- Semiconductor Materials & Components

- Calibration Services Market

Calibration Services Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Calibration Services Market by Calibration Type (Electrical Calibration, Flow Calibration, Temperature Calibration, Humidity Calibration, Pressure Calibration, Dimensional Calibration, Radio frequency Calibration, Vibration / Acoustic Calibration, Others), End-user, and Regional Analysis for 2026 - 2033

Calibration Services Market Size and Trends Analysis

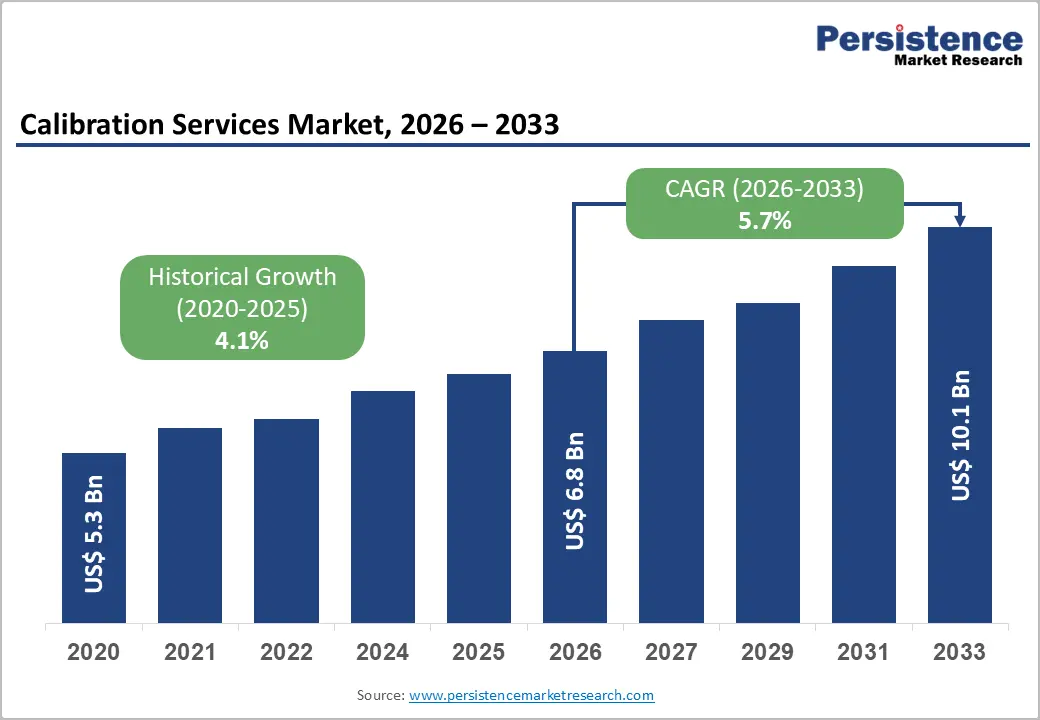

The global calibration services market is projected to reach US$6.8 billion in 2026 and US$10.1 billion by 2033. It is anticipated to grow at a CAGR of 5.7% from 2026 to 2033. The growing emphasis on preventive maintenance and equipment lifecycle optimization is driving the adoption of calibration services.

Rising awareness of product safety, environmental monitoring, and regulatory compliance further supports global demand. Industries increasingly prioritize operational accuracy and quality assurance, making calibration services essential for maintaining equipment performance and minimizing downtime across diverse applications.

Key Industry Highlights:

- Leading Calibration Type: Electrical calibration dominates with an over 25% share in 2026, valued at ~US$ 1.7 Bn, driven by growing adoption of automation, IoT, and advanced sensors that require precise voltage, current, and frequency measurements. Dimensional calibration is projected to exceed US$ 2.0 Bn by 2033. Radio frequency (RF) calibration is expected to grow at a CAGR of 8.7%, surpassing US$ 1.0 Bn by 2033, fueled by 5G/IoT expansion and increasing deployment of high-frequency electronics in aerospace, defense, and automotive sectors.

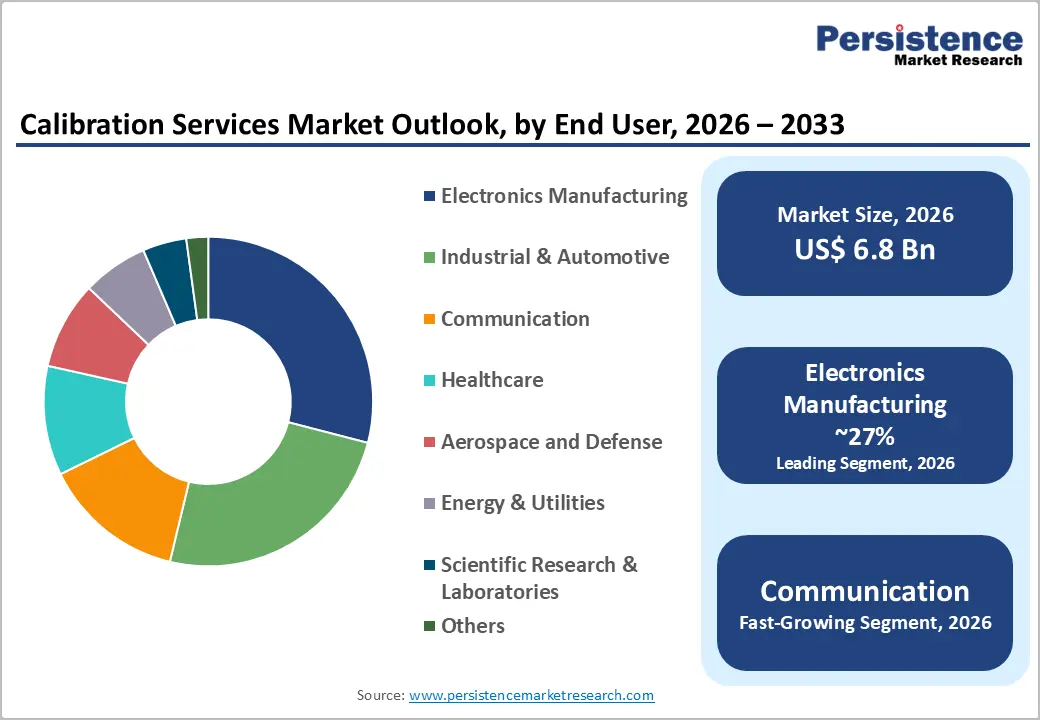

- Leading End-user: Electronics manufacturing accounts for over 27% of the market in 2026, valued at ~US$ 1.8 Bn, driven by high-precision requirements in semiconductor fabrication, PCB assembly, and quality control. The industrial and automotive sectors are projected to exceed US$ 3.0 Bn by 2033. The communication sector is growing at a CAGR of 9.1%, supported by 5G/6G network expansion. Healthcare follows at 6.4% CAGR due to precision medical equipment calibration.

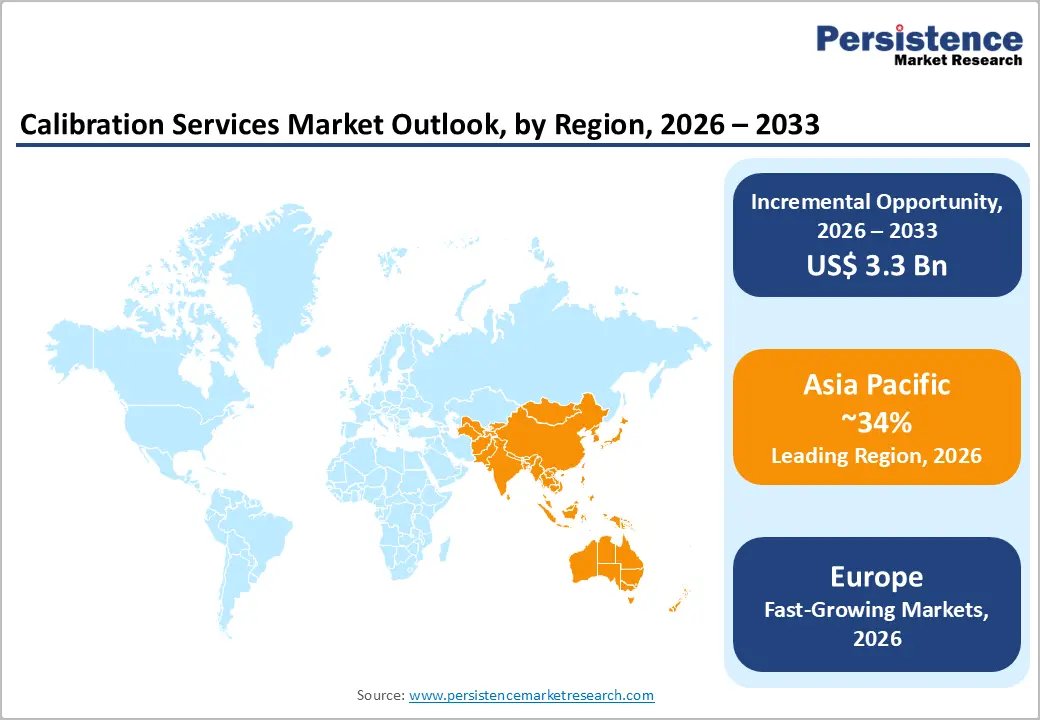

- Leading Region: North America is projected to grow at a CAGR of 5.4%. The U.S. dominates the region, projected to reach US$ 2.2 Bn by 2033, driven by aerospace spending, 5G deployment, and precision manufacturing.

- Fastest-Growing Region: Asia Pacific captures over 34% market share by 2026, projected to cross US$ 2.3 Bn. China is expected to reach US$ 800 Mn by 2026, and India is projected to grow at the highest CAGR of 9.7%. Europe is projected to reach over US$ 2.6 Bn by 2033, driven by regulatory harmonization, precision engineering, and industrial automation. Germany holds the largest share at over 21%, followed by the U.K., and France is expected to grow at a CAGR of 6.5%, surpassing US$ 350 Mn by 2033.

| Key Insights | Details |

|---|---|

|

Calibration Services Market Size (2026E) |

US$6.8 Bn |

|

Market Value Forecast (2033F) |

US$10.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Dynamics

Driver - Rising Focus on Preventive Maintenance and Equipment Lifecycle Management

Organizations are increasingly adopting preventive maintenance and predictive calibration strategies to reduce equipment downtime, extend asset lifecycles, and maintain product quality. Regular calibration ensures accurate measurements, optimizes efficiency, and minimizes waste, making it a cost-effective alternative to reactive repairs. Growing demand for such services is reflected in the Bureau of Labor Statistics' projected 5% employment growth for calibration technologists from 2024–2034. A 2025 audit showed only 20% of preventive maintenance and 35% of safety inspections for city vehicles were completed on time, underscoring the need for improved maintenance practices.

Stringent Regulatory Compliance and Quality Standards

Stringent regulatory compliance and quality standards across industries such as aerospace, healthcare, automotive, and manufacturing drive strong demand for calibration services. Organizations must adhere to regulations from bodies such as the FDA, FAA, ISO, and EASA, ensuring measurement instruments are accurate and traceable to national standards. Compliance with ISO 13485 for medical devices, AS9100 for aerospace components, and ISO 9001 across the EU is mandatory, with non-compliance leading to costly product recalls, penalties, and operational shutdowns. Growing emphasis on product safety, environmental protection, and precision manufacturing further reinforces the need for professional calibration to maintain business continuity.

Increased Focus on Product Quality & Traceability

Manufacturers are under growing pressure to ensure measurement accuracy to meet stringent quality standards and reduce defects. Traceability requirements mandate that measurement results be linked to national or international standards, making regular calibration essential. In sectors such as pharmaceuticals, aerospace, automotive, and electronics, even minor measurement deviations lead to product recalls, safety risks, or regulatory non-compliance. Globalized supply chains require uniform measurement standards across multiple locations, increasing reliance on accredited calibration providers. Together, these position calibration services are a critical enabler of quality assurance and transparent, auditable manufacturing processes.

Restraint - Capital-Intensive Operations and Pricing Pressures

High equipment and technology costs pose a significant barrier, as advanced instruments, environmental chambers, and calibration standards require substantial capital investment. Smaller service providers and in-house programs often struggle to match these capabilities. Rapid technological advancements necessitate ongoing investment in equipment upgrades and staff training. Intense competition and customer price sensitivity, especially for commoditized services, force providers to balance cost reductions with maintaining quality and compliance, limiting profitability and investment capacity.

Opportunity - Digital Calibration Solutions and Remote Services

The integration of IoT, AI, and cloud-based calibration management systems is transforming the delivery of calibration services. Remote calibration, predictive maintenance algorithms, and automated workflows enhance efficiency, reduce downtime, and lower operational costs. Cloud-based platforms enable real-time monitoring, automated scheduling, and comprehensive analytics, providing data-driven, value-added services. These technological advancements allow providers to differentiate themselves, improve customer outcomes, and create new revenue streams. In industries such as energy, AI-driven predictive maintenance and digital calibration help ensure equipment reliability, operational stability, and the effective integration of renewable energy sources.

Expanding Calibration Services in High-Precision Industries

The rise of technologies such as renewable energy systems, electric vehicles, and advanced medical devices is driving demand for specialized calibration services. These industries require precise measurements, unique expertise, and specialized equipment, often commanding premium pricing. Growing emphasis on environmental monitoring, food safety, and pharmaceutical manufacturing creates niche opportunities for providers with specialized capabilities. Calibration service companies capitalize on this demand through strategic partnerships with equipment manufacturers, industry associations, and regulatory bodies. Collaboration with technology providers can further foster innovative solutions and extend market reach.

Category-wise Analysis

Calibration Type Insights - Electrical Calibration Driving Accuracy and Reliability

Electrical calibration is expected to account for more than 25% share in 2026 and surpass the value of US$ 1.7 bn due to the rising dependence on electronic and digital measurement instruments that require high accuracy and stability. The growing adoption of automation, IoT devices, and advanced sensors increases the need for precise measurements of voltage, current, resistance, and frequency. Regular calibration ensures compliance with stringent quality and safety standards, reduces downtime, and maintains operational accuracy in critical applications. Dimensional calibration is expected to exceed US$ 2.0 Bn by 2033.

Radio frequency calibration is expected to grow at a CAGR of 8.7% and surpass US$ 1.0 Bn by 2033, driven by the expansion of wireless technologies, including 5G, IoT, and satellite communications. Global 5G connections surpassed US$ 2 billion in 2024, reflecting 48% year-over-year growth. The deployment of connected devices, base stations, and high-frequency electronics requires precise RF calibration to ensure signal reliability, minimize interference, and comply with regulatory standards. Advanced aerospace, defense, and automotive radar systems further drive demand for accurate RF testing.

End-user Insights - Electronics Manufacturing Driving High-Precision and Standard-Compliant Calibration Solutions

Electronics manufacturing is expected to account for over 27% share in 2026 and exceed US$ 1.8 Bn in value due to its critical need for high measurement accuracy, consistency, and compliance in component production and testing. Precision calibration ensures the reliability of instruments used in semiconductor fabrication, PCB assembly, and quality control. The increasing complexity of modern electronic devices, from smartphones to industrial automation control systems, drives the need for extensive calibration of testing equipment to ensure performance and compliance with standards such as ISO/IEC 17025. The industrial & automotive sector is expected to surpass US$ 3.0 Bn in value by 2033.

Communication is expected to grow at a CAGR of 9.1% due to rapid 5G/6G network expansion, increasing deployment of RF- and microwave-intensive equipment, and the need for frequent, high-precision calibration to ensure signal integrity and regulatory compliance. Healthcare is expected to grow at a CAGR of 6.4% due to the critical need for precision and reliability in medical equipment. Increasing adoption of advanced diagnostic, therapeutic, and monitoring devices requires regular calibration to ensure patient safety and regulatory compliance. The proliferation of digital and connected medical devices drives the need for specialized calibration services for imaging systems, monitoring devices, and portable diagnostic instruments.

Regional Insights

North America Calibration Services Market Trends

North America calibration services market is projected to grow at a CAGR of 5.4%, with the U.S. leading the region and expected to reach over US$2.2 Bn by 2033. Stringent regulatory frameworks, advanced industrial infrastructure, and significant R&D investment across sectors drive growth. Key factors include robust aerospace and defense spending, widespread medical device adoption, 5G deployment, and precision manufacturing requirements. The presence of major service providers, equipment manufacturers, and accreditation bodies such as NIST ensures high service quality, compliance, and continued technological advancement, giving North America a competitive edge.

Asia Pacific Calibration Services Market Trends

Asia Pacific is expected to capture over 34% of the calibration services market by 2026 and exceed US$ 2.3 Bn, driven by rapid industrialization, manufacturing expansion, and strong R&D investment. China is expected to reach a market value of over US$ 800 Mn by 2026, whereas India is expected to grow at the highest CAGR of 9.7%. Countries such as Japan, China, India, and Malaysia are seeing major expansions among service providers, with companies such as Tektronix setting up new calibration laboratories. The region benefits from skilled technical personnel, lower operational costs, and government support, while growing adherence to international quality standards and export requirements fuels demand. Expanding telecommunications infrastructure, including Thailand's 91% 5G coverage in 2024, creates strong demand for RF and electronic calibration, supported by high R&D spending in Japan at 66.9% of GDP and in China at 49.3%.

Europe Calibration Services Market Trends

Europe’s calibration services market is projected to reach over US$ 2.6 billion by 2033, driven by its regulatory harmonization, precision engineering traditions, and industrial automation focus. Germany holds the largest share at over 21%, followed by the U.K., and France is expected to grow at a CAGR of 6.5% and surpass the value of US$ 350 Mn by 2033. The region’s emphasis on environmental sustainability and energy efficiency opens opportunities in renewable energy and environmental monitoring applications, while IoT-enabled and remote calibration services support digitization and automation. With over 259 million registered passenger cars in 2024, a 5.9% increase since 2019, and 255+ automotive plants across Europe, the automotive sector remains a key driver, complemented by robust growth in manufacturing, healthcare, and energy sectors.

Competitive Landscape

The global calibration services market is moderately fragmented, with numerous regional and specialized providers competing alongside established multinational firms. Companies are focusing on expanding service portfolios across multiple instrument types and industries to strengthen market presence. Strategic initiatives include accreditation enhancements, automation integration, and partnerships with OEMs to ensure precision and compliance. Many players are also investing in digital calibration management platforms and on-site services to enhance customer convenience and retention.

Key Industry Developments

- In August 2025, WIKA Instruments acquired Godrej & Boyce’s calibration services business to expand its service portfolio and strengthen market presence. The acquisition combines Godrej’s local expertise with WIKA’s global capabilities, enabling customers to access a comprehensive range of high-quality and reliable calibration solutions.

- In August 2025, Transcat, Inc. acquired Essco Calibration Laboratory for $84 million in cash, effective August 5, 2025. The deal is backed by Transcat’s new $150 million syndicated credit facility led by M&T Bank and Wells Fargo, with customary adjustments and holdback provisions.

- In May 2025, Trescal partnered with Pickering Interfaces to become its authorized calibration service provider across the U.S. The collaboration enables faster turnaround times, reduced shipping costs, and ISO/IEC 17025-accredited support for Pickering’s products, enhancing service efficiency and customer satisfaction.

Companies Covered in Calibration Services Market

- Keysight Technologies

- Trescal Inc.

- Rohde & Schwarz

- ABB Ltd

- Endress+Hauser

- Tektronix

- TUV SUD

- Fluke Corporation

- Testo

- Hexagon

- VIAVI Solutions Inc

- Others

Frequently Asked Questions

The global market is projected to be valued at US$6.8 Bn in 2026.

The need for precise measurements, reliable equipment performance, and adherence to regulatory standards is a key driver of the market.

The calibration services market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Advancements in digital technologies are creating opportunities for remote, data-driven calibration services that enhance efficiency and reduce downtime.

Keysight Technologies, Trescal Inc., Rohde & Schwarz, ABB Ltd, Endress+Hauser, and Tektronix are among the leading key players.