- Medical Devices

- Medical Smart Glasses Market

Medical Smart Glasses Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Smart Glasses by Technology (Optic See Through, Virtual Retinal Display, Projection based), Display (OLED, LCOS, DLP), Application (Augmented Reality, Virtual Reality, Surgery Assistance), and Regional Analysis 2026–2033

Medical Smart Glasses Market Size and Trends Analysis

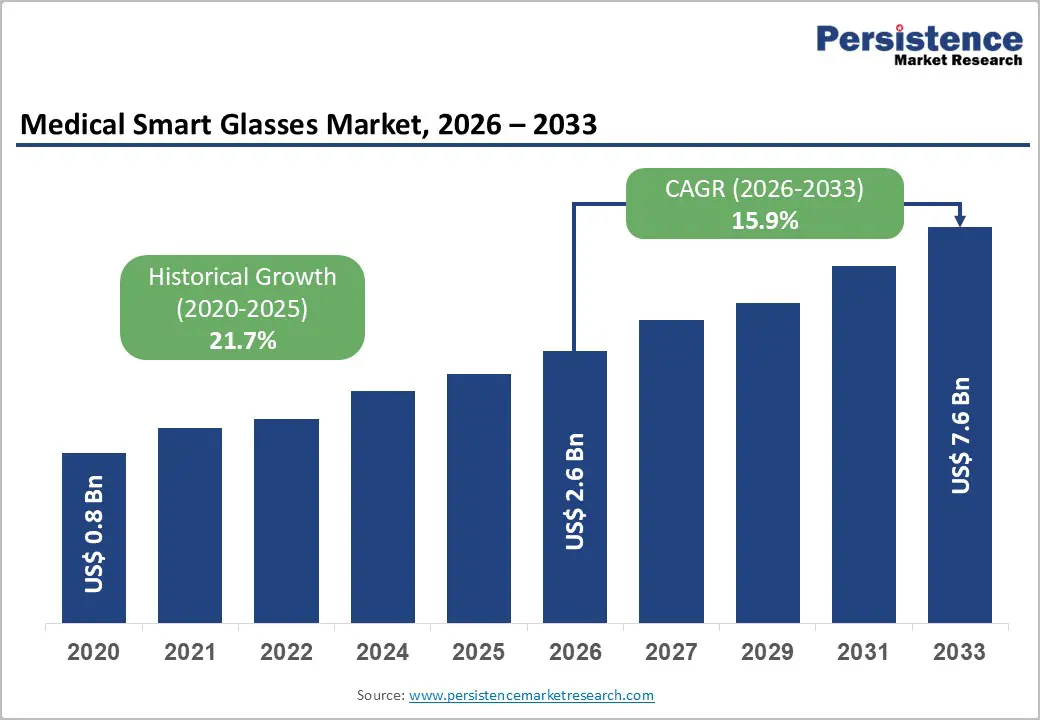

The global medical smart glasses market size is likely to be valued at US$2.6 billion in 2026 and is expected to reach US$7.6 billion by 2033, growing at a CAGR of 15.9% during the forecast period between 2026 and 2033, driven by the increasing use of augmented reality (AR) and virtual reality (VR) technologies in areas such as surgical visualization, remote patient monitoring, and telemedicine. Key factors fueling the market expansion include the rising adoption of telemedicine solutions, improvements in AR integration that enhance surgical accuracy and clinical efficiency, and the post-COVID normalization of telehealth services. The rollout of 5G connectivity, which supports real-time data transmission, along with AI-driven diagnostic tools, is broadening the applications of medical smart glasses across various surgical specialties and diagnostic fields.

Key Industry Highlights:

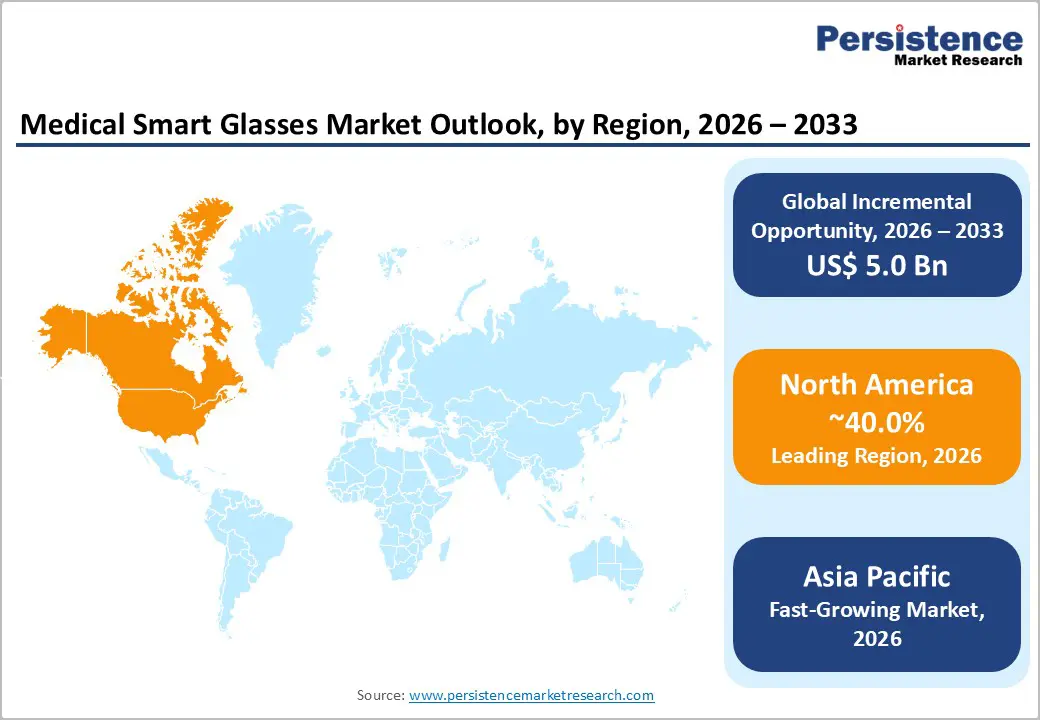

- Leading Region: North America is expected to remain the leading market for medical smart glasses, accounting for approximately 40% of global deployments, supported by advanced healthcare infrastructure, early adoption of AR-assisted surgical workflows, strong R&D funding, and clear regulatory pathways for clinical-grade wearable technologies.

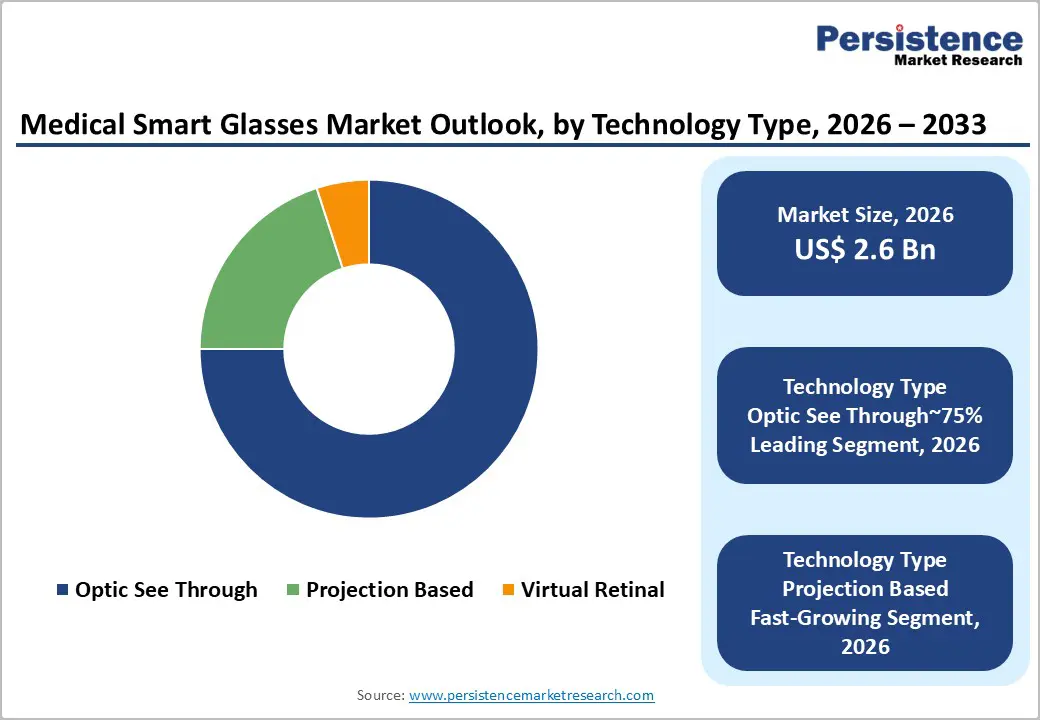

- Leading Technology Type: Optical see-through (OST) technology is expected to remain the leading technology segment, representing an estimated 75% share of adoption, due to its real-time, heads-up visualization that preserves direct patient visibility and aligns closely with surgical and interventional clinical workflows.

- Leading Application: Surgery assistance is expected to remain the leading application segment, accounting for approximately 45% of the total adoption, driven by demand for hands-free data access, real-time visualization, and remote expert collaboration in operating room environments.

- Key Industry Development: In February 2024, Pixee Medical secured US$15 million in funding to expand U.S. AR orthopedic solutions. This funding, led by investors like Bpifrance, supports scaling Knee+ solutions integrated with Vuzix M400 glasses, reducing surgical errors by 20% in pilots.

| Key Insights | Details |

|---|---|

| Medical Smart Glasses Market Size (2026E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 7.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 21.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

5G Connectivity and AI-Powered Real-Time Analytics Integration

The convergence of advanced connectivity and edge-level AI processing is structurally reshaping smart glasses adoption across regulated and enterprise-intensive sectors. Expanded 5G availability and energy-efficient OLED micro displays have removed legacy latency, bandwidth, and battery-life constraints that previously restricted continuous-use scenarios. On-device AI now supports real-time image recognition, intraoperative data overlays, and contextual decision support, reinforcing clinical precision and workflow compression. These capabilities reposition smart glasses from experimental visualization tools into productivity-enabling infrastructure, particularly in healthcare and industrial environments where responsiveness and situational awareness are non-negotiable.

In December 2025, SoftBank, Ericsson, and Qualcomm will trial 5G advanced technologies that achieve a 90% reduction in latency for AI-enabled XR streaming on smart glasses. This development underscores accelerating alignment between network evolution and immersive device requirements, reinforcing commercial viability at scale. Demonstrated latency compression strengthens real-time XR streaming, while reinforcing ecosystem readiness for regulated use cases. The adoption trajectories remain uneven, shaped by spectrum policy, cybersecurity mandates, and capital intensity, favoring markets with mature digital health and industrial compliance frameworks.

Data Privacy, Cybersecurity, and Recording Consent Compliance

Privacy, data governance, and cybersecurity exposure remain binding structural restraints that materially shape adoption pathways for medical smart glasses. Regulatory authorities increasingly frame continuous visual capture, behavioral inference, and biometric processing as high-risk activities, elevating compliance from a technical consideration to a gating requirement. Privacy-by-design mandates, explicit recording notifications, granular user controls, and auditable data-processing workflows intensify system-level integration demands. In healthcare environments, alignment with protected health data standards and hospital cybersecurity architectures further constrains deployment flexibility, reinforcing institutional risk sensitivity over functional performance gains.

These constraints extend well beyond device specifications, embedding compliance obligations across software validation, workflow redesign, governance oversight, and procurement cycles. The resulting escalation in ownership complexity and approval scrutiny disproportionately affects budget-limited institutions and multi-site providers. As regulatory interpretation continues to evolve and enforcement tightens, privacy and security readiness increasingly determines which solutions progress beyond pilots and which remain structurally constrained by unresolved compliance exposure.

AI-Enhanced Diagnostics and Surgical Training Innovations

AI-driven diagnostics and immersive surgical training represent a structurally significant opportunity layer within the medical smart glasses value chain. Predictive analytics embedded at the device level are reshaping diagnostic workflows by compressing decision cycles and improving procedural accuracy, particularly in high-variability surgical environments. Simultaneously, persistent skill gaps and limited access to live-case exposure continue to constrain surgical training scalability. XR-enabled simulations address these deficits by enabling repeatable, data-rich practice environments that align with outcome-based healthcare delivery models. Policy-backed research funding and institutional emphasis on cost-efficient workforce upskilling are reinforcing investment momentum, positioning education and training as a durable demand vector rather than a peripheral application.

In June 2025, Lucid Reality Labs won the AWE Auggie award for a medical AI agent enabling real-time XR simulations and error reduction in surgical training. This recognition signals growing validation of AI-mediated XR systems as a clinically relevant training infrastructure. As simulation fidelity, real-time feedback, and adaptive learning algorithms mature, the boundary between training and live clinical support continues to narrow, reshaping how surgical competence, risk mitigation, and long-term workforce resilience are structurally addressed.

Category–wise Analysis

Technology Type Insights

Optical see-through (OST) technology is expected to remain the leading technology segment in the medical smart glasses market, accounting for an estimated 75% share of total adoption in 2026. This leadership is anticipated due to its inherent “heads-up, see-through” design that allows clinicians to maintain uninterrupted visual contact with patients while accessing real-time data overlays. OST solutions align closely with surgical and interventional workflows, where situational awareness and zero-latency visual input are critical. Ongoing advances in waveguide optics, miniaturization, and lightweight frame engineering are reinforcing adoption across operating rooms and diagnostic settings. Platform-level ecosystem development, including AI-enabled contextual assistance and hospital-specific AR content creation, is further strengthening OST’s position. Increased scrutiny around clinical validation, device classification, and patient data protection is likely to favor established vendors with mature hardware-software stacks, secure operating environments, and proven deployment experience in clinical settings.

Projection-based smart glasses are anticipated to emerge as the fastest-expanding technology segment, driven by their ability to deliver high-brightness visuals in ultra-lightweight form factors suitable for extended medical use. This segment is gaining traction as healthcare providers seek hands-free visualization without adding ergonomic burden during long procedures or remote collaboration sessions. Advances in micro-projectors, laser beam scanning, and cloud-assisted rendering are expected to accelerate adoption in surgical guidance, remote assistance, and training environments. Projection systems are also benefiting from broader trends toward AI-assisted clinical decision support, edge computing, and high-speed connectivity, which enable complex visual overlays without on-device processing strain. Evolving approval pathways for advanced visualization tools, combined with stricter expectations around data security and recording controls, are likely to shape vendor strategies and accelerate consolidation among projection-focused technology providers.

Application Insights

Surgery assistance is expected to remain the leading application segment in the medical smart glasses market, accounting for approximately 45% of overall application-level adoption in 2026. This dominance reflects the growing integration of smart glasses into operating environments where real-time visualization, hands-free data access, and remote collaboration are becoming standard clinical requirements. Surgeons increasingly rely on in-field overlays for patient vitals, imaging references, and procedural guidance without disrupting sterile workflows. The segment’s strength is further reinforced by the rising adoption of minimally invasive procedures, where precision visualization and situational awareness directly influence outcomes. Large hospital systems and advanced surgical centers are likely to continue prioritizing surgery-focused deployments, as smart glasses support error reduction, workflow efficiency, and real-time expert consultation across complex procedures.

Augmented reality applications are anticipated to emerge as the fastest-expanding application segment within the medical smart glasses market. Growth is driven by the transition from passive display use cases toward active, context-aware procedural guidance, where digital content is dynamically anchored to the clinician’s physical field of view. AR is increasingly used for anatomical overlays, surgical navigation, remote expert annotation, and immersive training, making it central to next-generation clinical workflows. As hospitals accelerate digital transformation initiatives and regulatory frameworks increasingly formalize AI-enabled clinical tools, AR-based applications are likely to see broader institutional acceptance. Continued advances in optics, spatial mapping, and on-device intelligence are expected to further strengthen AR’s role across surgery, diagnostics, and medical training environments.

Regional Insights

North America Medical Smart Glasses Market Trends

North America is expected to lead, accounting for approximately 40% of the global medical smart glasses deployments, supported by advanced healthcare infrastructure, concentrated R&D investment, and favorable regulatory pathways. Mature digital ecosystems, coupled with NIH-backed R&D funding and early integration of AR-assisted surgical workflows, reinforce structural advantages, while competitive intensity among established technology and specialized medical device firms drives continuous innovation in optics, displays, and clinical software. These factors collectively sustain North America’s dominance, creating ecosystem effects that reinforce institutional adoption and operational integration.

Regulatory rigor and capital concentration continue shaping adoption dynamics, with FDA engagement providing predictable commercialization timelines while AI-enabled device validation introduces additional complexity. Market differentiation increasingly relies on specialized clinical applications, integrated software platforms, and managed service models rather than hardware alone. Venture capital and institutional investment in immersive technologies further strengthen structural readiness, positioning the region to capture incremental demand across surgical, diagnostic, and training applications.

Europe Medical Smart Glasses Market Trends

Market growth in Europe is driven by harmonized regulatory frameworks, industrial maturity, and targeted digital health investments. The Medical Device Regulation (MDR) provides a structured approval pathway, ensuring clinical credibility and data protection compliance, which, while adding procedural complexity and incremental costs, reinforces trust and supports adoption across hospitals and specialty clinics. Aging demographics, government-backed funding for digital health modernization, and established manufacturing ecosystems collectively sustain demand for AR-enabled visualization tools, extending applications beyond healthcare into rehabilitation and training workflows. Fragmented competition, with leading suppliers holding moderate shares, drives differentiation through integrated cybersecurity and privacy-respecting solutions, creating structural advantages for compliant manufacturers.

MDR-mandated clinical validation and cybersecurity oversight shape time-to-market and product positioning, establishing barriers for non-compliant entrants while fostering adoption among institutions prioritizing regulatory alignment. Investment trends, including cross-border collaborations and sustainable medtech financing, further reinforce ecosystem development. These structural factors position Europe as a stable and strategically differentiated market, with growth contingent on continued regulatory adherence, industrial collaboration, and integration of secure, evidence-based AR applications.

Asia Pacific Medical Smart Glasses Market Trends

Asia Pacific is expected to be the fastest-growing regional market, currently accounting for approximately 22% of global medical smart glasses deployments, driven by rapid healthcare expenditure growth, expanding middle-class populations, and accelerating digital health initiatives. Structural cost advantages in manufacturing enable competitively priced solutions for price-sensitive markets while maintaining developer margins, and telemedicine expansion in rural regions reinforces demand for remote expertise-sharing tools. Government-backed digitalization programs and policy frameworks further support technology adoption, establishing the region as a strategic growth frontier with significant volume-driven potential.

Regulatory approaches across Asia Pacific remain heterogeneous, shaping commercialization timelines and operational strategy. China’s centralized approval process requires local partnerships and coordinated engagement, while India’s comparatively flexible framework facilitates faster market entry with streamlined clinical validation. Incentives for regional manufacturing and software localization enhance developer competitiveness, yet regulatory variability introduces structural complexity for cross-border deployment. These factors collectively position Asia Pacific as a high-velocity growth market, where adoption acceleration is contingent on navigating diverse approval pathways and leveraging policy-aligned infrastructure to capture expanding clinical and telemedicine-driven demand.

Competitive Landscape

The global medical smart glasses market is moderately concentrated, led by top players capturing nearly half of total revenue, with second-tier manufacturers holding around a third, and emerging companies sharing the remainder. Key competitors leverage advanced R&D, regulatory compliance, and established healthcare procurement relationships to maintain market influence. Barriers to entry remain high due to capital-intensive development and complex clinical integration requirements.

North America dominates adoption through advanced hospital systems, while Europe and Asia Pacific show growing uptake driven by technology integration and clinical innovation. Competitive strategies focus on AI-enabled clinical software, next-generation display technologies, and strategic partnerships, with consolidation expected as smaller players merge or exit to sustain market evolution.

Key Industry Developments:

- In September 2025, Vuzix partnered with Saphlux to develop full-color AR displays for surgical applications, accelerating surgical overlays with 4K resolution. This collaboration aimed to reduce eye strain during prolonged OR use and leveraged Vuzix’s waveguide expertise to achieve a 40% brighter display.

- In April 2025, Pixee Medical received FDA 510(k) clearance for AR navigation in Ambulatory Surgery Centers, enabling real-time navigation through smart glasses without bulky trackers. After securing $15M in funding, the company targeted 40% of outpatient procedures, with pilots demonstrating 25% efficiency gains.

- In March 2024, Seiko Epson launched medical-grade Moverio AR Glasses for sterile OR workflows, optimized for sterile operating rooms with high-resolution Si-OLED displays for real-time 3D overlays.

Companies Covered in Medical Smart Glasses Market

- Vuzix Corporation

- Meta

- Google LLC

- Microsoft

- Apple

- Essilor Luxottica SA

- Seiko Epson Corporation

- Sony Group Corporation

- Magic Leap Inc.

- Lenovo Corporation

- Lumus Ltd.

- Qualcomm Inc.

- Pixee

- XReal

Frequently Asked Questions

The global medical smart glasses market is projected to be valued at US$2.6 billion in 2026 and is expected to reach US$7.6 billion by 2033.

Adoption is increasing due to rising use of augmented and virtual reality in surgical visualization, expanding telemedicine platforms, and growing demand for real-time clinical decision support and workflow efficiency.

The medical smart glasses market is expected to grow at a CAGR of 15.9% between 2026 and 2033, supported by post-pandemic telehealth normalization and advancing AR integration.

The medical smart glasses market is segmented by technology into optic see-through, virtual retinal display, and projection-based. Optic see-through currently holds the largest share.

Key players include Vuzix Corporation, Meta, Google LLC, Microsoft, Apple, Essilor Luxottica SA, Sony Group Corporation, Magic Leap Inc., Lenovo Corporation, Seiko Epson Corporation, Qualcomm Inc., Pixee, and XReal.