- Electrical Equipment & Services

- Clamp Meter Market

Clamp Meter Market Size, Share, and Growth Forecast, 2026-2033

Clamp Meter Market by Product Type (Analog, Digital, Smart, Alternating Current (AC) Clamp Meters, Direct Current (DC) Clamp Meters, AC/DC Clamp Meters, Hall-Effect, Flexible), End-User Industry (Industrial Manufacturing, Power & Utilities, Construction, Automotive, HVAC Services, Residential), Measurement Function (AC, DC, Voltage, Resistance & Continuity, Temperature, Capacitance, Data Logging), and Regional Analysis for 2026-2033

Clamp Meter Market Share and Trends Analysis

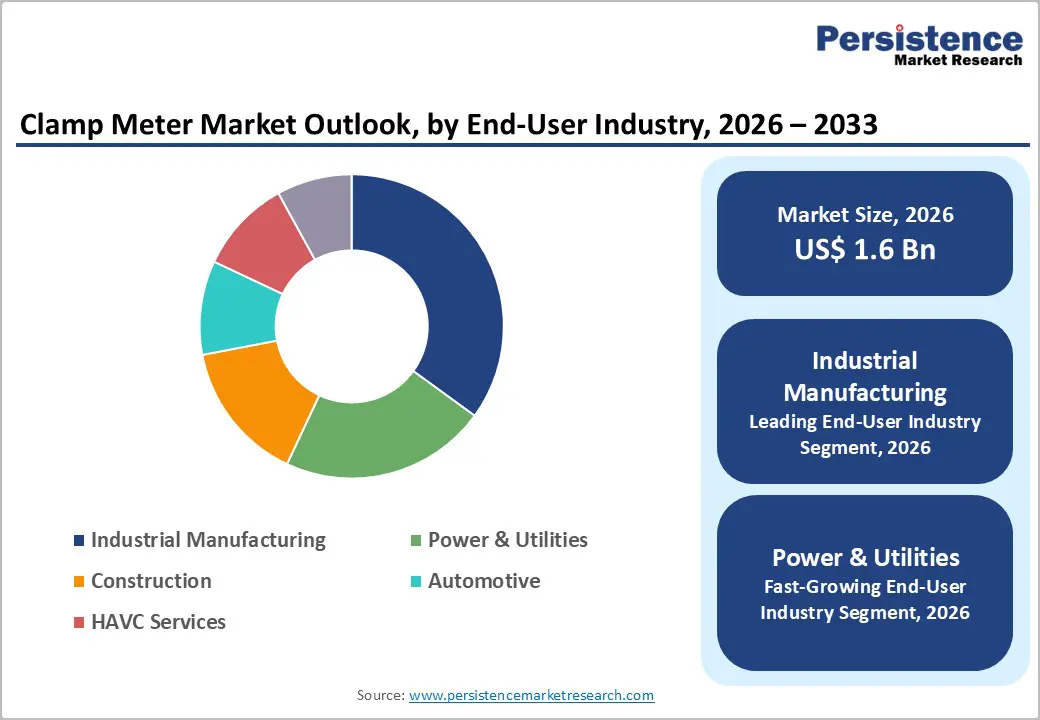

The global clamp meter market size is likely to be valued at US$ 1.6 billion in 2026, and is projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026 - 2033.

Market expansion reflects steady electrification across industrial, utility, construction, and automotive sectors, supported by sustained capital expenditure in power generation, transmission, and distribution infrastructure. According to the International Energy Agency (IEA), global electricity demand continues to grow at over 3% annually, reinforcing the need for reliable testing and diagnostic tools. Rising investments in renewable energy integration and grid modernization programs across North America, Europe, and Asia Pacific further strengthen equipment replacement cycles. Increasing adoption of digital and smart measurement technologies, compliance-driven safety testing standards, and the rapid proliferation of heating, ventilation, & air-conditioning (HVAC) systems and electric vehicle (EV) charging infrastructure collectively act as primary demand accelerators.

Key Industry Highlights

- Dominant Product Types: Digital clamp meters are expected to hold around 42% revenue share in 2026, while smart clamp meters are projected to grow the fastest through 2033, driven by connectivity and IoT-enabled diagnostics.

- Leading End-User Industries: Industrial manufacturing is set to lead with nearly 35% share in 2026, whereas power & utilities is anticipated to expand at the fastest rate during 2026–2033 due to grid upgrades and renewable integration.

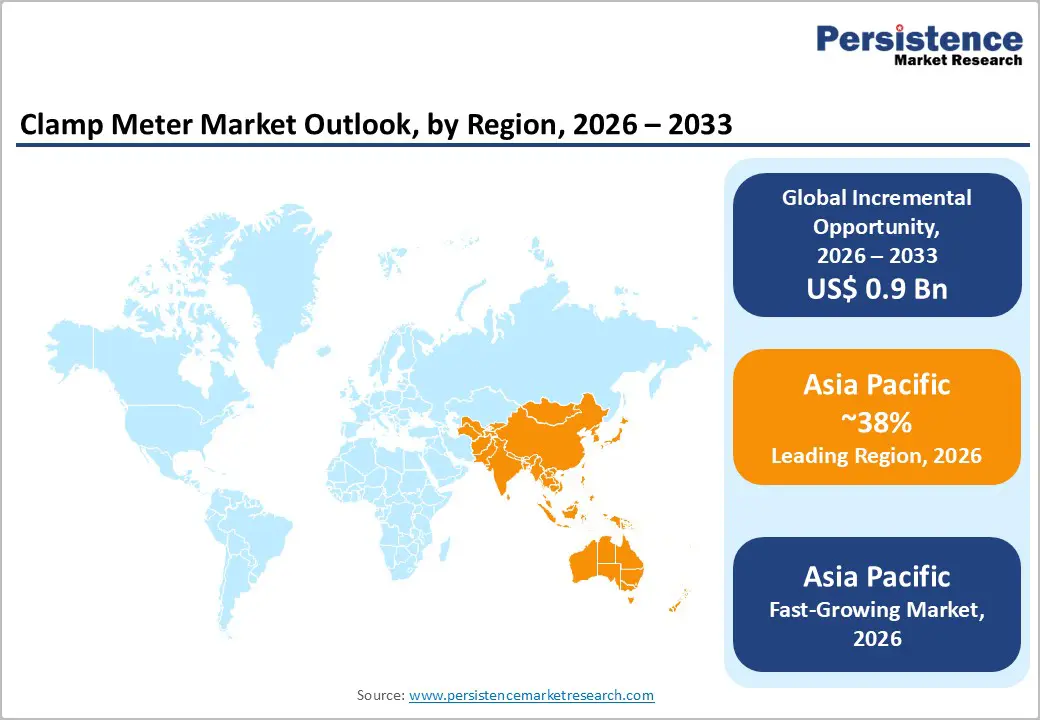

- Regional Leadership: Asia Pacific is projected to dominate with about 38% market share in 2026, supported by infrastructure expansion and rapid electrification.

- Competitive Environment: The market remains moderately fragmented, with competition centered on innovation, safety compliance, and expansion into high-growth emerging markets.

| Key Insights | Details |

|---|---|

|

Clamp Meter Market Size (2026E) |

US$ 1.6 Bn |

|

Market Value Forecast (2033F) |

US$ 2.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Accelerating Electrification, Renewable Integration, and Grid Modernization

The IEA reports that global grid investment surpassed US$ 330 billion in 2024, driven by renewable integration and transmission upgrades, with major capital deployment continuing through 2025. The U.S. Infrastructure Investment and Jobs Act allocated US$ 65 billion for power grid improvements, and the EU’s REPowerEU plan committed over €300 billion to decarbonization initiatives. Concurrently, utilities worldwide are modernizing distribution and medium-voltage infrastructure to support smart-grid technologies, reducing outages and improving reliability. These cumulative investments are expanding electrical network capacity and fueling testing and validation work across substations and distribution networks.

Clamp meters are essential for installation, testing, and maintenance of electrical systems in transmission lines, substations, and distributed energy assets. The rapid deployment of solar PV plants, wind farms, battery storage, and expanding EV charging networks requires accurate AC/DC current and voltage diagnostics, safety verification, and compliance reporting. As renewable capacity additions and grid upgrades accelerate, technicians increasingly adopt high-performance clamp meters to support real-time troubleshooting without de-energizing circuits. This sustained infrastructure expansion is creating recurring demand across utilities and electrical contractors, positioning the clamp meter market as a key beneficiary of broader electrification strategies.

Industrial Automation Expansion and Electrified End-Use Growth

Industrial automation adoption remains a major driver of clamp meter demand. Global factory automation systems, advanced production lines, and robotics integration require precise electrical monitoring to maintain uptime and optimize energy use. Predictive maintenance strategies are increasingly standard in smart manufacturing environments, pushing technicians to adopt digital and smart clamp meters with True RMS accuracy, data logging, and wireless connectivity for real-time diagnostics and trend analysis.

In parallel, electrified end-use sectors are expanding rapidly. Global electric vehicle sales surpassed 14 million units in 2023, and public and private capital continues to fund EV charging network rollouts in 2025–2026. Testing high-current DC infrastructure for safety, performance, and regulatory compliance drives adoption of DC and AC/DC clamp meters. HVAC system installations are also gaining ground as building electrification expands, requiring integrated temperature, resistance, and current measurement during service and commissioning. These industrial and electrified applications widen the end-user base for multifunctional clamp meters, supporting strong sustained demand beyond basic current measurement needs.

Intense Price Sensitivity and Margin Pressure from Low-Cost Competition

The clamp meter market faces margin pressure from low-cost Asian manufacturers offering basic digital models at prices 30–50% lower than premium brands. In price-sensitive emerging markets, purchasing decisions prioritize affordability over advanced features. This limits adoption of smart clamp meters despite their technological advantages. Contractors and small service providers often opt for entry-level devices that meet basic requirements rather than invest in multifunctional tools. This dynamic directly affects average selling prices and overall profitability.

Compounding this, semiconductor supply chain disruptions and component price inflation have intensified in 2025–2026, driving broad cost pressures across electronic manufacturing. Memory and passive component prices have surged substantially due to supply constraints and high demand for AI-oriented chips, increasing input costs for measurement device manufacturers. Lead times for critical components such as microcontrollers and memory modules have extended significantly to 20–25 weeks or more, reflecting persistent shortages. Such structural cost inflation constrains mid-tier manufacturers’ margins and slows product development cycles, making it harder to compete on both price and features.

Stringent Safety Standards and Rising Compliance Burden

Electrical testing equipment must comply with International Electrotechnical Commission (IEC) 61010 safety standards and region-specific certification requirements such as Underwriters Laboratories (UL) and Conformité Européenne (CE). These regulations ensure user protection in high-voltage environments but increase development complexity. Manufacturers must conduct rigorous insulation, overload, and environmental testing before commercialization, which extends product launch timelines and raises design costs. Regulatory compliance therefore acts both as a quality benchmark and an operational constraint on innovation and market entry.

Certification burdens have heightened in several jurisdictions through 2025. For example, Argentina implemented modernized electrical safety technical regulations (Resolutions No. 16/2025 & 17/2025) requiring updated conformity marks and detailed documentation, increasing certification complexity for imported electrical tools. At the same time, the European Union (EU) has adjusted hazardous substance restrictions under the RoHS directive, narrowing exemptions and requiring greater product transparency. These evolving regulations increase compliance overhead for manufacturers of electrical test equipment, slowing time to market. Calibration requirements further increase lifecycle costs, often by 5–8% annually for industrial users who must maintain certification records and adhere to audit standards, a factor that limits participation by smaller manufacturers.

Digitalization of Electrical Testing and Smart Infrastructure Expansion

Connected measurement tools with Bluetooth, cloud data logging, and mobile app integration represent a high-growth niche, enabling remote diagnostics, digital reporting, and predictive maintenance integration directly from field assets into centralized systems. IoT-enabled clamp meters support real-time condition monitoring, driving uptime improvements for industrial facilities and utilities. By 2030, more than 50 billion connected devices are expected globally, reinforcing the structural shift toward digital operations and data-driven maintenance practices, according to a recent industry report.

Smart grid investments and digital network upgrades have accelerated globally. For example, smart grid initiatives in ASEAN economies are advancing rapidly, with governments launching digital strategies and pilot programs that include smart metering, automated controls, and grid resilience measures to modernize energy systems and integrate renewable resources, as observed by the IoT M2M Council, 2025. The smart grid market itself is projected to grow sharply, driven by real-time monitoring and automation adoption, enhancing the importance of IoT-enabled electrical testing equipment across transmission, distribution, and facility management ecosystems.

Infrastructure Development and Renewable Energy Service Growth

The World Bank reports infrastructure investment needs in developing economies exceed US$ 1.5 trillion annually, with countries such as India and ASEAN nations expanding power distribution and urban construction. Large-scale electrification and grid upgrades increase electrical installation activity and create sustained demand for mid-range digital clamp meters. Asia Pacific, contributing over 45% of global electricity demand growth, remains a key regional growth engine, as per the IEA. Ongoing capital investment in grid modernization, and integration of next-generation monitoring technologies, expands the service opportunity for electrical testing tools.

Real-world developments in 2025–2026 underline this trend. For example, Portugal committed €400 million in grid upgrades following the June 2025 Iberian Peninsula blackout, increasing energy storage, control capacity, and resilience measures to reinforce critical infrastructure performance. India’s State Electricity Transition report (SET 2026) highlights significant advances in distributed solar adoption and power ecosystem preparedness across several leading states, reflecting expanding renewable portfolios and associated testing requirements. These developments emphasize the critical role of accurate current, voltage, and safety measurements in supporting emerging energy infrastructure and renewable service networks.

Category-wise Analysis

Product type Insights

The digital segment is projected to account for approximately 42% of the clamp meter market revenue share in 2026, supported by their accuracy, durability, and compliance suitability across industrial applications. In 2025, multiple electrical safety advisories issued by national workplace safety authorities emphasized the importance of certified test instruments for high-voltage environments, reinforcing procurement preference for CAT III and CAT IV rated digital meters. Industrial maintenance teams are increasingly standardizing approved toolkits to align with updated safety inspection norms. This institutional procurement pattern supports steady replacement demand. Digital models are also widely specified in public infrastructure tenders requiring documented measurement accuracy. These factors collectively sustain their revenue leadership.

Smart clamp meters are estimated to be the fastest-growing product segment, expanding at around 8.2% CAGR during 2026–2033, driven by connected diagnostics and digital workflow integration. In 2026, several leading instrument manufacturers introduced upgraded Bluetooth-enabled clamp meters designed for mobile app synchronization and cloud reporting, supporting field digitization initiatives. Facility managers increasingly require automated service logs to meet audit standards and internal compliance reporting. Wireless data capture reduces manual documentation errors and enhances technician productivity. The integration of diagnostic tools with asset management software is expected to accelerate adoption. As digital maintenance ecosystems expand, smart clamp meters are likely to gain incremental share.

End-User industry Insights

Industrial manufacturing is expected to lead with an estimated 35% of the clamp meter market share in 2026, boosted by ongoing automation and equipment electrification. In 2025, several automotive and electronics manufacturers announced capacity expansions across Asia and North America, increasing demand for electrical commissioning and maintenance tools. Manufacturing facilities continue to implement preventive and predictive maintenance protocols to minimize downtime risks. Routine motor diagnostics, load verification, and control panel inspections remain standard operating procedures. Clamp meters form part of approved maintenance toolkits across heavy and discrete manufacturing plants. These operational requirements are projected to sustain industrial segment dominance.

Power & utilities is forecast to be the fastest-growing end-user industry, registering around 7.4% CAGR through 2033, driven by accelerated grid resilience projects. In 2026, multiple governments announced distribution network reinforcement and substation automation programs following extreme weather-related outages. Utilities increasingly require high-accuracy AC/DC measurement tools for feeder line diagnostics and renewable integration testing. Field engineers are deploying advanced clamp meters for real-time current verification during infrastructure upgrades. Expanded inspection frequency under updated reliability standards is expected to further stimulate demand. These structural upgrades position utilities as the most dynamic growth contributor.

Regional Analysis

North America Clamp Meter Market Trends

North America remains a mature and strategically important market, supported by sustained federal infrastructure investments and grid modernization initiatives. In 2025, the U.S. Department of Energy (DOE) advanced funding under its Grid Resilience and Innovation Partnerships program to strengthen transmission reliability and wildfire mitigation infrastructure. These initiatives increase field-level electrical inspection and testing activity. Expansion of EV charging corridors overseen by the U.S. Department of Transportation (DOT) continues to accelerate electrical installation projects across interstate networks. Ongoing compliance with National Electrical Code standards sustains structured equipment replacement cycles. Industrial retrofits and substation upgrades further reinforce procurement stability.

The regional outlook remains stable, driven by renewable capacity expansion and infrastructure resilience planning. In early 2026, the U.S. Energy Information Administration (EIA) reported continued additions in utility-scale solar and battery storage capacity, increasing diagnostic requirements across grid-connected assets. Canada’s grid strengthening initiatives supported by Natural Resources Canada also contribute to steady demand for certified testing tools. Utilities continue prioritizing outage prevention and predictive maintenance strategies. Procurement decisions emphasize compliance, safety certification, and long-term reliability. Market consolidation supports premium positioning of established brands.

Europe Clamp Meter Market Trends

In Europe, the market for clamp meter is likely to experience steady demand, owing to regulatory harmonization and energy transition policies. In 2025, the European Commission (EC) expanded funding under the Connecting Europe Facility to accelerate cross-border electricity infrastructure upgrades. These projects require standardized and certified electrical measurement solutions. Germany’s industrial automation expansion, supported by the Federal Ministry for Economic Affairs and Climate Action, reinforces ongoing diagnostic equipment needs across manufacturing facilities. Renewable integration programs, particularly offshore wind development, further stimulate testing requirements. CE marking and IEC compliance frameworks maintain uniform procurement standards. Western Europe remains the dominant sub-regional contributor.

The market environment remains compliance-driven and technology-focused. In 2026, the UK Department for Energy Security and Net Zero confirmed continued investment in electricity network upgrades to meet clean power targets. France’s transmission modernization efforts reported by RTE highlight grid digitalization and monitoring system expansion. These developments increase demand for high-accuracy and safety-rated measurement devices. Procurement processes prioritize reliability, certification, and lifecycle performance. Competitive intensity remains strong among established engineering brands. Overall, Europe maintains steady expansion under policy-backed electrification objectives.

Asia Pacific Clamp Meter Market Trends

Asia Pacific is anticipated to dominate with 38% of the clamp meter market value in 2026, driven by strong industrial production and infrastructure expansion. In 2025, China’s renewable and grid expansion programs reported by the National Energy Administration reinforced large-scale transmission development and distributed energy integration. India’s distribution reform and smart metering initiatives under the Ministry of Power continue to accelerate diagnostic and installation activity. Manufacturing growth across ASEAN economies further strengthens equipment demand. Japan’s grid reinforcement strategy supported by the Ministry of Economy Trade and Industry enhances system reliability investments. These structural drivers reinforce Asia Pacific’s market leadership.

Asia Pacific is also expected to be the fastest-growing regional market through 2033, expanding above the global average growth trajectory. In 2026, the Asian Development Bank announced financing support for transmission modernization and renewable integration projects across South and Southeast Asia. Rapid urbanization and commercial construction continue to elevate electrical inspection requirements. Infrastructure-focused foreign direct investment accelerates electrification across industrial clusters. Cost-efficient manufacturing ecosystems improve regional scalability and supply chain responsiveness. Government-backed resilience initiatives further support long-term equipment adoption. As a result, the region combines volume leadership with the strongest forward growth outlook.

Competitive Landscape

The global clamp meter market structure is moderately fragmented, with leading multinational test and measurement companies such as Fluke Corporation, Keysight Technologies, Hioki, and Klein Tools accounting for a substantial portion of global revenue. These companies leverage strong distribution networks, established industrial relationships, and certified product portfolios. Their focus on True RMS accuracy, high safety ratings, and durable field performance strengthens brand preference. Continuous R&D investment supports wireless connectivity and data logging innovation. Brand reliability remains a decisive factor in professional procurement.

Regional and Asian manufacturers such as UNI-T and Mastech compete aggressively in cost-sensitive markets. These players prioritize affordable digital models targeting electricians and small contractors. Compliance with IEC safety standards and certification requirements creates moderate entry barriers. However, digital integration and mobile-enabled reporting are enabling product differentiation. Gradual consolidation and strategic partnerships are expected to reshape competitive positioning over time.

Key Industry Developments

- In February 2026, MECO Instruments introduced new 3¾-digit, 6000-count digital clamp meters designed for professional electrical measurements, offering True RMS current measurement up to 1000A and voltage measurement up to 1000V. The devices also measure resistance, capacitance, frequency, and temperature, and include features such as data hold and non-contact voltage detection.

- In November 2025, S-5! launched the S-5-CP clamp for solar carports, designed to attach photovoltaic panels to Cee and Zee purlin structures without drilling holes, enabling faster installation and improved structural reliability. The clamp integrates with the company’s PVKIT rail-less mounting system and uses a bottom-oriented setscrew, allowing installers to secure solar modules from beneath the canopy.

- In April 2025, Teledyne FLIR introduced a new range of PV inspection solutions, including a clamp meter, irradiance meter, and I-V curve tracer, designed to simplify testing during solar panel installation and maintenance. The tools enable installers and utilities to measure panel performance, detect overheating components, and document system data through wireless connectivity, improving efficiency in solar system diagnostics and verification.

Companies Covered in Clamp Meter Market

- Fluke Corporation

- Hioki E.E. Corporation

- Chauvin Arnoux

- Klein Tools

- Extech Instruments

- Amprobe

- UNI-T

- Mastech Group

- Kyoritsu Electrical Instruments

- Megger Group

- Keysight Technologies

- Gossen Metrawatt

- Sanwa Electric Instrument

- Yokogawa Test & Measurement

Frequently Asked Questions

The global clamp meter market is projected to reach US$ 1.6 billion in 2026.

Rising electrification, grid modernization, industrial automation, and EV infrastructure expansion are key growth drivers.

The market is poised to witness a CAGR of around 6.6% from 2026 to 2033.

Smart IoT-enabled clamp meters, renewable energy servicing, and emerging market infrastructure development present major opportunities.

Fluke Corporation, Hioki, Keysight Technologies, and Klein Tools are some of the key players in the market.