- Home Appliances

- Lamp Market

Lamp Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Lamp Market by Product Type (Floor Lamp, Wall Lamp, Desk Lamp, Ceiling Lamp), Connectivity (Manual, Wi-fi, Bluetooth), Application (Residential, Commercial), Distribution Channel (Online, Hypermarket, Specialty Store), and Regional Analysis for 2026 - 2033

Lamp Market Size and Trend Analysis

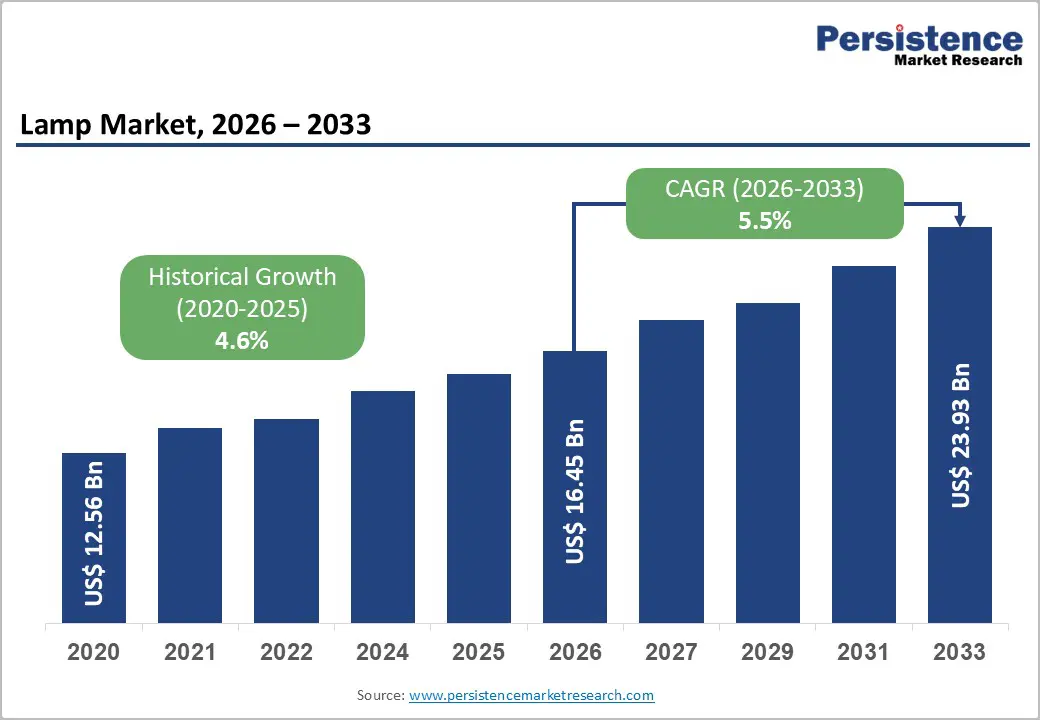

The global lamp market size is likely to be valued at US$ 16.5 billion in 2026 and is projected to reach US$ 23.9 billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

Stringent government energy efficiency regulations and the accelerated transition from conventional incandescent bulbs to LED and smart lighting solutions primarily drive the market expansion. The U.S. Department of Energy (DOE) mandates that general service lamps achieve a minimum of 45 lumens per watt by 2023, with targets increasing to 120 lumens per watt by July 2028, which is compelling manufacturers and consumers to adopt advanced lighting technologies.

Key Market Highlights:

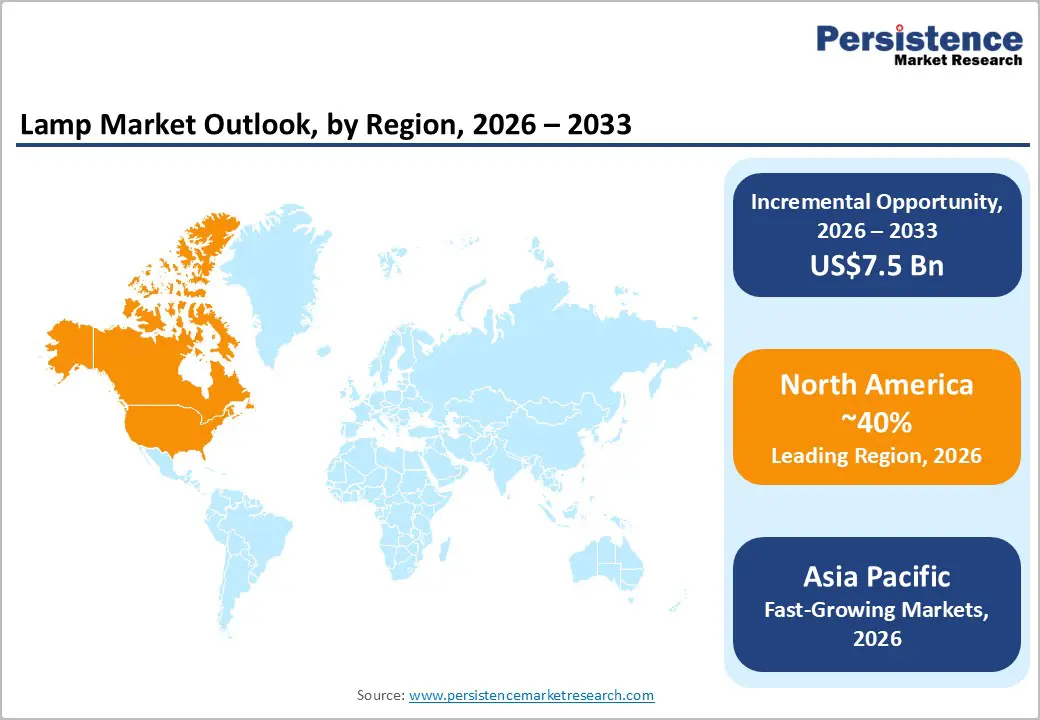

- Regional Leader: North America maintains global lamp market leadership, commanding approximately 40% of market share, driven by a sophisticated e-commerce infrastructure and regulatory frameworks prioritizing energy efficiency.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market, with China commanding around half of the region's LED lighting share through massive manufacturing capacity and "Made in China 2025" policy support.

- Leading Segment: Ceiling lamps dominate product type segmentation with approximately 45% market share, driven by building code requirements for primary ambient illumination in commercial offices, retail establishments, and residential spaces.

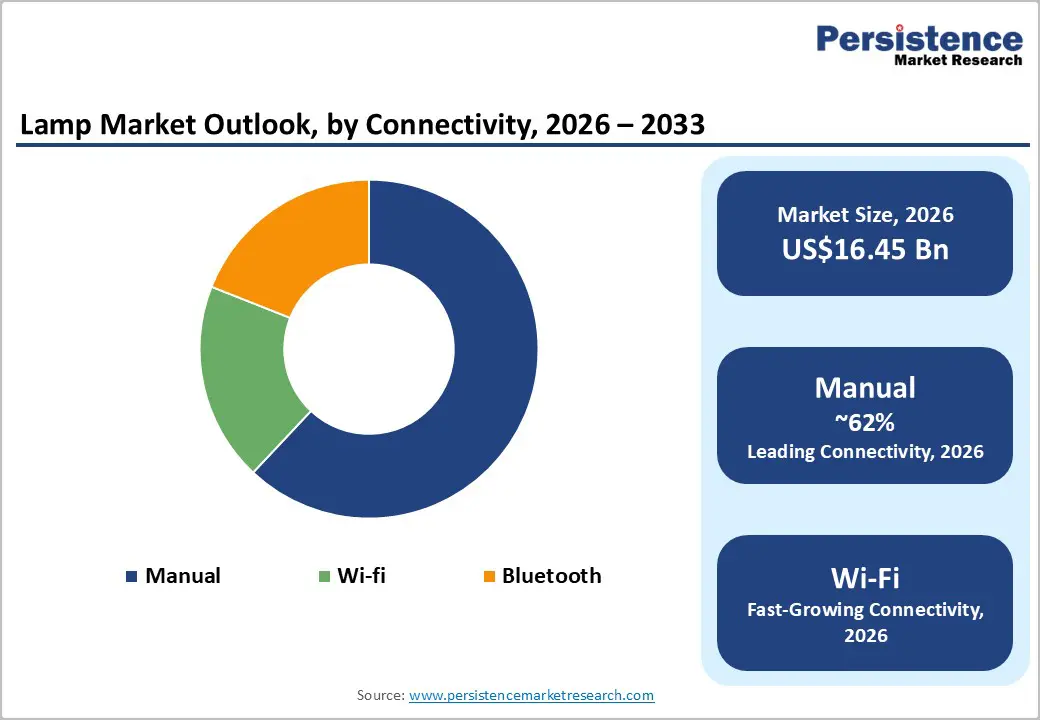

- Fastest Growing Segment: Wi-Fi-connected smart lamps represent the fastest-growing segment, driven by rising consumer demand for intelligent home automation integration and remote luminaire control capabilities supporting personalized lighting experiences.

- Key Market Opportunity: Artificial intelligence integration in lighting control systems presents the most significant market opportunity, exemplified by Signify's January 2025 launch of generative AI assistants enabling personalized scene creation through natural language, differentiating premium offerings while building ecosystem lock-in and recurring software revenue streams.

| Key Insights | Details |

|---|---|

| Lamp Market Size (2026E) | US$ 16.5 Bn |

| Market Value Forecast (2033F) | US$ 23.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 4.6% |

Market Dynamics

Drivers - Stringent Energy Efficiency Regulations Accelerating LED Lamp Adoption

Government regulations across major economies are significantly transforming the lamp market by eliminating inefficient lighting technologies. In July 2023, the U.S. Department of Energy implemented Congressionally mandated energy efficiency standards for general service lamps, requiring a minimum performance of 45 lumens per watt. This measure effectively removed traditional incandescent bulbs from the market. These standards are expected to generate annual savings of approximately $1.6 billion in household energy costs and reduce greenhouse gas emissions by 70 million metric tons over 30 years, equivalent to the annual emissions of nine million homes.

Furthermore, the DOE’s upcoming target of 120 lumens per watt by July 2028 is prompting leading manufacturers, such as Signify (Philips Lighting) and OSRAM, to accelerate advancements in LED technology and smart lighting solutions. Notably, LED technology represented about 48% of installed residential lighting units in 2020, a substantial increase from 8% in 2015, underscoring the rapid pace of market transformation.

Proliferation of Smart Home Ecosystems and IoT-Connected Lighting

The integration of wireless connectivity protocols such as Wi-Fi, Bluetooth, and the Matter standard in lamp products is creating significant opportunities for advanced lighting control and automation. In January 2025, Signify introduced AI-powered features for Philips Hue, including a generative AI assistant that delivers personalized lighting scenes based on user preferences. Similarly, Inter IKEA B.V. launched over 21 Matter-compatible smart home products in November 2025, including the KAJPLATS smart bulb range with expanded color options and enhanced light intensity.

Commercial deployments in smart city initiatives, particularly across the Asia Pacific regions, demonstrate accelerating penetration. China added 106 million urban residents between 2020 and 2024, collectively demanding intelligent infrastructure, including networked LED streetlighting. The installed base of connected light points reached approximately 153 million units globally by Q1 2025, with connected solutions representing over one-third of leading manufacturers' total business revenues, signaling sustained momentum in this segment.

Restraints - High Initial Investment Costs Limiting Consumer Adoption

The high initial cost of advanced lighting technologies, particularly smart lamps and premium LED fixtures, remains a significant barrier to widespread adoption. According to the U.S. Department of Energy, LED lamps, despite offering superior energy efficiency and extended lifespans, can cost up to five times more than traditional incandescent bulbs. This price disparity discourages cost-sensitive consumers, especially in developing regions where affordability often outweighs long-term savings.

The LED desk lamp market faces similar challenges, as models with adjustable color temperature and smart features are priced considerably higher than conventional alternatives. While the total cost of ownership favors LED and smart lighting solutions due to reduced energy consumption and durability, the upfront expense continues to limit adoption among residential and small commercial buyers operating under tight budget constraints.

Supply Chain Disruptions and Critical Material Shortages

The lamp manufacturing industry continues to grapple with persistent supply chain instabilities and the scarcity of essential components. According to the U.S. Department of Commerce, the global semiconductor shortage that intensified during the pandemic has severely impacted production of smart lighting systems that rely on advanced electronic components for connectivity and control functions. Rare earth metals, including gallium and indium, which are critical for LED manufacturing, face geopolitical tensions and export restrictions as noted by the International Energy Agency, creating supply vulnerabilities and price volatility.

The Bureau of Labor Statistics reported that transportation bottlenecks and rising freight costs exacerbated these challenges, with shipping expenses increasing by over 200% during peak disruption periods. These compounding factors have elevated production costs, extended lead times for new product launches, and constrained manufacturers' ability to meet accelerating consumer demand for energy-efficient and smart lighting solutions.

Opportunity - Expansion in Sustainable and Eco-Friendly Lamp Designs

The adoption of Matter as a universal smart home standard is creating significant growth opportunities for lamp manufacturers by addressing consumer demand for interoperability. Inter IKEA B.V. has announced a major product refresh, introducing more than 20 Matter-over-Thread smart home solutions in November 2025, with a focus on usability and affordability to broaden access to smart lighting. Matter eliminates compatibility issues across leading ecosystems such as Apple, Google, Amazon, and Samsung, enabling seamless integration regardless of existing infrastructure.

Signify is also expanding Matter support within its Philips Hue portfolio, positioning lighting as a core component of connected homes. This standardization is particularly relevant to the floor lamp segment, where consumers increasingly seek stylish ambient lighting that integrates with voice assistants and automation features. Manufacturers that quickly secure Matter certification and highlight cross-platform compatibility in their marketing strategies are well positioned to capture market share from consumers reluctant to adopt proprietary systems.

Artificial Intelligence Integration in Personalized Lighting Experiences

The integration of artificial intelligence (AI) and machine learning into lighting control systems presents a significant opportunity for differentiation and premium market positioning. Signify initiated this trend with the January 2025 launch of a generative AI assistant within the Philips Hue application, enabling users to create customized lighting scenes through natural language prompts based on mood, occasion, or aesthetic preferences.

The technology supports dynamic adjustments throughout the day, with IKEA introducing similar adaptive lighting features in its smart bulb range in December 2024. As AI capabilities advance, opportunities emerge for lamps that automatically optimize energy consumption, enhance productivity in commercial environments, and improve sleep quality in residential settings through intelligent spectral tuning.

Category-wise Analysis

Product Type Insights

Ceiling lamps hold the largest share of the global market, accounting for approximately 45%, due to their critical role in providing primary illumination for residential and commercial spaces. Data from the U.S. Department of Energy indicates that ceiling-mounted fixtures represent the most prevalent lighting category in commercial buildings, particularly in offices, retail environments, and educational facilities. This dominance is supported by building code requirements that mandate adequate ambient lighting, making ceiling lamps a fundamental component of lighting design.

LED adoption within this segment has grown substantially, with leading manufacturers such as Signify, OSRAM GmbH, and Panasonic offering extensive portfolios of recessed downlights, flush-mount fixtures, and pendant luminaires that combine energy efficiency with aesthetic appeal. The commercial sector favors ceiling lamps for their ability to deliver uniform light distribution across large areas while reducing maintenance costs through extended LED lifespans, which often exceed 35,000 hours for premium products.

Connectivity Insights

Manual lamps currently account for approximately 62% of market share, reflecting sustained consumer preference for traditional switching mechanisms and the slower adoption of smart connectivity features. Despite advancements in Wi-Fi and Bluetooth-enabled lighting, cost sensitivity and perceived complexity continue to limit smart lamp penetration, particularly in price-conscious residential segments and developing markets. However, the connectivity landscape is evolving rapidly.

Wi-Fi-enabled lamps are gaining traction in premium residential installations where consumers value seamless integration with home networks and compatibility with voice assistants such as Amazon Alexa, Google Assistant, and Apple Siri. The LED desk lamp market illustrates this trend, with models increasingly incorporating USB charging ports, Bluetooth speakers, and app-based controls for home office and study environments.

Application Insights

The residential application segment accounts for approximately 58% of market share, driven by the high volume of lighting installations in homes compared to commercial spaces. According to the U.S. Department of Energy, residential lighting consumes 31% of total lighting electricity despite the large unit count, reflecting the shift toward lower-wattage LED solutions that have reduced average lamp wattage to 22 watts.

Consumer preferences increasingly favor aesthetically designed, multifunctional lamps that complement interior décor while offering energy efficiency and smart home integration. The floor lamp segment benefits significantly from demand for flexible lighting solutions that provide ambient illumination without permanent installation, particularly in rental properties and urban apartments.

Distribution Channel Analysis

Specialty stores maintain market leadership with approximately 41% market share, leveraging their expertise in lighting consultation, product demonstration, and technical support that online and mass retail channels struggle to replicate. Specialty lighting retailers provide critical services, including lighting design consultation, custom product configuration, and professional installation coordination, which are particularly valued for complex residential renovations and commercial projects.

However, online channels are experiencing the fastest growth trajectory, propelled by the expanded product selection, competitive pricing, and convenience of e-commerce platforms operated by manufacturers like Signify and retailers including Inter IKEA B.V. The COVID-19 pandemic accelerated digital adoption, with consumers becoming more comfortable purchasing lamps online when supported by detailed product specifications, customer reviews, and favorable return policies.

Regional Insights

North America Lamp Market Trends

North America maintains market leadership driven by the United States' stringent regulatory framework and robust innovation ecosystem, fostering rapid adoption of advanced lighting technologies. The U.S. Department of Energy's finalized efficiency standards for general service lamps, mandating 45 lumens per watt, which took effect in July 2023, effectively eliminated traditional incandescent bulbs and accelerated the transition to LED solutions. These regulations are projected to save American households more than $27 billion on utility bills over 30 years while reducing greenhouse gas emissions equivalent to removing 9 million homes from the electrical grid annually.

The region's innovation leadership is exemplified by companies including Lutron Electronics, pioneering advanced dimming controls, and Koncept Inc., introducing USB-rechargeable task lamps with integrated wireless charging. Smart lighting integration with Amazon Alexa and Google Assistant voice control systems has become standard in new residential construction throughout major metropolitan areas.

Europe Lamp Market Trends

Europe is experiencing strong growth in sustainable lighting adoption, led by Germany, the United Kingdom, France, and Spain, which are aligning regulations with European Union energy efficiency directives and circular economy principles. The EU Ecodesign Directive enforces rigorous standards for lamp performance, durability, and recyclability, surpassing requirements in most global markets.

Consumer preferences in Europe emphasize design excellence and architectural integration, with Italian brands Artemide and Flos commanding premium pricing through designer collaborations in residential and hospitality sectors. Smart lighting adoption has accelerated following the introduction of Matter standard support, as consumers increasingly value energy monitoring features that provide real-time insights into electricity usage and carbon footprint reduction.

Asia Pacific Lamp Market Trends

Asia Pacific exhibits the fastest regional growth trajectory, propelled by China, Japan, India, and ASEAN nations' expanding middle-class populations, rapid urbanization, and manufacturing cost advantages that position the region as the global production hub for lamp components and finished products. China commanded around 40.6% share of the Asia Pacific LED lighting market in 2024, driven by massive industrial output and government-led initiatives, including the "Made in China 2025" policy that emphasizes energy-efficient technologies and advanced manufacturing capabilities.

Japan maintains technological leadership in specialized lamp applications and quality standards, with Panasonic Corporation and Toshiba Lighting developing innovative products for the aging population, including circadian rhythm-optimized lighting and color-rendering solutions for elderly vision requirements. The ASEAN region benefits from foreign direct investment in lighting manufacturing facilities seeking to diversify supply chains beyond China, with Vietnam, Thailand, and Malaysia emerging as alternative production bases.

Competitive Landscape

The global lamp market demonstrates moderate consolidation, with multinational corporations maintaining significant market share through comprehensive product portfolios, established distribution networks, and substantial investments in research and development. Leading companies such as Signify (Philips Lighting) and OSRAM GmbH employ vertical integration strategies that encompass LED chip production, luminaire manufacturing, and smart lighting software platforms, ensuring competitive advantage and premium positioning. Emerging business models include direct-to-consumer e-commerce channels that bypass conventional retail distribution, lighting-as-a-service offerings for commercial clients, and strategic partnerships with major smart home platform providers such as Amazon, Google, Apple, and Samsung to ensure compatibility with voice assistants and automation systems.

Key Market Developments:

- January 2025: Signify launched groundbreaking AI-powered smart lighting features for Philips Hue, introducing the lighting industry's first generative artificial intelligence assistant integrated directly into the Hue mobile app, enabling users to create personalized lighting scenes through natural language descriptions of mood, occasion, or aesthetic preferences.

- November 2025: Inter IKEA B.V. announced a comprehensive smart home range revamp featuring 21 new Matter-compatible products launching in January 2026, with the KAJPLATS smart bulb line offering eleven variations across different shapes, sizes, lumen levels, and color capabilities, all designed to work seamlessly with the universal Matter smart home standard.

- September 2025: Signify launched the Philips Aura Floodlight in India, a market-first decorative professional floodlight designed specifically for the country's vibrant cultural and festive landscape, offering 5000 lumen output with 80 CRI and available in six distinctive designs at INR 2,499 across all variants.

Top Companies in the Lamp Market

- Signify (Philips Lighting) (Netherlands) maintains global market leadership through its comprehensive Philips and Philips Hue brand portfolios spanning residential, commercial, and industrial lighting applications. The company's January 2025 introduction of generative AI technology in the Philips Hue ecosystem demonstrates continued innovation leadership, while its extensive intellectual property portfolio covering LED efficiency, color tuning, and wireless connectivity protocols creates substantial barriers to entry.

- OSRAM GmbH (Germany) leverages its heritage as a pioneer in lighting technology and contemporary leadership in LED semiconductor components to maintain premium market positioning. The company's Duris S 5 LED achieves lifespans exceeding 35,000 hours while withstanding high application temperatures, exemplifying engineering excellence that differentiates OSRAM in professional and commercial segments.

- Inter IKEA B.V. (Sweden) disrupts traditional lamp market dynamics through its combination of Scandinavian design aesthetics, aggressive pricing strategies, and rapid smart home technology adoption. IKEA's global retail footprint, exceeding 400 stores across 50+ countries, provides unmatched physical distribution reach, while its vertically integrated supply chain enables industry-leading price points that pressure premium competitors.

Companies Covered in Lamp Market

- Signify (Philips Lighting)

- OSRAM GmbH

- Herman Miller Inc.

- Inter IKEA B.V.

- Artemide S.p.A.

- Panasonic Corporation

- Lutron Electronics

- Koncept Inc.

- OttLite Technologies

- Flos S.p.A.

- EGLO

- GE Lighting

- Toshiba Lighting

- Schneider Electric

Frequently Asked Questions

The global lamp market is projected to reach US$ 23.9 Bn by 2033, growing from an estimated US$ 16.5 Bn in 2026 at a CAGR of 5.5% during the forecast period, driven by stringent energy efficiency regulations and smart lighting adoption.

The market is primarily driven by government energy efficiency mandates, particularly the U.S. Department of Energy's requirement for 45 lumens per watt minimum efficiency and future targets of 120 lumens per watt by 2028, combined with the proliferation of IoT-connected smart home ecosystems and AI-powered personalization features from manufacturers.

Ceiling Lamp leads the Lamp market, with 45% share, driven by building code requirements for primary ambient illumination in commercial and residential spaces, with LED ceiling fixtures offering extended lifespans exceeding 35,000 hours.

North America maintains market leadership, with 40% market share, supported by stringent U.S. regulatory frameworks, including DOE efficiency standards that are projected to save American households $27 billion over 30 years.

Artificial intelligence integration in lighting control systems presents the most transformative opportunity, exemplified by Signify's January 2025 launch of generative AI assistants in Philips Hue that enable personalized scene creation through natural language, allowing manufacturers to command premium pricing while building ecosystem lock-in and recurring software revenue.

Leading market participants include Signify (Philips Lighting), OSRAM GmbH, Inter IKEA B.V., Panasonic Corporation, and Honeywell International, with competition based on technology innovation, design excellence, and smart home ecosystem integration.