- Beauty & Personal Care

- Anti-aging Products Market

Anti-aging Products Market Trends, Size, Share, and Growth Forecast, 2025 - 2032

Anti-aging Products Market By Product Type (Facial Serum, Moisturizer, Creams, and Lotions), Device and Technology (Microdermabrasion, Aesthetic Energy Devices), Distribution Channel (Supermarkets/Hypermarkets), and Regional Analysis for 2025 - 2032

Anti-aging Products Market Size and Trends Analysis

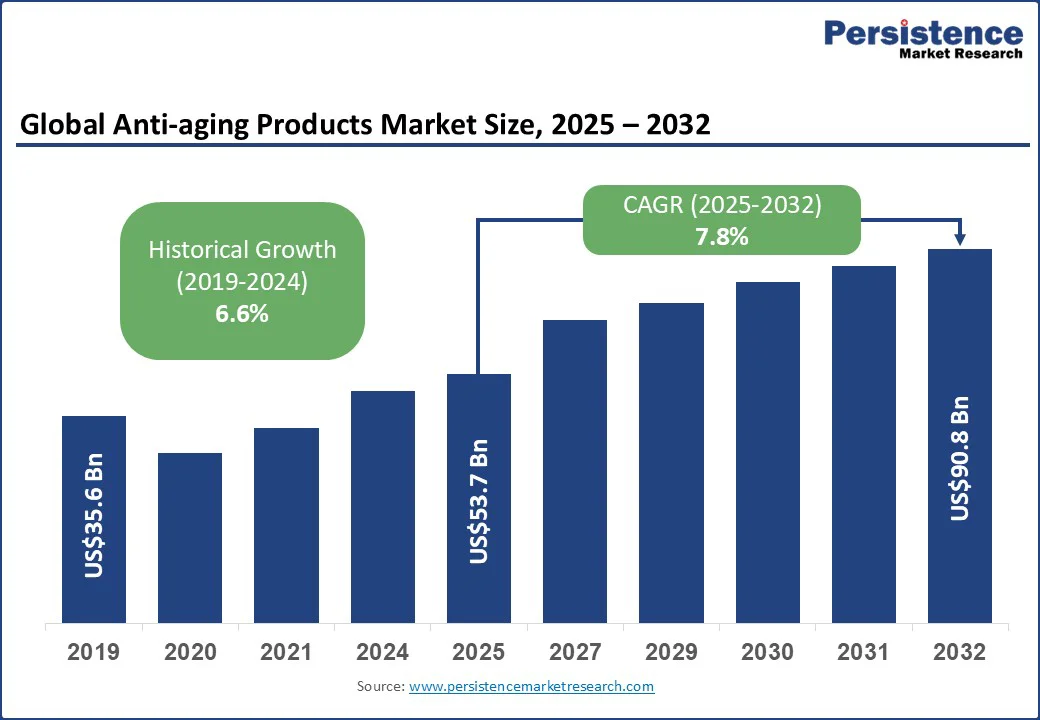

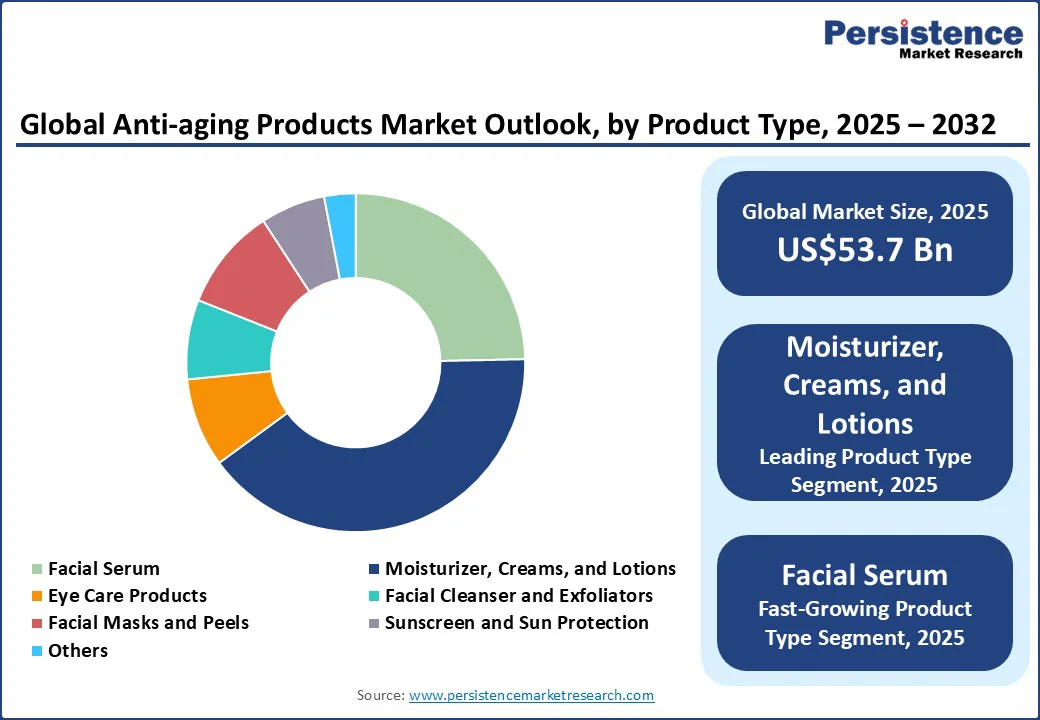

The global anti-aging products market size is likely to be valued at US$53.7 Bn in 2025 and is estimated to reach US$90.8 Bn in 2032, growing at a CAGR of 7.8% during the forecast period 2025 - 2032 due to the increasing desire for preventive and corrective skincare across age groups.

Key Industry Highlights:

- Leading Product Type: Moisturizers, creams, and lotions hold nearly 40.3% share in 2025, as they provide easy-to-use, daily hydration with added anti-aging actives.

- Dominant Device and Technology: Microdermabrasion devices, which are projected to account for approximately 58.5% of the anti-aging products market share in 2025, as these deliver professional-level exfoliation and skin renewal at home.

- Device Approval: South Korea-based Classys secured the European Union approval for its anti-aging device Volnewmer. It became the first company to receive CE Medical Device Regulation (MDR) certification for a radiofrequency-based aesthetic system.

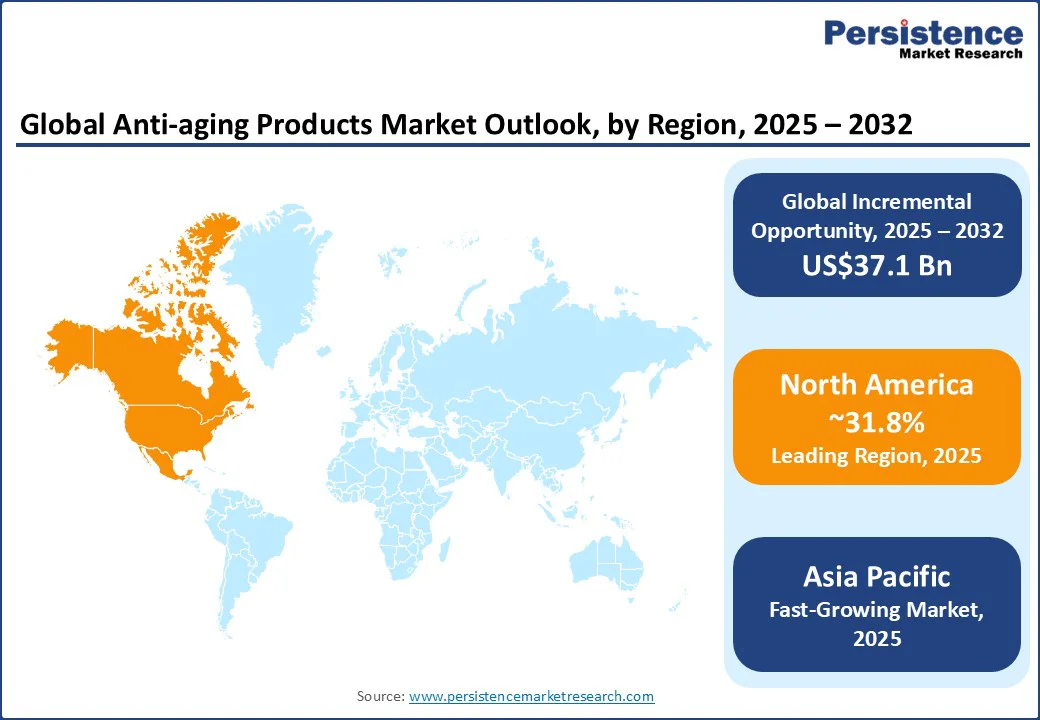

- Leading Region: North America, with about 31.8% share in 2025, owing to the adoption of both topical and device-based anti-aging solutions.

- Fastest-growing Region: Asia Pacific, backed by the acceptance of novel skincare and clinic-adjacent products.

| Global Market Attribute | Key Insights |

|---|---|

| Anti-aging Products Market Size (2025E) | US$53.7 Bn |

| Market Value Forecast (2032F) | US$90.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Celebrity-led Skincare Launches Turn Anti-aging into a Mainstream Cultural Movement

Celebrity-led brands are transforming the market by making products aspirational yet relatable. When figures such as Hailey Bieber, Brad Pitt, or Pharrell Williams launch skincare lines, it endorses positivity, lifestyle influence, and massive social reach into the category.

This has shifted anti-aging from a niche or clinical conversation to a mainstream cultural topic. For instance, Brad Pitt’s Beau Domaine launched in Europe with grape-derived antioxidants and positioned aging as graceful rather than something to be hidden. Such endorsements create trust, accelerate awareness, and push consumers to adopt preventive routines earlier.

Pollution-protective anti-aging solutions are also gaining popularity, mainly in urbanized areas of the Asia Pacific, where air quality concerns are high. These products combine traditional wrinkle-fighting actives with ingredients that shield skin from particulate matter, free radicals, and blue light exposure.

For instance, Shiseido’s Ultimune Power Infusing Concentrate was recently reformulated to emphasize defense against environmental stressors. By linking anti-aging to everyday concerns, including smog or screen exposure, brands are making their products feel more relevant.

Premium Brands Face Pressure to Justify Pricing or Lose Young Buyers

The lack of approval from the Food and Drug Administration (FDA) and limited clinical testing creates a trust gap among consumers, particularly in the U.S., where buyers are growing increasingly cautious about long-term safety.

Gen Z and young millennials are questioning the rush to use retinol and other strong actives early, as dermatologists warn that premature use can damage the skin barrier. A peer-reviewed study in Pediatrics recently found that skincare routines promoted to young teens on TikTok often involve multiple products and tend to result in irritation, allergic reactions, or other harm.

Financial strain is another deterrent. Anti-aging routines often involve multi-step regimens with premium creams, serums, and devices, which can be costly. Several young buyers are now opting for simple and budget-friendly routines focusing on sunscreen and moisturizers rather than investing in expensive anti-aging products. This has pressured luxury and premium brands to justify their pricing or risk losing young consumers.

Rising Acceptance of Men’s Skincare Creates Growth Opportunities

The surging acceptance of men’s skincare as part of self-care is creating new opportunities for anti-aging brands to broaden beyond the traditionally female-focused market. Gen Z men are rejecting the stigma around beauty routines and instead see skincare as part of wellness and self-expression. This gives brands the chance to design products with gender-neutral packaging, light textures, and multi-functional benefits that appeal to men without alienating women.

In June 2024, Cetaphil launched a digital campaign titled "Made For Phil" to encourage men to embrace skincare confidently. Premiering during the week of Father's Day, the campaign featured two hero videos on Cetaphil's social channels introducing the humorous Ceta Six Pack and the versatile CetaGrill.

This shift also creates fresh storytelling opportunities. Featuring male models in ad campaigns for serums, eye creams, or SPF-based anti-aging moisturizers helps normalize usage and broaden the consumer base.

Category-wise Analysis

Product Type Insights

By product type, the market is divided into facial serum, moisturizer, creams, and lotions, eye care products, facial cleanser and exfoliators, facial masks and peels, sunscreen and sun protection, and others. Among these, moisturizers, creams, and lotions are highly preferred as they fit perfectly into daily routines without requiring lifestyle changes or specialized knowledge.

Most consumers already use a moisturizer, and hence, anti-aging creams an easy swap-in that doesn't feel like an additional step. This convenience factor makes them ideal for long-term use, thereby recording a share of nearly 40.3% in 2025.

Anti-aging facial serums are gaining momentum as they deliver concentrated doses of active ingredients directly into the skin with lightweight textures that absorb quickly.

They penetrate deep layers, making them attractive for consumers who want quick and visible results from ingredients such as vitamin C, retinol, or hyaluronic acid. Serums can also be layered and mixed depending on specific concerns, including fine lines, dark spots, dehydration, or dullness. This gives consumers a sense of control over their regimen.

Device and Technology Insights

In terms of device and technology, the market is bifurcated into microdermabrasion devices and aesthetic energy devices. Out of these, microdermabrasion devices are poised to account for a 58.5% share in 2025, as they provide visible and salon-like results at home, giving users a smooth texture and a reduced appearance of fine lines without invasive procedures.

These deliver immediate exfoliation and radiance, which appeals to consumers looking for quick transformations. They are also favored due to their ability to stimulate natural skin renewal by removing dead cells and promoting collagen production.

Aesthetic energy devices are seeing steady growth due to their ability to provide minimally invasive solutions that bridge the gap between topical skincare and surgical procedures. Consumers now seek visible anti-aging results without downtime.

Technologies such as radiofrequency, ultrasound, and fractional lasers deliver skin tightening, wrinkle reduction, and collagen stimulation with far less recovery compared to facelifts. In addition, consumers in their late 20s and 30s are turning to such preventive procedures to delay visible aging, not just correct it later.

Regional Insights

North America Anti-aging Products Market Trends - High Demand for Science-backed Skincare Fuels Growth

In 2025, North America is likely to account for a 31.8% share as it is considered one of the most advanced markets with a high demand and known for science-backed skincare. Modern consumers are willing to pay a premium for visible results. The region is home to renowned players such as Estée Lauder, L’Oréal, and Procter & Gamble, who continue to dominate with superior brand diversification as well as research and development.

In the U.S. anti-aging products market, both large incumbents and fast-growing indie brands are pushing growth. Leading players are broadening their presence through acquisitions, while small-scale direct-to-consumer firms are attracting attention with transparent ingredient lists and viral social media campaigns.

Consumers also combine topical products with in-office procedures, making the U.S. a key hub for crossover between clinical aesthetics and home-use skincare.

In Canada, the market is smaller but more regulation-sensitive, with consumers showing trust in dermatologist-approved brands. Seoul-based Aestura, for example, recently debuted in Sephora Canada with its ATOBARRIER365 collection, bringing dermocosmetic solutions for sensitive skin to local consumers.

Asia Pacific Anti-aging Products Market Trends - South Korea’s K-beauty Revolution Directs Global Product Development

Asia Pacific is one of the fastest-evolving regions for anti-aging cosmetic products owing to its diverse demographics and consumer preferences. Japan and China have large aging populations, while South Korea propels product development that influences global trends.

E-commerce, livestream shopping, and social media accelerate product adoption, making the Asia Pacific a growth engine and a testing ground for new formulations. In China, demand is shifting from basic cosmetics to what consumers call light medical beauty.

It refers to products and devices that deliver clinical-grade results without invasive treatments. Livestream platforms, including Douyin and Taobao, have become key sales channels, where brands can achieve viral success overnight if backed by dermatologists or Key Opinion Leader (KOL) endorsements.

South Korea remains a major hub with K-beauty augmenting ingredient-first anti-aging solutions such as gentle retinoids, peptides, and novel delivery systems. For example, in 2025, Meditherapy’s Retinal Skin Booster Serum rapidly achieved social media popularity as users shared their experiences widely on TikTok.

Europe Anti-aging Products Market Trends - France’s Luxury-pharmacy Blend Influences Consumer Preference for Sensorial Products

Clinical credibility, strict regulations, and consumer trust in pharmacy and dermocosmetic brands influence Europe’s beauty industry. Buyers in the region place heavy emphasis on safety, proven results, and dermatological approval.

This makes brands such as La Roche-Posay, Vichy, and Eucerin staples across pharmacies. The anti-aging ingredients market is steadily growing as the aging population expands. Still, it is also diversifying into new categories such as SPF-based anti-aging and biotech-backed actives.

In the U.K., the demand for high-performance yet accessible brands has led to a surge in clinically positioned indie players. A notable example is L’Oréal’s 2025 majority stake acquisition of Medik8, a Borehamwood-based brand focused on vitamin A formulations.

This shows how global giants are tapping into the U.K.’s thriving science-based skincare ecosystem. France remains a leader in dermocosmetics, where consumers combine luxury sensorial experiences with pharmacy-backed trust. Germany shows a preference for technically advanced formulations and eco-conscious positioning.

Competitive Landscape

The global anti-aging products market is highly competitive, with global giants such as L’Oréal, Estée Lauder, and Shiseido dominating through acquisitions and brand diversification. These companies are broadening their portfolios to capture both premium and affordable segments.

Competition is also fueled by a race around ingredients and science-backed formulations. Brands are investing in biotech-derived actives such as peptides, NAD+ boosters, and stabilized retinol to stand out with superior clinical credibility. Small indie and direct-to-consumer brands are disrupting the market with affordable, transparent, and ingredient-first ranges.

Key Industry Developments:

- In March 2025, Chemyunion launched a next-generation tetrapeptide called Peptid4 B-Like. It provides a sustainable and high-performance alternative for wrinkle reduction. Its cost-effective production ensures affordability without compromising purity and performance.

- In January 2025, Shiseido introduced a new, refillable anti-aging serum named the Ultimune Power Infusing Serum. Its main ingredient is a concentrated extract of Japanese camellia that hails from Gotoh Island. This launch aims to help the company strengthen its position in skin care.

Companies Covered in Anti-aging Products Market

- Unilever PLC

- The Procter & Gamble Company

- Beiersdorf AG

- L'Oréal S.A.

- The Estée Lauder Companies Inc.

- Oriflame Holding AG

- Avon Products, Inc.

- Shiseido Company, Limited

- PMD Beauty (Age Sciences Inc.)

- Revlon, Inc.

- Allergan plc

Frequently Asked Questions

The anti-aging products market is projected to reach US$53.7 Bn in 2025.

Rising consumer focus on preventive skincare and surging disposable income are the key market drivers.

The anti-aging products market is poised to witness a CAGR of 7.8% from 2025 to 2032.

Expansion into men’s grooming and the launch of multifunctional products are the key market opportunities.

Unilever PLC, The Procter & Gamble Company, and Beiersdorf AG are a few key market players.