- Beauty & Personal Care

- Libya Cosmetics Market

Libya Cosmetics Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Libya Cosmetics Market by Product Type (Skin Care, Hair Care, Body Care, Makeup, and Others), Nature (Natural/Organic and Synthetic), Price Range (Mass and Premium), End-user, and Country Analysis for 2025 - 2032

Libya Cosmetics Market Size and Share Analysis

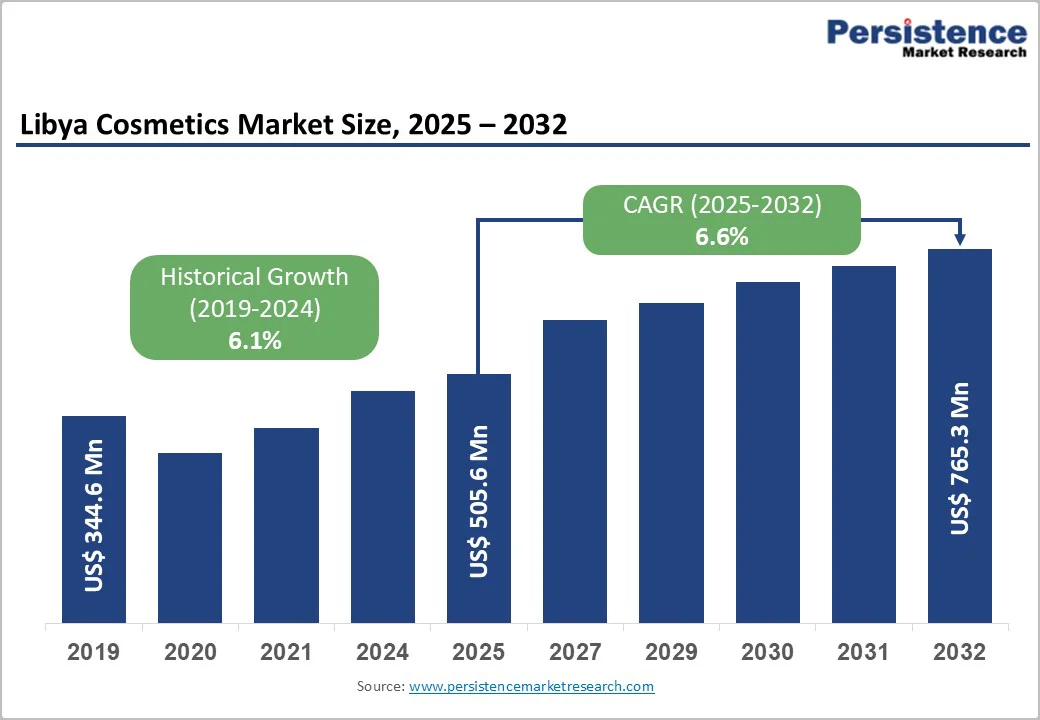

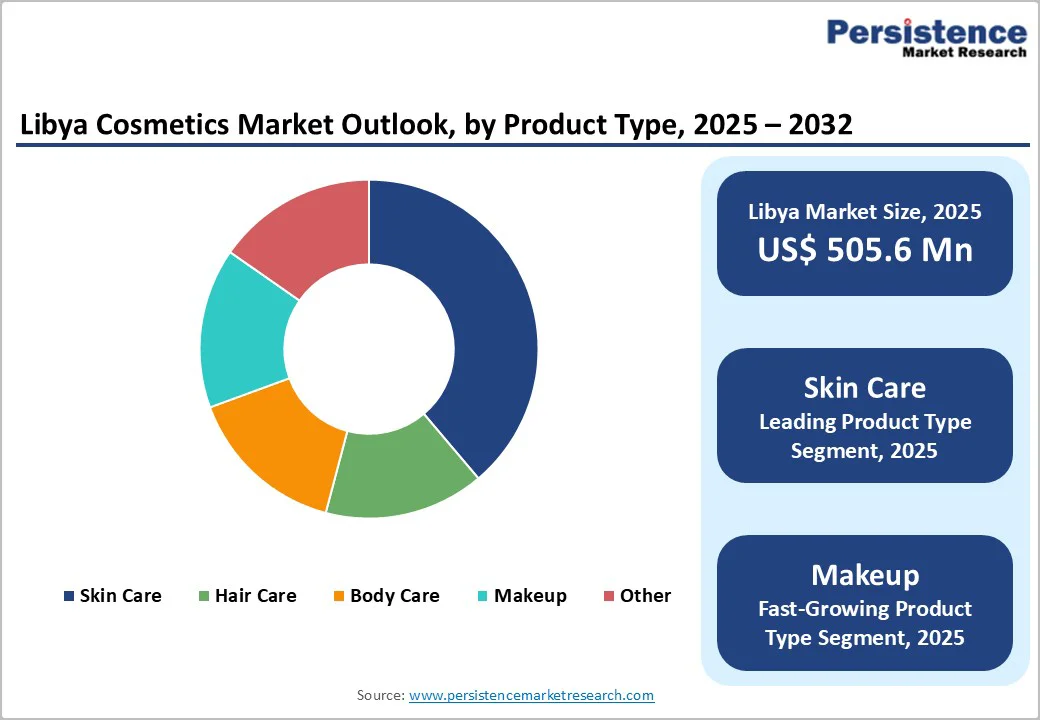

The Libya cosmetics market size is valued at US$ 505.6 million in 2025 and is projected to reach US$ 765.3 million by 2032, growing at a CAGR of 6.1% between 2025 and 2032.

Growing consumer awareness about beauty and personal grooming, rising disposable incomes, particularly among younger demographics and working women, and increasing penetration of international brands through digital platforms are some of the primary factors accelerating cosmetics market growth. Increasing demand for natural and organic cosmetics reflecting sustainability trends, rapid e-commerce expansion enabling broader product accessibility, and post-conflict economic stabilization will also stimulate market growth.

Key Market Highlights

- Dominant Product Type: Skincare Products command the largest product category at 38% market share, driven by harsh climate conditions, anti-aging consciousness, UV protection requirements, and consumer investment in complexion health.

- Leading Nature: Synthetic cosmetics lead the Libya cosmetics market with 62% share, due to their affordability, availability, and strong consumer familiarity.

- Fastest Growing Nature: Natural and organic cosmetics are emerging as the fastest-growing segment, fueled by rising ingredient consciousness, demand for chemical-free products, and increasing preference for safer, skin-friendly formulations.

- Fastest Growing End-user: Male Grooming Products represent fastest-growing category at 7.8% CAGR, driven by changing cultural attitudes, younger demographic adoption, beard care trends, and social media normalization supporting exceptional expansion.

- Key Market Opportunity: Libya’s cosmetics market offers strong growth potential through rising demand for climate-specific, dermatologically safe skincare products. Expanding e-commerce and social commerce channels further create opportunities for international and D2C brands to penetrate underserved consumer segments.

| Key Insights | Details |

|---|---|

|

Libya Cosmetics Market Size (2025E) |

US$ 505.6 Mn |

|

Market Value Forecast (2032F) |

US$ 765.3 Mn |

|

Projected Growth CAGR(2025-2032) |

6.6% |

|

Historical Market Growth (2019-2024) |

6.1% |

Market Dynamics

Drivers - Rising Disposable Income and Emerging Middle-Class Consumer Base

Rapid urbanization in Libya is significantly reshaping consumer lifestyles, driving demand for modern beauty and personal care products. As more people move into urban centers like Tripoli, Benghazi, and Misrata, exposure to global beauty trends increases through social media, retail outlets, and influencer-driven marketing. This shift is encouraging Libyan consumers, especially young women, to adopt skincare, haircare, fragrances, and color cosmetics as essential parts of their daily routines rather than luxury items.

Growing internet penetration further amplifies awareness about new brands, product ingredients, and specialized beauty regimes. The influence of regional beauty standards from neighboring MENA markets also plays a role in expanding product demand. As a result, international and local brands have a wider base of modern, trend-conscious consumers seeking premium formulations, organic cosmetics, and specialized solutions for skin and hair concerns common in arid climates. This evolving preference landscape is a primary driver of sustained market growth.

Increasing Focus on Personal Grooming Among Both Genders

There is a noticeable cultural shift in Libya where personal grooming is gaining importance among both men and women, reflecting broader lifestyle modernization. Men are increasingly using grooming and hygiene products like beard oils, hair styling products, skincare essentials, and fragrances. Women, traditionally strong consumers in the sector, are now diversifying their product choices, moving beyond basic cosmetics to include advanced skincare, anti-aging products, serums, and hair treatments suited to harsh climatic conditions.

The rising middle-class population is also contributing to higher disposable spending on beauty and wellness categories. The expansion of beauty salons, barbershops, and dermatology clinics is nurturing a grooming-focused culture. Media content promoting self-care and aesthetic enhancement reinforces these behaviors. Collectively, these factors contribute to a broadening consumer base, driving consistent growth and category diversification in the Libya cosmetics market.

Restraints - Political and Economic Instability Impacting Consumer Confidence

Persistent political uncertainty and regional instability are affecting long-term consumer confidence and spending predictability. Currency fluctuations creating pricing volatility and inflation pressures on imported cosmetic products. Government policy changes impacting import regulations and tariff structures are affecting product availability and pricing. Limited local manufacturing infrastructure creates heavy dependence on imports and supply chain vulnerabilities. Unresolved security concerns in certain regions are limiting retail expansion and distribution network development.

Limited Regulatory Framework and Product Quality Concerns

The Libya cosmetics market faces a significant restraint due to the limited regulatory oversight governing product quality, safety standards, and import controls. Weak enforcement allows entry of counterfeit, substandard, and unverified cosmetic products, which undermines consumer trust and creates market instability. This issue particularly affects premium and international brands, as inconsistent product availability and rising concerns over authenticity discourage long-term brand loyalty. Additionally, the lack of standardized regulations challenges companies attempting to introduce dermatologically safe or specialized formulations, slowing market expansion and affecting overall consumer confidence.

Opportunities - Expansion of E-Commerce and Digital Beauty Retailing

Libya’s digital ecosystem is rapidly improving, creating a strong opportunity for online cosmetic retail and digital-first brands. Although e-commerce is still developing, social commerce through Facebook, Instagram, and WhatsApp is booming, giving sellers a direct route to consumers. This shift allows brands to bypass traditional retail limitations and reach customers across cities and remote areas at lower operational costs. Digital platforms also provide space for virtual consultations, influencer collaborations, and targeted marketing campaigns that resonate with younger demographics, Libya’s most active online users.

With rising smartphone adoption and online payment improvements, the convenience of browsing, comparing, and purchasing beauty products online is becoming more appealing. International brands that are not physically present in Libya can leverage digital channels to test market traction, build brand awareness, and scale faster. As digital infrastructure strengthens, e-commerce is expected to become a major growth accelerator in the cosmetics market.

Untapped Demand for Dermatologically-Safe and Climate-Specific Products

Libya’s climatic conditions, hot weather, high UV exposure, and dryness, create a strong opportunity for brands offering dermatologically-tested, climate-specific formulations. Consumers increasingly seek products addressing skin hydration, sun protection, pigmentation, acne management, and hair damage caused by environmental stress. However, the local market remains underpenetrated in specialized products such as SPF moisturizers, lightweight non-greasy skincare, heat-resistant makeup, and hair serums tailored to dryness and UV exposure. This gap gives international and regional brands significant room for expansion. Furthermore,

Dermatologists and skincare clinics are gaining prominence, creating channels for prescribing or recommending science-backed products. Clean beauty and sensitive-skin formulations are also gaining traction, especially among younger consumers who are more ingredient-conscious. Thus, brands focusing on climate-fit innovation, natural extracts, and dermatological efficacy can capture a growing niche segment with high loyalty and premium spending power.

Category-wise Analysis

Product Type Insights

Skincare products dominate the Libya cosmetics market, accounting for approximately 38% of total market share, primarily due to the country’s harsh climatic conditions. The intense heat, high UV exposure, and dry, arid environment drive strong demand for protective and nourishing skincare solutions. Moisturizers, sunscreens, and anti-aging creams hold a leading position as consumers increasingly prioritize hydration, sun protection, and prevention of premature aging. These products address common skin concerns such as dryness, pigmentation, sun damage, and early wrinkle formation, making them essential items in daily personal care routines. The growing preference for dermatologically tested, climate-specific, and lightweight formulations further strengthens the category's leadership within the market.

Nature Insights

Synthetic cosmetics maintain a dominant market share of approximately 62% in the Libya cosmetics market, supported by long-standing consumer familiarity, broad product availability, and competitive pricing. Conventional formulations continue to account for the majority of sales, especially across mass-market segments where affordability and accessibility remain key purchase drivers. Many consumers still rely on synthetic products due to their widespread presence in supermarkets, beauty stores, and informal retail channels, as well as strong brand recognition built over the years.

Natural/organics cosmetics are emerging as the fastest-growing category, driven by increasing awareness of ingredient safety, rising interest in chemical-free beauty routines, and the growing influence of global clean-beauty trends. Libyan consumers, particularly younger women, are becoming more conscious about product composition, preferring items with plant-based ingredients, gentle formulations, and dermatologically safe profiles. Improving e-commerce access and social media–led education further support rapid growth in this segment, positioning natural cosmetics as a key future opportunity within the market.

Price Range Insights

Mass-market cosmetics hold a dominant share of approximately 58% in the Libya cosmetics market, driven by strong affordability and widespread distribution across supermarkets, pharmacies, and informal retail channels. Budget-conscious consumers make up the largest portion of the population, leading to high demand for cost-effective daily grooming essentials such as basic skincare, haircare, and personal hygiene products. These affordable offerings continue to anchor the market, especially among lower- and middle-income groups that prioritize functionality and accessibility.

Premium cosmetics are steadily gaining traction, supported by rising urbanization, increasing disposable incomes, and growing exposure to international beauty trends through social media. Consumers, particularly young women in major cities, are showing a stronger preference for high-quality formulations, imported brands, natural ingredients, and specialized skincare solutions.

End-user Insights

Women consumers continue to dominate the Libya cosmetics market, accounting for approximately 72% of total cosmetics consumption. This dominance is rooted in long-established beauty and personal care traditions, as well as a strong cultural emphasis on skincare, grooming, and aesthetic enhancement. The growing population of working women is further accelerating demand, particularly in skincare and color cosmetics, as higher purchasing power and exposure to global beauty trends drive interest in premium, specialized, and climate-specific formulations. Women across urban centers are increasingly adopting multi-step skincare routines and exploring a wider range of cosmetic categories, reinforcing their leadership in overall market revenue.

Competitive Landscape

The Libya cosmetics market is highly fragmented, with international brands dominating the premium segment while local players remain strong within mass-market categories. Leading global manufacturers such as L'Oréal S.A., The Estée Lauder Companies, Groupe Rocher (Flormar), and Elizabeth Arden collectively account for approximately 35–40% of the market, supported by their extensive product portfolios, strong brand equity, and well-established distribution networks

Emerging online retailers and direct-to-consumer beauty brands are rapidly expanding their presence by leveraging social commerce, influencer collaborations, and targeted digital marketing. Companies across the market are increasingly focusing on localized product formulations, innovative digital marketing strategies, stronger brand building, and premium positioning, all of which contribute to competitive differentiation and sustained growth.

Key Market Developments

- In March 2024, L’Oréal S.A. expands its North Africa operations, including Libya, by strengthening its distribution network and introducing localized skincare solutions tailored to regional climate conditions. L’Oréal intensified its presence across the Libyan market by collaborating with regional distributors to improve product availability in major cities such as Tripoli, Benghazi, and Misrata.

- In May 2024, Groupe Rocher (Flormar) strengthens its premium positioning through luxury boutique expansion in Tripoli and Benghazi metropolitan areas. The brand invested in modern store formats, beauty advisory counters, and experiential product-testing zones to elevate customer engagement.

- In February 2024, Estée Lauder Companies increases investment in digital beauty activation and partners with Libyan distributors to introduce advanced skincare brands. Estée Lauder expanded the availability of its prestige brands, particularly Estée Lauder, Clinique, and M·A·C, through exclusive tie-ups with leading Libyan distributors

Companies Covered in Libya Cosmetics Market

- L'Oréal S.A.

- Staked Skincare Inc.

- Vichy Laboratoires

- The Estée Lauder Companies, Inc.

- Elizabeth Arden

- Groupe Rocher (Flormar)

- Hobby Cosmetics

- Suarez Company

- LILA Cosmetics

- Lorience Paris

- Joop

- Grupo PYD

- ParisVally

- Unilever PLC

- Procter & Gamble Co.

Frequently Asked Questions

Libya cosmetics market was valued at US$ 505.6 million in 2025 and is projected to reach US$ 765.3 million by 2032, representing a CAGR of 6.1% during the forecast period.

Primary demand drivers include post-conflict economic stabilization increasing consumer confidence, rising female workforce participation expanding purchasing power, Internet penetration enabling e-commerce adoption, and rising beauty trends influencing younger demographics through social media platforms.

Skincare Products command the dominant segment at approximately 38% market share, driven by harsh desert climate necessitating protective formulations, rising anti-aging consciousness, UV protection requirements, and consumer investment in complexion health supporting mainstream adoption.

Natural and organic cosmetics segment represents the highest-value opportunity growing at 12.3% CAGR through premium pricing power, sustainability consciousness, climate-specific botanical formulations, and regulatory certification standards supporting margin expansion and premium market positioning.

Market leaders include L'Oréal S.A. (France) with comprehensive skincare and color cosmetics portfolios, Groupe Rocher (Flormar) (France) with premium beauty positioning, and Vichy Laboratoires (France) leveraging dermatological expertise, collectively representing approximately 35-40% market concentration.