- Semiconductor Materials & Components

- Diffractive Optical Element Market

Diffractive Optical Element Market Size, Share, and Growth Forecast, 2025 - 2032

Diffractive Optical Element Market by Product Type (Beam Shapers, Beam Splitters, and Beam Diffusers), Application (Laser Material Processing, Biomedical Devices, LiDAR, Lithographic and Holographic Lighting, Optical Sensors, Communication, and Others), Industry and Regional Analysis for 2025 - 2032

Diffractive Optical Element Market Size and Trends Analysis

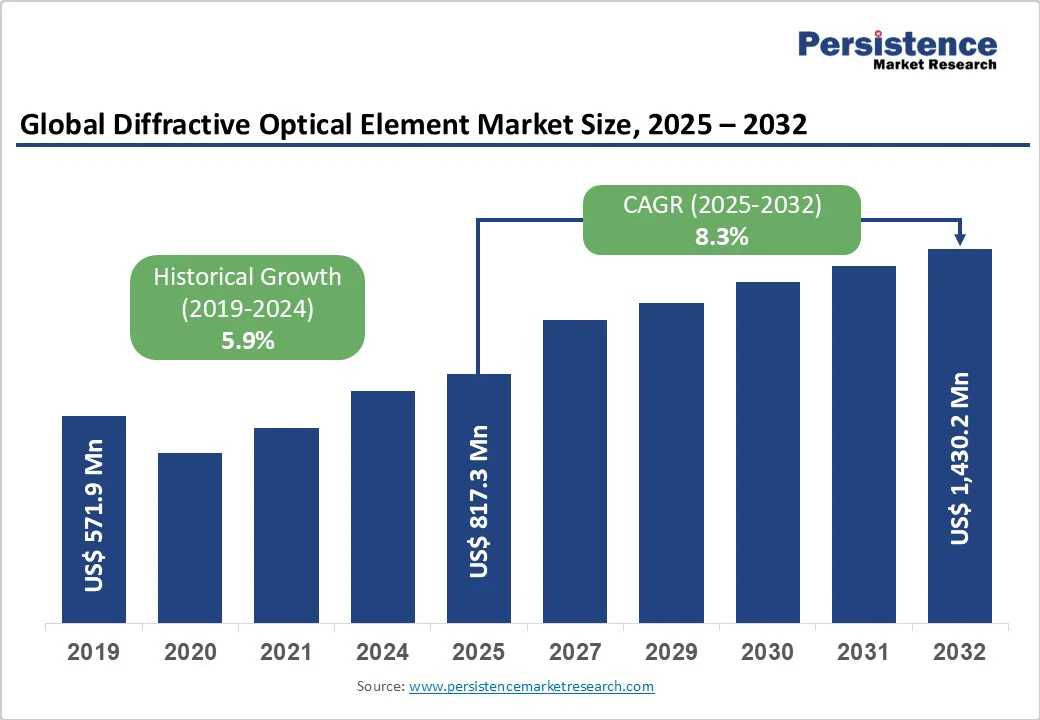

The global diffractive optical element (DOE) market size is likely to value US$817.3 Mn in 2025 to US$1,430.2 Mn by 2032, growing at a CAGR of 8.3% during the forecast period from 2025 to 2032. The miniaturization of optical systems and the rising demand for compact, energy-efficient solutions are fueling the adoption of DOEs. Advancements in nanofabrication and optical design are increasing their precision, versatility, and accessibility. The growing need for high-performance optical solutions in emerging applications is driving sustained market growth.

Key Industry Highlights:

- Leading Product Type: Beam splitters dominate with over 52% share in 2025 due to precise light division and multifunctional capabilities, while beam shapers are growing fastest, driven by demand for uniform beam intensity and high-precision beam profiling.

- Leading Application: Biomedical devices account for more than 27% share in 2025, driven by precision optics in imaging, diagnostics, and minimally invasive surgery.

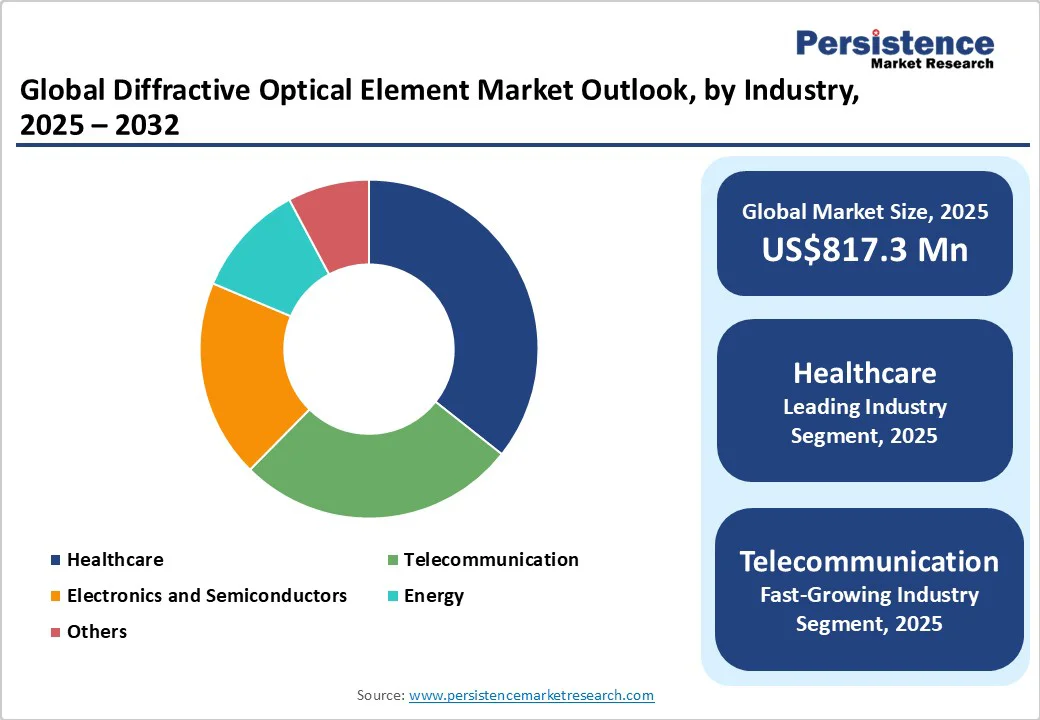

- Leading Industry: Electronics and semiconductors hold over 23% share in 2025, supported by miniaturization, photolithography, and high-precision beam shaping requirements.

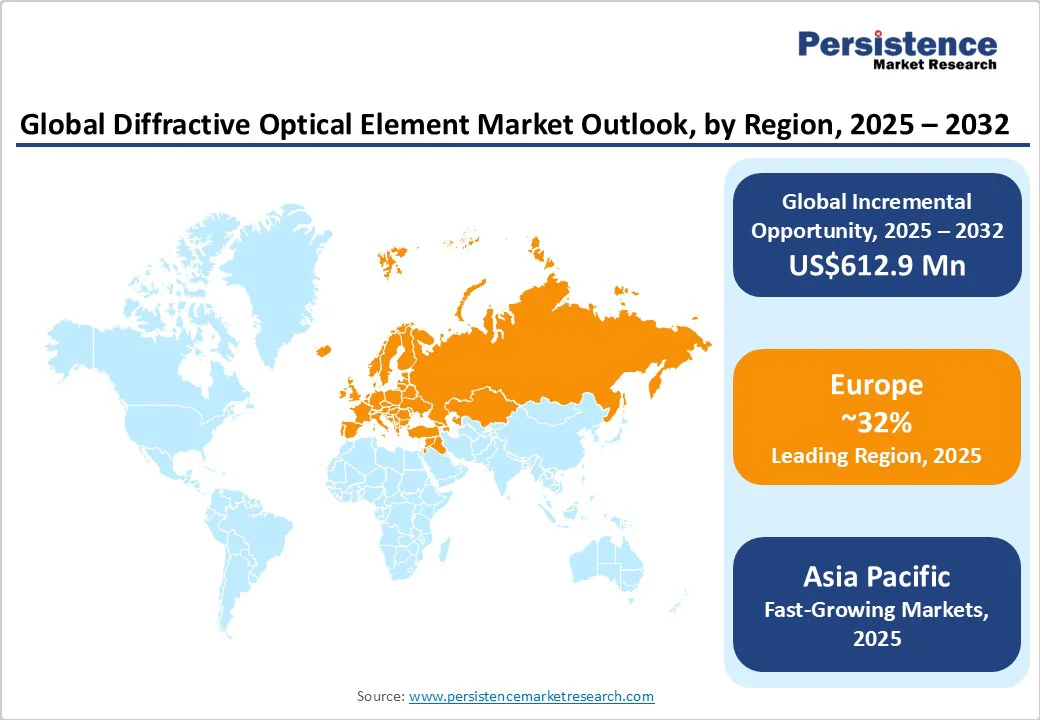

- Leading Region: Europe accounts for more than 32% share, driven by medical devices, automotive, semiconductor sectors, and renewable energy initiatives. Asia-Pacific is the fastest-growing region, supported by high-volume electronics manufacturing, 5G expansion (~4.5 million base stations by May 2025), and cost-effective production.

- Key Opportunity: Adoption in LiDAR and ADAS improves resolution, range, and safety in electric and autonomous vehicles, while AR/VR devices benefit from compact, high-precision light shaping for immersive displays and gesture/facial recognition. Government funding, e.g., $25.7 million by NHTSA (2024) for vehicle automation research, further accelerates growth.

| Key Insights | Details |

|---|---|

|

Diffractive Optical Element Market Size (2025E) |

US$817.3 Mn |

|

Market Value Forecast (2032F) |

US$1,430.2 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

8.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.9% |

Market Dynamics

Driver - Miniaturization of Optical Systems

Compact optical systems in consumer electronics, medical devices, and aerospace are increasingly adopting diffractive optical elements to achieve precise light manipulation in smaller, lightweight designs. By replacing bulky lens assemblies, DOEs help reduce size, weight, and power consumption while maintaining high performance in applications such as LiDAR, laser projectors, and advanced imaging systems. Ongoing nanofabrication advancements allow for finer DOE structures, improving optical efficiency and expanding their use across industries. For instance, the U.S. National Nanotechnology Initiative (NNI) allocated $2.16 billion in 2024 to support innovations in compact optical technologies, highlighting DOEs as a critical enabler of next-generation miniaturized devices.

Growth in Telecommunications and Data Centers

High-speed fiber-optic networks increasingly depend on DOEs for precise beam shaping and splitting to enhance signal quality and minimize data loss. The rapid adoption of 5G, cloud computing, and edge computing drives demand for compact, high-precision optical components that support higher bandwidth and lower latency. Data centers with dense interconnects rely on DOE-based solutions to optimize space, energy efficiency, and performance, while LiDAR integration in network monitoring further expands applications. According to Ericsson, global mobile data traffic is set to exceed 280 EB/month by 2030 (430 EB/month including FWA), with 5G rising from 35% in 2024 to 80% by 2030, directly fueling DOE adoption in telecommunications.

Restraint - Manufacturing Complexity and Technical Integration Challenges

Diffractive optical element manufacturing involves advanced nanolithography and precision molding, requiring significant capital investment, specialized cleanroom facilities, and skilled technicians. High initial tooling and metrology costs restrict adoption in low-volume or price-sensitive applications, keeping production concentrated among established players. The wavelength-specific design of DOEs demands specialized optical expertise and requires system redesigns for integration, while temperature sensitivity and environmental stability concerns further limit application scope, slowing adoption and extending development timelines.

Opportunity - Advanced Automotive Sensing Technologies

Diffractive optical elements (DOEs) are becoming essential in LiDAR systems and advanced driver-assistance systems (ADAS) for autonomous and electric vehicles. By enabling compact, high-precision, and cost-effective optical sensors, DOEs improve resolution, range, and efficiency, enhancing vehicle safety and intelligence. The growing adoption of electric and autonomous vehicles is increasing the optical component content per vehicle, prompting automakers to invest in miniaturized DOE solutions for aesthetic integration and mass-market deployment. These technologies are key to meeting stringent automotive standards while supporting next-generation vehicle sensing systems. For instance, the National Highway Traffic Safety Administration (NHTSA) allocated an additional $25.7 million in 2024 for research, rulemaking, and enforcement activities to translate automation technology into safety improvements.

AR/VR Technology Integration

Consumer electronics manufacturers are increasingly adopting diffractive optical elements (DOEs) in AR/VR devices for facial recognition, gesture control, and immersive display applications. For instance, Apple’s TrueDepth camera uses an Active DOE to project over 30,000 infrared dots for precise 3D face mapping. DOEs enable ultra-compact, high-performance light shaping, essential for realistic depth cues in gaming, industrial training, and remote collaboration. Their miniaturization capabilities support wearable devices, accelerate product development cycles, and benefit from high-volume manufacturing economies. As AR/VR adoption grows, DOEs are poised to see significant demand as a critical enabling technology in next-generation consumer electronics.

Category-wise Analysis

By Product Type, Beam Splitters Enabling Precise Light Management and Multifunctional Optical Systems

Beam splitters are expected to account for more than 52% share in 2025 as they are essential for dividing and directing light with high precision. They support accurate signal routing, power balancing, and wavelength separation, which are fundamental for advanced optical systems. The rising need for compact, efficient, and multifunctional components enhances their adoption. Their versatility in handling multiple light paths makes them the most widely used solution among diffractive elements.

Beam shapers are expected to grow at the highest rate due to the rising demand for precise beam profiling in various applications. Industries increasingly require uniform intensity distribution and high accuracy for microfabrication, lithography, and laser surgery. The shift toward miniaturization of electronic components and higher efficiency in laser systems further drives adoption. The growing use of high-power lasers in industrial and biomedical fields strengthens the need for advanced beam shaping solutions.

By Application, Biomedical Devices Drive Growth Through Precision Optics in Imaging, Diagnostics & Minimally Invasive Surgery

Biomedical devices are expected to account for more than 27% share in 2025 due to rising demand for precision optics in imaging, diagnostics, and minimally invasive surgical tools. The growing need for high-resolution, compact, and cost-effective optical solutions in endoscopy, OCT, and laser-based treatments is driving adoption. The increasing prevalence of chronic diseases and the expanding use of advanced biomedical imaging systems further fuel demand. DOE’s ability to improve accuracy and efficiency in medical instruments makes them indispensable in healthcare applications.

Laser material processing is expected to grow rapidly due to rising demand for precise, high-speed manufacturing in industries like automotive, electronics, and aerospace. DOEs enhance laser performance by enabling beam shaping and splitting, improving cutting, welding, and surface treatment efficiency. The shift toward automation and smart factories further accelerates the adoption of DOE-based laser solutions in modern manufacturing.

By Industry, Electronics and Semiconductors Driving Precision and Efficiency

Electronics and semiconductors are expected to account for over 23% share in 2025 due to their critical role in miniaturization, high-precision beam shaping, and advanced photolithography processes. With growing demand for smaller, more powerful chips, DOEs enable efficient light manipulation in semiconductor fabrication and inspection systems. The surge in consumer electronics, 5G devices, and high-performance computing further drives the need for DOE-enabled optical solutions to enhance manufacturing accuracy, throughput, and cost-efficiency.

Telecommunication is expected to grow at the highest rate due to the surging demand for high-speed data transmission and 5G/6G network deployments. Increasing bandwidth requirements, network densification, and the need for compact, efficient optical components drive the adoption of DOEs in fiber-optic systems. Rising internet traffic and cloud-based services further accelerate this growth. For instance, according to the Department of Telecommunications, as of June 30, 2025, over 4.86 lakh 5G Base Transceiver Stations (BTSs) have been installed in India, covering 99.8% of districts.

Regional Insights

North America Diffractive Optical Element Market Trends

North America, led by the U.S., is a major contributor to the DOE market, supported by strong R&D in photonics, a robust innovation ecosystem, and supportive regulatory frameworks. High defense spending drives demand for specialized optical components in military applications such as infrared countermeasures and advanced targeting systems, with the DoD allocating $74.6 billion in 2024 for modernization. Investments in 5G networks, quantum technologies, and advanced healthcare systems further boost adoption, exemplified by the FCC’s $9 billion 5G expansion initiative for rural areas. The region’s established photonics companies and research institutions accelerate innovation, commercialization, and sustain market growth.

Asia Pacific Diffractive Optical Element Market Trends

Asia-Pacific is the fastest-growing market, driven by rapid industrialization and technological adoption in China, Japan, India, and ASEAN countries. China’s booming electronics manufacturing, extensive 5G network rollout with ~4.5 million base stations (35% of total base stations till May 2025), and advanced telecom infrastructure drive high-volume DOE demand. Japan leads in precision optics and advanced displays, while India’s expanding telecom and medical device sectors offer significant opportunities. ASEAN contributes through electronics assembly and rising industrial automation. Government incentives, technology investments, and cost-effective manufacturing further support sustained regional market growth.

Europe Diffractive Optical Element Market Trends

Europe is expected to account for a share of more than 32% in 2025, driven by advanced manufacturing, photonics, and precision engineering. Strong growth in medical devices, including laser diagnostics and surgical systems, and Germany’s automotive and semiconductor sectors, fuels DOE adoption. EU regulations, energy efficiency initiatives, and policies supporting green technologies and digitization enhance cross-border deployment. Rising investments in renewable energy, solar concentration, LiDAR systems, and upgraded fiber-optic networks further boost demand across Europe. In 2024, the EU installed nearly 66 GW of new solar energy capacity, setting a record and creating opportunities for DOE applications in energy-efficient technologies.

Competitive Landscape

The diffractive optical element market is fragmented, with a mix of specialized startups and established photonics players competing globally. They are focusing on continuous R&D to deliver high-efficiency, application-specific solutions for sectors. Companies are pursuing mergers and acquisitions to scale production and expand geographic reach while maintaining cost competitiveness through process optimization and nanofabrication expertise. Zeiss maintains a significant market presence through precision optics leadership and a diversified application portfolio, while Jenoptik leverages automotive and semiconductor industry relationships for sustained growth.

Key Industry Developments:

- In January 2025, Coherent Corp. launched its Ultrabroadband UV-VIS and VIS-NIR diffraction gratings, advancing optical system performance for life science, medical, and industrial applications. These high-precision gratings enhance spectral resolution, simplify system design, and deliver broad wavelength compatibility for applications like flow cytometry, Raman spectroscopy, OCT, and laser diode stabilization.

- In January 2025, Radiant Opto-Electronics Corporation completed its acquisition of NIL Technology. The deal combines NILT’s advanced optics expertise with ROE’s large-scale manufacturing capabilities to accelerate high-volume production of next-generation optical solutions.

Companies Covered in Diffractive Optical Element Market

- Broadcom Inc.

- Laserglow Technologies

- Jenoptik AG

- Zeiss

- HOLO/OR LTD.

- LightTrans GmbH

- HOLOEYE Photonics

- Laser Optical Engineering Ltd.

- SILIOS Technologies

- Sintec Optronics

- Edmund Optics

- AGC Group

- NIL Technology

- VIAVI Solutions

- Coherent, Inc.

- Others

Frequently Asked Questions

The global diffractive optical element market is projected to be valued at US$817.3 Mn in 2025.

The growing demand for compact, high-precision optical components, driven by miniaturization and the need for enhanced performance, is a key driver of the market.

The diffractive optical element market is poised to witness a CAGR of 8.3% from 2025 to 2032.

The growing adoption of LiDAR and advanced sensing in autonomous vehicles, along with the expansion of high-speed optical networks, creates strong growth opportunities.

Broadcom Inc., Laserglow Technologies, Jenoptik AG, Zeiss, HOLO/OR LTD., LightTrans GmbH, HOLOEYE Photonics, and Laser Optical Engineering Ltd. are among the leading key players.