- Non-food Packaging

- Lip Care Packaging Market

Lip Care Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Lip Care Packaging Market by Packaging Type (Tubes, Tins, Others), Material Type (Paperboard, Plastic, Others), Applicator Type, and Regional Analysis for 2026 - 2033

Lip Care Packaging Market Size and Trends Analysis

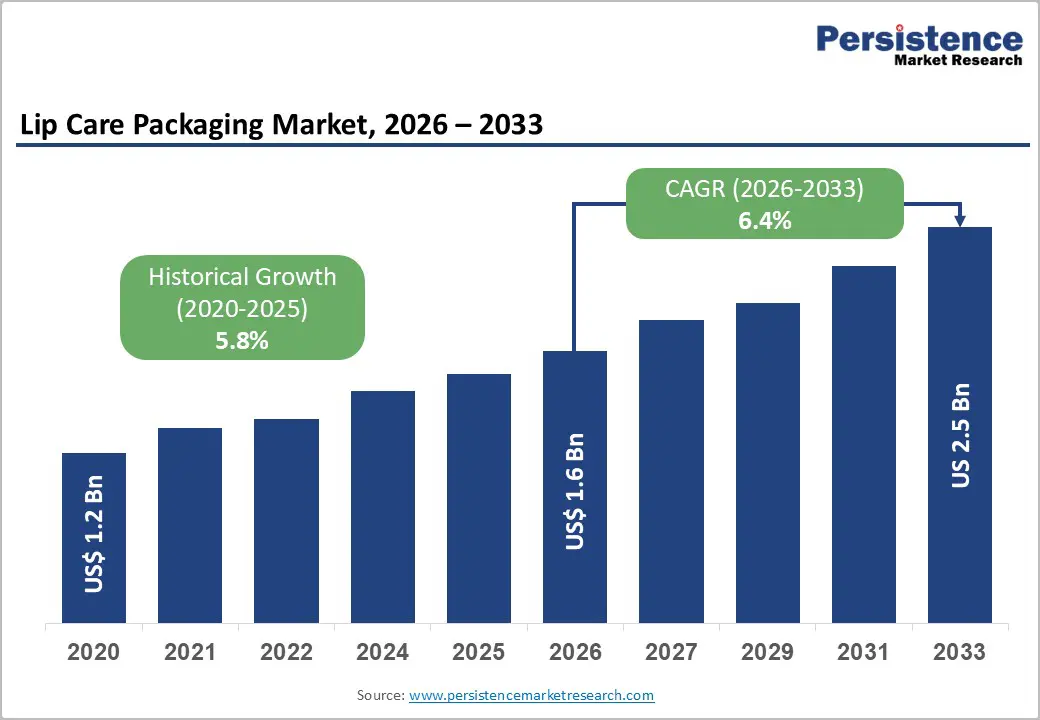

The global lip care packaging market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$2.5 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033, driven by rising per-capita personal care expenditure, increasing premiumization of lip care products such as serums, SPF balms, and tinted formulations, and sustained brand investment in sustainable and differentiated primary packaging solutions.

E-commerce growth and omnichannel sampling strategies are increasing the number of SKUs per brand, elevating packaging complexity and average packaging value per unit. Over the forecast period, demand will increasingly concentrate on lightweight tubes, mono-material refillable sticks, and advanced applicators that enhance hygiene, portability, and user experience.

Key Industry Highlights

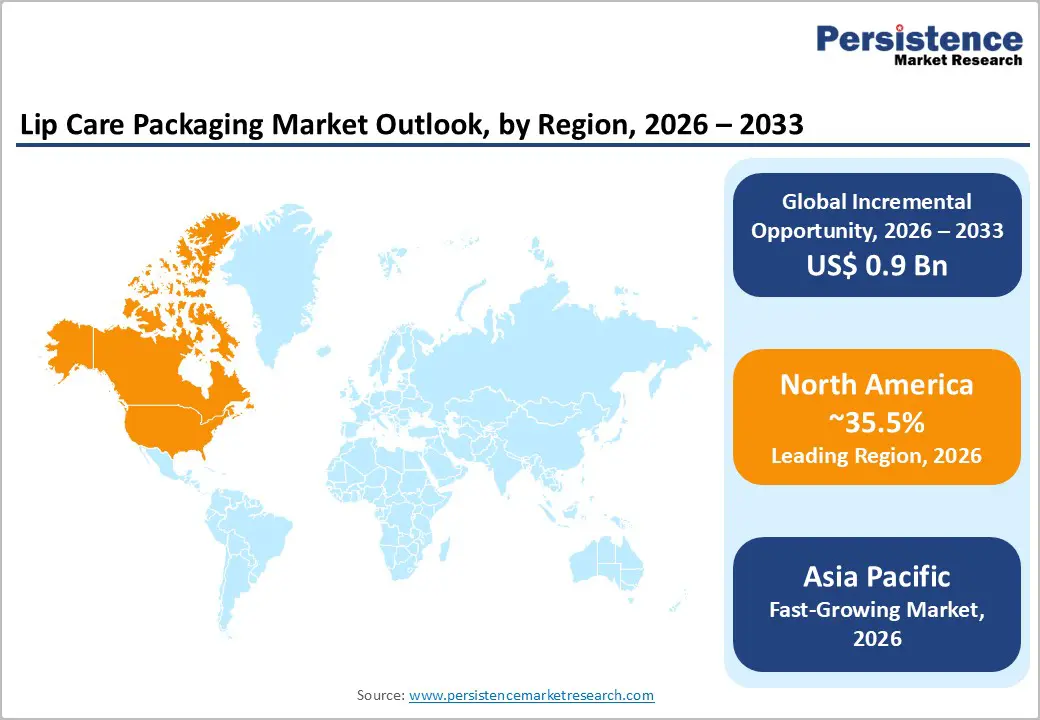

- Leading Region: North America is projected to lead the market, supported by premium product penetration and high packaging spend per unit, accounting for approximately 35.5% of market share, driven by strong U.S. SKU launch activity, DTC adoption, and advanced regulatory-compliant packaging demand.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, fueled by population scale, rapid e-commerce growth, and accelerating lip care consumption in China, India, and ASEAN markets.

- Investment Plans: Packaging investments are concentrated in short-run tooling, regional decoration hubs, and refill-compatible platforms, with over 60% of new capital deployment focused on recyclable materials, PCR integration, and near-shore manufacturing to improve speed-to-market and regulatory compliance.

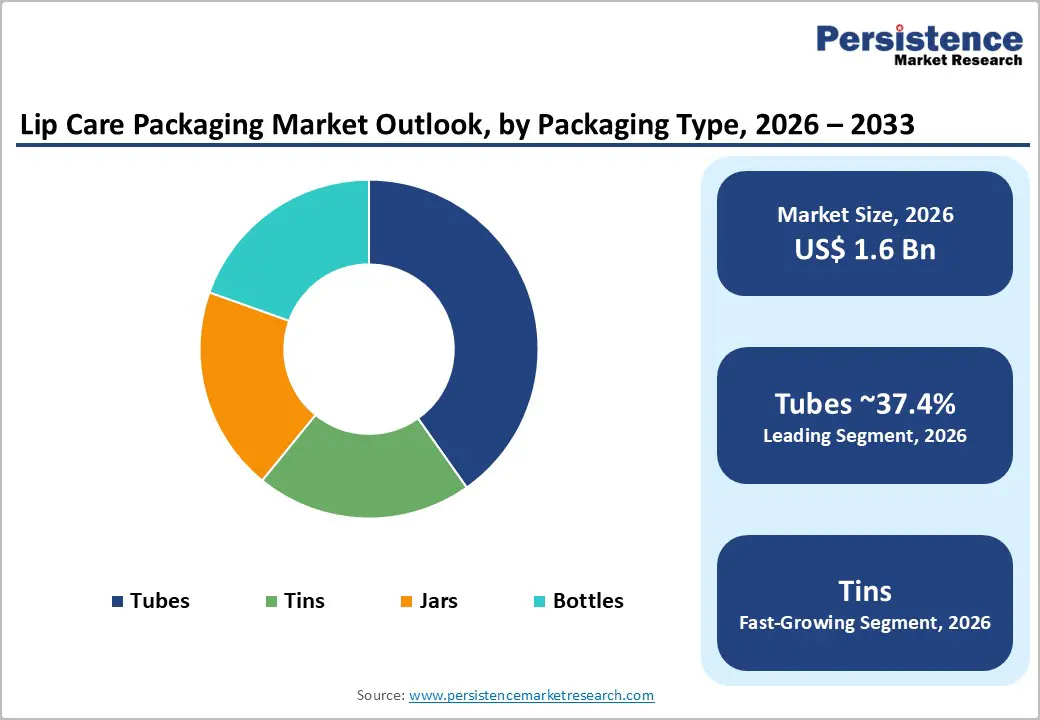

- Dominant Packaging Type: Tubes are anticipated to dominate the packaging type segment, holding 37.4% revenue share, supported by cost efficiency, hygienic dispensing, and widespread adoption across mass and mid-priced lip care products.

- Leading Material Type: Paperboard is estimated to lead the material segment with a 34.6% share, driven by sustainability mandates, lightweight structure, and strong adoption in secondary packaging and gift-oriented lip care formats.

| Key Insights | Details |

|---|---|

| Lip Care Packaging Market Size (2026E) | US$1.6 Bn |

| Market Value Forecast (2033F) | US$2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability Regulations and Brand ESG Commitments

Growing regulatory scrutiny and consumer expectations around sustainability are reshaping lip care packaging design. Brands are actively replacing multi-material laminates with mono-material tubes and introducing refillable stick systems to improve recyclability and reduce lifecycle environmental impact. While these formats typically incur higher per-unit packaging costs, they enable compliance with emerging waste-reduction frameworks and strengthen brand ESG positioning.

Supplier activity in 2024-2025 indicates widespread adoption across both premium and mass-market segments, with recyclable and refillable packaging accounting for a significant share of new product launches. Business impact: procurement teams will need to manage higher initial packaging costs to achieve regulatory compliance, enhanced shelf visibility, and alignment with long-term sustainability goals.

Formulation Innovation Increasing Packaging Complexity

The proliferation of advanced lip care formulations, including SPF balms, active serums, and overnight repair products, has significantly expanded packaging requirements. These products require specialized dispensing systems such as airless tubes, roll-ons, and precision applicators, along with enhanced barrier protection to preserve active ingredients.

In parallel, SPF and medicated lip products are subject to stricter labeling and compliance standards, increasing design complexity and development timelines. This diversification raises average packaging value per SKU while shortening product replacement cycles. Suppliers offering integrated co-engineering capabilities across materials, dispensing systems, and regulatory requirements are securing premium, longer-term partnerships.

Omnichannel Sampling and Premiumization

Direct-to-consumer channels, subscription boxes, and influencer-led launches are accelerating demand for small-format and limited-run packaging. Sample tubes, tins, and mini formats require specialized tooling, rapid decoration, and flexible production schedules. Premium brands are increasingly investing in metalized finishes, tactile coatings, and decorative caps to reinforce brand differentiation. These trends increase per-unit packaging revenue and favor suppliers with regional manufacturing footprints and digital decoration capabilities. Brands must integrate tooling amortization and short-run pricing models into procurement strategies to maintain launch agility.

Barrier Analysis - Volatility in Polymer and Metal Feedstock Costs

Fluctuating prices for polyethylene, polypropylene, and aluminum continue to pressure packaging margins. For lip care formats with relatively low absolute unit values, sudden cost increases can disrupt product economics, delay launches, or force material substitutions. Historically, sharp feedstock price movements have increased packaging costs by 3-8% within a single fiscal year, raising breakeven volumes and slowing innovation pipelines.

Recycling Infrastructure Limitations

Despite advances in mono-material packaging design, recycling infrastructure remains uneven across regions. Labels, adhesives, and multi-component closures often limit recyclability in the real world. Brands making recyclable claims face reputational and regulatory risks when collection systems do not support those formats. In several major markets, effective recyclability for cosmetic packaging remains below 50%, increasing compliance complexity and transition costs.

Opportunity Analysis - Refillable and Modular Stick Systems

Refillable lipstick and balm systems represent a high-value growth opportunity. By transitioning 10-15% of premium launches to refillable formats by 2028, brands can improve customer lifetime value while reducing material consumption. This shift could generate US$ 40-80 million in incremental supplier revenue through refill cartridges, premium outer cases, and standardized refill mechanisms. Suppliers that develop scalable refill platforms stand to benefit from recurring revenue streams and deeper brand integration.

Sustainable Alternatives to Multi-Laminate Tubes

Replacing conventional laminated tubes with mono-material or recyclable laminate alternatives addresses both regulatory pressure and consumer sustainability expectations. Packaging suppliers that successfully convert mass-market lip balm volumes to recyclable tube solutions can secure long-term contracts with large consumer brands. If even 20% of conventional laminated tube volume converts to recyclable alternatives by 2030, suppliers gain access to higher-margin opportunities in tooling, decoration, and materials innovation.

Category-wise Analysis

Packaging Type Insights

Tubes are expected to maintain a dominant position, accounting for approximately 37.4% of global lip care packaging revenue, supported by their portability, hygienic dispensing, and compatibility with a broad range of formulations, from balms and medicated lip treatments to tinted glosses. High-volume extrusion and injection molding capabilities enable large-scale manufacturing with consistent quality, enabling brand owners to achieve cost efficiency and rapid SKU turnover. These characteristics make tubes the preferred packaging format for mid-priced and mass-market lip care products distributed through pharmacies, supermarkets, and e-commerce platforms. Customization flexibility further strengthens tube adoption. Brands frequently leverage printed sleeves, metallic finishes, and decorative caps to support seasonal promotions and influencer-led product refreshes. Travel-size and on-the-go formats are widely adopted by global players such as Unilever, Beiersdorf, and Johnson & Johnson, reinforcing tubes as a commercially resilient and operationally efficient packaging choice across mature and emerging markets.

Metal tins are anticipated to register the fastest growth rate among packaging types during the forecast period, driven by rising demand for premium, giftable, and reusable lip care formats. Tins resonate strongly with heritage brands and indie cosmetic labels seeking tactile differentiation and a vintage or artisanal aesthetic. Their durability, refill potential, and perceived sustainability value align well with clean-beauty and low-waste brand positioning strategies. Higher decoration flexibility, including embossing, debossing, and full-surface printing, supports premium pricing and limited-edition product launches. Brands such as Lush, Burt’s Bees, and niche DTC players increasingly use tins for seasonal gift sets and specialty balms, accelerating adoption. While tins remain costlier than tubes, their ability to command higher margins and enhance brand storytelling contribute to faster segment growth than conventional formats.

Material Type Insights

Paperboard is anticipated to account for 34.6% of material share, driven by its strong sustainability credentials and extensive use in secondary packaging, gift sets, and promotional bundles for lip care products. Brands favor paperboard for its recyclability, lightweight structure, and suitability for high-quality graphic storytelling, which is critical for shelf differentiation in premium and mass-market segments. Compared to metal alternatives, paperboard offers lower transportation emissions and improved cost efficiency at scale. Advances in water-based barrier coatings, FSC-certified fibers, and higher recycled content ratios have strengthened paperboard’s position across both premium and mass-market applications. Leading cosmetic groups, including L’Oréal and Estée Lauder Companies, increasingly integrate paperboard solutions into sustainability roadmaps, reinforcing long-term demand across global retail and travel-retail channels.

Plastic is anticipated to remain the fastest-growing material category, representing approximately 33% share, supported by its lightweight durability, design versatility, and precision injection-molding capabilities. Plastic materials remain essential for primary lip care packaging due to their ability to support complex dispensing mechanisms, airtight sealing, and consistent applicator performance across liquid, semi-solid, and balm formulations. Ongoing innovation in mono-polymer designs and increased use of post-consumer recycled (PCR) content allow plastic packaging to meet functional requirements while aligning with evolving recyclability standards. Major packaging suppliers such as AptarGroup, Albéa, and HCP Packaging continue to invest in recyclable plastic systems, ensuring plastics remain indispensable for applicators and closures despite rising regulatory scrutiny.

Regional Insights

North America Lip Care Packaging Market Trends - Premium Differentiation, FDA Oversight, and Refill-Ready Innovation

North America is projected to represent a high-value lip care packaging market, underpinned by a premium-heavy product mix, high packaging spend per unit, and complex regulatory oversight. The U.S. leads the region in SKU proliferation, direct-to-consumer (DTC) adoption, and speed of product refresh cycles. Large beauty conglomerates and indie brands alike prioritize packaging differentiation, driving sustained demand for advanced applicators, decorative finishes, and short-run customization. Sustainability commitments from major players such as Estée Lauder Companies, L’Oréal USA, and Unilever North America are accelerating the shift toward recyclable materials, PCR content, and refill-compatible designs in both primary and secondary packaging.

Regulatory scrutiny significantly influences packaging development in the region. Oversight by the U.S. Food and Drug Administration (FDA) of SPF-containing and medicated lip products increases compliance requirements for labeling, material safety, and dosage control. This elevates packaging complexity and often extends development timelines, particularly for applicator systems and air-tight closures. In response, brands increasingly favor suppliers with proven regulatory expertise and localized manufacturing. Packaging companies such as AptarGroup and Berry Global have expanded North American capabilities in precision molding, testing, and regional decoration, enabling faster regulatory validation and reduced time-to-market. Investment momentum remains concentrated in short-run tooling, regional decoration hubs, and refill-friendly platforms aligned with evolving consumer and regulatory expectations.

Europe Lip Care Packaging Market Trends - EPR-Led Sustainability and Luxury Refillable Packaging Ecosystems

Europe remains a mature yet innovation-driven market, supported by a strong concentration of prestige beauty brands and one of the world’s most stringent sustainability policy frameworks. Regulatory harmonization across the European Union, coupled with Extended Producer Responsibility (EPR) schemes and packaging waste directives, continues to accelerate the adoption of recyclable, mono-material, and refillable formats. These regulations directly influence material selection, component weight reduction, and design-for-recycling strategies, making compliance-driven innovation a core competitive requirement rather than a differentiator.

Western Europe, particularly France, Germany, and the U.K., leads premium packaging innovation, driven by the presence of global beauty brand headquarters and advanced design ecosystems. Brands such as Chanel, Dior, and LVMH-owned labels have expanded refillable lip care formats and paperboard-heavy secondary packaging, reinforcing demand for high-quality decoration and certified sustainable substrates. Southern Europe, especially Italy and Spain, plays a critical role as a manufacturing and decoration hub, hosting specialized converters and metal packaging suppliers. Ongoing supplier consolidation and closer brand-converter partnerships are strengthening circular packaging ecosystems, with investments focused on recycled aluminum, water-based inks, and modular component systems that comply with EU sustainability mandates while preserving luxury aesthetics.

Asia Pacific Lip Care Packaging Market Trends - High-Volume Digital Commerce and Precision-Driven Premium Growth

Asia Pacific is the fastest-expanding regional market for lip care packaging, driven by population scale, rising disposable incomes, and rapid growth in digital commerce channels. China leads incremental volume growth, supported by strong domestic beauty brands and high-frequency product launches on platforms such as Tmall and Douyin. This dynamic retail environment favors packaging formats that support rapid SKU rotation, localized decoration, and cost-efficient scalability. Chinese packaging suppliers have responded by investing in high-speed injection molding and automated decoration lines, enabling faster turnaround for both domestic and international brands.

Japan and South Korea continue to set benchmarks for premium innovation, particularly in applicator precision, ergonomic design, and compact formats. Brands such as Shiseido, Amorepacific, and Kao emphasize functional performance and aesthetic refinement, driving demand for advanced plastic components and high-tolerance manufacturing. India and ASEAN markets remain relatively price-sensitive but are witnessing accelerated adoption of sustainability messaging in urban centers. Brands such as Hindustan Unilever and regional DTC players increasingly incorporate recyclable plastics and paperboard-based secondary packaging to align with emerging consumer awareness. Regional investments in tooling, decoration, and near-shore production across Southeast Asia are improving supply chain flexibility and enabling faster market responsiveness across diverse price tiers.

Competitive Landscape

The global lip care packaging market is moderately consolidated, with global suppliers dominating high-volume tubes and precision dispensing systems, while regional specialists serve premium tins, decoration, and short-run formats. Competitive advantage increasingly depends on integrated capabilities across materials engineering, sustainability compliance, and localized production.

Leading suppliers emphasize design-for-circularity, refill platform standardization, localized decoration, and co-engineering with brands. Differentiation increasingly depends on regulatory expertise, rapid prototyping, and advanced surface decoration to support fast innovation cycles.

Key Industry Developments

- In July 2025, Quadpack announced the launch of new monomaterial PET packaging technology at its Kierspe, Germany, facility, enabling the production of fully recyclable lip gloss bottles and airless packs using PET and post-consumer recycled content to reduce environmental impact and improve lead times.

- In February 2025, Berry Global introduced three new compact sizes in its recyclable Stick and Refill range, expanding options for cosmetics and lip care brands with lighter, fully recyclable PET and PP sticks that support personalized decorative finishes.

Companies Covered in Lip Care Packaging Market

- AptarGroup

- Albéa Group

- Berry Global

- HCP Packaging

- Quadpack

- Silgan Dispensing

- RPC Group

- Gerresheimer

- Berlin Packaging

- Amcor

- Cosmopak

- Aptar Beauty + Home

- Wheaton Group

- Piramal Glass

- Coveris

- CTK Cosmetics

- Rieke Packaging Systems

- Huhtamaki

Frequently Asked Questions

The global lip care packaging market is valued at US$1.6 billion in 2026.

By 2033, the lip care packaging market is projected to reach US$2.5 billion.

Key trends include rising adoption of sustainable materials such as paperboard and PCR plastics, growing demand for refill-friendly and reusable formats, increased use of short-run and decorative packaging for rapid SKU refreshes, and higher investment in regulatory-compliant applicator systems for SPF and medicated lip products.

The tubes packaging segment leads the market, accounting for 37.4% revenue share, driven by portability, hygienic dispensing, and cost-efficient scalability across mass and mid-priced lip care products.

The lip care packaging market is expected to grow at a CAGR of 6.4% between 2026 and 2033.

Major players include AptarGroup, Albéa Group, Berry Global, HCP Packaging, and Quadpack.