- Specialty & Fine Chemicals

- Methyl Ester Sulfonate Market

Methyl Ester Sulfonate Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Methyl Ester Sulfonate Market by Form (Liquid, Powder, Flakes), Application (Detergents, Personal Care Products, Industrial, Other), and Regional Analysis for 2026 - 2033

Methyl Ester Sulfonate Market Size and Trend Analysis

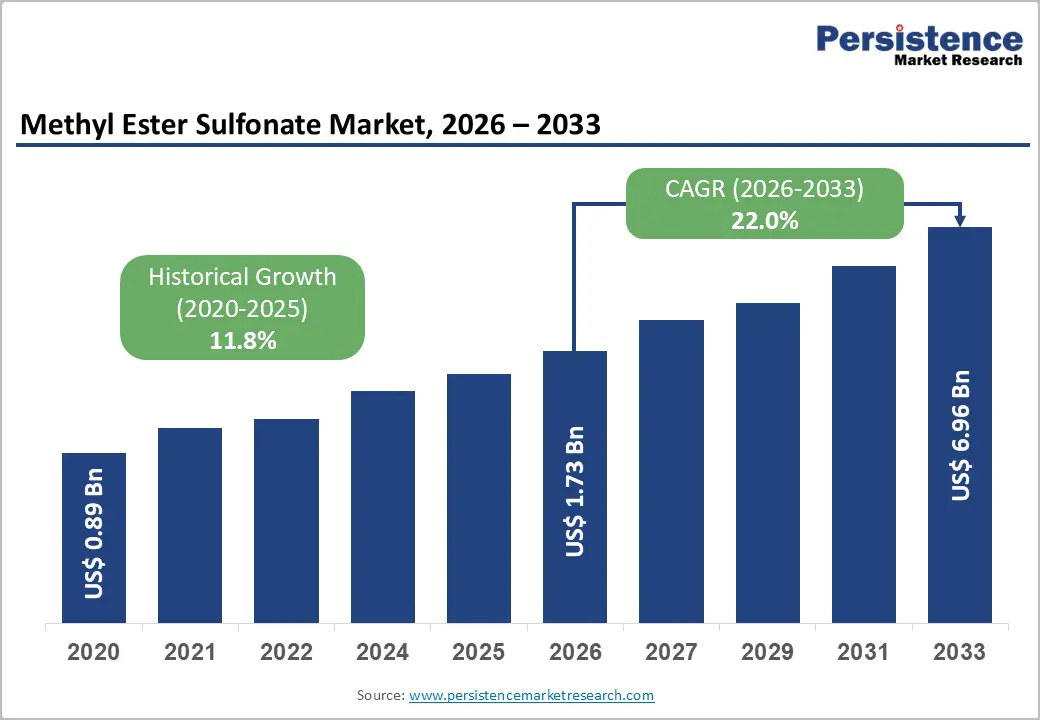

The global methyl ester sulfonate market size is likely to be valued at US$ 1.7 billion in 2026 and is projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 22.0% between 2026 and 2033. The accelerating shift toward biodegradable and eco-friendly surfactants in detergents is expected to add mileage to the adoption of methyl ester sulfonate in the personal care industry.

Stringent environmental regulations, particularly the European Union's REACH framework and updated Detergents and Surfactants Regulation (EC) 648/2004, mandate ultimate biodegradability of surfactants, positioning MES as a preferred alternative to petroleum-derived Linear Alkylbenzene Sulfonates (LAS).

Key Market Highlights

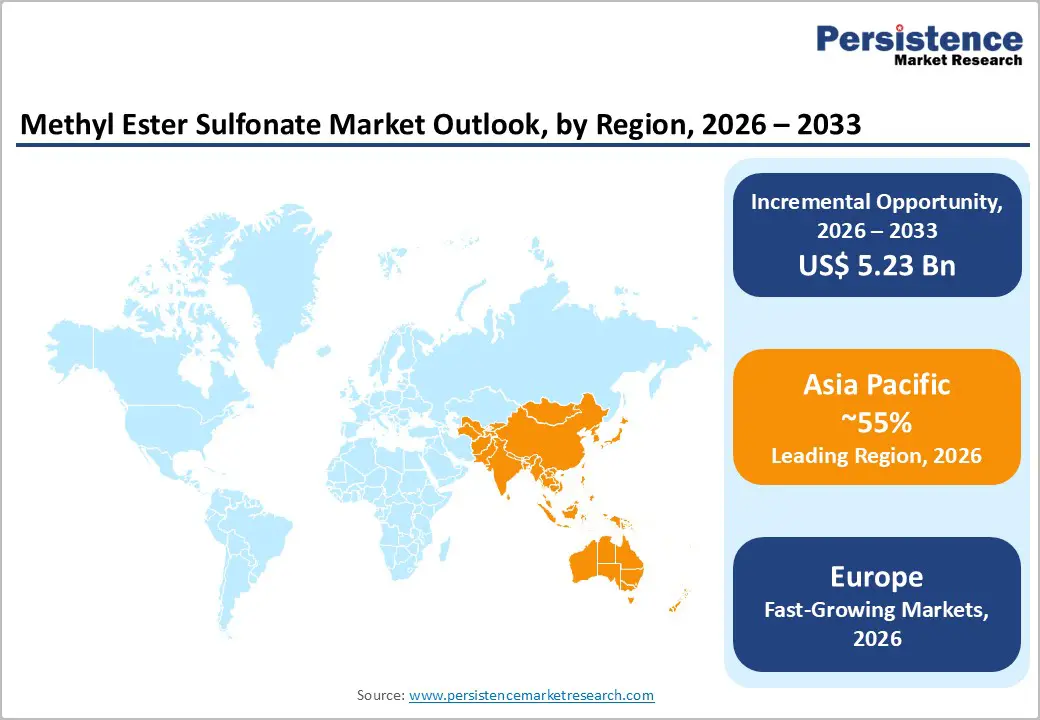

- Regional Leader: Asia Pacific leads the global Methyl Ester Sulfonate market with approximately 55% consumption share, driven by China, India, and Southeast Asian nations' rapid urbanization.

- Fastest Growing Region: Europe emerges fastest-growing region, driven by stringent regulatory harmonization and aggressive sustainability targets that strongly favor MES adoption across detergent and personal care applications.

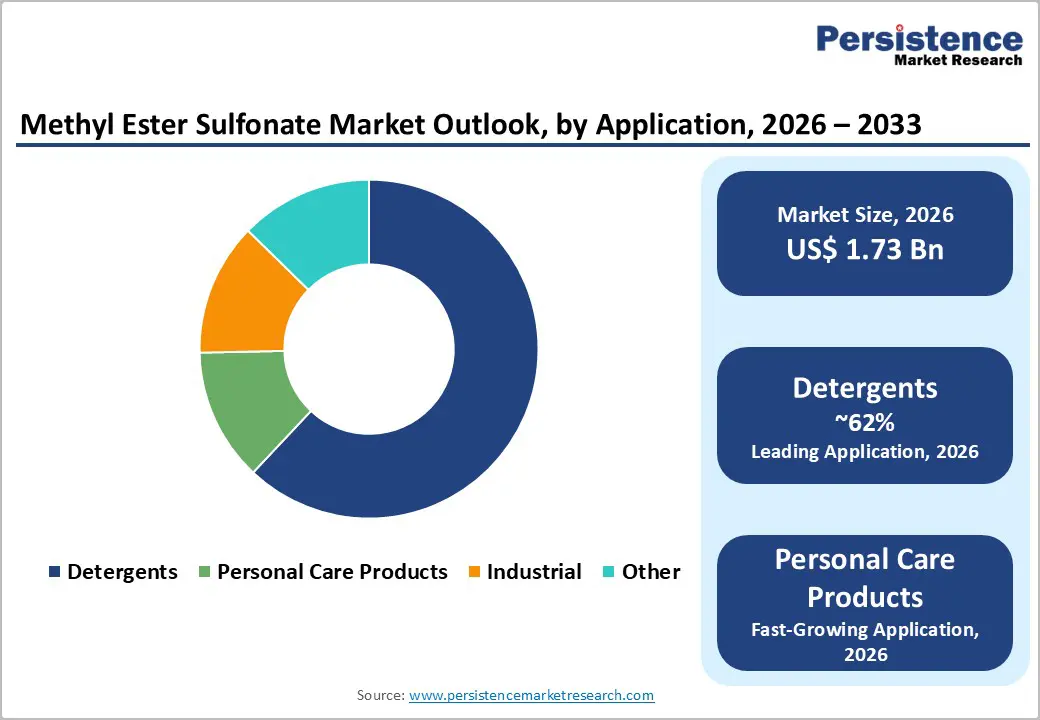

- Leading Segment: Powder form dominates with approximately 58% share, reflecting strong preferences in developing economies for cost-effective laundry detergents suitable for hand-washing applications, while demonstrating excellent solubility and hard water resistance critical for Asia Pacific market.

- Fastest Growing Segment: Personal Care Products application segment, driven by the Natural and Organic Personal Care Market expansion and consumer demand for sulfate-free, mild surfactants with superior dermatological profiles.

- Key Market Opportunity: The anticipated replacement of petroleum-derived LAS in powder detergent formulations across the Asia Pacific presents the most significant market opportunity, potentially generating incremental MES demand of 150,000-200,000 MT by 2030 as environmental regulations intensify globally.

| Key Insights | Details |

|---|---|

| Methyl Ester Sulfonate Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 6.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 22.0% |

| Historical Market Growth (2020 - 2025) | 11.8% |

Market Dynamics

Drivers - Rising Demand for Biodegradable Surfactants

Governments and regulatory bodies worldwide are implementing stringent environmental compliance standards that mandate the use of biodegradable surfactants in household and industrial cleaning products. The EU, in December 2025, approved an updated Detergents and Surfactants Regulation that strengthens biodegradability requirements for all surfactant components and introduces a Digital Product Passport system for enhanced traceability. REACH regulations in Europe and comparable frameworks in North America restrict non-biodegradable surfactants, creating substantial market opportunities for MES.

The compound's compatibility with palm-based feedstocks ensures reliable supply chains while reducing carbon footprints by approximately 30-40% compared to traditional alternatives. This regulatory momentum is particularly pronounced in developed markets where manufacturers are reformulating products to achieve eco-label certifications, thereby driving structural shifts in surfactant procurement strategies across the Detergent Chemicals Market.

Rising Consumer Preference for Sustainable Personal Care and Cleaning Solutions

The global personal care and cosmetics sector is witnessing transformative growth in demand for natural, mild, and environmentally responsible ingredients, directly benefiting the MES market. MES, derived from renewable palm oil through transesterification and sulfonation processes, offers superior skin compatibility and produces silky lather without irritating skin, eyes, or respiratory systems. This positions MES favorably within the expanding Natural and Organic Personal Care Market, where it serves as a sulfate-free alternative in shampoos, body washes, and baby care formulations.

The ingredient's versatility extends to the personal care chemicals ingredients, where it functions effectively across pH ranges while maintaining foam stability. Rising disposable incomes, urbanization, and growing awareness about personal hygiene, particularly in Asia Pacific economies like China, India, and Southeast Asia, are amplifying consumption patterns. The rapid expansion of e-commerce platforms has further democratized access to premium sustainable products, accelerating market penetration rates across demographic segments.

Restraints - Price Volatility and Supply Chain Dependencies on Palm Oil Derivatives

The MES production process relies heavily on palm-based feedstocks, particularly methyl esters derived from palm oil, making the market vulnerable to fluctuations in agricultural commodity prices. Indonesia accounts for approximately 57% of global palm oil production, creating significant geographic concentration risk. Seasonal variations, geopolitical developments in palm oil-producing regions, and sustainability concerns regarding deforestation can disrupt raw material availability and escalate costs.

Furthermore, Fatty Alcohol Market dynamics directly influence MES production economics, as both industries compete for similar palm-derived intermediates. Smaller manufacturers lacking vertical integration or advanced processing facilities face particular challenges in maintaining stable, high-purity MES formulations during feedstock volatility periods.

Technical Challenges in Formulation Stability and Cold-Water Performance

While MES demonstrates excellent biodegradability and surfactant properties, certain technical limitations constrain its broader application. Liquid detergent formulations containing MES can exhibit significant pH drift over time, requiring the incorporation of stabilizers such as urea or similar compounds to maintain product consistency. The compound's solubility characteristics, though generally favorable in powder detergents, present formulation challenges in concentrated liquid formats where maintaining homogeneity during storage and transportation is critical.

Furthermore, MES performance in cold-water washing conditions, increasingly important in energy-efficient washing machine cycles, requires careful formulation optimization with co-surfactants and builders. These technical complexities necessitate investment in research and development capabilities, potentially deterring market entry by smaller players who lack the resources to navigate formulation science intricacies.

Opportunity - Expanding Applications in Specialty Personal Care and Industrial Cleaning Segments

The evolution of consumer preferences toward premium personal care products presents substantial growth opportunities for MES-based formulations. The compound's mild nature and excellent dermatological profile position it advantageously for next-generation shampoos, body washes, baby care products, and specialty skincare applications where harshness reduction is paramount. Strategic collaborations between surfactant manufacturers and cosmetic formulators can unlock high-value, differentiated product offerings that command premium pricing in the natural and organic personal care market.

Beyond consumer applications, the industrial cleaning segment, encompassing oilfield chemicals, metal cleaners, agrochemical formulations, and specialty industrial applications, represents untapped potential. As industries adopt stricter effluent discharge norms and environmental impact assessments, MES-based industrial cleaners can capture market share from traditional petroleum-derived sulfonates and sulfates. The compound's compatibility with hard water and effectiveness as a calcium soap dispersant make it particularly valuable in industrial applications where water quality varies significantly.

Geographic Expansion and Capacity Additions in High-Growth Emerging Markets

Emerging markets, such as the Asia Pacific, are driving the demand for MES, driven by rapid urbanization, expanding middle-class populations, and rising washing machine penetration rates. Major producers, including Lion Corporation and KLK Oleo, have established significant manufacturing footprints in Malaysia, with combined production capacities exceeding 200,000 MT annually, positioned near palm oil source regions. The proximity to raw materials in palm oil-producing nations such as Indonesia and Malaysia creates structural cost advantages that support competitive pricing strategies.

Furthermore, government initiatives promoting sustainable manufacturing practices and green chemistry frameworks in China and Southeast Asian nations are expected to incentivize domestic MES production investments. The anticipated replacement of LAS in powder detergent formulations across the Asia Pacific could represent incremental demand of 150,000-200,000 MT by 2030, presenting significant volume growth opportunities for established and emerging market participants.

Category-wise Analysis

Form Insights

The powder form segment commands approximately 58% of the global methyl ester sulfonate market, reflecting its dominant position in developing economies where powder detergents remain the preferred choice for laundry applications. MES demonstrates excellent solubility and stability in powder formulations, making it particularly suitable for high-concentration detergent products popular in Asia.

The powder segment's market leadership is further reinforced by MES's superior performance as a calcium soap dispersant and its strong resistance to hard water conditions commonly encountered in these geographies. Production data from Malaysian Palm Oil Board (MPOB) confirms that palm stearin-based MES with C16/18 carbon chain compositions exhibits optimal detergency performance in powder applications. However, the Liquid form segment is experiencing rapid growth, particularly in developed markets and urban centers where consumers increasingly adopt liquid detergents for their convenience, ease of dissolution, and compatibility with modern washing machines.

Application Insights

The detergents application segment represents over 62% of global MES consumption, with laundry detergents accounting for the majority share within this category. This dominance reflects MES's fundamental role as an eco-friendly alternative to LAS in powder and liquid laundry formulations, where manufacturers increasingly reformulate products to meet environmental regulations and consumer expectations. Dishwashing applications constitute a smaller but growing sub-segment, where MES's mildness and skin compatibility provide advantages in hand-dishwashing liquid formulations.

The personal care products application segment, encompassing shampoos, body washes, and specialty formulations, emerges as the fastest-growing segment. This rapid expansion is driven by the Natural and Organic Personal Care Market's growth trajectory, where MES serves as a sulfate-free cleansing agent that delivers gentle yet effective performance. The shampoo formulations containing 10-15% MES active matter achieve optimal foaming characteristics while maintaining biodegradability standards.

Regional Insights

North America Methyl Ester Sulfonate Market Trends

North America maintains a mature yet strategically important position in the global MES market, with the U.S. demonstrating leadership in regulatory frameworks and innovation ecosystems that promote sustainable surfactant adoption. The region's stringent environmental standards, enforced through agencies such as the EPA, which maintains comprehensive Safer Choice Criteria for Surfactants, drive manufacturers toward biodegradable alternatives in household and industrial cleaning applications.

Major surfactant manufacturers, including Stepan Company and Chemithon Corporation, have invested in MES production capabilities and formulation technologies to serve domestic demand while supporting export markets. The North American regulatory environment emphasizes life cycle assessments, carbon footprint reduction, and circular economy principles, creating favorable conditions for bio-based surfactants despite higher initial costs compared to conventional alternatives.

Europe Methyl Ester Sulfonate Market Trends

Europe represents a sophisticated market characterized by stringent regulatory harmonization and aggressive sustainability targets that strongly favor MES adoption across detergent and personal care applications. The European Union's recently approved update to Regulation (EC) 648/2004 introduces strengthened biodegradability requirements, prohibits animal testing, and mandates Digital Product Passports for detergent products, creating structural advantages for bio-based surfactants.

REACH regulations compel manufacturers to substantiate the safety and environmental profiles of all chemical substances used in consumer products, effectively limiting the use of non-biodegradable surfactants and accelerating the transition toward alternatives like MES. European consumers demonstrate a high willingness to pay premium prices for products carrying eco-labels such as EU Ecolabel, Nordic Swan, and Der Blaue Engel, creating market opportunities for differentiated MES-based formulations. The region's established supply chain relationships with palm oil producers and advanced sulfonation technologies support product quality consistency and regulatory compliance.

Asia Pacific Methyl Ester Sulfonate Market Trends

Asia Pacific dominates the global Methyl Ester Sulfonate market, accounting for approximately 55% share of the global market. China alone accounts for over 35% of the Asia Pacific laundry detergent market, with strong consumer preferences for both powder and liquid formats creating diverse application opportunities for MES.

The region's strategic advantage stems from its proximity to palm oil production sources, with Indonesia supplying 57% of global palm oil output and Malaysia hosting major MES manufacturing facilities, including Lion Corporation's plant in Tanjung Langsat, Johor, and KLK Oleo's Oleomas facility in Pulau Indah, Selangor. These integrated production ecosystems enable competitive pricing while ensuring reliable raw material access, creating structural cost advantages that support aggressive market penetration strategies in price-sensitive segments.

Competitive Landscape

The global methyl ester sulfonate market exhibits a moderately consolidated structure with a mix of established multinational chemical corporations and regional specialty producers competing across different geographic and application segments. Market leaders pursue vertical integration strategies to secure palm oil feedstock supplies while investing in advanced sulfonation technologies and application development capabilities. Strategic partnerships between surfactant manufacturers and detergent brands enable collaborative product development and formulation optimization, particularly for challenging applications like concentrated liquids and cold-water detergents. Emerging business model trends include offering integrated surfactant systems combining MES with complementary co-surfactants and builders to simplify customer formulation processes.

Key Market Developments:

- December 2025: The European Union approved comprehensive updates to the Detergents and Surfactants Regulation, strengthening biodegradability requirements and introducing Digital Product Passport systems that enhance transparency and traceability for surfactant supply chains, benefiting compliant bio-based alternatives like MES.

- June 2025: Wilmar International Limited is set to acquire PZ Cussons plc’s 50% stake in their Nigerian joint venture, PZ Wilmar, making Wilmar the sole owner. PZ Wilmar operates one of Nigeria’s largest sustainable palm oil businesses, producing popular edible oils under the Mamador and Devon King’s brands.

- February 2025: KLK OLEO expanded its global presence by opening a new representative office in Mumbai, India, under KLK OLEO India (KLKOI). This strategic move strengthens its position in the growing Indian market, particularly for applications such as Methyl Ester Sulphonates (MES), widely used in detergents and personal care formulations.

Top Companies in Methyl Ester Sulfonate

- KLK Oleo (Selangor, Malaysia) operates one of the world's largest MES production facilities with 150,000 MT annual capacity at its Oleomas plant in Pulau Indah. The company leverages its integrated palm oil value chain to produce PALMFONATE branded Methyl Ester Sulphonates, positioning itself as a leading supplier to detergent manufacturers across Asia Pacific, Europe, and the Americas. KLK Oleo's vertical integration from plantation to specialty oleochemicals provides cost advantages and supply chain reliability that support competitive pricing strategies in volume-sensitive detergent applications.

- Lion Corporation (Tokyo, Japan) has established a significant MES manufacturing presence through its Lion Eco Chemicals subsidiary in Tanjung Langsat, Johor, Malaysia, with 50,000 MT production capacity serving regional and export markets. The company's expertise in consumer products formulation enables it to develop application-specific MES grades optimized for laundry detergents, dishwashing liquids, and personal care products.

- Stepan Company (Northfield, Illinois, U.S.) brings over 90 years of surfactant manufacturing expertise to the MES market, focusing on high-purity grades and specialized formulations for personal care and industrial applications. The company's technical service capabilities and formulation support differentiate its market position, particularly in premium segments where performance optimization and regulatory compliance are critical.

Companies Covered in Methyl Ester Sulfonate Market

- KLK Oleo

- Jinchang Chemical

- Zanyu Technology Group Co., Ltd.

- Lion Corporation

- Chemithon Corporation

- Wilmar International Ltd.

- KPL International Ltd.

- Stepan Company

- Henan Surface Chemical Industry Co., Ltd.

- Shaoxing Zhenggang Chemical Co.,Ltd.

- Guangzhou Keylink Chemical Co., Ltd.

Frequently Asked Questions

The global Methyl Ester Sulfonate market is projected to reach US$ 6.9 Bn by 2033, expanding from US$ 1.7 Bn in 2026 at a robust compound annual growth rate of 22.0% during the forecast period.

The methyl ester sulfonate market is primarily driven by stringent environmental regulations mandating biodegradable surfactants, particularly the European Union's updated Detergents and Surfactants Regulation and REACH framework, combined with rising consumer preferences for sustainable personal care and cleaning products across global markets.

The Detergents application segment dominates with over 62% market share, driven by widespread adoption in laundry and dishwashing formulations as an eco-friendly alternative to petroleum-derived Linear Alkylbenzene Sulfonates in powder and liquid detergent formats.

Asia Pacific leads with approximately 55% of global consumption, driven by China, India, Indonesia, and ASEAN nations' rapid urbanization, proximity to palm oil raw materials, and expanding middle-class populations with increasing washing machine penetration.

The most significant opportunity lies in the anticipated replacement of LAS in powder detergent formulations across the Asia Pacific, potentially generating 150,000-200,000 MT of incremental demand by 2030.

Key players include KLK Oleo, Lion Corporation, Stepan Company, Wilmar International Ltd., Chemithon Corporation, Zanyu Technology Group, Jinchang Chemical, and KPL International Ltd., with KLK Oleo and Lion Corporation.