- Industrial Automation

- Low Voltage Batteries Market

Low Voltage Batteries Market Size, Share, and Growth Forecast 2026 - 2033

Low Voltage Batteries Market by Battery Type (Li-ion, Lead Acid, Nickel Cadmium, Nickel Metal Hydride, Other), Application (Automotive, Consumer Electronics, Industrial Equipment, Energy Storage Systems, Other), End User (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Low Voltage Batteries Market Size and Trend Analysis

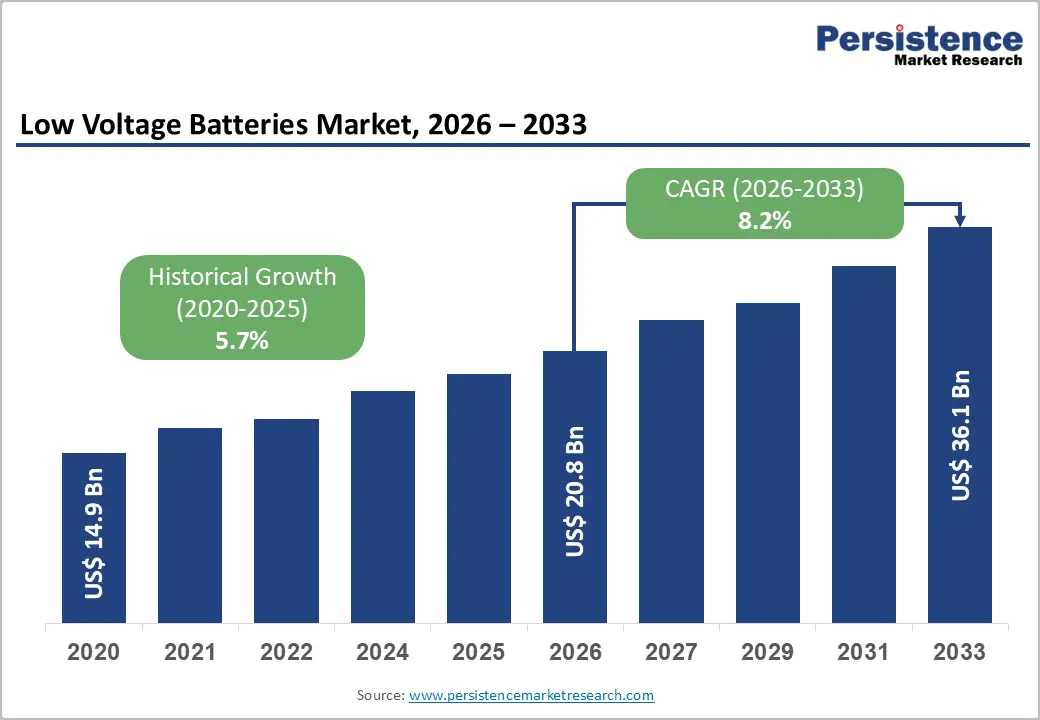

The global low voltage batteries market size is supposed to be valued at US$ 20.8 Bn in 2026 and is projected to reach US$ 36.1 Bn by 2033, growing at a CAGR of 8.2% between 2026 and 2033.

The market is propelled by the accelerating adoption of mild hybrid electric vehicles with 48V systems across North America, Europe, and Asia-Pacific regions, the expanding deployment of renewable energy storage systems requiring efficient battery solutions for grid stabilization, and rising demand for backup power infrastructure in telecommunications, healthcare, and industrial sectors. These drivers represent fundamental shifts in transportation electrification and energy infrastructure modernization, supported by increasingly stringent emission regulations and declining battery costs that have fallen below historical price benchmarks.

Key Market Highlights

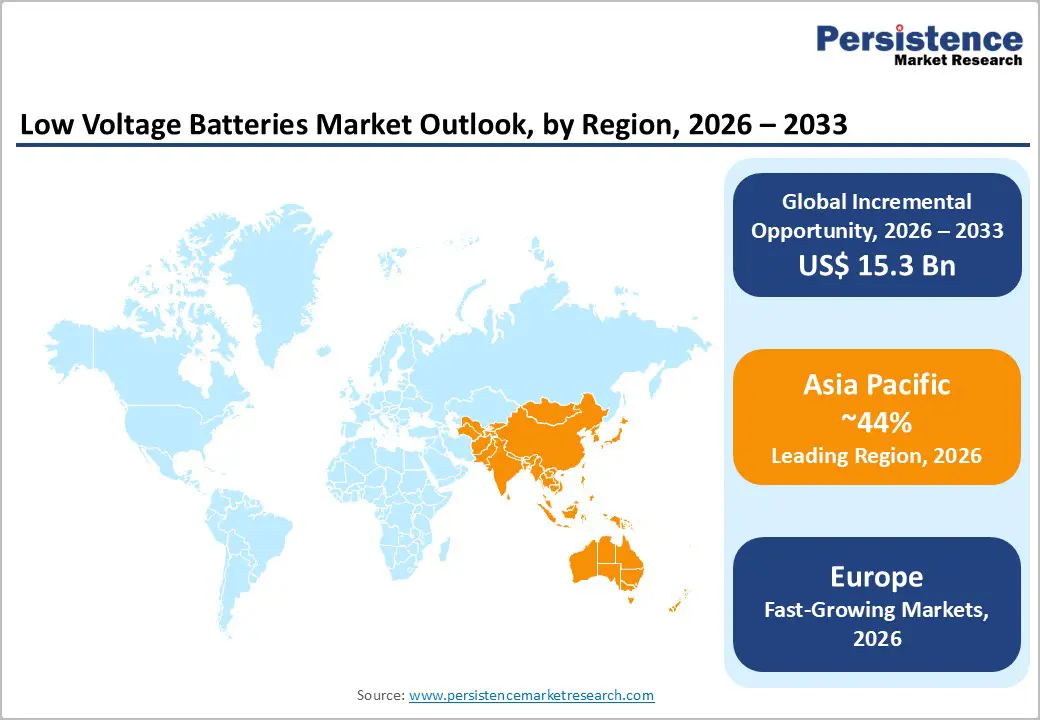

Leading Region: Asia-Pacific dominates the global low-voltage batteries market, accounting for over 60% of global manufacturing capacity and 44% of worldwide consumption, driven by China's integrated supply chains, manufacturing scale, and government EV incentives.

Fastest Growing Region: Europe represents the fastest-growing region for the low-voltage batteries market, with technological leadership and start-stop systems now standard on more than 80% of new vehicles in developed markets.

Dominant Segment: Lithium-ion batteries command a dominant market position with approximately 60% market share, driven by superior performance, declining costs, and lithium price reductions of 85% since the 2022 peaks.

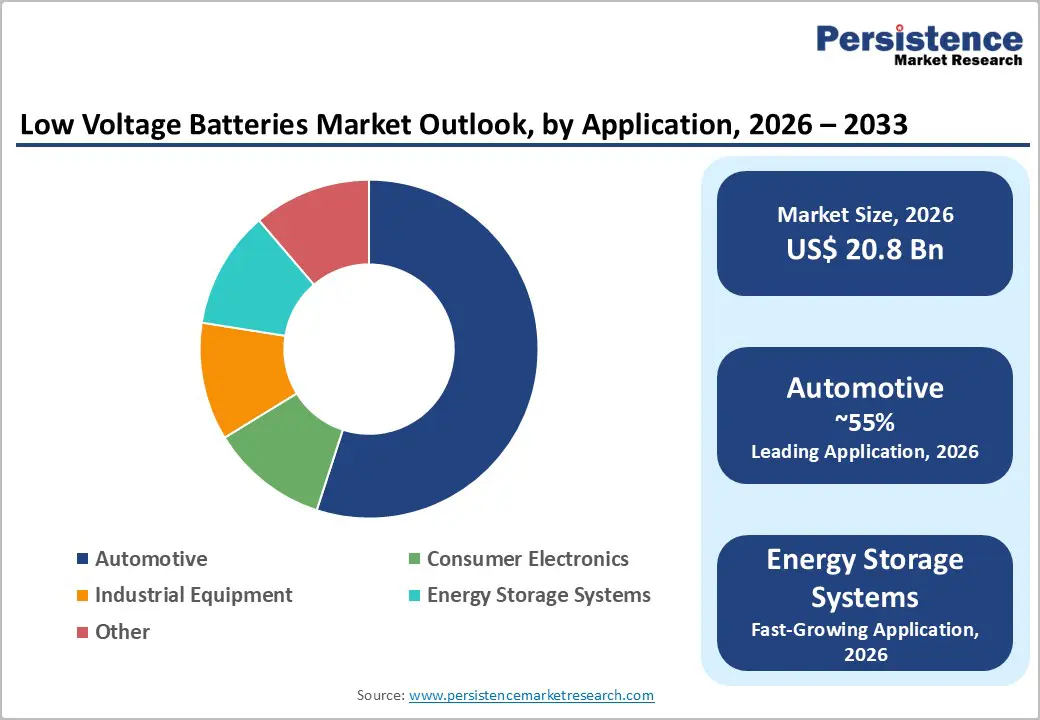

Fastest Growing Segment: Energy storage systems represent the fastest-growing application segment with 15.8% CAGR through 2030, fueled by grid modernization initiatives, renewable energy integration requirements, and residential adoption driven by solar-plus-storage system integration and consumer desire for energy independence.

Key Market Opportunity: Residential and distributed energy storage systems represent the primary opportunity, supported by government incentives, declining battery costs below $100 per kilowatt-hour, and smart battery management system integration enabling grid services participation.

| Key Insights | Details |

|---|---|

| Market Size (2026E) | US$ 20.8 Bn |

| Market Value Forecast (2033F) | US$ 36.1 Bn |

| Projected Growth CAGR (2026-2033) | 8.2% |

| Historical Market Growth (2020-2025) | 5.7% |

Market Dynamics

Market Growth Drivers

Electrification of Vehicle Powertrains and Mild Hybrid Adoption

The automotive industry is experiencing a significant transformation driven by the adoption of mild hybrid technology, which employs 48-volt battery systems to reduce fuel consumption by approximately 10–15% while offering a cost-effective alternative to full hybrid systems. In Europe, stringent emission regulations mandating a limit of 95 grams of CO? per kilometer have accelerated the widespread integration of start-stop systems, with Germany, France, and Italy achieving penetration rates exceeding 80% of new vehicles.

Similar regulatory measures in North America and China’s New Energy Vehicle policies are reinforcing this trend, creating substantial demand for low-voltage battery solutions. The mild hybrid vehicle production grew by more than 30% year-on-year in 2024, signaling sustained structural demand growth expected to continue throughout the forecast period as global electrification initiatives expand.

Surge in Renewable Energy Storage and Grid Modernization Initiatives

The global renewable energy sector is driving unprecedented demand for battery energy storage systems, with utility-scale installations projected to grow at an annual rate of 29% through 2030. In the United States, the Inflation Reduction Act is supporting over 20 GW of additional battery capacity, while Europe’s Green Deal Industrial Plan is accelerating grid modernization initiatives across member states.

According to IRENA, global battery storage capacity is expected to reach 1,200 gigawatt-hours by 2030, with lithium-ion technology accounting for more than 80% of deployments. The integration of renewable energy sources is creating critical requirements for backup power systems in both utility and commercial applications, positioning low-voltage battery solutions as indispensable components for achieving global decarbonization objectives.

Market Restraints

Rapid Manufacturing Capacity Expansion and Price Erosion

Global battery cell manufacturing capacity expanded by approximately 30% in 2024, reaching 3.3 terawatt-hours annually and creating substantial overcapacity compared to the actual demand of around 950 gigawatt-hours. This imbalance has intensified price competition, particularly in China, where battery prices fell nearly 30% during the year, making products more than 30% cheaper than European production and 20% below North American costs. As a result, market participants are facing significant margin compression, with established manufacturers leveraging economies of scale to maintain competitiveness, thereby limiting profitability for smaller players. Overcapacity is anticipated to persist through 2026–2027, prolonging downward price pressures and potentially delaying new capacity investments despite favorable long-term growth prospects.

Environmental Regulations and Raw Material Supply Constraints

The European Union has introduced stringent battery regulations mandating carbon footprint disclosure and supply chain transparency, significantly increasing operational complexity for manufacturers. Producers of lead-acid batteries face tightening environmental standards related to mining practices and recycling protocols, resulting in escalating compliance costs across developed markets. Despite recent price stabilization, concerns regarding raw material availability persist, such as lithium, cobalt, and nickel supplies remain geographically concentrated in regions vulnerable to geopolitical tensions.

Furthermore, manufacturing facilities are required to adhere to increasingly rigorous environmental compliance standards, necessitating substantial capital investments in advanced recycling infrastructure and emissions reduction technologies. These regulatory and supply chain challenges underscore the growing need for sustainable practices and strategic resource management within the global battery industry.

Market Opportunities

Emerging Energy Storage Systems for Distributed and Residential Applications

The residential and commercial energy storage sector is witnessing rapid expansion, with the rising solar energy storage battery market. Homeowners and small businesses are increasingly adopting behind-the-meter battery systems to reduce electricity costs and enhance energy resilience, supported by battery pack prices falling below $100 per kilowatt-hour, making residential installations economically viable.

Government incentives in regions such as Australia, Germany, and California are further accelerating adoption, while smart battery management systems are becoming standard, enabling grid services and demand response participation. This segment is anticipated to emerge as the fastest-growing application for low-voltage batteries through 2033, particularly in developed markets with mature solar infrastructure.

Electric Vehicle Two-Wheeler and Light Commercial Vehicle Segment Expansion

The electric two-wheeler market is witnessing exceptional growth, with India alone accounting for over 200 million units, creating significant demand for both replacement and new vehicles. Leading manufacturers are responding to this trend, with Exide Industries initiating lithium-ion cell production specifically for two-wheeler applications, while BYD and other global players are expanding dedicated production capacities.

Light commercial vehicles are also increasingly adopting electric powertrains, with Chinese manufacturers dominating this segment through cost-effective offerings. Regulatory initiatives, including subsidies and preferential licensing, are accelerating electric two-wheeler adoption across India, China, and Southeast Asia. This segment presents substantial volume opportunities for low-voltage battery suppliers, with projected growth rates expected to surpass those of mainstream automotive categories through 2033.

Category-wise Insights

Battery Type Analysis

Lithium-ion batteries have established a dominant position in the low-voltage battery market, accounting for approximately 60% of the total share due to superior performance characteristics and steadily declining costs. This transition from traditional lead-acid chemistry to lithium-ion solutions underscores a fundamental shift in automotive electrification, particularly for 48V mild hybrid systems and energy storage applications.

Among lithium-ion technologies, lithium iron phosphate (LFP) chemistry is gaining rapid traction, with penetration reaching nearly 50% of global EV battery sales in 2024, driven by enhanced safety, longer cycle life, and lower material costs compared to nickel-manganese-cobalt (NMC) alternatives. Advancements in battery management systems, thermal regulation, and safety features are accelerating adoption across automotive and stationary applications, supported by an 85% reduction in lithium material prices since the 2022 peaks.

Application Analysis

Automotive applications constitute the dominant segment of the global low-voltage batteries market, accounting for approximately 55% of total demand. This leadership is driven by mandatory adoption of start-stop systems and the increasing integration of mild hybrid electrification across vehicle platforms. The European Union’s stringent requirement of 95 grams of CO? per kilometer, along with tightening emission standards in North America and China, has made low-voltage battery solutions indispensable for conventional and hybrid powertrains.

Electric vehicle production surged by 25% in 2024 to reach 17 million units globally, with China contributing nearly 60% of total sales, necessitating substantial battery capacity. Rising regulatory compliance costs have rendered low-voltage battery integration economically unavoidable for automotive manufacturers, ensuring sustained demand growth. Additionally, consumer electronics, including smartphones, tablets, and wearables, represent a growing segment, supported by over 2.5 billion smartphones projected to be in use by 2025.

End-User Analysis

Commercial end-users constitute the largest segment of the low-voltage battery market, representing approximately 50% of the total market value. This segment includes industrial backup systems, data centers, and telecommunications infrastructure requiring an uninterrupted power supply. Telecom operators are increasingly transitioning from lead-acid to lithium-ion backup systems, driven by the expansion of 5G networks and the need for compact, maintenance-free solutions. Data centers, facing rising computational loads, are adopting advanced battery technologies to ensure seamless power continuity, while renewable energy developers are deploying battery systems at utility scale to support grid stability.

Residential applications are also gaining momentum through solar battery installations and home backup systems, with growth rates exceeding 25% annually in mature markets. Additionally, industrial equipment manufacturers are integrating low-voltage batteries into production systems, material handling, and automation equipment.

Regional Insights

North America Low Voltage Batteries Trends

North America represents a mature market characterized by a strong automotive heritage and advanced regulatory frameworks that drive low-voltage battery adoption. The U.S. automotive battery market is valued at approximately US$ 50–55 billion, with low-voltage solutions comprising a significant share. The U.S. vehicle fleet exceeds 280 million units, creating substantial replacement demand, while new production emphasizes 48V mild hybrid integration under CAFE emission standards.

The Inflation Reduction Act is catalyzing manufacturing expansion, with ten new battery plants expected by 2025, boosting capacity to 421.5 GWh annually, a 90% increase from 2024. Manufacturers are localizing production through partnerships with Panasonic, LG, Samsung SDI, and SK On. Additionally, start-stop system adoption is projected to grow at a CAGR of 14.7% through 2035, supported by regulatory harmonization across USMCA countries and robust aftermarket infrastructure.

Europe Low Voltage Batteries Trends

Europe remains the global leader in low-voltage battery technology adoption, with start-stop systems now standard on more than 80% of new vehicles in developed markets. Germany dominates regional production and consumption, accounting for approximately 28–29% of market share through its automotive manufacturing strength and leadership in 48V mild hybrid integration. EU regulations mandating 95 grams of CO? per kilometer by 2025 and tightening Euro 6/7 standards have made low-voltage battery solutions essential across vehicle platforms, driving structural demand growth independent of economic cycles.

AGM (Absorbent Glass Mat) and EFB (Enhanced Flooded Battery) technologies hold market leadership in start-stop applications, supported by premium pricing and superior performance. Additionally, France, the U.K., Italy, and Spain are advancing adoption through renewable energy initiatives, while Eastern Europe emerges as a cost-competitive manufacturing hub.

Asia Pacific Low Voltage Batteries Trends

Asia-Pacific is the dominant region for the market, accounting for over 60% of global battery manufacturing capacity and approximately 44% of worldwide low-voltage battery demand. China dominates the region through integrated supply chains, large-scale production, and strong government support, producing more than 70% of global lithium-ion batteries while maintaining cost advantages of 30–50% compared to other regions. Leading players such as BYD and CATL reinforce this dominance, with CATL’s production capacity exceeding 260 GWh annually and BYD achieving global EV sales leadership in 2024.

China’s New Energy Vehicle policies and dual-credit system have accelerated electrification, with NEV sales surpassing 9 million units in 2024. India is emerging as a critical growth market, supported by FAME-II and PLI schemes, while Japan, South Korea, and Southeast Asia strengthen regional competitiveness through technological leadership and cost-efficient manufacturing hubs.

Competitive Landscape

Market Structure Analysis

The global low-voltage battery market exhibits a consolidated competitive structure dominated by established manufacturers leveraging scale, technological leadership, and extensive distribution networks. In contrast, lead-acid battery markets remain fragmented, with regional players sustaining competitiveness via cost advantages and long-standing automotive relationships. Key industry participants such as LG Energy Solution, Panasonic, and Samsung SDI specialize in advanced lithium-ion technologies for automotive and energy storage applications. Market consolidation is accelerating through strategic acquisitions and backward integration by major automakers into battery production.

Key Market Developments

- December 2024: Stellantis and CATL establish €4.1 billion joint venture for Spanish lithium iron phosphate battery plant, targeting 50 GWh capacity by 2026 to support European EV production.

- November 2024: BYD announces next-generation Blade Battery launch in 2025, featuring enhanced lithium iron phosphate chemistry with improved safety and elimination of fire risk, strengthening competitive position in stationary storage applications.

July 2025: Panasonic Energy commences mass production at its new Kansas automotive lithium-ion battery factory with a targeted annual capacity of 32 GWh, marking a significant milestone in North American battery localization and supporting US electric vehicle manufacturers, including Tesla, and emerging partnerships with Zoox autonomous vehicles.

Top Companies in the Low Voltage Batteries Market

CATL (Ningde, China) maintains global market leadership through production capacity exceeding 260 gigawatt-hours annually and strategic partnerships with major automakers, including Tesla and BMW. The company has pioneered NCMA and LFP battery chemistries while establishing manufacturing facilities across China, Germany, and Indonesia.

BYD Company Limited (Shenzhen, China) operates as an integrated manufacturer combining vehicle production with battery manufacturing, achieving 2024 global EV sales leadership through competitive cost structures and vertical integration advantages. The company is pioneering lithium iron phosphate battery technology and solid-state battery development, with production capacity exceeding 115 gigawatt-hours annually across multiple facility locations.

LG Energy Solution (Seoul, South Korea) is expanding its global manufacturing footprint to 540 gigawatt-hours annual capacity through facilities in South Korea, Poland, the U.S., and China. The company specializes in advanced nickel-based lithium-ion chemistries while investing in solid-state battery development and pursuing strategic collaborations with General Motors and other major automakers.

Companies Covered in Low Voltage Batteries Market

- CATL

- Panasonic Corporation

- LG Chem/LG Energy Solution

- Samsung SDI

- BYD Company Ltd.

- Exide Industries

- GS Yuasa Corporation

- EnerSys

- C&D Technologies, Inc.

- East Penn Manufacturing Company

- SK On Co., Ltd.

- Gotion High-tech

- Honda Motor Co., Ltd.

- Tesla, Inc.

Frequently Asked Questions

The global low-voltage batteries market is valued at US$ 20.8 billion in 2026 and projected to reach US$ 36.1 billion by 2033, representing a CAGR of 8.2% during the forecast period.

The principal market drivers include mandatory adoption of 48-volt mild hybrid systems across automotive platforms to meet emission regulations, renewable energy storage expansion requiring lithium-ion solutions for grid stability, and increasing demand for backup power infrastructure across telecommunications, healthcare, and data center sectors.

Lithium-ion batteries account for approximately 60% of the global low-voltage battery market share, driven by superior performance characteristics, declining cost curves, and widespread adoption across automotive and energy storage applications.

Asia-Pacific dominates the global low-voltage batteries market, accounting for over 60% of global manufacturing capacity and approximately 44% of worldwide consumption. China leads regional production through integrated supply chains, manufacturing scale, government electrification policies, and cost advantages of 30-50% relative to Europe and North America.

The primary opportunities include residential and distributed energy storage systems, with the electric two-wheeler and light commercial vehicle segments experiencing explosive growth across India, China, and Southeast Asia.

Major market participants include CATL, BYD Company Limited, LG Energy Solution, Panasonic Corporation, Samsung SDI, Exide Industries, GS Yuasa Corporation, EnerSys, and C&D Technologies, maintaining a strong North American market presence.