- Retail

- Mycelium Leather Market

Mycelium Leather Market Size, Share, and Growth Forecast, 2026 - 2033

Mycelium Leather Market by Product Type (Dyed Mycelium Leather, Unstained Mycelium Leather, Others), Application (Bags, Footwear, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Mycelium Leather Market Size and Trends Analysis

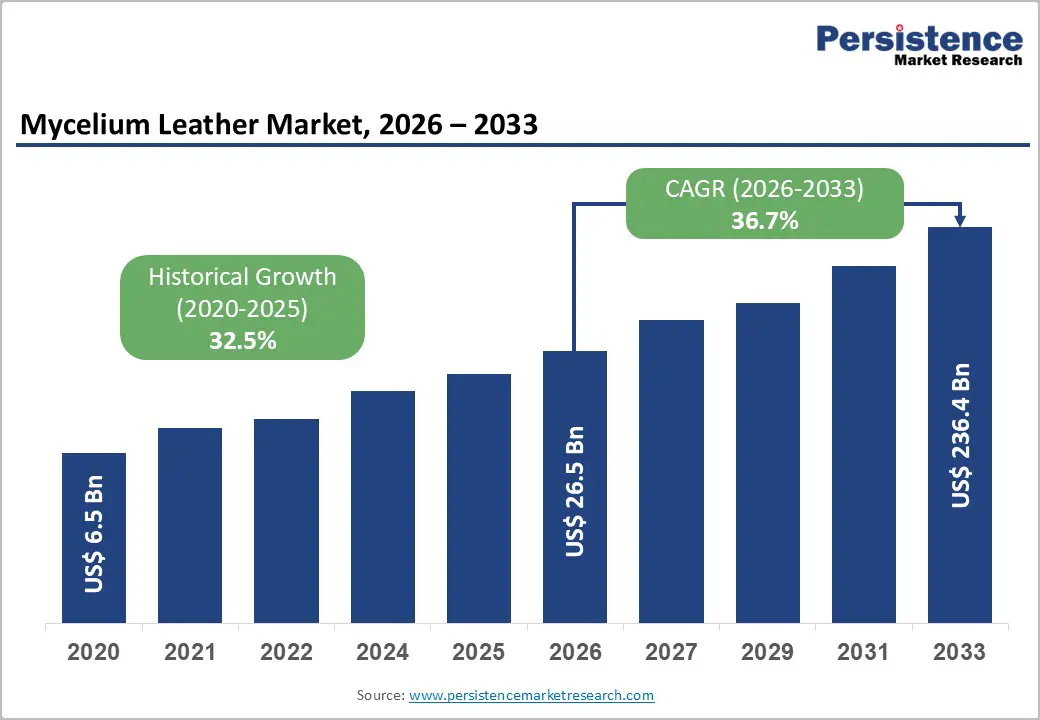

The global mycelium leather market size is likely to be valued at US$26.5 billion in 2026 and is expected to reach US$236.4 billion by 2033, growing at a CAGR of 36.7% between 2026 and 2033, driven by increasing brand commitments to animal-free materials, advancements in scalable mycelium cultivation and processing technologies, and the emergence of a broader supplier ecosystem that is gradually lowering production costs.

Key Industry Highlights

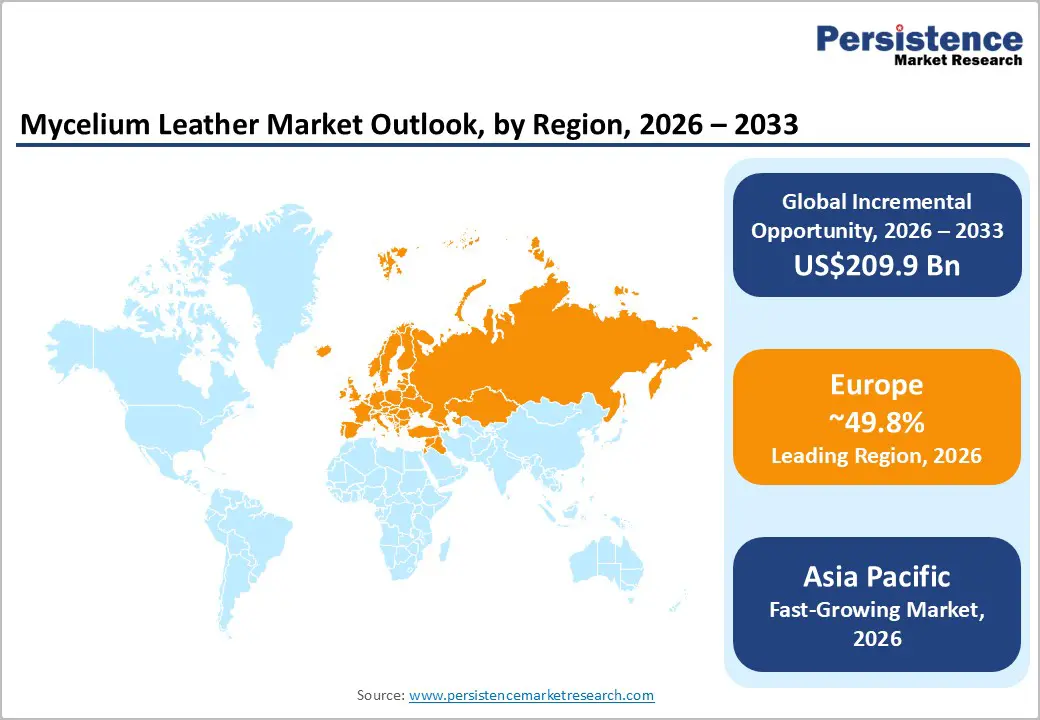

- Leading Region: Europe is projected to account for approximately 49.8% of the global market share, supported by strong demand for luxury fashion, harmonized sustainability regulations under the EU Green Deal, and active public-private innovation programs.

- Fastest-growing Region: Asia Pacific, projected to register the highest growth rate over the forecast period, driven by scalable manufacturing capabilities, cost-efficient production ecosystems, and rising domestic demand for sustainable materials across China, India, and ASEAN countries.

- Investment Plans: Capital deployment focuses on pilot-to-commercial-scale manufacturing, cultivation optimization, and finishing technologies, with the majority of investments concentrated in North America and Europe, where startups and material innovators are expanding capacity through brand partnerships and technology licensing.

- Dominant Product Type: Dyed mycelium leather is anticipated to hold approximately 54.5% market share, owing to its color stability, surface uniformity, and seamless integration into existing fashion, footwear, and accessories manufacturing processes.

- Leading Application: Bags are estimated to account for around 38.2% of market share, as handbags and accessories remain the primary commercialization pathway due to their premium pricing potential, manageable production volumes, and strong consumer acceptance.

| Key Insights | Details |

|---|---|

| Mycelium Leather Market Size (2026E) | US$26.5 Bn |

| Market Value Forecast (2033F) | US$236.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 36.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 32.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Large Brand Adoption and Procurement Commitments

Major fashion, footwear, and lifestyle brands are increasingly piloting mycelium leather across limited-edition and capsule collections, signaling early procurement intent and long-term sourcing potential. These collaborations validate material performance, aesthetics, and consumer acceptance, reducing perceived adoption risk for broader commercial rollouts. Brand-backed pilots often serve as qualification programs that convert experimentation into structured supply agreements for bags, footwear, and accessories. From a market perspective, such programs accelerate time-to-scale by anchoring demand before full-capacity investments are completed. Suppliers engaging with multiple brand programs have demonstrated faster revenue ramp-up, indicating that brand-led commercialization remains one of the most critical demand-side growth catalysts.

Advances in Production Science and Cost Reduction

Ongoing improvements in substrate optimization, controlled-environment cultivation, and downstream processing have significantly reduced production cycle times and labor intensity. Several producers have progressed from weeks-long laboratory growth cycles to industrial-scale processes completed in days, improving throughput and yield consistency. Advances in coating, dyeing, and texturing technologies have further enhanced material durability and aesthetic consistency, enabling broader application suitability. These innovations are translating into measurable cost reductions per square meter, narrowing the price gap with animal leather and premium synthetic alternatives. As scale facilities mature, economies of scale are reinforcing a downward cost curve, supporting wider commercial adoption.

Regulatory and ESG Pressure Favoring Biobased Materials

Corporate sustainability commitments and environmental regulations are reshaping material procurement strategies across consumer goods, automotive, and furniture sectors. Companies are increasingly aligning sourcing decisions with carbon reduction, biodiversity preservation, and animal welfare goals. Procurement frameworks are prioritizing lower-impact, biobased alternatives for interiors and consumer-facing products. Public and private sustainability initiatives, including green procurement guidelines and environmental reporting standards, are indirectly supporting demand for mycelium leather. Compared to conventional bovine leather and many petroleum-based synthetics, mycelium leather aligns more closely with lifecycle impact reduction objectives, prompting gradual reallocation of procurement budgets toward alternative leather materials.

Barrier Analysis - Scale and Feedstock Supply Constraints

Despite technological progress, the availability of consistent, large-scale feedstock and cultivation infrastructure remains a structural challenge. Many producers depend on localized agricultural residues or wood-based substrates, which are subject to seasonal variability and logistical limitations. These constraints can create production bottlenecks and input price volatility as volumes scale. In several cases, facility ramp-up timelines have been adjusted due to feedstock sourcing challenges or infrastructure readiness, resulting in modest short-term reductions in expected output. Until feedstock supply chains are fully industrialized, scale-related risks will continue to affect near-term capacity expansion.

Commercialization, Economics, and Capital Cycles

Scaling mycelium leather production requires substantial upfront investment in controlled growth environments, processing equipment, and quality assurance systems. While brand interest remains strong, access to growth capital fluctuates with broader investment cycles. Periods of investor caution have led some high-profile projects to pause or restructure production plans, slowing commercialization momentum. Funding gaps can increase unit costs and delay breakeven timelines, underscoring the sector’s sensitivity to capital availability. This dynamic represents a near-term restraint, even as long-term demand fundamentals remain favorable.

Opportunity Analysis - Automotive Interiors and High-Value Upholstery

Automotive manufacturers are actively evaluating animal-free interior materials to support sustainability targets and evolving consumer preferences. Mycelium leather can be engineered to meet performance requirements for abrasion resistance, fire safety, and tactile quality, positioning it for use in seating and interior panels. Even limited penetration into automotive interiors represents a significant revenue opportunity due to long contract durations and high-volume requirements. If automotive applications capture a small share of the broader alternative leather market by 2030, suppliers that achieve OEM qualification could access multi-hundred-million-dollar revenue streams supported by long-term supply agreements.

Emerging Markets and Localized Manufacturing

Asia Pacific offers a compelling opportunity for localized mycelium leather production due to its proximity to global apparel and footwear manufacturing hubs. Establishing regional production facilities can reduce logistics costs, shorten lead times, and lower carbon intensity while serving both export-oriented manufacturers and growing domestic brands. Adoption across China, India, and the ASEAN markets is expected to grow rapidly as sustainability awareness increases. Local joint ventures, licensing agreements, and contract manufacturing models present scalable pathways for market entry while mitigating capital intensity for technology owners.

Category-wise Analysis

Product Type Insights

Dyed mycelium leather is anticipated to remain the leading product type, accounting for approximately 54.5% of the market share during the forecast period. Early commercialization strategies across the mycelium leather ecosystem prioritized dyed and fully finished materials that could integrate seamlessly into existing luxury and premium product lines, particularly handbags, footwear, and small accessories. Superior color consistency, surface uniformity, and compatibility with established fashion palettes made dyed variants the most viable option for first-generation launches. Companies such as Bolt Threads (Mylo™) and MycoWorks (Reishi™) have focused heavily on dyed formats to meet brand requirements from partners like Adidas, Stella McCartney, and Hermès. Continued investments in finishing, coating, and durability-enhancement technologies have improved abrasion resistance and lifecycle performance, reinforcing dyed mycelium leather’s dominant commercial position.

Unstained mycelium leather is anticipated to be the fastest-growing product segment over the forecast period, driven by rising demand from premium, eco-luxury, and artisanal brands seeking minimally processed, bio-authentic materials. Unstained variants emphasize natural textures, organic coloration, and biodegradability, aligning strongly with circular design narratives and transparent sourcing commitments. Advances in cultivation control, surface smoothing, and gentle finishing techniques have improved material consistency without compromising sustainability credentials. Designers increasingly position unstained mycelium leather as a statement material in limited-edition footwear, handbags, and interiors, commanding higher average selling prices despite lower volumes. As consumer awareness of material provenance increases, unstained mycelium leather is expected to capture incremental share, particularly within luxury and bespoke segments.

Application Insights

Bags are anticipated to remain the largest application segment, accounting for approximately 38.2% of market share. Handbags, totes, and small leather goods offer an optimal entry point for mycelium leather adoption, with manageable production volumes, lower mechanical stress requirements, and strong visual differentiation. Luxury and premium brands have successfully leveraged bags as flagship products to introduce mycelium leather to consumers, often through capsule collections and limited releases. Examples include premium handbags and accessories launched by MycoWorks’ brand partners and Bolt Threads’ collaborations with luxury fashion houses. The category benefits from high margins, repeat purchase cycles, and strong storytelling potential, supporting stable demand and long-term commercial viability.

Footwear is expected to be the fastest-growing application segment and capture an increasing share of total demand over the forecast period. Recent product launches across sneakers, casual footwear, and lifestyle shoes demonstrate that mycelium leather can be integrated into existing footwear manufacturing processes with minimal retooling. Brands such as Adidas and other performance-lifestyle players have validated material performance in uppers, panels, and overlays. Rising production volumes, improved tear resistance, and enhanced moisture management are accelerating adoption. Footwear’s higher unit throughput than bags positions it as a critical lever for scaling volume for mycelium leather suppliers, making it a key growth engine as the market transitions from pilot programs to broader commercialization.

Regional Insights

North America Mycelium Leather Market Trends - Innovation-Led Commercialization Driven by Venture Capital and Brand Validation

North America, led by the U.S., remains a critical hub for mycelium leather innovation and commercialization, underpinned by a strong venture capital ecosystem, advanced biomaterials research, and early brand partnerships. The U.S. accounts for the majority of regional activity, with investment concentrated in pilot-scale manufacturing, strain optimization, and downstream processing technologies. Companies such as Bolt Threads (California) and MycoWorks (California) have anchored the regional ecosystem through proprietary cultivation platforms and strategic collaborations with global fashion and footwear brands. Bolt Threads’ Mylo™ material, for example, has been integrated into footwear and accessories through partnerships with Adidas and Stella McCartney, validating performance standards and accelerating downstream adoption.

The regulatory environment in North America emphasizes product safety, labeling transparency, and material performance compliance, overseen by agencies such as the U.S. Consumer Product Safety Commission and state-level environmental authorities. While sustainability regulation remains less prescriptive than in Europe, state-led incentives in California, New York, and Oregon have supported bio-based manufacturing, clean-tech R&D, and low-emission production models. These policies have encouraged continued capital inflows into mycelium-based materials, particularly for applications in footwear, accessories, and automotive interiors. As a result, North America plays a pivotal role in technology validation, IP development, and early commercialization, shaping global standards for mycelium leather performance and scalability.

Europe Mycelium Leather Market Trends - Regulatory-Backed Luxury Adoption and Public-Private Scale-Up

Europe is projected to lead the market with approximately 49.8% market share, driven by the region’s strong luxury fashion ecosystem, harmonized sustainability regulations, and structured public-private innovation programs. Countries including Germany, the U.K., France, and Spain occupy complementary positions across the value chain. France and Italy act as demand centers through luxury fashion houses and premium accessories brands, while Germany and the U.K. contribute advanced materials testing, automotive interior validation, and applied research capabilities. European fashion leaders have increasingly integrated mycelium leather into pilot collections, reinforcing market credibility and accelerating supplier onboarding.

Regulatory clarity has been a decisive growth enabler. The EU Green Deal, Ecodesign directives, and forthcoming Digital Product Passport requirements have strengthened confidence in bio-based materials by standardizing environmental claims and lifecycle transparency. This has reduced buyer risk for brands evaluating alternatives to animal leather and synthetic PU. Companies such as MycoWorks have expanded engagement with European luxury groups, while regional material innovators have benefited from EU-funded research programs focused on bio-fabrication and circular textiles. Spain’s growing role in textile finishing and France’s luxury manufacturing expertise further support scale-up. Europe’s leadership position reflects not only demand strength, but also a regulatory and institutional framework that actively accelerates adoption across fashion, automotive, and premium consumer goods.

Asia Pacific Mycelium Leather Market Trends - Manufacturing-Scale Expansion Enabled by Cost Efficiency and Policy Support

Asia Pacific is the fastest-growing regional market for mycelium leather, supported by manufacturing scale, cost efficiency, and rising domestic demand for sustainable materials. China, India, and ASEAN countries are emerging as strategic hubs for localized production, processing, and supply-chain integration. The region’s established textile, footwear, and synthetic leather infrastructure enables mycelium leather producers to transition from pilot to commercial-scale operations more rapidly than in Western markets. Asian contract manufacturers are increasingly engaging with mycelium leather developers to adapt existing equipment for the production of bio-based materials.

Government support has further accelerated adoption. China’s broader push toward green manufacturing and bio-economy development, alongside India’s initiatives promoting sustainable textiles and startup innovation, has created favorable conditions for material innovation. International brands sourcing from Asia-Pacific have begun evaluating mycelium leather for footwear and accessories to reduce supply-chain emissions and improve sustainability disclosures. ASEAN countries, particularly Vietnam and Indonesia, are benefiting from rising demand for footwear and accessories, positioning mycelium leather as a next-generation alternative material. As consumer awareness of sustainability grows across urban Asia, the region is expected to play a central role in volume scaling, cost optimization, and long-term global supply expansion for mycelium leather.

Competitive Landscape

The global mycelium leather market remains early-stage but is consolidating around a small group of technology leaders and regional manufacturers. Competition centers on proprietary cultivation processes, finishing capabilities, and strategic brand relationships. The market exhibits moderate concentration, with ongoing experimentation in licensing, joint ventures, and contract manufacturing models. Recent years have seen increased focus on commercialization, restructuring of capital-intensive operations, and a shift toward asset-light production models. Brand collaborations continue to play a central role in validating use cases and accelerating adoption across categories. Leading players emphasize performance optimization, vertical partnerships, and selective brand engagement. Emerging firms focus on cost control, feedstock security, and rapid certification to access automotive and furniture markets.

Key Industry Developments

- In October 2025, Hyundai Motor Group and Toray Industries signed a strategic joint development agreement to advance high-performance composite materials for future mobility applications, aiming to enhance lightweight design and material efficiency in electric vehicles and next-generation platforms.

- In October 2025, Hyundai and Toray Industries expanded their composite material collaboration to deepen research on carbon fiber-reinforced solutions across automotive applications, reinforcing commitments to sustainable mobility and advanced lightweight structures.

Companies Covered in Mycelium Leather Market

- Bolt Threads

- MycoWorks

- Ecovative Design

- Modern Meadow

- Mycelium Materials Europe

- Ananas Anam

- Mogu S.r.l.

- Circular Systems

- MycoFutures

- MycoTex

- Biohm

- Grown.bio

- Boltaron

- Spiber

- Natural Fiber Welding

- Vivobarefoot

- Stella McCartney

- Adidas

Frequently Asked Questions

The global mycelium leather market size is valued at US$26.5 billion in 2026.

By 2033, the mycelium leather market is expected to reach US$236.4 billion.

Key trends include rising demand for sustainable and animal-free leather alternatives, increased collaboration between biomaterial startups and luxury brands, technological advancements in cultivation and finishing processes, and growing adoption in footwear and automotive interiors alongside fashion accessories.

Dyed mycelium leather is the leading product type segment, accounting for approximately 54.5% market share, due to its compatibility with existing design palettes, consistent surface quality, and ease of integration into established manufacturing workflows.

The mycelium leather market is projected to grow at a CAGR of 36.7% between 2026 and 2033.

Major players include Bolt Threads, MycoWorks, Ecovative Design, Ananas Anam, and Modern Meadow.