- Marine

- Marine Vessel Market

Marine Vessel Market Size, Share, and Growth Forecast, 2025 - 2032

Marine Vessel Market By Vessel Type (Cargo Vessels, Passenger Vessels, Others), Application (Commercial Shipping, Military Operations, Recreational Boating, Others), Propulsion Type (Diesel-powered, LNG-powered, Hybrid-Electric, Others), and Regional Analysis for 2025 - 2032

Marine Vessel Market Share and Trends Analysis

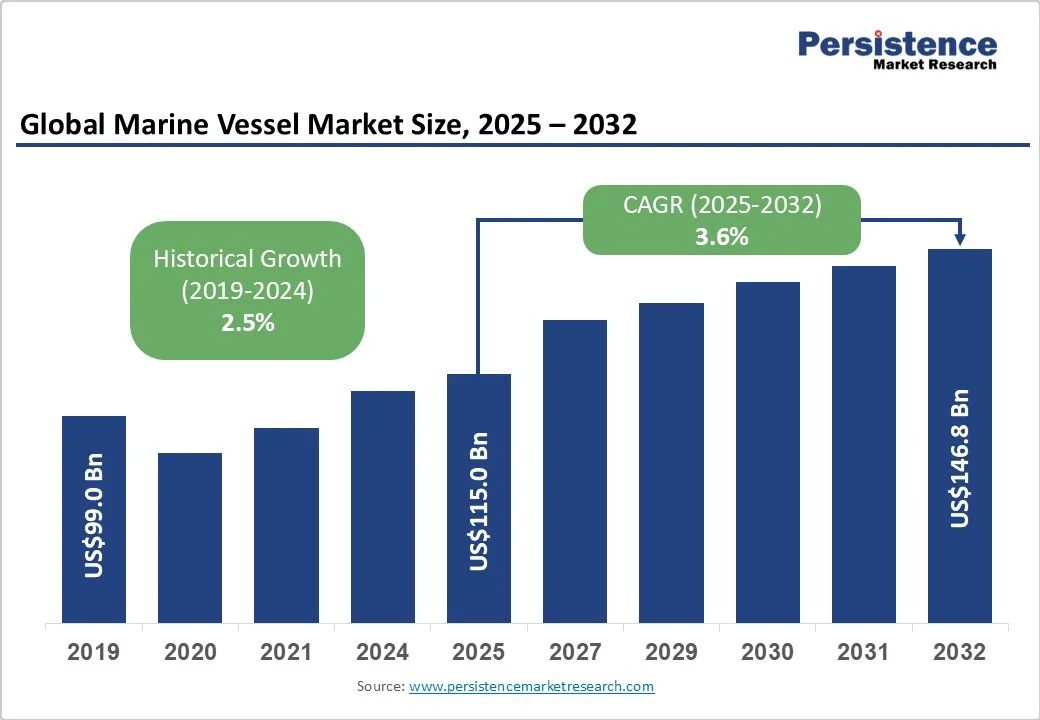

The global marine vessel market size is likely to be valued at US$115 Billion in 2025, and is estimated to reach US$146.8 Billion by 2032, growing at a CAGR of 3.6% during the forecast period 2025−2032, underpinned by expanding global trade volumes, accelerating fleet replacement cycles, and increasing investments in sustainable propulsion technologies.

Key drivers include stricter emissions regulations driving demand for alternative fuels, rising naval defense budgets, and growing offshore energy and tourism sectors. Success hinges on aligning fleet renewal with green propulsion and focusing on high-growth segments such as offshore services and hybrid vessels.

Key Industry Highlights

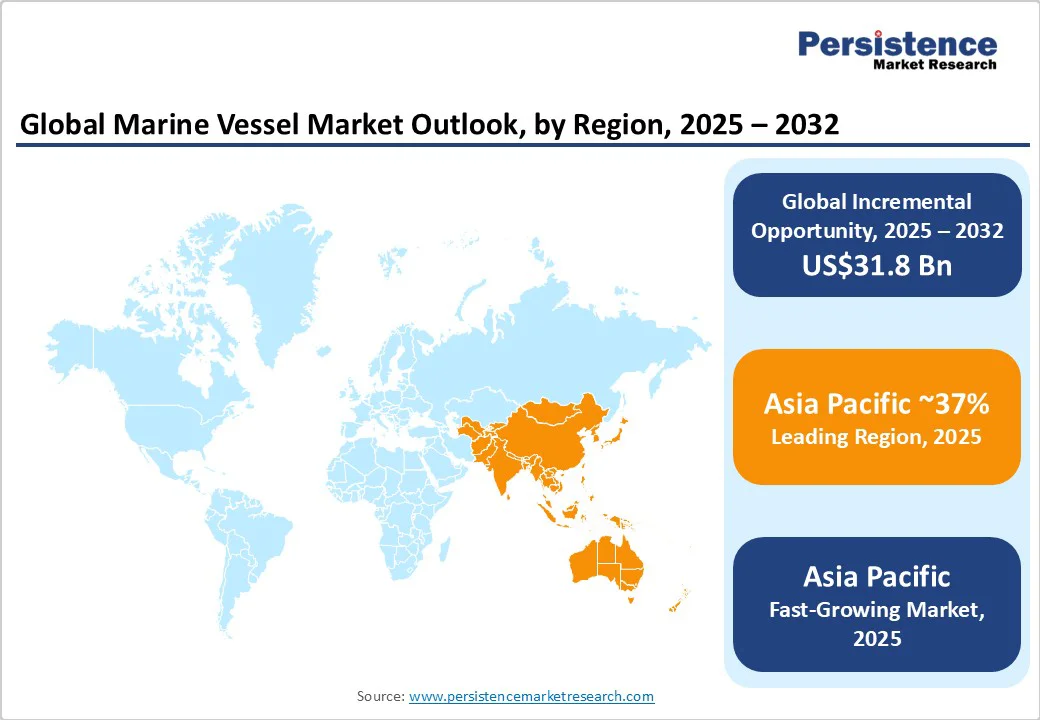

- Dominant Region & Fastest-growing Regional Market: Asia Pacific is likely to dominate in 2025 with around 38% share, and is expected to grow the fastest through 2032.

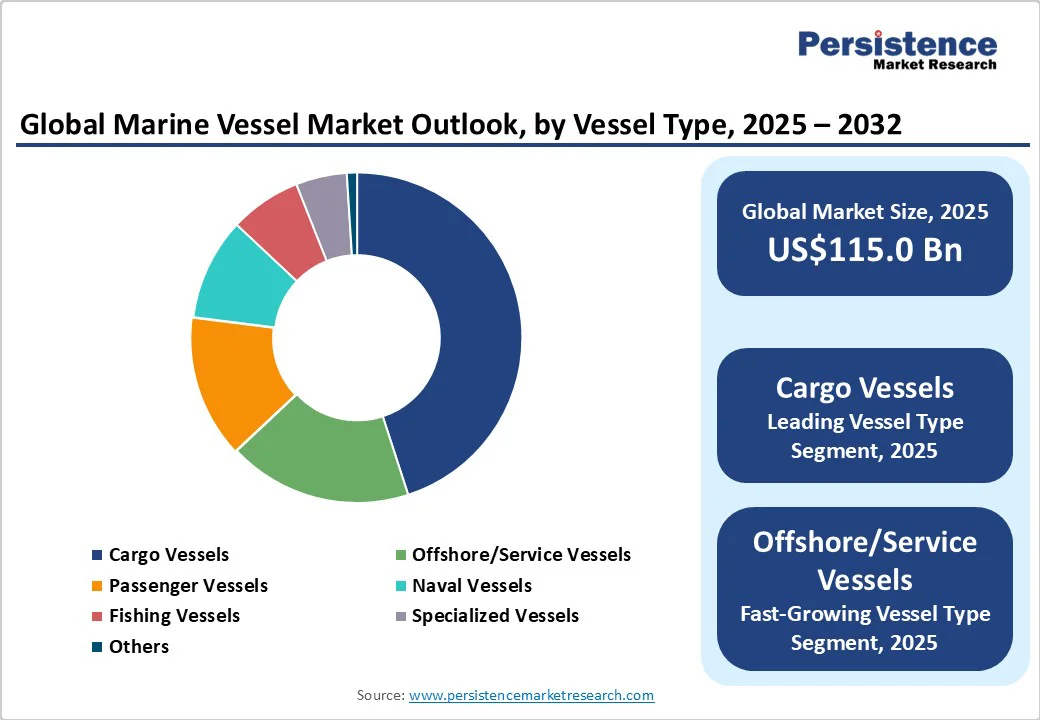

- Leading & Fastest-growing Vessel Types: Cargo vessels are estimated to hold the largest share of approximately 40%, while offshore/service vessels are poised for the fastest growth from 2025 to 2032.

- Leading Propulsion Type: Diesel-powered systems are set to dominate in 2025, supported by mature supply chains and fuel logistics; hybrid-electric systems are forecast to register the highest growth, driven by emissions regulations and fuel flexibility demands.

- Strategic Developments: Major methanol vessel orders, joint ventures, vertical integration via acquisitions, and shore-power infrastructure partnerships.

- September 2025: Hapag-Lloyd and DHL Global Forwarding signed a three-year agreement to reduce Scope 3 greenhouse gas emissions by purchasing emission reductions from sustainable marine fuels used in Hapag-Lloyd’s shipping operations.

| Key Insights | Details |

|---|---|

|

Marine Vessel Market Size (2025E) |

US$115 Bn |

|

Market Value Forecast (2032F) |

US$146.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Decarbonization Mandates & Emissions Targets

Governments and maritime regulators, led by the International Maritime Organization (IMO), are tightening emissions standards to accelerate the sector’s decarbonization. In April 2025, the IMO adopted a Net-Zero Framework mandating alignment of both new and existing vessels with 2050 decarbonization targets. Regional policies, such as the EU’s FuelEU Maritime initiative and the upcoming IMO carbon levy (expected by 2028), introduce escalating compliance costs for high-emission vessels. These regulatory pressures are compelling ship-owners to invest in cleaner propulsion technologies, particularly LNG and hydrogen, well before their fleets risk obsolescence. Dual-fuel and hybrid-capable vessels are becoming the norm in new orders as ship-owners hedge against future carbon penalties. Reuters forecasts that LNG bunkering demand could more than double by 2030, reinforcing this transition.

Global freight trade is set to expand, fueled by cross-border manufacturing, energy commodity flows, and supply chain regionalization. With over 80% of global merchandise trade moving by sea, rising trade volumes are directly boosting demand for container and cargo vessels. The offshore energy sector, both oil & gas and wind, is driving demand for specialized vessels such as dynamic positioning ships, crew transfer vessels, and cable layers. As offshore infrastructure expands, so too does the need for complex, service-oriented vessel builds.

High Capital & Lifecycle Cost Barriers

Marine vessels are capital-intensive assets with large upfront costs, long depreciation cycles, and significant maintenance expenses. Transitioning to novel propulsion, such as hybrid electric, often requires higher capital expenditures (CAPEX) and retrofitting costs. The incremental premium for dual-fuel or hybrid systems can range 10% to 20% above conventional diesel builds, depending on scale and fuel compatibility complexity. Several smaller ship-owners, especially in emerging markets, are constrained from absorbing these premiums.

Financing structures and risk profiles for experimental propulsion may deter lenders or raise interest spreads. In an environment of interest rates volatility, this cost sensitivity becomes a structural drag, delaying adoption in price-sensitive segments. Lifecycle operating costs are uncertain for alternative fuels, marred by fuel price volatility, bunkering availability, and infrastructure reliability add risk. If the fuel cost arbitrage or regulatory incentives do not materialize as projected, ship-owners may face stranded assets or under-utilized technology investments, spiking the total cost of ownership (TCO).

Retrofit & Repowering Market for Legacy Fleets

A significant share of the global marine fleet is aging and nearing midlife, opening a sizable retrofit and repowering market. To extend vessel life while meeting tightening emissions regulations, many ship-owners are exploring modular upgrades such as LNG conversion kits and hybrid battery assist systems. Industry estimates indicate that 20% to 30% of the active fleet could be retrofit-eligible between 2025 and 2032. This creates a tangible opportunity for OEMs, engineering firms, and retrofit integrators to offer turnkey solutions. A compelling model involves fuel conversion-as-a-service, bundling performance guarantees, financing, and end-to-end lifecycle support. First movers who standardize modular kits, build classification expertise, and establish global service networks will be well positioned to secure retrofit contracts and build long-term customer relationships. Retrofitting also strengthens the aftermarket revenue base, supporting business resilience amid newbuild market fluctuations.

While conventional cargo vessels tend to adopt new technologies cautiously, niche segments, such as coastal ferries, inland passenger vessels, and luxury cruise yachts, are leading adopters of hybrid, electric, methanol, hydrogen, or fuel-cell systems. These vessels typically operate on fixed or return-to-base routes, ideal for charging or refueling. In regions, including Scandinavia and the Mediterranean, policy mandates and port electrification are accelerating demand for zero-emission passenger vessels.

Category-wise Analysis

Vessel Type Insights

In 2025, cargo vessels are expected to command the largest share, approximately 40% of total market value, owing to their dominance in global trade, high throughput, and frequent replacement cycles. Cargo vessels also benefit from scale economies, standardization, and global routes, making them the backbone of the marine vessel segment. As bulk and container shipping account for the majority of global marine freight, most vessel ordering activity is concentrated in these classes.

Between 2025 and 2032, the fastest-growing vessel types are likely to be offshore/service vessels/specialized vessels, fueled by accelerating offshore wind farm buildouts, subsea infrastructure expansion, such as undersea cables and carbon capture pipelines, and marine energy projects. In addition, specialized vessels, such as cable-layers and dredgers, demand higher customization, leading to greater margin potential. The confluence of energy transition policies and infrastructure spending is driving strong demand in these niche high-velocity segments. Shipyards and investors can prioritize capacity specialization, modular templates, and value-added systems, such as automation and station-keeping, to capture this growth.

Propulsion Type Insights

Conventional diesel-powered propulsion is set to remain dominant, with an estimated 63% of the marine vessel market revenue share in 2025. Diesel engines are well-understood, widely available, and supported by mature supply chains and fuel logistics. Many ship-owners remain risk-averse to newer propulsion systems until alternatives demonstrate clear TCO advantages and regulatory certainty.

From 2025 to 2032, hybrid-electric propulsion systems are the fastest-growing, driven by emissions regulation, fuel flexibility demands, and incentives/subsidies in certain jurisdictions. LNG dual-fuel adoption is projected to double bunkering demand by 2030. As component costs decline and certification frameworks mature, these propulsion types will steadily erode the dominance of diesel, especially in mid-sized vessels and retrofits. OEMs must develop modular hybrid platforms, integrate advanced control systems, and engage in strategic fuel supply partnerships to stay competitive.

Application Insights

Among applications, commercial shipping, which includes cargo transport, bulk, container, and tanker, is projected to represent around 55% of total market value, consistent with the dominance of trade-driven vessel demand. The high throughput, replacement cycles, and capital investment capacity of the commercial sector ensure it remains the backbone of the marine vessel application landscape.

Offshore oil & gas, renewable energy support, and service applications are expected to register the highest CAGR of approximately 7% through 2032. Renewable-energy investment, especially offshore wind, is surging globally, and subsea infrastructure deployment requires specialized vessels. The demand for search & rescue, research, and survey vessels is increasing with marine science funding, climate monitoring, and climate adaptation projects.

Regional Insights

Asia Pacific Marine Vessel Market Trends

In 2025, Asia Pacific is projected to be the largest regional market, accounting for approximately 37% of global market share, fueled by the shipbuilding powerhouses of China, Japan, and South Korea, alongside the rapidly expanding industries in India and Southeast Asia. The region also leads in growth, driven by rising intra-Asia trade, infrastructure upgrades, and expanding shipyard capacity.

China is a dual leader in demand and supply, propelled by its domestic shipping modernization, Belt and Road maritime corridors, and push for green propulsion. South Korea remains dominant in large container ships and LNG carriers, while Japan excels in niche, high-tech vessels. Taiwan also plays a strategic role in propulsion system development. India is accelerating with new shipyard incentives, coastal trade initiatives, and a growing retrofit market. Meanwhile, Southeast Asia’s focus on ferry upgrades and intra-regional logistics is boosting demand for service and passenger vessels.

Regional shipyards are actively investing in hybrid-ready platforms, modular construction techniques, and advanced lightweight materials. Global OEMs and shipbuilders increasingly base operations in Asia to benefit from scale, cost efficiencies, and proximity to demand. Capital is flowing into megayards and local propulsion manufacturers to strengthen Asia’s role as the world’s marine vessel production and innovation hub.

Europe Marine Vessel Market Trends

Europe is projected to capture approximately 24% of the market by 2025, underpinned by its strong shipbuilding heritage, robust maritime ecosystem, and proactive regulatory environment. The rising demand for green vessel retrofits and offshore wind service vessels is driving market growth. European shipbuilders, particularly in Germany, the U.K., France, and Spain, lead in specialized vessel segments, including cruise ships, ferries, and offshore service vessels.

Regulatory harmonization through EU-wide emissions mandates, such as Fit-for-55, the Emissions Trading System (ETS), and FuelEU Maritime, is accelerating fleet modernization. These policies, combined with national incentives in countries including Norway and Denmark, are spurring early adoption of low-emission technologies. Germany and the Netherlands are key propulsion and systems hubs, while the U.K. benefits from offshore wind expansion. Spain and France remain strong in cruise and ferry construction.

European yards are actively investing in fuel-cell systems, methanol engine retrofits, and modular green vessel designs. Partnerships between OEMs and shipbuilders are fostering innovation, while infrastructure development, such as expanded bunkering facilities in Rotterdam, Hamburg, and Gothenburg, supports alternative fuel uptake. These strengths position European players well to secure retrofit and newbuild contracts.

North America Marine Vessel Market Trends

Led by the U.S., North America is likely to account for a share of about 18% of the marine vessel market. U.S. naval modernization, offshore wind infrastructure, and coastal vessel replacement will support continuous demand. The U.S. is the primary driver, with defense spending on naval vessels, the Jones Act, and offshore wind lease zones stimulating demand. Canada and Mexico contribute via coastal shipping, oil & gas service vessels, and small-scale ferry/utility builds. The U.S. also enforces strict emissions legislation, including the Environmental Protection Agency (EPA) maritime fuel rules and state-level port electrification mandates.

The Inflation Reduction Act also provides subsidies and tax credits for clean energy and offshore wind infrastructure, indirectly supporting green vessel demand. Major U.S. and Canadian yards are competing to supply hybrid and dual-fuel vessels, often in partnership with propulsion OEMs, such as GE Marine and Rolls-Royce. Investment is being channeled toward small- to medium-shipyards upgrading capabilities for hydrogen/hybrid builds, and port bunkering infrastructure expansions on both coasts. The strategic opportunity lies in retrofitting government and coastal fleets and pioneering zero-emission vessels for short-sea applications.

Competitive Landscape

The global marine vessel market exhibits a moderately consolidated structure, featuring specialized and regional shipyards and system integrators. The top players control around 35% of market revenue, benefiting from scale, integrated capabilities, global service networks, and advanced R&D. Meanwhile, many niche yards and retrofit integrators operate regionally or by vessel type specialization.

Even though barriers to market entry are high due to capital intensity and technological complexity, opportunities for differentiation, such as in the green propulsion space, are available for nimble players. Competitive positioning centers on innovation, fuel-agnostic platforms, modular systems, and aftermarket service networks. Players that can integrate vessel design, propulsion, digital systems, and financing will enjoy a competitive moat.

Key Industry Developments

- In October 2025, Swiss marine power firm WinGD announced the launch of its first ethanol-fueled two-stroke engine, set for 2026, with deliveries starting in 2027 for both newbuilds and retrofits. Based on its methanol-powered X-DF-M platform, the engine uses diesel-cycle combustion optimized for ethanol’s higher energy density. It offers a low-carbon alternative for ship-owners, aligning with emission regulations and backed by partnerships with ship-owners, ethanol suppliers, and the Global Ethanol Association.

- In June 2025, HD Hyundai’s subsidiary, HD Korea Shipbuilding & Offshore Engineering, unveiled Korea’s first Modular Multilevel Converter (MMC) high-pressure propulsion drive for electric vessels. Verified onshore in 2024, the system enhances motor control and power quality while cutting size and weight by over 20%. Set for commercialization by 2027, the innovation supports Korea’s ship electrification goals and positions HD Hyundai among the few global leaders in advanced electric propulsion.

- In April 2025, Viking and Fincantieri unveiled the world’s first hydrogen-powered cruise ships, Viking Libra and Astrea, set for delivery in late 2026 and 2027. Viking Libra, a 54,300 GT vessel with 499 staterooms, will feature liquefied hydrogen fuel cells generating up to 6?MW of zero-emission power, ideal for accessing environmentally sensitive regions. The project marks a strategic push toward zero-emission cruising, with more hydrogen-powered ships planned through 2031.

Companies Covered in Marine Vessel Market

- China State Shipbuilding Corporation (CSSC)

- Hyundai Heavy Industries (HHI)

- Daewoo Shipbuilding & Marine Engineering (DSME)

- Samsung Heavy Industries

- Fincantieri S.p.A.

- Meyer Werft GmbH & Co. KG

- STX Offshore & Shipbuilding

- Wärtsilä Corporation

- MAN Energy Solutions

- Rolls-Royce

- ABB Marine & Ports

- Mitsubishi Heavy Industries

- Kawasaki Heavy Industries

- Hyundai Mipo Dockyard Co., Ltd.

- Vard Marine

Frequently Asked Questions

The marine vessel market is projected to reach US$115 Billion in 2025.

Expanding global trade volumes, accelerating fleet replacement cycles, and increasing investments in sustainable propulsion technologies are driving the market.

The marine vessel market is poised to witness a CAGR of 3.6% from 2025 to 2032.

Rising modernization budgets for naval vessels, growth in offshore energy & tourism vessel demand, and alignment of fleet renewal programs with green propulsion transitions are key market opportunities.

China State Shipbuilding Corporation (CSSC), Hyundai Heavy Industries (HHI), and Daewoo Shipbuilding & Marine Engineering (DSME) are some of the key players in the marine vessel market.