- Advanced Materials

- Lithium Niobate Market

Lithium Niobate Market Size, Share, and Growth Forecast, 2026-2033

Lithium Niobate Market by Form (Powder, Ingot, Wafer, Others), Grade (Electron Grade, Agriculture Grade, Industrial Grade), Application (Electro-Optical Modulators, Acousto-Optical Filters, Quasi-Phase Matched Frequency Generation, Integrated Optical Devices, Wavefront Distortion, Acoustic Transducers), End-Use (Industrial, Aerospace, Defense, Telecommunication, Others), and Regional Forecast for 2026-2033

Lithium Niobate Market Share and Trends Analysis

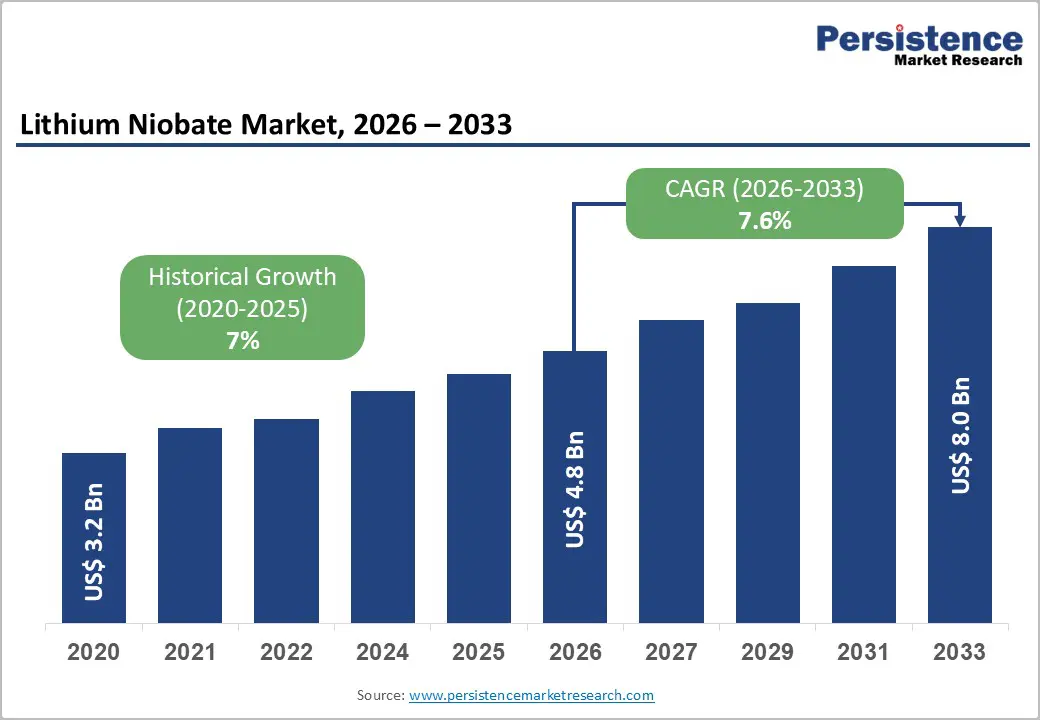

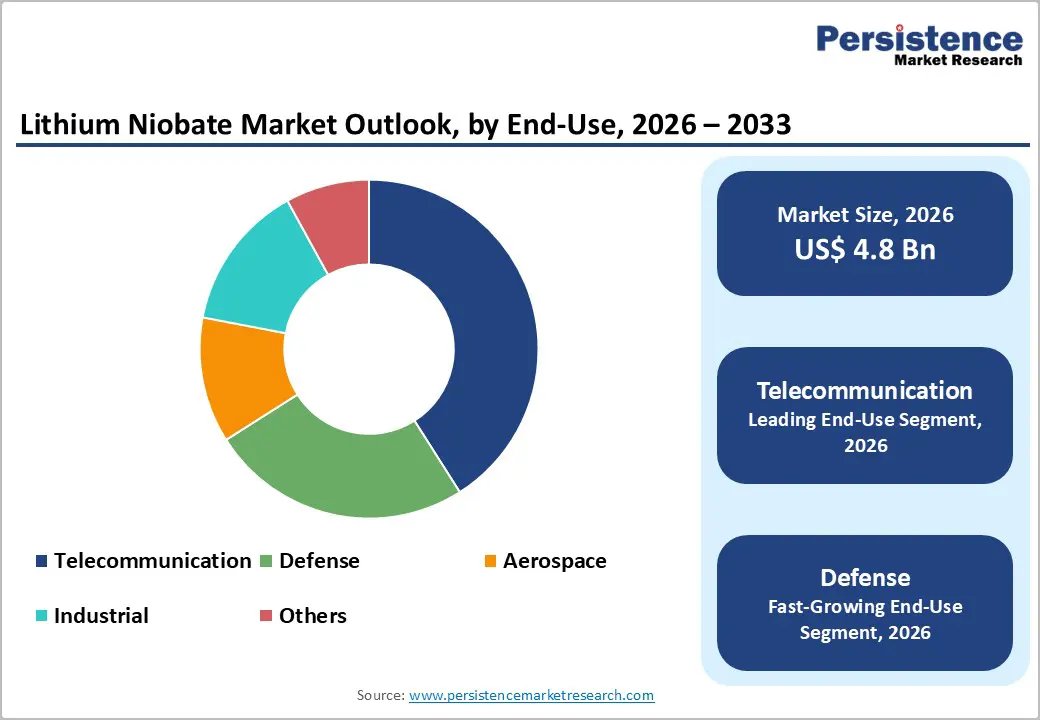

The global lithium niobate market size is likely to be valued at US$ 4.8 billion in 2026, and is projected to reach US$ 8.0 billion by 2033, growing at a CAGR of 7.6% during the forecast period 2026 - 2033.

The market is advancing at a promising pace as advanced photonic systems are becoming central to modern communication and sensing infrastructure. Demand is increasing as lithium niobate is supporting high speed optical signal modulation and precise wavelength control in next generation optical communication networks. Telecommunications providers and data center operators are increasingly integrating lithium niobate based components to improve bandwidth efficiency and signal stability. At the same time, defense and aerospace programs are adopting this material for secure communication, radar systems, and electro optic sensing applications that require high reliability and performance. Market development is further strengthening as research institutions and technology companies are accelerating work on integrated optical devices and quantum computing platforms. Lithium niobate is enabling tighter integration between semiconductor electronics and photonic circuits, supporting faster data processing and lower energy consumption. Public and private funding is continuing to support material innovation, fabrication techniques, and scalable manufacturing.

Key Industry Highlights

- Dominant Form: Wafers are expected to lead with approximately 46% revenue share in 2026, driven by chip-scale photonics.

- Leading Grade: Electronic-grade lithium niobate is expected to hold nearly 52% share in 2026 due to strict purity requirements, whereas industrial-grade is likely to grow fastest at an 8.4% CAGR.

- Application Landscape: Electro-optical modulators are expected to dominate with around 38% share in 2026, while integrated optical devices are anticipated to expand fastest at a 10.2% CAGR, supported by photonics–semiconductor convergence.

- End-Use Demand Profile: Telecommunications is expected to remain the largest end-use segment with about 41% share in 2026, while defense is likely to grow steadily at an 8.8% CAGR through multi-year procurement programs.

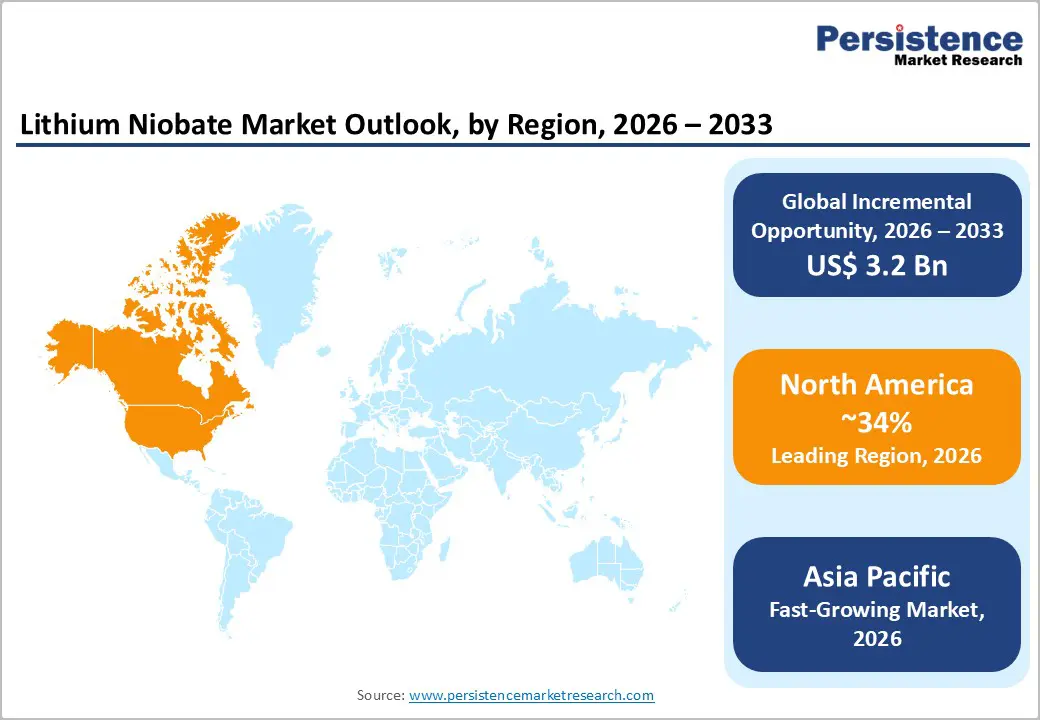

- Regional Dynamics: North America is expected to lead with about 34% share in 2026, supported by advanced telecom and defense investments.

- Fastest-growing Market: The Asia Pacific market is projected to grow the fastest at an estimated 8.9% CAGR through 2033, driven by large-scale telecom rollouts and manufacturing expansion.

- Technology Evolution: Thin-film lithium niobate has enabled compact, energy-efficient photonics, accelerating adoption across integrated optics, quantum systems, and next-generation sensing.

- December 2025: Silicon Austria Labs (SAL) unveiled the world's first 8-inch thin-film lithium niobate (TFLN) wafer processed entirely in-house for scalable integrated photonics, using proprietary hard-mask deposition, stitching-free electron beam lithography, and precision etching.

| Report Attribute | Details |

|---|---|

|

Lithium Niobate Market Size (2026E) |

US$ 4.8 Bn |

|

Market Value Forecast (2033F) |

US$ 8.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Acceleration of Optical, Defense, and Quantum Photonic Infrastructure

According to the International Telecommunication Union (ITU), global internet traffic has consistently grown at double-digit rates, driving demand for electro-optical modulators capable of supporting ultra-high bandwidth and low latency. Major telecom operators such as AT&T and Verizon Communications continue expanding fiber-optic transport and backhaul networks to support 5G and broadband upgrades, while infrastructure deployments such as Transworld Associates’ and Cybernet’s terabit-class optical backbones in Pakistan reflect real-world scaling of high-capacity long-haul connectivity. In the Middle East, du’s nationwide 400G optical backbone rollout further underscores demand for high-speed optical transmission across commercial networks.

Rising adoption of photonic systems in defense and aerospace further amplifies this demand. Defense modernization programs increasingly rely on advanced optical materials for radar, secure communications, and sensing technologies, with sustained investment in electro-optic and acousto-optic systems for missile guidance, surveillance, and electronic warfare. In parallel, research programs supported by the U.S. National Science Foundation, Japan’s METI, and the European Commission prioritize integrated optical devices and quantum photonics platforms, where lithium niobate wafers enable scalable, low-loss signal processing. These initiatives, combined with advances in thin-film lithium niobate technology, are accelerating commercialization across data centers, quantum communication networks, and next-generation computing architectures.

High Production Complexity and Supply Chain Concentration Risks

Lithium niobate manufacturing is a highly complex and costly enterprise, with precision-controlled crystal growth and wafer processing requiring advanced furnace systems and cleanroom infrastructure. Recent capacity expansions by companies such as Shin-Etsu Chemical in Japan, which expanded lithium niobate wafer production to 8-inch substrates, underscore the scale of investment needed to meet demand for advanced photonics. These elevated production requirements significantly increase the final component cost, limiting price competitiveness with alternative electro-optic materials in cost-sensitive applications. As a result, manufacturers face structural cost pressures that constrain broader adoption in lower-margin segments.

The global supply chain for lithium niobate is concentrated in a limited set of regions and facilities, exposing the industry to geopolitical and policy risks. China remains a dominant producer of lithium niobate and advanced materials, and recent export control updates by China’s Ministry of Commerce on high-tech inputs illustrate how policy shifts can affect material flows. At the same time, geopolitical tensions have prompted governments, including the United States under its CHIPS and Science Act, to fund domestic production initiatives to reduce reliance on imports. These dynamics, combined with energy-intensive processing and localized fabrication capacity, can lead to delivery delays for telecom and defense customers and heighten supply chain vulnerability during geopolitical or trade disruptions.

Expansion of Advanced Photonics and Telecom Applications

The commercialization of thin-film lithium niobate (TFLN) platforms is creating significant market expansion opportunities, as compact, energy-efficient integrated optical devices enter deployment. Cloud service providers such as Microsoft Azure and Alibaba Cloud have deployed TFLN modulators in data centers to support bandwidth-intensive applications, while major equipment manufacturers such as Broadcom secured contracts to supply LiNbO-based modulators for 800G/1.6T optical networks. The researchers at Harvard SEAS developed an integrated TFLN photonic device capable of direct digital-to-analog conversion, combining modulation in a single step, reducing energy consumption, and enabling high-speed performance up to 186 Gbps. This breakthrough demonstrates the potential for energy-efficient optical computing, AI acceleration, and next-generation communications, further validating the adoption of thin films in commercial-scale systems.

Emerging markets are accelerating telecom infrastructure investments, particularly in fiber-optic and 5G backhaul networks, driving incremental demand for lithium niobate-based modulation and filtering components. Operators across Canada and South Korea have integrated advanced LiNbO components in pilot 5G deployments, highlighting regional connectivity upgrades and performance requirements. Beyond telecom, lithium niobate’s nonlinear optical properties support precision frequency conversion, quantum communication, and high-performance sensing applications. As pilot initiatives evolve into commercial deployments, demand for high-purity wafers and customized crystal formats is expected to grow structurally, reinforcing market expansion across both connectivity and advanced photonics applications.

Category-wise Analysis

Form Insights

Wafer-based lithium niobate is expected to contribute roughly 46% of market revenue in 2026, as its established process flows support widespread use in telecom and photonic device manufacturing. Nokia announced the modernization of Vodafone Idea’s optical transport network in India using advanced optical transport technologies to support growing 4G/5G data traffic, reflecting increased operator investment in high-performance optical components that underpin demand for high-bandwidth modulators. Wafer formats offer proven performance, reliability, and integration with existing optical transceiver platforms across telecommunications and data infrastructure sectors.

The fastest-growing product form is likely to be thin-film and engineered wafers, forecast to grow at a CAGR of 9.1% through 2033, driven by strengthening demand for compact photonic integrated circuits (PICs) and energy-efficient optical components. For example, Hamamatsu Photonics launched thin-film lithium niobate modulators for high-bandwidth communications, accelerating integration into optical networks and high-performance PICs. As fabrication techniques compatible with semiconductor processing mature, the adoption of engineered wafer types continues to expand into advanced computing and miniaturized optical systems.

Grade Insights

Electronic grade is slated to hold approximately 52% of the lithium niobate market share in 2026, driven by stringent purity and performance requirements for optical modulators, frequency conversion devices, and mission-critical systems. Its high electro-optic coefficient, thermal stability, and signal fidelity under extreme conditions make it essential for telecom, aerospace, and defense applications. Supporting this leadership, Lumentum showcased new 400/800G ZR+ pluggable transceivers and 800G modules at OFC 2025, designed to enhance optical network capacity across data centers, metro, and long-haul infrastructure. These developments illustrate the critical role of electronic-grade lithium niobate in enabling high-speed, high-bandwidth systems. Additionally, expanding adoption of integrated photonics and advanced sensing platforms further reinforces demand for premium-grade material.

Industrial-grade lithium niobate is projected to be the fastest-growing from 2026 to 2033, propelled by broader use cases in sensors, acoustic transducers, and industrial automation systems. Samsung Electronics, for example, announced a partnership with JASCO to co-develop lithium niobate-based modulators targeting next-generation display and sensing applications in the 300–900-nm band, highlighting broader industry engagement with LiNbO thin-film technologies and cross-industry applications that often leverage industrial-grade materials where extreme purity is not mandated. These developments fuel steady volume growth for industrial-grade LiNbO across non-critical optical applications and manufacturing hubs.

Application Insights

Electro-optical modulators are anticipated to be the dominant application segment, commanding a market revenue share of approximately 38% in 2026, as telecom operators and hyperscale data centers increasingly deploy high-speed modulators to handle growing bandwidth and low-latency requirements. These modulators form the backbone of optical communication networks, enabling reliable data transmission across long-haul, metro, and access networks. For example, Gooch & Housego expanded its U.S. presence through the acquisition of Global Photonics, enhancing its capabilities in high-performance optical systems and expanding manufacturing capacity. This development strengthens G&H’s ability to supply advanced modulators for both commercial telecom networks and aerospace and defense applications. The expansion also signals growing industry investment in domestic production of critical optical components.

The integrated optical devices are projected to be the fastest-growing application with a CAGR of 10.2% through 2033, supported by ongoing photonics-semiconductor convergence and increasing miniaturization. Optica Thin-Film Lithium Niobate webinar highlighted progress toward commercial thin-film platforms with an agile foundry focus, underscoring broader industry alignment toward scalable, integrated photonic circuits and devices. Real-world research breakthroughs, such as mid-infrared integrated lithium niobate modulators showing high-speed performance and broad optical-range potential, furthering signal momentum in embedded integrated optical solutions. These developments reflect expanded adoption of integrated optical devices across telecommunications, sensing, and computing domains.

End-Use Insights

The telecommunications sector is expected to remain the largest end-user with about 41% revenue share in 2026, driven by fiber-optic upgrades and advanced network deployments. Recent optical communication advancements showcased at industry events in 2025 emphasize the critical importance of high-performance optical technologies for next-generation data rates, supporting ongoing telecom investments. NVIDIA’s roadmap for co-packaged optics and silicon photonics for AI GPU communication reflects the growing importance of high-bandwidth optical links in future telecom and hyperscale applications.

The defense sector is projected as the fastest-growing end-use segment, projected to display a CAGR of approximately 8.8% from 2026 to 2033, as strategic programs adopt photonic sensing and secure communication systems. India’s Defense Research and Development Organisation (DRDO) completed fabrication of its first photonic radar system, indicating expanding defense photonics deployment that aligns with high-performance optical technologies. These verified milestones highlight how advanced optical materials and integrated solutions are powering growth in secure communications and sensing across defense and aerospace ecosystems.

Regional Insights

North America Lithium Niobate Market Trends

North America holds a leading position in the lithium niobate market, with the U.S. contributing approximately 34% of revenue in 2026, driven by photonics R&D, defense procurement, and telecom infrastructure. Federal funding and university-industry collaborations support innovation pipelines in integrated photonics, optical interconnects, and high-speed communication components. Regulatory oversight emphasizes material reliability and performance standards, promoting adoption of electronic-grade and integrated optical devices. Investments focus on next-generation modulators, integrated circuits, and defense-grade components. Mature supply chains and domestic manufacturing reduce operational risks. Early commercialization of thin-film lithium niobate platforms accelerates adoption and market growth.

Ciena showcased coherent 1.6 Tb/s optical solutions at OFC San Francisco, demonstrating North America’s leadership in next-generation optical networking. Similarly, Taara Connect’s free-space optical links delivering 20 Gbps highlight growing applications beyond fiber networks. Intellectual property protections and skilled labor support the rapid adoption of high-performance optical components. Infrastructure upgrades and defense modernization programs are reinforcing demand for LiNbO. Pilot projects in quantum and AI-assisted photonics expand commercial use. These factors ensure North America maintains strong market leadership with stable growth through 2033.

Europe Lithium Niobate Market Trends

The market for lithium niobate in Europe is anticipated to exhibit steady growth through 2033, with Germany, the U.K., France, and Spain supported by Horizon Europe programs in integrated optics, nonlinear photonics, and advanced materials. Sustainability and energy-efficient production are prioritized by manufacturers, influencing supplier selection for premium LiNbO components. Regulatory harmonization ensures consistent quality across member states. Collaborative academic and industry projects strengthen Europe’s competitive position. Fiber-optic upgrades, research investments, and photonic integration programs support market expansion. Advanced optical device adoption in telecom, industrial, and defense sectors sustains demand.

Photonics innovations received strong visibility at the 51st European Conference on Optical Communication (ECOC) conference in Copenhagen, showcasing advancements in coherent technologies and silicon photonics. National initiatives in quantum photonics and fiber-optic backbone expansion are driving increased adoption of LiNbO components across telecom and industrial networks. Cross-border collaborations and joint R&D projects continue to advance the deployment of integrated optical devices. Investments in AI-enabled optical networks and industrial photonics applications further strengthen commercial and defense use cases. Coordinated policies and dedicated funding programs enhance infrastructure readiness and technology integration.

Asia Pacific Lithium Niobate Market Trends

Projected to post a 2026-2033 CAGR of about 8.9%, Asia Pacific is poised to be the fastest-growing regional market for lithium niobate, driven by robust telecom infrastructure expansion and strong manufacturing ecosystems. China, Japan, India, and ASEAN economies lead adoption through government-backed fiber-optic and semiconductor programs. Manufacturing scale advantages and precision material expertise accelerate lithium niobate deployment. Thin-film LiNbO platforms and integrated photonic devices increase production efficiency. Academic-industry collaborations support innovation in next-generation sensing and communication solutions. Rising data center demand and industrial automation further reinforce market momentum.

Asia Pacific emerged as a hub for advanced photonics innovation, with the Asia Photonics Expo in Singapore highlighting high-performance optical communication solutions, including LiNbO modulators and integrated circuits. The Asia Communications and Photonics Conference (ACP 2025) in Suzhou focused on optical access networks and deployment strategies, reflecting regional industry engagement. Government initiatives in India and ASEAN continue to strengthen telecom and semiconductor infrastructure. Expansion of optical testing, certification, and production facilities enhances regional supply capabilities. Combined with rising network demands and industrial automation, these developments establish Asia Pacific as a critical growth engine for the global lithium niobate market.

Competitive Landscape

The global lithium niobate market structure is moderately consolidated, with leading players such as Gooch & Housego, Lumentum, Fujifilm, and Sumitomo Electric collectively accounting for over half of the total revenue. These established companies leverage extensive optical component expertise, high-purity crystal production capabilities, and long-standing relationships with telecom, defense, and industrial clients. They also invest significantly in R&D for thin-film LiNbO, integrated optical devices, and high-speed modulators, maintaining technological leadership in next-generation photonics.

Regional and niche competitors, including Mitsubishi Electric, Nikon, and Chinese domestic manufacturers, focus on specialized segments such as data-center interconnects, quantum photonics, and industrial sensing. High barriers, including precision manufacturing requirements, purity standards, and complex device integration, limit new entrants. However, emerging digital photonics platforms and thin-film innovations are enabling smaller technology providers to enter through partnerships and pilot deployments. Market consolidation is expected to increase gradually, as global leaders acquire smaller players to expand technologically and geographically, while software, integration, and semiconductor firms continue collaborating to develop next-generation LiNbO-based photonic solutions.

Key Industry Developments

- In January 2026, Theon International finalized the acquisition of a 9.8% stake in Exosens SA for € 268.7 million (US$ 311 million). Announced in October 2025, the transaction secured a strategic supply chain for Theon’s night vision products. The deal reinforced the long-standing commercial partnership between the companies, including an extended supply agreement through 2030.

- In December 2025, Hamamatsu Photonics introduced the HyperGauge® In-Plane Film Thickness Meter (Model C17319-11) to enhance semiconductor manufacturing productivity. The device enables full-surface, high-speed film thickness measurements, improving quality control and throughput. This launch highlights the company’s leadership in precision materials and photonics technology innovation.

- In December 2025, NTT Research, collaborating with Cornell and Stanford, published in Nature Physics a lithium niobate-based 2D programmable photonic waveguide offering around 10,000 spatial degrees of freedom for precise light wave control. The simply fabricated chip, programmed via illumination patterns as virtual electrodes, performed all-optical neural network inference, enabling complex optical computations for datacenters, communications, and beyond.

Companies Covered in Lithium Niobate Market

- Sumitomo Metal Mining

- Coherent Corp.

- Fujian Castech Crystals

- Exail (iXblue)

- Thorlabs Inc.

- Gooch & Housego

- Raicol Crystals

- Deltronic Crystal Industries

- Altechna

- HC Photonics

- EKSMA Optics

- CASTECH Inc.

Frequently Asked Questions

The global lithium niobate market is projected to reach US$ 4.8 billion in 2026.

Key growth drivers include the expansion of high-speed optical communication infrastructure, adoption of lithium niobate in defense and aerospace photonics, and commercialization of thin-film integrated optical devices.

The market is poised to witness a CAGR of 7.6% between 2026 and 2033.

Major opportunities are coming up in thin-film LiNbO₃ platforms for integrated photonics, emerging market telecom infrastructure expansion, and quantum/sensing photonics applications.

Gooch & Housego, Lumentum, Fujifilm, Sumitomo Electric, and Mitsubishi Electric are a few among the key players.