- Inks, Coatings, Adhesives & Sealants (ICAS)

- Europe Optical Coating Market

Europe Optical Coating Market Size, Share, and Growth Forecast 2026 - 2033

Europe Optical Coating Market by Product Type (Filter, Reflective, Anti-reflective, Transparent Conductive, Others), by Technology (Ion Beam Sputtering, Evaporation Deposition, Vacuum Deposition, Advanced Plasma Reactive Sputtering), End-user (Automotive, Electronics, Solar, Medical, Others), and Regional Analysis for 2026 - 2033

Europe Optical Coating Market Size and Trend Analysis

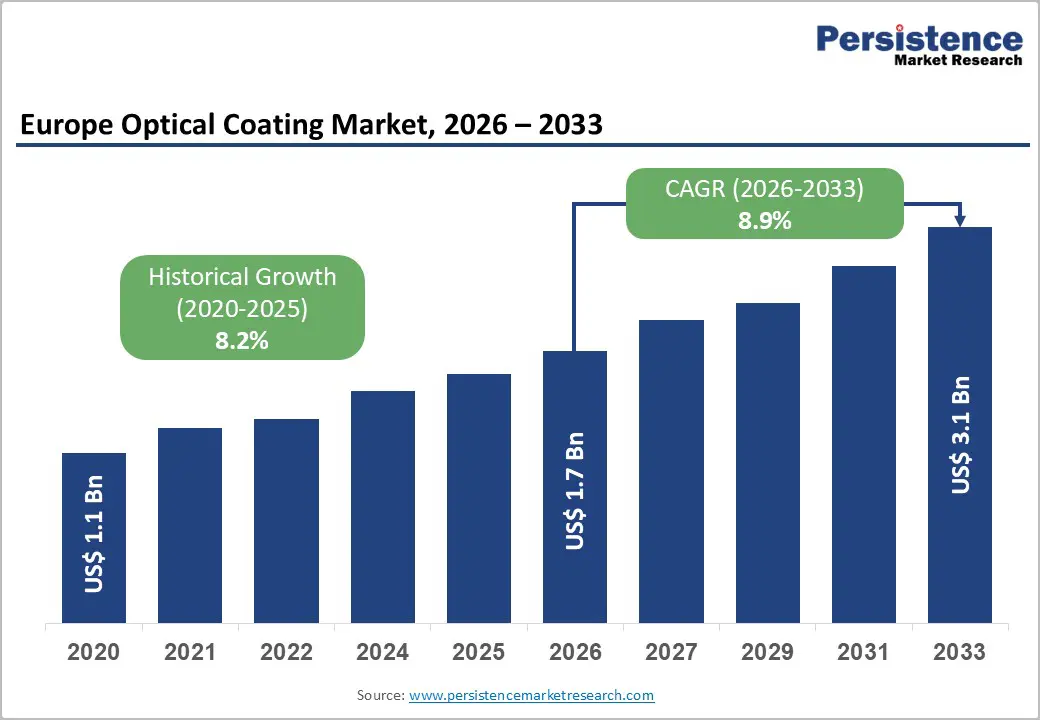

Europe Optical Coating market size is supposed to be valued at US$ 1.7 Billion in 2026 and is projected to reach US$ 3.1 Billion by 2033, growing at a CAGR of 8.9% between 2026 and 2033.

The European optical coating market's robust and accelerating growth is driven by the region's world-leading precision optics manufacturing heritage, escalating adoption of advanced driver assistance systems (ADAS) in the European automotive industry, the rapid deployment of solar energy infrastructure under the European Green Deal's renewable energy targets, and growing demand for high-performance optical components in medical imaging, semiconductor lithography, and consumer electronics applications.

Key Market Highlights

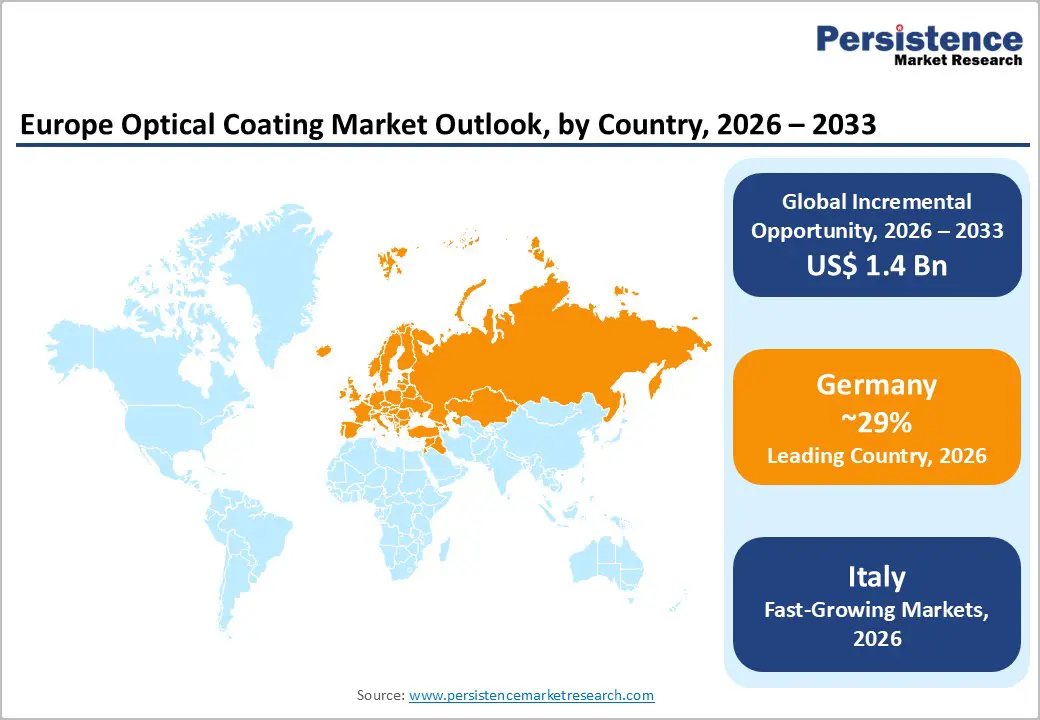

- Leading Country: Germany leads the European Optical Coating market, anchored by Zeiss Group, LEYBOLD GmbH, and OptoTech's headquarters concentration, Fraunhofer IOF EUV coating research, Spectaris-documented €30 billion German photonics industry revenues, and the ACEA-confirmed European automotive ADAS mandate under EU General Safety Regulation (EU) 2019/2144 generating structurally growing precision automotive optical filter and AR coating procurement.

- Fastest Growing Country: Italy is a high-growth European market, driven by Anfao-represented world-leading ophthalmic lens manufacturing in Veneto, GSE-documented Italian solar expansion toward 80 GW by 2030 under PNIEC, and Next Generation EU capital investment supporting optical coating equipment modernization upgrades across Italian ophthalmic and solar module manufacturing facilities.

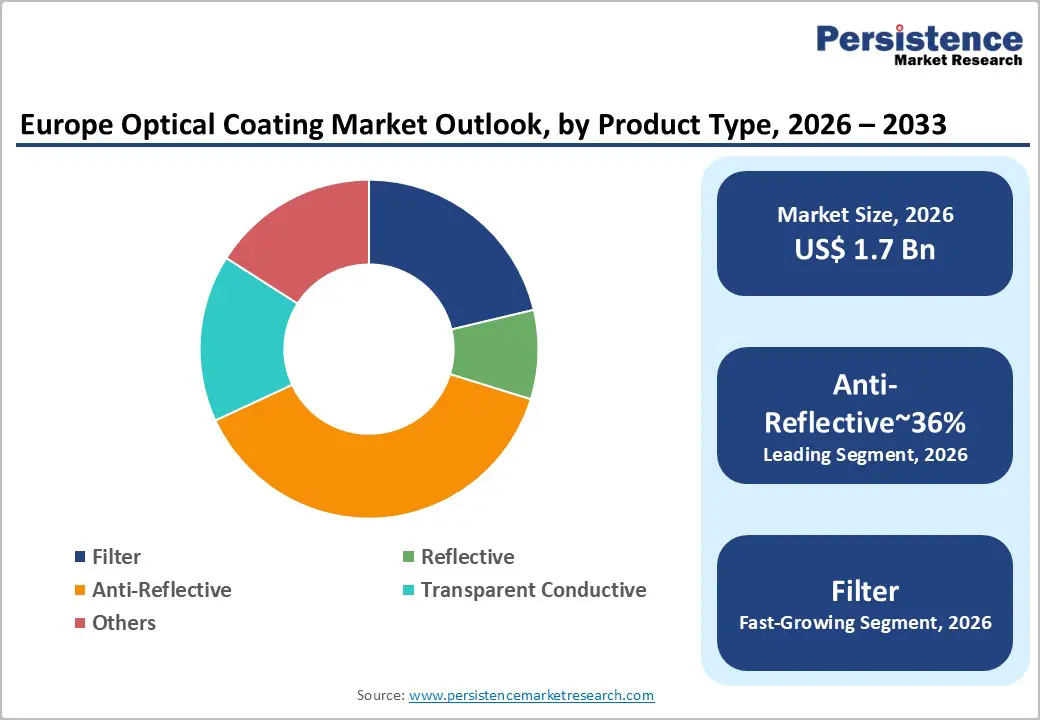

- Dominant Product Type: Anti-Reflective Coatings dominate, with approximately 36% revenue share, anchored by ophthalmic lens AR coating volumes, solar PV module glass coating demand under REPowerEU's 510 GW solar target, and ADAS sensor lens anti-reflective coating procurement driven by Euro NCAP safety ratings and EU General Safety Regulation mandates generating above-average forecast period growth.

- Fastest Growing End-user: Solar is the fastest-growing end-user segment, propelled by SolarPower Europe's documented 65 GW+ annual European PV installations, REPowerEU's tripling of European solar capacity targets to 510 GW by 2030, and Evatec AG's CLUSTERLINE® APRS platform addressing next-generation perovskite-silicon tandem solar cell TCO coating requirements achieving 30%+ power conversion efficiency benchmarks.

- Opportunity: EUV semiconductor lithography and AI-driven precision optics represent the key European optical coating opportunity, with the €43 billion EU CHIPS Act stimulating domestic semiconductor investment, ASML's High-NA EUV scanner scale-up requiring precision Mo/Si mirror coatings, and Zeiss Group's Fraunhofer IOF R&D partnership positioning Europe's leading optical coating technology base to capture ultra-high-value next-generation semiconductor optics coating demand through the forecast period.

| Key Insights | Details |

|---|---|

|

Europe Optical Coating Market Size (2026E) |

US$ 1.7 Billion |

|

Market Value Forecast (2033F) |

US$ 3.1 Billion |

|

Projected Growth CAGR (2026–2033) |

8.9% |

|

Historical Market Growth (2020–2025) |

8.2% |

Market Dynamics

Drivers - European Automotive ADAS and LiDAR Expansion Driving Precision Optical Filter and Anti-Reflective Coating Demand

The European automotive industry's mandatory transition toward advanced safety technology, driven by the European New Car Assessment Programme (Euro NCAP)'s progressively tightening vehicle safety rating criteria, the EU General Safety Regulation (EU) 2019/2144 mandating ADAS features including automatic emergency braking, lane-keeping assist, and intelligent speed assistance across all new vehicle categories from July 2024, is generating structurally growing demand for high-performance optical filter coatings, anti-reflective coatings, and precision lens coatings essential to camera, LiDAR, and radar sensor optical systems. Each ADAS-equipped vehicle incorporates multiple cameras and sensors, each requiring multi-layer anti-reflective coatings, bandpass filter coatings, and protective hard coatings applied with nanometer-scale thickness precision to achieve the optical transmission and wavelength selectivity required for reliable autonomous driving perception across variable ambient lighting and weather conditions.

The ACEA's production data confirms that European automotive OEM platforms, from Volkswagen Group, BMW, Mercedes-Benz, and Stellantis, are standardizing full ADAS sensor suite integration across vehicle ranges well above EU mandate minimums, generating above-mandate optical coating procurement growth from the European automotive supply chain. Zeiss Group's automotive optics division and Buhler Holding AG's precision coating deposition systems directly serve the automotive optical coating supply chain at the lens grinding, coating, and sensor assembly integration levels.

Solar Energy Capacity Expansion Under European Green Deal Creating Large-Scale Anti-Reflective and TCO Coating Demand

The European Commission's landmark REPowerEU Plan, adopted in May 2022 targeting 510 GW of installed solar photovoltaic capacity by 2030, nearly triple Europe's 2022 installed base, is creating a large-scale and multi-year structural demand wave for solar-grade anti-reflective (AR) coatings and Transparent Conductive Oxide (TCO) coatings that are essential performance-enhancing components in photovoltaic module and thin-film solar cell manufacturing. Anti-reflective coatings applied to PV module cover glass and solar cell active surfaces reduce reflection losses and increase light transmission into the active photovoltaic layer, with high-performance AR coatings documented in peer-reviewed photovoltaics literature including the Progress in Photovoltaics journal to improve module power output by 2–4% relative to uncoated reference modules, translating directly into measurable additional energy yield and improved levelized cost of electricity (LCOE) for solar farm operators.

The European Photovoltaic Industry Association (SPE PVTECH / SolarPower Europe)'s Solar Outlook Report 2024 projected that Europe added over 65 GW of solar PV capacity in 2023 alone, the highest single-year installation figure in European history, confirming the structural scale of the solar coating demand wave being generated by the European Green Deal implementation across Germany, Italy, Spain, Netherlands, and Poland. Oerlikon Balzers Coating AG and Evatec AG, both headquartered in Switzerland and serving European solar and industrial coating markets, are expanding their thin-film deposition equipment and process capabilities to serve this structurally growing renewable energy coating demand category.

Restraints - High Capital Investment Requirements for Ion Beam Sputtering and Advanced Deposition Equipment Creating Adoption Barriers

The most technically capable optical coating deposition technologies, particularly Ion Beam Sputtering (IBS) and Advanced Plasma Reactive Sputtering (APRS), require capital investment in vacuum deposition systems that typically cost between €500,000 and €5,000,000 per chamber configuration depending on substrate size capacity, layer complexity, and process control sophistication, creating substantial capital barriers to entry that limit adoption of premium coating technology to large-scale optical manufacturers and well-capitalized specialty coating service providers.

European precision optics manufacturers, predominantly concentrated in Germany, Austria, and Switzerland, face the challenge of justifying large IBS system capital expenditures for product lines where annual coating revenue volumes may not generate acceptable returns on investment at current technology cost levels, constraining the rate at which premium coating technology diffuses into the broader European optical manufacturing supply chain.

Skilled Workforce Shortage in Precision Thin-Film Deposition Engineering Constraining European Production Capacity Expansion

The European optical coating industry faces a structural constraint in the availability of highly trained precision thin-film deposition engineers, combining expertise in vacuum physics, optical design, materials science, and coating process control, required to operate, optimize, and innovate advanced optical coating production systems.

Germany's Federal Institute for Vocational Education and Training (BIBB) has documented persistent skilled labor shortages in precision optics and photonics manufacturing across Bavaria, Baden-Württemberg, and Thuringia, the primary German optical industry clusters, with the European Photonics Industry Consortium (EPIC) estimating that European photonics companies face a growing talent gap of thousands of technically qualified workers that constrains the region's ability to expand production capacity at a pace commensurate with demand growth in solar, automotive, and medical optical coating applications.

Opportunities - Semiconductor Lithography and EUV Optics Creating Ultra-High-Value Precision Coating Technology Demand

The global semiconductor industry's migration to Extreme Ultraviolet (EUV) and High-NA EUV lithography platforms, led by ASML's EUV scanner technology which is essential for sub-5nm and below semiconductor node manufacturing, is creating a new and extraordinarily high-value optical coating application category that demands the most technologically sophisticated coating processes available, including precision multilayer Mo/Si (Molybdenum-Silicon) reflective coatings applied with sub-nanometer layer thickness tolerances to EUV lithography mirror substrates. ASML (headquartered in Eindhoven, Netherlands), the world's sole supplier of EUV lithography systems and the critical enabler of advanced semiconductor manufacturing at TSMC, Samsung, and Intel, works with specialized European optical coating partners to develop and produce EUV mirror coating systems that operate at 13.5nm wavelength reflectivity requirements far beyond conventional visible or near-IR optical coating capabilities.

The European Commission's €43 billion CHIPS Act for Europe, adopted in 2023 to stimulate European semiconductor manufacturing investment, is expected to drive domestic European fab investment that increases EUV optical component demand over the forecast period, creating a premium-priced specialty coating opportunity for Zeiss Group's semiconductor optics division and specialty coating research institutions including Fraunhofer Institute for Applied Optics and Fine Mechanics (IOF) in Jena, Germany. LEYBOLD GmbH's advanced vacuum deposition systems serve the ultra-high vacuum requirements of EUV optical coating applications.

Medical Imaging and Ophthalmology Optical Coating Demand Accelerated by European Healthcare Digitalization

The European healthcare sector's ongoing digital transformation, encompassing the widespread adoption of minimally invasive endoscopic surgery, digital pathology, optical coherence tomography (OCT) diagnostic imaging, robotic surgical systems, and advanced ophthalmic wavefront correction, is generating structurally growing and premium-priced demand for certified medical-grade optical coatings in surgical optics, ophthalmic lens systems, endoscope objective lenses, and diagnostic imaging optical systems that must comply with the EU Medical Device Regulation (MDR) (EU) 2017/745 rigorous performance and biocompatibility certification requirements. The European Union's European Health Data Space (EHDS) regulatory initiative, adopted by the European Parliament in 2024, is accelerating healthcare digital infrastructure investment across EU member states that stimulates procurement of advanced medical imaging equipment incorporating precision optically coated components.

Zeiss Group's medical technology division, which produces surgical microscope systems, ophthalmic diagnostic equipment, and ophthalmic lens coating systems, is the European market leader in medical optical coating applications, with its precision anti-reflective and hydrophobic lens coatings for ophthalmic applications manufactured at its Oberkochen and Jena facilities serving a globally distributed surgical and diagnostic customer base. Artemis Optical Ltd and OptoTech Optikmaschinen GmbH serve European ophthalmic and medical optical component coating markets with specialized precision coating services and equipment.

Category-wise Analysis

By Product Type Insights

Anti-Reflective (AR) Coatings lead the European Optical Coating market by product type, accounting for approximately 36% of total product type segment revenue in 2026, a commercially dominant position anchored in AR coatings' foundational application breadth across ophthalmic lenses, camera lens systems, solar PV modules, automotive sensor optics, display panels, and medical imaging optics where minimizing surface reflection losses is the primary optical performance requirement in the broadest range of end-use applications.

AR coatings, deposited as quarter-wave optical thickness single layers or broadband multi-layer stack designs using MgF2, SiO2, Al2O3, and TiO3 dielectric materials, are the highest-volume optical coating category by application count, with the global ophthalmic lens market alone applying AR coatings to hundreds of millions of prescription lens pairs annually. Zeiss Group's ZEISS DuraVision® anti-reflective ophthalmic lens coating range and Oerlikon Balzers' broad AR coating service portfolio exemplify the commercial breadth of this leading segment. Filter coatings, at approximately 25% of product type revenue, are the fastest-growing segment, driven by ADAS bandpass filter requirements and semiconductor lithography applications.

By Technology Insights

Vacuum Deposition leads the European Optical Coating market by technology, commanding approximately 42% of total technology segment revenue in 2026, reflecting vacuum deposition's established position as the broadest-application, most commercially mature thin-film coating deposition technology platform, encompassing both thermal evaporation and electron beam evaporation processes that have been industrially deployed at European optical manufacturing scale for over five decades and remain the dominant coating technology for high-volume ophthalmic lens, spectacle lens, and display optical coating production.

Vacuum deposition systems, supplied by European equipment leaders including Buhler Holding AG (through its Leybold Optics division) and Satis Vacuum Technologie SA, offer well-characterized process repeatability, established materials databases, and relatively lower equipment capital costs compared to IBS systems that make them the default coating technology for high-volume ophthalmic and consumer optics production. Ion Beam Sputtering holds approximately 28% of technology revenue, valued for its exceptional layer density, low scatter loss, and thermal stability in precision laser, astronomical, and EUV optical applications, and is the fastest-growing technology segment driven by semiconductor lithography and defense optical coating demand.

By End-user Insights

The Electronics end-use segment leads the European Optical Coating market, accounting for approximately 34% of total end-use segment revenue in 2026, reflecting the broad and technically demanding optical coating requirements of the European electronics manufacturing ecosystem spanning display panel optical coatings, consumer optical device lens coatings, semiconductor photomask coatings, optical fiber end-face coatings, and laser optical component coatings across both consumer and industrial electronics applications. The European photonics industry, documented by Photonics21 (the European photonics association) as generating over €100 billion in European photonics company revenues, represents a major and technically sophisticated domestic demand base for precision optical coatings across a diverse range of electronic and photonic device applications.

The Medical end-use segment holds the second-largest share at approximately 22% of revenue, driven by EU MDR compliance requirements, Zeiss Group's surgical optics programs, and the European ophthalmic lens industry's large-volume AR coating procurement. Solar represents the fastest-growing end-use segment, propelled by SolarPower Europe's documented 65 GW+ annual European PV installation volumes and the REPowerEU Plan's 510 GW solar target by 2030.

Regional Insights

Germany Optical Coating Market Trends

Germany leads the European Optical Coating market by a substantial margin, anchored by its unparalleled concentration of world-class precision optics manufacturers, photonics research institutions, and optical coating equipment companies that collectively constitute one of the world's most technically advanced optical manufacturing ecosystems. The German Optics and Photonics industry association (Spectaris) and VDMA Photonics document that Germany's photonics industry employs approximately 140,000 people and generates over €30 billion in annual revenues, with precision optics and coating technologies representing core competency areas sustaining Germany's global technical leadership. Zeiss Group (headquartered in Oberkochen and Jena), LEYBOLD GmbH (headquartered in Cologne), and OptoTech Optikmaschinen GmbH (headquartered in Wettenberg) are all headquartered in Germany, reinforcing the country's position as Europe's dominant optical coating technology and manufacturing geography.

Germany's automotive industry, with Volkswagen Group, BMW, and Mercedes-Benz collectively investing billions annually in ADAS, LiDAR, and camera sensor optical systems, sustains one of Europe's largest automotive-grade optical coating procurement volumes from domestic coating service providers and optical component manufacturers. The Fraunhofer Institute for Applied Optics and Fine Mechanics (IOF) in Jena, part of the world's largest applied research organization Fraunhofer-Gesellschaft, conducts cutting-edge research in EUV mirror coatings, broadband anti-reflective coatings, and precision thin-film deposition processes that directly feed technology transfer into German industrial optical coating production programs, maintaining Germany's competitive advantage in next-generation coating technology development.

Italy Optical Coating Market Trends

Italy is a significant market for optical coatings, anchored by its world-renowned ophthalmic lens manufacturing industry centered in the Belluno/Cadore district of Veneto, home to Luxottica (now part of EssilorLuxottica) and a dense cluster of lens manufacturing companies that collectively make Italy the world's largest ophthalmic frame and lens manufacturing geography. The Italian optics industry, represented by Anfao (Associazione Nazionale Fabbricanti Articoli Ottici), encompasses hundreds of companies across ophthalmic, industrial, and precision optical manufacturing segments, generating substantial domestic procurement demand for anti-reflective, hydrophobic, and oleophobic lens coatings applied to ophthalmic prescription and sunglass lens products distributed globally under Italian optical brands. Buhler Holding AG's and Satis Vacuum Technologie SA's vacuum deposition systems serve the Italian ophthalmic lens coating market.

Italy's growing renewable energy sector, with Gestore dei Servizi Energetici (GSE) documenting Italy's accelerating solar PV installation program targeting 80 GW of national solar capacity by 2030 under the Italian National Energy and Climate Plan (PNIEC), is generating expanding procurement demand for solar-grade anti-reflective coatings from Italian solar module manufacturers and installation program material supply chains. The EU Cohesion Funds and Next Generation EU (NGEU) Recovery and Resilience Facility investments in Italian industrial modernization are supporting capital investments in advanced coating equipment upgrades across Italian optical manufacturing facilities, positioning the Italian optical coating sector for accelerating technical capability improvements aligned with the European market's premium performance requirements through the forecast period.

France Optical Coating Trends

France maintains a technically sophisticated and innovation-driven optical coating market, anchored by its world-leading aerospace and defense optics sector, nationally strategic nuclear energy program requiring precision optical components, and advanced scientific research optical infrastructure including the Commissariat à l'Énergie Atomique et aux Énergies Alternatives (CEA) and the CNRS Institute of Optics. France's defense and space agency CNES (Centre National d'Études Spatiales) and Thales Alenia Space are significant institutional consumers of precision IBS and EUV reflective optical coatings for satellite telescope mirrors, space-borne imaging systems, and directed energy weapon optical components, representing a high-value, technically demanding application category sustaining French demand for the most sophisticated available optical coating technologies. Cutting Edge Coatings GmbH and specialty French optical coating houses serve these premium government and defense optical coating procurement programs.

France's medical device and pharmaceutical optical analysis sectors, anchored by companies including Essilor International (part of EssilorLuxottica, headquartered in Charenton-le-Pont) for ophthalmic lens coatings and Thales Group for medical imaging systems, sustain consistent premium demand for certified medical-grade and ophthalmic-grade optical coatings compliant with EU MDR and CE marking requirements. Essilor's Crizal® anti-reflective lens coating range, one of the world's best-selling ophthalmic optical coating brands, is a direct embodiment of France's technical leadership in ophthalmic lens coating chemistry and deposition process engineering, with EssilorLuxottica's French technical centers continuously advancing next-generation low-reflection, anti-smudge, and blue-light filtering ophthalmic coating platforms that set commercial performance benchmarks for the global ophthalmic coating industry.

Competitive Landscape

Europe optical coating market is moderately consolidated, with a tier-1 group of precision optics, vacuum equipment, and specialty coating companies, Zeiss Group, Buhler Holding AG, Oerlikon Balzers Coating AG, and Evatec AG, commanding leading positions through decades of application expertise, world-recognized brand equity, and proprietary deposition technology intellectual property. LEYBOLD GmbH and Ionbond AG compete through high-vacuum equipment platform capabilities and surface engineering service networks.

Key competitive differentiators include ISO 9001 and ISO 13485 medical quality certifications, semiconductor-grade cleanroom coating facilities, proprietary multi-layer design software, and application engineering teams embedded within automotive, medical, and solar OEM customer programs. Emerging trends include AI-assisted coating process optimization, integrated digital twin coating simulation platforms, and sustainability-certified low-energy IBS deposition systems targeting the European Green Deal's industrial carbon reduction agenda.

Key Developments:

- In February 2025, Zeiss Group announced an expansion of its EUV mirror coating technology capabilities at its Oberkochen optics facility, investing in next-generation Mo/Si multilayer deposition capacity to support ASML's High-NA EUV lithography scanner program as it scales to serve advanced semiconductor customers targeting 2nm and below node chip manufacturing requirements globally.

- In September 2024, Evatec AG launched its CLUSTERLINE® 300 II advanced sputtering platform featuring enhanced Advanced Plasma Reactive Sputtering (APRS) capabilities, targeting the growing demand from European solar cell manufacturers for ultra-uniform transparent conductive oxide (TCO) coatings required in next-generation perovskite-silicon tandem solar cell structures achieving over 30% power conversion efficiency.

- In April 2024, Oerlikon Balzers Coating AG expanded its European optical coating service network by opening a new state-of-the-art optical hard coating and AR coating production center in Germany, targeting the rapidly growing automotive camera lens and LiDAR sensor optics market generated by European ADAS mandate implementations under EU General Safety Regulation (EU) 2019/2144.

Companies Covered in Europe Optical Coating Market

- Cutting Edge Coatings GmbH

- Artemis Optical Ltd.

- OptoTech Optikmaschinen GmbH

- Buhler Holding AG

- Evatec AG

- Zeiss Group

- LEYBOLD GmbH

- Satis Vacuum Technologie SA

- Oerlikon Balzers Coating AG

- Ionbond AG

- EssilorLuxottica

- Fraunhofer Institute for Applied Optics and Fine Mechanics (IOF)

- Thales Alenia Space

Frequently Asked Questions

Europe Optical Coating market is estimated to be valued at US$ 1.7 Billion in 2026 and is projected to reach US$ 3.1 Billion by 2033, registering a forecast CAGR of 8.9% from 2026 to 2033. The market recorded a historical CAGR of 8.2% between 2020 and 2025, driven by automotive ADAS expansion, solar energy deployment under the REPowerEU Plan, and growing medical device optical coating demand under EU MDR (EU) 2017/745 compliance requirements.

The primary drivers are EU General Safety Regulation (EU) 2019/2144 mandating ADAS systems across all new European vehicles from July 2024, generating precision optical filter and AR coating demand for automotive camera and LiDAR sensors, and the REPowerEU Plan's target of 510 GW of European solar PV capacity by 2030, with SolarPower Europe documenting 65 GW+ annual European solar installations requiring solar-grade AR and TCO coatings at large commercial scale.

Anti-Reflective (AR) Coatings lead the Product Type segment with approximately 36% revenue share in 2026, anchored by ophthalmic lens volume production, solar module glass coating demand from REPowerEU PV deployment, and automotive sensor optical coating requirements under Euro NCAP safety ratings. Zeiss Group's DuraVision® AR ophthalmic range, Oerlikon Balzers' BALORA® service platform, and EssilorLuxottica's Crizal® brand represent the leading commercial AR coating platforms in the European market.

Germany leads the European Optical Coating market, anchored by Zeiss Group, LEYBOLD GmbH, and OptoTech's headquarters concentration, Spectaris-documented €30 billion German photonics industry, Fraunhofer IOF EUV coating research excellence, and the country's world-leading automotive ADAS production programs from Volkswagen Group, BMW, and Mercedes-Benz generating Europe's highest per-country precision optical coating procurement volumes across automotive, medical, and semiconductor application segments.

The most significant opportunity is EUV semiconductor lithography and EU CHIPS Act-driven domestic fab investment, with the €43 billion EU Chips Act stimulating European semiconductor manufacturing and ASML's High-NA EUV platform scaling requiring ultra-precision Mo/Si multilayer reflective coatings manufactured to sub-nanometer tolerances. Zeiss Group in partnership with Fraunhofer IOF is positioned to capture the premium ultra-high-value EUV optical coating demand this semiconductor expansion wave will generate through the forecast period.