.1 Bn by 2026, led by the U.S., which is expected to surpass US$ 824.2 Mn. The region accounts for over 30% of the global market share, supported by mature industrial infrastructure, advanced manufacturing, and strict automation safety standards. U.S. dominance is reinforced by CHIPS Act investments in semiconductor fabrication and incentives for automotive electrification, accelerating encoder adoption. A robust innovation ecosystem enables integration of optical encoders into AI-driven positioning and sensor fusion systems, while regulatory focus on precision and workplace safety sustains consistent demand across manufacturing sectors.

Asia Pacific Optical Encoders Market Trends

Asia Pacific dominates the market, holding over 37% share by 2026 with value reaching US$ 1.3 Bn, driven by rapid industrial automation and manufacturing expansion. China anchors regional growth through Made in China 2025, accelerating adoption of robotics and factory automation, and fostering cost-competitive local encoder manufacturing alongside global players. Japan sustains technology leadership in miniaturized and high-precision encoders, while South Korea’s semiconductor and electronics manufacturing expansion fuels strong demand. India and ASEAN economies are scaling up manufacturing capacity through equipment imports and local production, supporting encoder demand across both domestic and export-oriented machinery.

Europe Optical Encoders Market Trends

Europe is projected to account for over 22% of the market share by 2026, with a value exceeding US$ 535.1 Mn. Germany, the U.K., France, and Spain drive demand through automotive electrification, industrial automation, robotics, and renewable energy deployment, where precise motion and position feedback is critical. EU policy frameworks such as the Fit for 55 package and the European Green Deal accelerate the adoption of energy-efficient manufacturing systems, increasing encoder usage in servo motors, industrial drives, EV powertrains, and wind and solar tracking systems. Germany’s strong automotive and machinery export base positions it as a core demand hub, while Spain and southern Europe benefit from rapid investment in solar and automation. EU-wide regulatory harmonization on safety, EMC, and eco-design, along with Industrie 4.0 and VDMA digital standardization initiatives, supports widespread adoption of standardized, high-precision encoder technologies across the region.

Competitive Landscape

The optical encoders market is moderately fragmented, with global leaders competing alongside strong regional and niche manufacturers. Leading players focus on technology differentiation through higher resolution, compact designs, and ruggedized encoders for harsh industrial environments. Manufacturers are also focusing on application-specific customization for robotics, CNC machines, and automation systems to lock in OEM partnerships. Cost-competitive pricing and localized manufacturing are used to defend share against emerging Asian suppliers.

Key Industry Developments

- In September 2025, Encoder Products Company launched the LP1 Accu-LaserPro, a non-contact laser-based optical encoder for packaging, labeling, material handling, and industrial automation applications. The LP1 measures speed and distance without physical contact, eliminating slip, reducing maintenance, and preventing material wear or marking.

- In September 2024, Renishaw introduced longer FORTiS enclosed optical encoder scales, now up to 4.24 m, to support high-precision large CNC machines. These encoders enable accurate position feedback for applications like giga casting dies, vertical turning lathes, and large gantry machines in automotive and industrial manufacturing.

Companies Covered in Optical Encoders Market

- Broadcom Inc.

- Honeywell International Inc.

- Renishaw plc

- Sensata Technologies

- Bourns, Inc

- Hans Turck GmbH & Co. KG

- CTS Corporation

- Allied Motion Technologies, Inc.

- Baumer Electric AG

- FSI Technologies, Inc.

- Exxelia Group

- Dr. Fritz Faulhaber GmbH & Co. KG

- Others

Frequently Asked Questions

The global optical encoders market is projected to be valued at US$3.5 Bn in 2026.

Growing demand for precise motion control and position feedback in applications is a key driver of the market.

The market is expected to witness a CAGR of 10.4% from 2026 to 2033.

The adoption of miniaturized, IoT-integrated optical encoders for smart factories, robotics, and autonomous systems is creating strong growth opportunities.

Broadcom Inc., Honeywell International Inc., Renishaw plc, Sensata Technologies, Bourns, Inc, are among the leading key players.