- Specialty & Fine Chemicals

- Dimethyl Sulfide (DMS) Market

Dimethyl Sulfide (DMS) Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Dimethyl Sulfide (DMS) Market by Purity Type (Industrial Grade, Pharmaceutical Grade, Food Grade), Application (Food & Beverages, Chemical Manufacturing, Pharmaceuticals, Agriculture), End-User (Food & Beverages Industry, Chemical Industry, Pharmaceuticals Industry, Agriculture Industry), and Regional Analysis for 2026 - 2033

Dimethyl Sulfide (DMS) Market Share and Trends Analysis

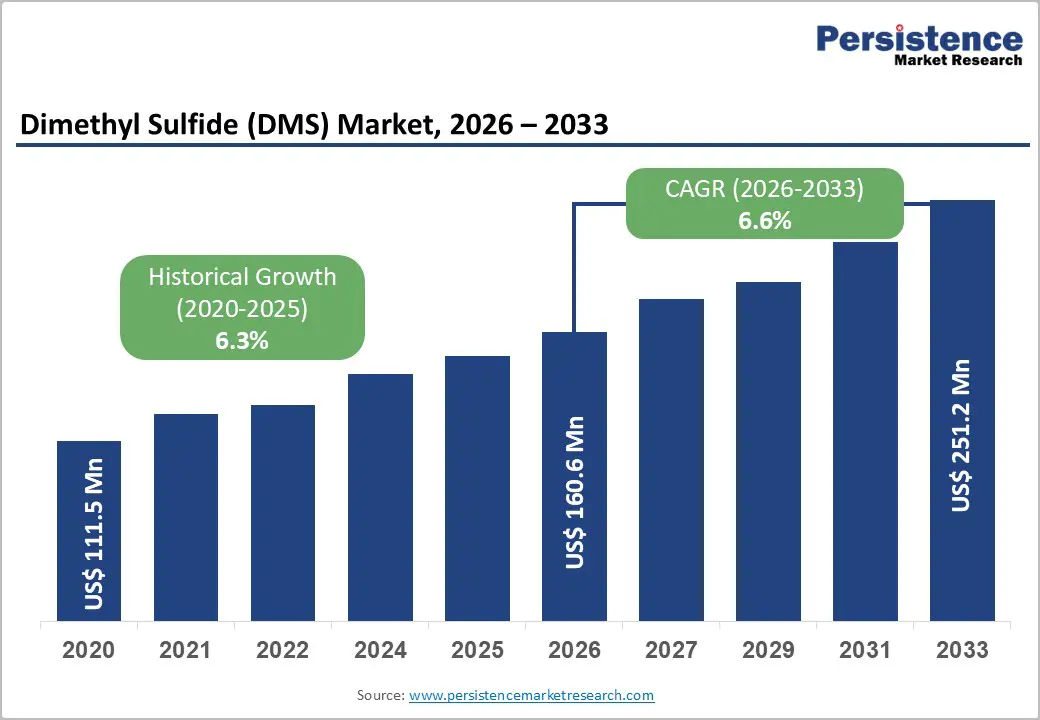

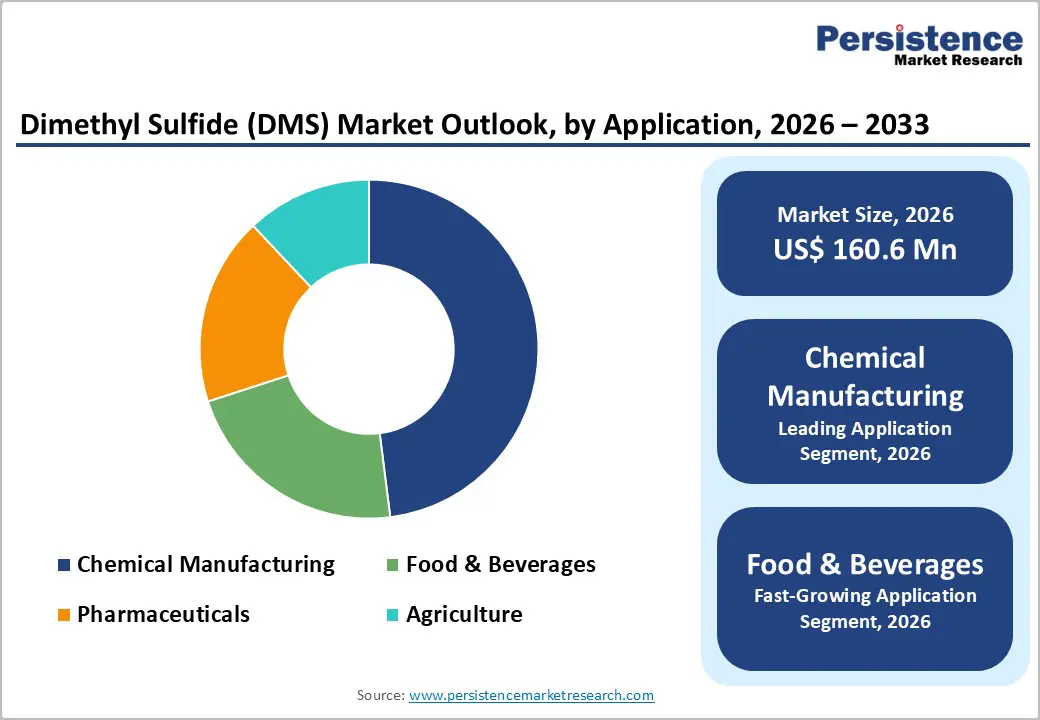

The global dimethyl sulfide (DMS) market size is likely to be valued at US$ 160.6 million in 2026, and is projected to reach US$ 251.2 million by 2033, growing at a CAGR of 6.6% during the forecast period 2026 - 2033.

Demand has been expanding across food flavoring, chemical synthesis, and pharmaceutical intermediate applications, with food and beverage producers in particular having relied on dimethyl sulfide (DMS) to support standardized flavor systems as processed food volumes have increased worldwide. At the same time, industrial users in chemical production have been using DMS within sulfide-based reaction chains for agrochemicals and specialty chemicals, which has helped to anchor a predictable baseline of technical demand across business cycles.

Growth has also been reinforced by broader regulatory acceptance of carefully controlled sulfur-based ingredients in food applications, together with ongoing improvements in purity control and odor management technologies that have enhanced product consistency and handling characteristics. These factors have created a market in which both volume and value opportunities have emerged across the entire application spectrum, from large flavor houses and food processors to integrated chemical and pharmaceutical manufacturers.

Operators that have been refining formulation strategies, investing in advanced quality assurance, and engaging early with regulators will have positioned themselves to capture a greater share of this growth as demand for differentiated flavors and high-performance intermediates has continued to rise.

Key Industry Highlights

- Application Dominance: Chemical manufacturing is slated to command an estimated 48% share in 2026, underpinned by high-volume production of specialty chemicals.

- Fastest-growing Application: Food and beverages are projected to be the fastest-growing through 2033, driven by the widespread demand for processed foods and flavor innovation.

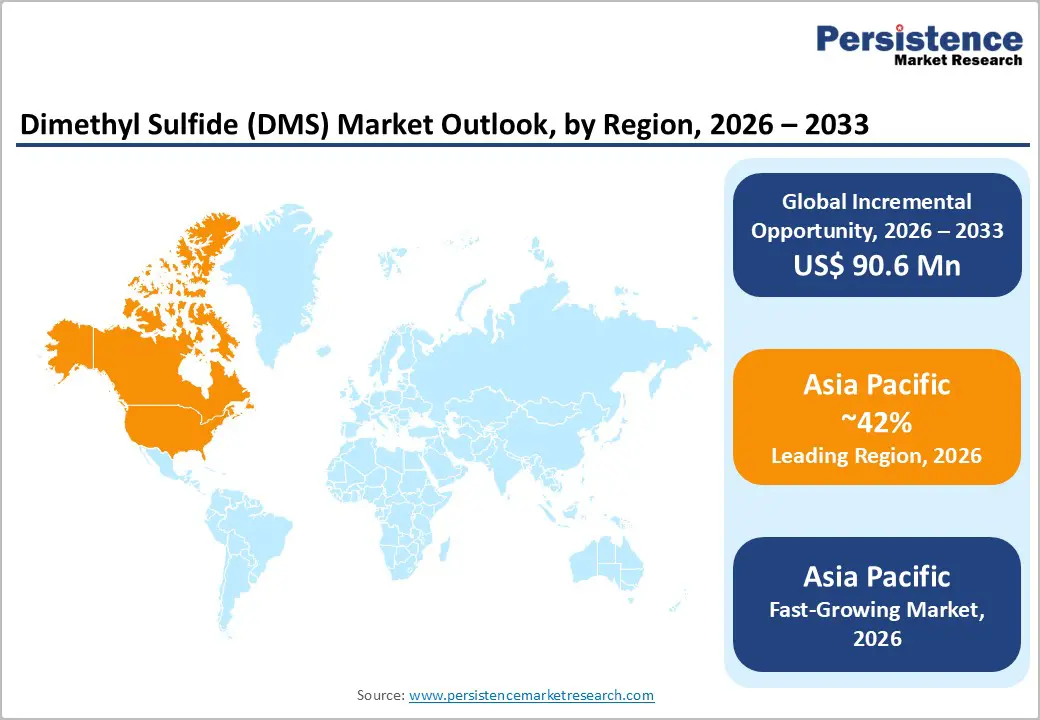

- Dominant Region: Asia Pacific is expected to lead the DMS market share in 2026 with about 42%, supported by strong chemical manufacturing and downstream industrial demand.

- Fastest-growing Regional Market: Asia Pacific is projected to emerge as the fastest-growing market through 2033, propelled by expanding chemical production.

| Key Insights | Details |

|---|---|

| Dimethyl Sulfide (DMS) Market Size (2026E) | US$ 160.6 Mn |

| Market Value Forecast (2033F) | US$ 251.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.6 % |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand in Petrochemical and Chemical Industries

Rising demand from petrochemical and chemical industries stands as a primary growth catalyst for the dimethyl sulfide value chain due to its functional role as an intermediate in specialty chemical synthesis and performance-driven applications. Refinery operators and chemical processors prioritize sulfur-based intermediates that support selective reactions, odorant formulations, and catalyst conditioning processes where process stability and yield optimization remain critical.

Expansion of downstream chemicals such as methionine, agrochemical intermediates, and sulfur-containing fine chemicals strengthens procurement volumes, supported by continuous capacity debottlenecking across integrated petrochemical complexes. Operational efficiency requirements within petrochemical and chemical manufacturing further elevate adoption levels, as producers seek cost-effective inputs that align with process reliability, scalability, and regulatory compliance. Sulfur management strategies increasingly favor compounds that enable controlled sulfur introduction without complex handling risks, supporting consistent quality across batch and continuous processing environments.

Growth in gas processing, refining upgrades, and specialty chemical diversification across Asia Pacific and the Middle East reinforces long-term demand visibility, supported by capital investments targeting higher-value chemical derivatives. Strategic sourcing agreements and backward integration initiatives signal confidence in sustained usage patterns, reflecting its importance in maintaining competitive cost structures and product performance standards.

Tightening Environmental and Safety Regulations

Stringent environmental and safety regulations act as a key restraint due to the compound's high volatility, strong odor profile, and potential health risks across production, storage, and transportation stages. Even low-level emissions trigger community complaints, regulatory scrutiny, and mandatory mitigation investments, raising operational complexity. Air quality frameworks in multiple regions classify sulfur-based compounds under hazardous air pollutants, requiring advanced containment, leak detection, and odor control systems.

Compliance demands specialized infrastructure such as sealed reactors, scrubbers, and continuous monitoring, which elevates capital expenditure and extends project timelines. Occupational safety standards further intensify constraints by enforcing strict exposure limits and emergency response protocols. The compound presents inhalation risks that necessitate comprehensive worker training, personal protective equipment, and redundant safety systems, increasing fixed operating costs.

For evidence, the odor detection threshold for dimethyl sulfide is reported at approximately 0.1-0.3 parts per billion, a level documented by environmental health agencies, which explains why even trace releases attract regulatory action and public opposition. Downstream users face parallel pressure as end-use sectors prioritize substitutes with lower compliance burdens to reduce liability exposure.

Emerging DMS Applications in Sustainable Agriculture and Bio-based Pesticides

The emergence of sustainable agriculture and bio-based pesticides represents a high-impact opportunity for dimethyl sulfide due to its functional relevance within ecological crop protection systems. Transition toward residue-free food production and regenerative farming practices elevates demand for inputs that align with soil health, biodiversity preservation, and compliance-driven farming models. DMS supports pest behavior modulation through semiochemical activity, enabling targeted control strategies that reduce reliance on broad-spectrum synthetic formulations.

This functional advantage positions it as a valuable component in integrated pest management programs adopted by large-scale farms and agri-input suppliers seeking performance efficiency under tightening regulatory frameworks. Structural shifts across the agricultural value chain reinforce long-term commercial relevance. Expansion of organic and sustainable farming systems reshapes input procurement priorities toward bio-based, low-toxicity compounds with scalable production economics.

DMS benefits from efficient synthesis routes, formulation flexibility, and alignment with biological crop protection products developed for cereals, horticulture, and specialty crops. Regulatory preference for biodegradable and environmentally neutral inputs enhances commercialization prospects, while agri-technology companies leverage DMS to broaden bio-pesticide portfolios and strengthen differentiation in premium segments.

Category-wise Analysis

Purity Type Insights

Industrial-grade dimethyl sulfide is likely to be the leading segment with a projected 62% of the DMS market revenue share in 2026 due to its dominant role in large-scale chemical manufacturing, agrochemical synthesis, and sulfur-based intermediate production. Industrial consumers operate volume-intensive processes that favor standardized grades with consistent performance and competitive pricing. Long-term supply contracts, predictable demand cycles, and relatively lower regulatory complexity support stable consumption patterns. Procurement strategies focus on supply reliability, logistics efficiency, and cost control, reinforcing repeat purchasing behavior.

Pharmaceutical-grade is anticipated to be the fastest-growing segment from 2026 to 2033 due to expanding active pharmaceutical ingredient manufacturing and rising regulatory scrutiny around purity, traceability, and batch consistency. Pharmaceutical producers increasingly prioritize qualified suppliers capable of meeting stringent compliance standards and documentation requirements. Growth is further supported by outsourcing trends toward Asia Pacific manufacturing hubs, where capacity expansion continues across regulated facilities. Higher value realization, premium pricing structures, and long-term supply agreements enhance commercial attractiveness.

Application Insights

Chemical manufacturing is projected to hold 48% of the dimethyl sulfide market revenue share in 2026, supported by its integral role in producing high-value intermediates for specialty chemicals, solvents, and sulfur-containing compounds. Demand is reinforced by large-scale batch and continuous synthesis processes that rely on dimethyl sulfide for efficiency and consistency. Industrial-scale operators favor predictable supply, cost stability, and compatibility with complex chemical reactions. High technical entry barriers and the need for process standardization further consolidate this segment in the market.

Food and beverages are estimated to be the fastest-growing segment from 2026 to 2033, underpinned by rising innovation in flavor enhancement, natural ingredient formulations, and industrial-scale taste modulation. Increasing urbanization and processed food demand in Asia Pacific and Latin America drive the need for scalable flavor compounds. Manufacturers are leveraging dimethyl sulfide for subtle aroma enhancement and preservation of sensory profiles in packaged foods and beverages. Investment in new production facilities and advanced blending technologies enables higher adoption rates.

End-User Insights

The chemical end-user segment is slated to hold a dominant position, with an anticipated 50% of the dimethyl sulfide market share in 2026, supported by its critical role in large-scale synthesis of specialty chemicals, solvents, and sulfur-based intermediates. Industrial-scale operations rely on DMS for consistent reaction efficiency, predictable supply, and cost optimization. Established procurement channels, long-term contracts, and technical process requirements strengthen demand stability. High barriers to entry and integration across multiple chemical value chains reinforce its market dominance

The food and beverages end-user segment is forecasted to be the fastest-growing between 2026 and 2033, boosted by rising consumption of packaged and processed foods, product diversification, and premium flavor enhancement. Dimethyl Sulfide is utilized to improve aroma, maintain flavor consistency, and support scalable industrial production. Expansion in emerging markets, increasing urbanization, and consumer preference for high-quality sensory experiences drive adoption. Regulatory clarity on permissible usage levels and continuous innovation in flavor systems further strengthen growth prospects.

Regional Insights

North America Dimethyl Sulfide (DMS) Market Trends

North America is estimated to remain a significant market for dimethyl sulfide, underpinned by well-established chemical manufacturing infrastructure, robust industrial activity, and diversified end-use demand across specialty chemicals, pharmaceuticals, and agrochemical intermediates. The presence of major manufacturing hubs in the United States and Canada supports high-volume production with efficient supply chains and advanced process control.

Industrial users prioritize consistency, compliance with strict environmental and safety standards, and predictable supply, which strengthens baseline demand. Long-term procurement arrangements, strategic partnerships with downstream manufacturers, and advanced logistics networks reinforce market stability and revenue predictability.

The North America DMS market also benefits from ongoing investments in process innovation and energy-efficient production methods, enabling higher output quality with lower environmental impact. Expanding pharmaceutical and food additive production, along with increasing adoption of bio-based chemical inputs, drives additional demand for DMS. Strong regulatory frameworks ensure safe handling and traceability, attracting global buyers seeking compliant supply.

Technological advancements in intermediate synthesis, controlled reaction processes, and precision chemical manufacturing further enhance adoption. Access to export markets, combined with skilled technical workforce and research capabilities, enables manufacturers to scale operations efficiently.

Europe Dimethyl Sulfide (DMS) Market Trends

Europe is predicted to maintain a prominent share of the DMS market in 2026, anchored by its strong presence of established chemical manufacturing clusters and highly regulated industrial practices. Countries such as Germany, France, and Italy have mature chemical production infrastructure that emphasizes process efficiency, high-purity output, and compliance with stringent environmental and safety standards. Industrial users in specialty chemicals, pharmaceuticals, and fine chemical synthesis rely on DMS for consistent performance in multi-step reactions, intermediate synthesis, and flavor enhancement applications.

Europe also benefits from widespread adoption of sustainable production methods and bio-based chemical inputs. Focus on low-emission manufacturing, circular economy initiatives, and regulatory enforcement of product safety encourages use of DMS in controlled and compliant processes. Rising demand from food and beverage flavor applications and pharmaceutical intermediates drives diversification of consumption, reducing dependence on any single sector. Strategic trade positioning enables efficient access to export markets, reinforcing economic viability of large-scale production.

Asia Pacific Dimethyl Sulfide (DMS) Market Trends

Asia Pacific is positioned to dominate in 2026, capturing an estimated 42% of the DMS market share, reflecting its strategic concentration of chemical manufacturing hubs, integrated supply chains, and economies of scale that support high-volume production. Leading economies such as China, India, and Japan benefit from robust industrial infrastructure, advanced chemical process expertise, and proximity to raw material sources, which reduce input costs and enhance supply reliability.

Dominance is reinforced by a well-established network of downstream industries, including agrochemicals, specialty chemicals, and pharmaceuticals, that heavily rely on DMS as a sulfur-based intermediate. Strong industrial procurement frameworks, long-term contracts, and high operational efficiency enable consistent offtake while mitigating market volatility. Government incentives for industrial clusters, export-oriented policies, and access to low-cost skilled labor further consolidate market leadership.

Asia Pacific is also forecast to emerge as the fastest-growing market through 2033, fueled by expanding domestic chemical production, rising urbanization, and increasing demand for sustainable industrial solutions. Emerging economies in the area are investing heavily in capacity expansion for pharmaceutical-grade and food-grade DMS applications, tapping into growing organic and processed food sectors. Technological upgrades in precision chemical synthesis, energy-efficient production, and controlled-release industrial processes enable manufacturers to scale rapidly while maintaining high product quality. Rising adoption of bio-based agrochemical intermediates, stricter regulatory compliance, and growing exports of specialty chemicals contribute to accelerated market growth.

Competitive Landscape

The global dimethyl sulfide market has achieved moderate consolidation, where leading producers such as Arkema, Merck, Chevron Phillips, Tokyo Chemical Industry, and Toray Fine Chemicals Company Limited have secured a substantial share of worldwide supply. These firms have concentrated on manufacturing high-purity DMS for critical uses including chemical intermediates, pharmaceutical synthesis, agrochemical production, and flavor compounds.

Advanced research & development (R&D) efforts, coupled with technological advancements and streamlined production methods, have consistently delivered reliable quality to meet diverse industry standards. Operators partnering with these suppliers have gained access to tailored formulations that enhance reaction efficiency and reduce impurities in downstream processes.

For deepening their market presence, companies are implementing targeted strategies such as capacity expansions, creation of specialized DMS variants, and partnerships with pharmaceutical and industrial clients. Operators have prioritized robust process controls, rigorous quality certifications, and adherence to environmental regulations, which have built trust and facilitated multi-year supply agreements.

Continuous refinement of product grades and pursuit of high-margin applications in emerging sectors have positioned these leaders for sustained growth. Companies that diversify into sustainable production methods and novel uses will have optimized profitability while addressing tightening global compliance demands by 2033.

Key Industry Developments

- In January 2026, Oregon State University researchers developed a gas chromatography-mass spectrometry (GC-MS)-supported sensory lexicon for cannabis inflorescence aroma, showing terpenes alone fail to predict perception while volatile sulfur compounds such as dimethyl sulfide play key roles.

- In July 2025, astronomers identified K2-18b as a potential habitable exoplanet with signs of DMS, a possible biosignature gas produced by marine phytoplankton on Earth. Future James Webb Space Telescope observations will confirm if this Hycean world truly hosts life indicators.

- In June 2025, an Indian Institute of Tropical Meteorology study reported that emissions of the ocean-produced sulfur gas DMS were projected to increase due to stronger winds and warmer sea surface temperatures, potentially enhancing natural aerosol formation that could modestly help cool the planet as global warming continues.

Frequently Asked Questions

The global dimethyl sulfide (DMS) market is projected to reach US$ 160.6 million in 2026.

Rising demand from chemical manufacturing, pharmaceuticals, agrochemicals, and food and beverage flavoring applications drives growth in the market.

The market is poised to witness a CAGR of 6.6 % from 2026 to 2033.

Key market opportunities include expanding applications in sustainable agriculture, pharmaceuticals, food and beverage flavoring, and industrial chemical intermediates.

Key players in the market include Arkema, Merck KGaA, Chevron Phillips Chemical Company LLC, and Tokyo Chemical Industry (India) Pvt. Ltd.