- Medical Devices

- Libya Critical Care Equipment Market

Libya Critical Care Equipment Market Size, Share, and Growth Forecast, 2026 – 2033

Libya Critical Care Equipment Market by Product Type (Therapeutic Devices, Patient Monitoring Devices, Diagnostic Devices, Other), Patient Population (Pediatric, Adults, Geriatric), and End-user Analysis (Hospitals, Specialty Clinics, Others), 2026 – 2033

Libya Critical Care Equipment Market Size and Trends Analysis

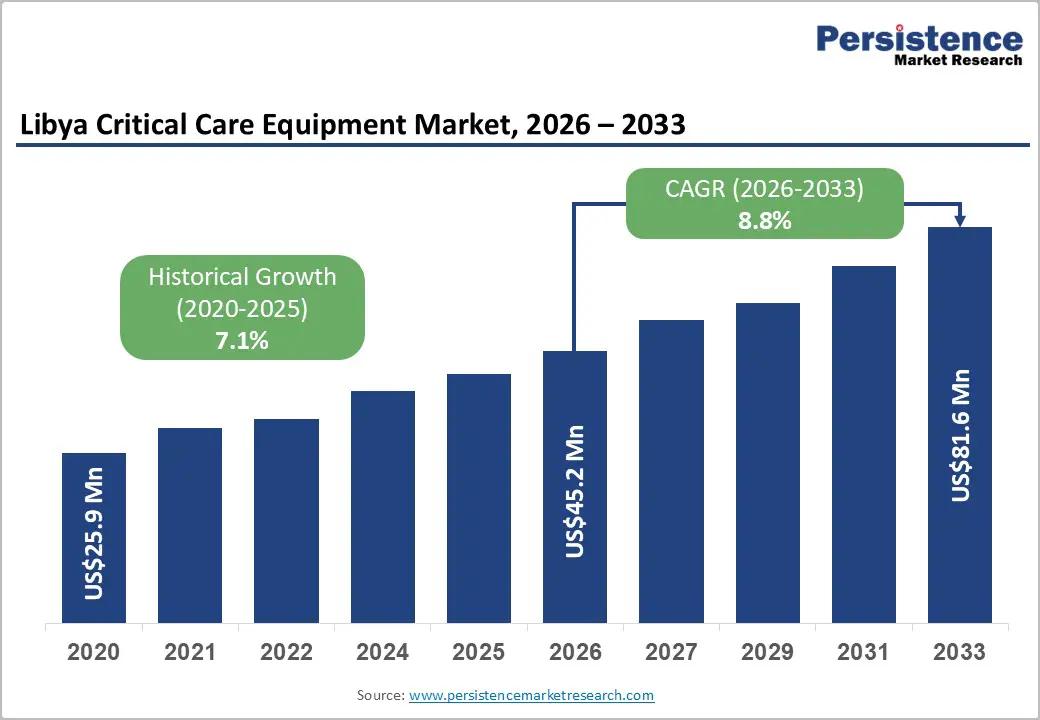

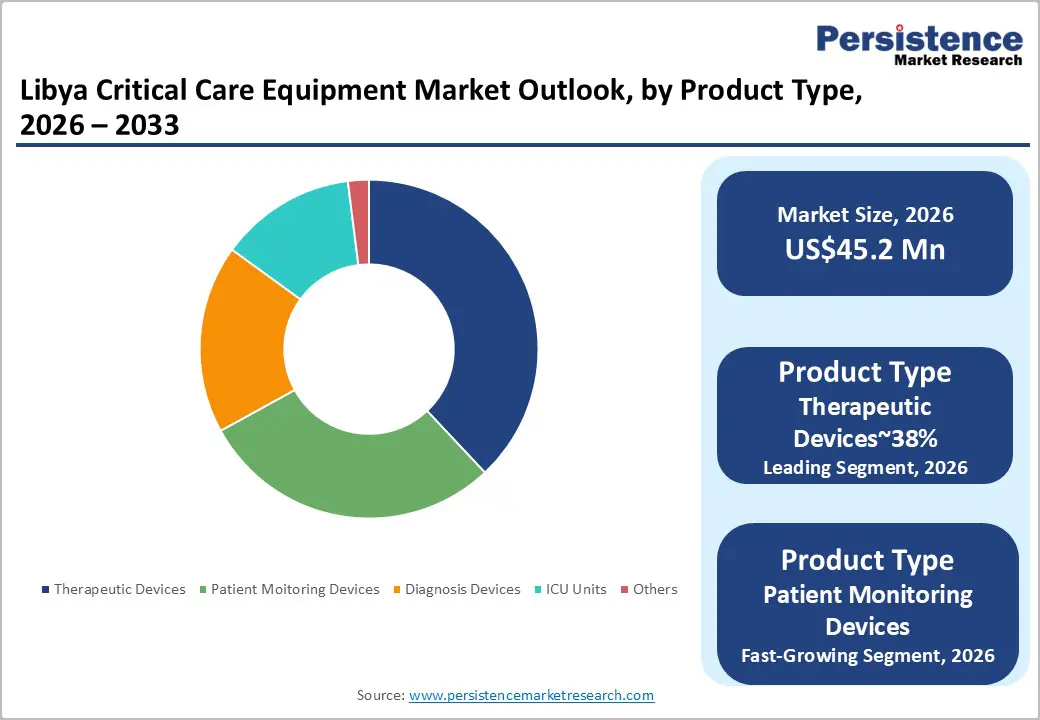

The Libya critical care equipment market size is likely to be valued at US$45.2 million in 2026 and is expected to reach US$81.6 million by 2033, growing at a CAGR of 8.8% during the forecast period from 2026 to 2033, driven by substantial investments in cutting-edge medical infrastructure and updated regulatory frameworks for healthcare technology.

Growth in the market is being fueled by a nationwide initiative for healthcare self-reliance and strategic international collaborations in high-value reconstruction projects. Growth stems from rising chronic disease prevalence, post-conflict healthcare infrastructure investments, and international aid for ICU enhancements. Libya relies heavily on imports for ventilators and monitoring systems, supported by WHO-led initiatives delivering essential equipment.

Key Industry Highlights:

- Leading Product Type: Therapeutic devices are expected to lead, accounting for approximately 38% share in 2026, supported by their critical role in life-support interventions such as ventilation, dialysis, and infusion therapy across intensive care environments.

- Fastest-growing Product: Patient monitoring devices are anticipated to grow the fastest, due to the rising adoption of continuous multi-parameter monitoring systems, digital ICU integration, and increasing demand for real-time patient data and early clinical deterioration detection.

- Leading End-user: Hospitals are projected to dominate due to centralized procurement, large ICU infrastructure, and continuous demand for advanced critical care equipment, holding approximately 67% share of the market in 2026.

- Fastest-Growing End-user: Specialty clinics are expected to grow the fastest as private healthcare investment expands, and decentralized care models emerge, driving demand for compact monitoring systems, transport ventilators, and high-dependency treatment units.

| Key Insights | Details |

|---|---|

|

Libya Critical Care Equipment Market Size (2026E) |

US$45.2 Mn |

|

Market Value Forecast (2033F) |

US$81.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

8.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Healthcare Infrastructure Rehabilitation and Modernization

The market is principally driven by extensive reconstruction of medical facilities impacted by past armed conflicts. Nearly half of primary healthcare centers have faced operational disruptions, prompting the Libyan Ministry of Health to implement the National Health Strategy. This strategy prioritizes restoring intensive care capacities, incorporating advanced ventilators, dialysis systems, and hemodynamic monitoring devices to enhance critical patient management. Support from international organizations such as the World Bank and UNDP has facilitated infrastructure upgrades, introducing modern hospital layouts and integrating specialized ICU technologies. Investment flows from foreign direct investment and large-scale government procurement programs further stimulate demand across both public and private healthcare networks, reinforcing systemic recovery.

The modernization trend encompasses regulatory alignment, safety certification compliance, and standardization of equipment procurement protocols, shaping the market’s operational framework. Technological evolution in ICU and emergency care devices encourages the adoption of multi-parameter monitoring systems and automated critical care workflows. The emphasis on upgrading outdated facilities also influences cost structures, creating opportunities for high-margin equipment deployment. Regional disparities in infrastructure recovery necessitate targeted strategies for equipment allocation, embedding efficiency and resilience into Libya’s emerging critical care ecosystem.

Technological Advancements and Digital Health Integration

Technological innovation is a primary catalyst for the market, driven by the adoption of AI-enabled diagnostics and tele-ICU solutions. These advancements address the persistent shortage of specialized intensivists, enabling remote patient monitoring and clinical decision support across geographically dispersed hospitals. Equipment with automated weaning protocols, simplified interfaces, and multi-parameter integration facilitates consistent care delivery, particularly in facilities with variable clinical expertise. Digital health records and interoperable bedside devices further improve operational efficiency, data accuracy, and patient safety, accelerating the replacement of legacy equipment across the healthcare network.

The shift toward digitalized ICU environments also influences regulatory and procurement practices, requiring alignment with national standards for medical device interoperability and data security. Technology-driven operational efficiencies reduce clinical errors while reshaping cost structures and investment priorities within hospital systems. The integration of telemedicine and connected monitoring solutions embeds resilience into critical care delivery, expanding adoption of sophisticated devices and reinforcing modernization objectives within Libya’s healthcare infrastructure. This convergence of digital tools and critical care equipment strategically enhances both service quality and systemic capacity.

Barrier Analysis – Political Instability and Economic Volatility

Libya’s healthcare system continues to face substantial challenges due to political instability, fragmented infrastructure, and inconsistent medical practices. Political uncertainty and economic volatility act as major restraints on the market, influencing government policies, healthcare budgeting, and procurement cycles. Frequent shifts in governance structures can lead to sudden changes in healthcare priorities, directly affecting the allocation of ICU equipment and the pace of hospital modernization initiatives. In addition, Libya’s heavy dependence on oil revenues makes the national healthcare budget highly vulnerable to fluctuations in global energy markets, creating ongoing fiscal uncertainty.

These conditions hinder long-term planning, complicate international tender processes, and introduce considerable operational risks for suppliers and healthcare administrators. The unstable environment often disrupts procurement timelines, leading to delayed payments and extended delivery schedules for imported medical technologies. Regulatory approvals may also be postponed or inconsistently enforced due to administrative changes, limiting the adoption of advanced critical care devices. Furthermore, currency fluctuations and inflationary pressures increase equipment costs and reduce purchasing power, influencing hospital investment decisions. Collectively, these political and economic constraints slow market expansion, restrict equipment deployment, and impede the development of a stable and sustainable critical care infrastructure across Libya.

Limited Technical Workforce and After-Sales Service Gaps

A structural restraint for the market is the shortage of specialized technical personnel capable of maintaining sophisticated medical systems. Advanced ventilators, hemodynamic monitors, and continuous renal replacement therapy platforms require routine calibration and preventive servicing to sustain clinical performance. However, healthcare facilities frequently depend on international service teams for maintenance and technical troubleshooting. This reliance increases operational expenditures and extends equipment downtime, disrupting intensive care workflows. Hospitals often face delays in restoring malfunctioning systems, which constrains operational continuity and reduces the reliability of critical care delivery.

Workforce shortages among trained nurses and biomedical technicians further limit the functional capacity of intensive care units. Even when hospitals possess modern equipment, operational utilization remains constrained due to insufficient staffing and technical oversight. The absence of localized after-sales service ecosystems also complicates technology transfer and user training for advanced devices. Political instability compounds these constraints by disrupting workforce development and recruitment initiatives across the healthcare system. Collectively, these structural gaps hinder optimal equipment utilization and slow the diffusion of complex critical care technologies throughout Libya’s hospital infrastructure.

Opportunity Analysis – Telemedicine Expansion and Remote Critical Care Monitoring

The expansion of telemedicine platforms and remote patient monitoring technologies presents a significant opportunity within the Libya critical care equipment market. Rural and geographically dispersed communities frequently encounter limited access to specialized intensive care services, creating demand for connected monitoring devices capable of transmitting real-time physiological data. Internet of Things-enabled vital signs tracking systems allow clinicians to supervise patients remotely while maintaining continuous observation across distributed healthcare facilities. This capability supports more efficient allocation of scarce clinical expertise and strengthens continuity of care for critically ill patients outside major urban hospitals.

Digital health infrastructure development following recent healthcare modernization initiatives is accelerating the adoption of interoperable monitoring equipment and tele-intensive care frameworks. Remote alert systems integrated with bedside monitors enhance early clinical intervention and reduce reliance on constant physical supervision within resource-constrained facilities. The integration of networked devices into hospital information systems also supports standardized patient records and coordinated treatment oversight. These operational efficiencies lower infrastructure pressures and create cost advantages compared with conventional intensive care models, positioning telemedicine-enabled monitoring systems as a scalable pathway for strengthening Libya’s critical care capacity.

Expansion of Private Healthcare and Public–Private Partnerships

The expansion of private healthcare infrastructure presents a structural opportunity for the Libya critical care equipment market. Public hospitals continue facing operational pressure due to infrastructure gaps and service demand imbalances. Consequently, private hospital groups are increasingly investing in advanced intensive care units and specialized treatment facilities. These investments focus on modern ventilatory support systems, hemodynamic monitoring technologies, and integrated critical care platforms. The objective is to attract affluent domestic patients and emerging medical travel flows seeking reliable tertiary services. Private sector participation also introduces greater procurement flexibility, enabling faster technology adoption compared with conventional public acquisition cycles.

Public–private partnerships are emerging as an operational mechanism for expanding intensive care capacity within the healthcare system. Through collaborative management structures, private operators can oversee ICU departments while public institutions maintain regulatory oversight and clinical governance. Such arrangements facilitate long-term equipment procurement, maintenance contracts, and lifecycle service agreements for technology providers. The partnership model also supports capital mobilization for facility modernization and specialized workforce training. Collectively, the growth of private healthcare networks and partnership frameworks strengthens investment flows and expands demand for advanced critical care technologies across Libya’s evolving hospital infrastructure.

Expansion of Homecare and Portable Critical Care Solutions

The transition of patients from intensive care units to structured home care environments is creating a new opportunity within the Libya critical care equipment market. Hospitals frequently experience pressure on limited intensive care capacity, encouraging healthcare providers to explore alternative care pathways for clinically stable patients requiring continued respiratory or physiological monitoring. Portable ventilators, compact patient monitoring systems, and connected oxygen support devices enable continuity of care outside conventional hospital settings. These technologies support earlier patient discharge while maintaining clinical supervision, thereby reducing strain on hospital infrastructure and improving operational efficiency across critical care facilities.

The evolution of integrated home monitoring ecosystems further strengthens this opportunity by combining portable hardware with cloud-enabled data management platforms. Connected devices capable of transmitting patient vitals to centralized monitoring hubs allow clinicians to maintain oversight without continuous physical presence. Such systems also support coordinated care between hospital specialists, home care providers, and community health services. The adoption of remote monitoring architectures improves patient safety while lowering operational burdens on hospitals. Consequently, portable critical care technologies are emerging as a complementary extension of institutional intensive care capacity within Libya’s evolving healthcare framework.

Category–wise Analysis

Product Type Insights

Therapeutic devices are projected to lead the market, accounting for approximately 38% share in 2026, supported by the urgent clinical shift toward active life-support intervention across hospital intensive care environments. Ventilators, dialysis platforms, and infusion pumps remain foundational technologies required for managing respiratory distress, renal failure, and complex medication delivery. Sustained demand is reinforced by heavy utilization cycles, environmental wear conditions, and expanding ICU bed capacity following pandemic-era infrastructure upgrades. Manufacturers such as Dräger, Hamilton Medical, Fresenius Medical Care, and Baxter anchor deployment through advanced ventilation platforms, dialysis systems, and connected infusion technologies integrated with hospital workflows. Government modernization initiatives and decentralized procurement across regional facilities further sustain equipment replacement cycles.

Patient monitoring devices are anticipated to be the fastest-growing segment, driven by the transition toward continuous data-driven clinical oversight across intensive and high-dependency care environments. Hospitals increasingly deploy multi-parameter bedside monitors and centralized monitoring stations to enable real-time visibility of patient vitals and early deterioration detection. Platforms from Mindray, Philips Healthcare, GE HealthCare, and Nihon Kohden integrate advanced analytics, wireless sensors, and interoperability features that support modern ICU digitalization strategies. Adoption is further accelerated by nursing shortages, encouraging automated early-warning scoring systems that expand patient management capacity without proportional staffing increases. Expansion of step-down units, mobile intensive care ambulances, and remote monitoring capabilities reinforces equipment demand, positioning connected monitoring systems as a critical enabler of proactive and scalable critical care delivery.

End-user Insights

Hospitals are projected to lead the market, accounting for approximately 67% share in 2026, reflecting the structural concentration of intensive care services within large public medical centers and teaching hospitals. Centralized procurement mechanisms managed by national health authorities prioritize high-capacity institutions capable of hosting advanced intensive care infrastructure and multidisciplinary treatment units. Major modernization programs across Tripoli and Benghazi are accelerating the installation of integrated ICU platforms combining ventilatory support, dialysis systems, and multi-parameter monitoring technologies. Leading manufacturers, including GE HealthCare, Siemens Healthineers, and Dräger, supply hospital-grade systems designed for continuous operation in high-acuity environments. This convergence of procurement scale, infrastructure readiness, and clinical training mandates secures hospitals as the dominant end-user segment.

Specialty clinics are anticipated to be the fastest-growing segment, supported by expanding private healthcare investments and the growing need for decentralized patient management models. Specialty cardiology and pulmonology clinics are increasingly establishing high-dependency care units equipped with compact monitoring systems, transport ventilators, and short-stay recovery infrastructure. Providers such as Mindray and Nihon Kohden supply advanced monitoring platforms that combine strong performance with flexible deployment across smaller facilities. Demand for portable critical care technologies is also rising within homecare environments as hospitals pursue earlier patient discharge strategies to relieve pressure on intensive care beds.

Competitive Landscape

The Libya critical care equipment market is moderately fragmented, with leadership concentrated among multinational medical technology suppliers supported by regional distribution networks. Global manufacturers, including GE HealthCare, Philips Healthcare, Medtronic, and Dräger, exert strong influence over procurement standards, clinical technology preferences, and hospital equipment configurations. Their significance stems from extensive portfolios spanning ventilation platforms, patient monitoring systems, and integrated intensive care solutions that align with complex hospital requirements. Market access is largely mediated through local distributors such as IMEC and other specialized import partners that manage logistics, installation, and training.

Competitive positioning within the market is defined by the ability to combine advanced hardware platforms with lifecycle service capabilities and localized technical support. Leading manufacturers differentiate through integrated product ecosystems linking ventilators, monitoring systems, and hospital information platforms into unified clinical workflows. The Libya critical care equipment market is dominated by a mix of Global Original Equipment Manufacturers (OEMs) who provide the high-end technology and Tier-1 Local Distributors who navigate the complex regulatory and tender landscape of the Ministry of Health (MoH).

Key Industry Developments:

- In February 2026, Healthcare Infrastructure launched the "100 Days for Priority Reforms" strategy to inaugurate over 20 new health facilities nationwide. This initiative creates a massive, immediate demand for newly equipped Intensive Care Units (ICUs) and emergency monitoring systems to populate these modernized facilities.

- In January 2026, GKSD Holding and San Donato Group finalized a US$2 billion agreement to modernize the Benghazi Medical Center, establishing an Italian-led technology standard for future regional healthcare tenders. This partnership triggers a significant replacement cycle for critical care infrastructure, creating high-entry barriers for competitors.

- In December 2025, Medical Regulatory Affairs launched the first national pharmacovigilance system to track medical device safety and performance. Stricter oversight favors established global brands with robust safety data, potentially squeezing out low-cost, uncertified competitors from public tenders.

Companies Covered in Libya Critical Care Equipment Market

- GE HealthCare

- Philips Healthcare

- Medtronic

- Drägerwerk AG & Co. KGaA

- Getinge AB

- Siemens Healthineers

- Baxter International

- Fresenius Medical Care

- Mindray Medical

- Nihon Kohden

- Hamilton Medical

- ICU Medical

- B. Braun Melsungen AG

- Fisher & Paykel Healthcare

- Smiths Medical

- IMEC Ltd.

Frequently Asked Questions

The Libya critical care equipment market is projected to be valued at US$45.2 million in 2026 and is expected to reach US$81.6 million by 2033, supported by large-scale healthcare infrastructure reconstruction, international funding initiatives, and increasing demand for advanced intensive care technologies across hospitals and specialized medical facilities.

Government-led initiatives under the national health strategy, supported by international organizations and foreign investment, are focused on restoring intensive care capacity with modern ventilators, dialysis systems, and advanced patient monitoring technologies.

The Libya critical care equipment market is forecast to grow at a CAGR of 8.8% from 2026 to 2033, reflecting increasing investments in hospital modernization, rising prevalence of chronic diseases requiring intensive care, and expanding adoption of digital health technologies such as tele-ICU platforms and connected patient monitoring systems.

Hospitals represent the leading end-user segment, accounting for approximately 67% of the market share in 2026. Large public hospitals and teaching institutions remain the central hubs for intensive care delivery, supported by government procurement programs and the modernization of major medical centers in cities such as Tripoli and Benghazi.

The Libya critical care equipment market is moderately fragmented, with key global medical technology companies including GE HealthCare, Philips Healthcare, Medtronic, Drägerwerk AG & Co. KGaA, Siemens Healthineers, Baxter International, Fresenius Medical Care, Mindray Medical, Nihon Kohden, and Hamilton Medical.