- Medical Devices

- Phototherapy Lamps Market

Phototherapy Lamps Market Size, Share, and Growth Forecast, 2026-2033

Phototherapy Lamps Market by Technology (LED, Fluorescent, Halogen, Fiber-Optic), Application (Neonatal Jaundice, Psoriasis, Vitiligo, Atopic Dermatitis, Dermatological Disorders, Seasonal Affective Disorder), End-User (Neonatal Intensive Care Units (NICUs), Dermatology Clinics, Specialty Phototherapy Centers, Homecare Settings, Research & Academic Institutes), and Regional Analysis for 2026-2033

Phototherapy Lamps Market Share and Trends Analysis

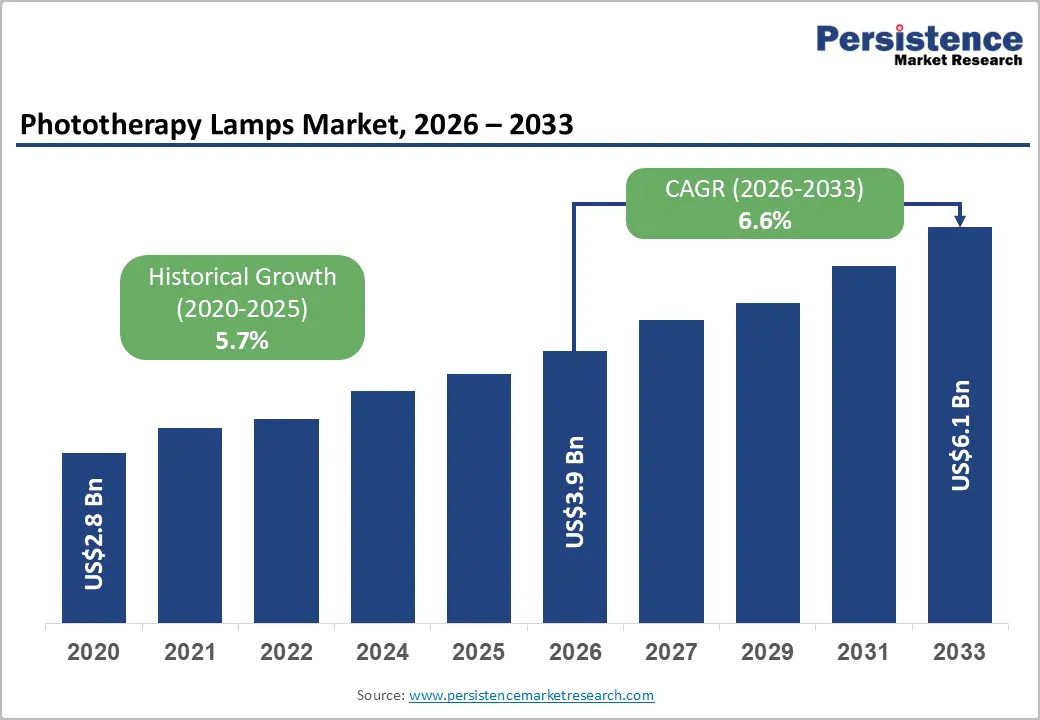

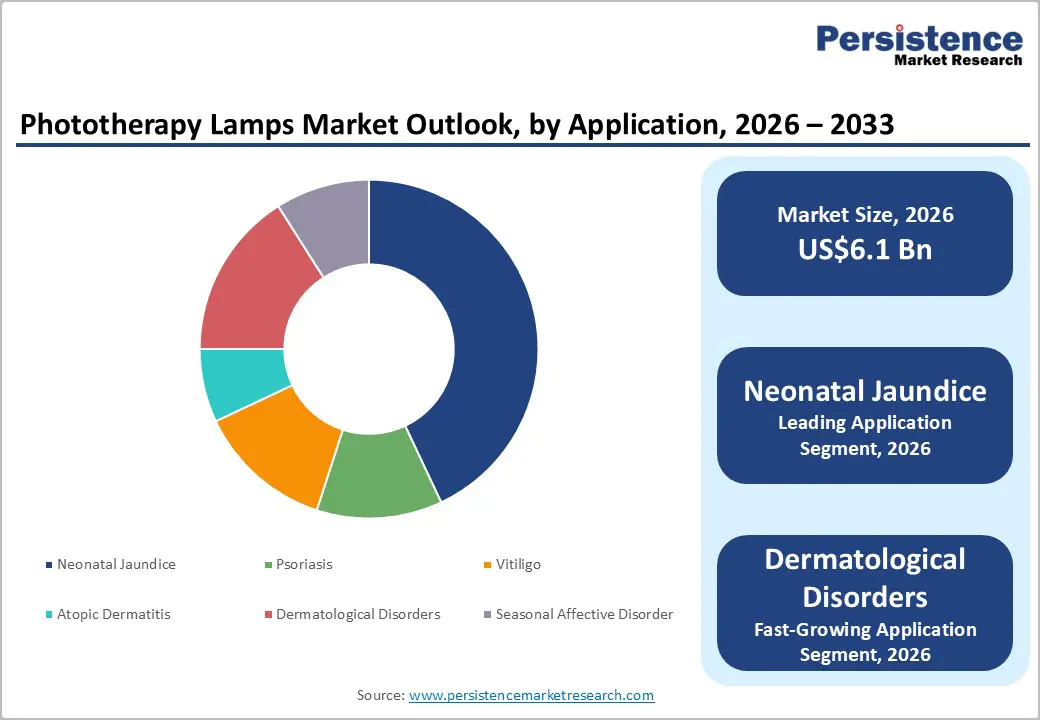

The global phototherapy lamps market size is likely to be valued at US$ 3.9 billion in 2026, and is projected to reach US$ 6.1 billion by 2033, growing at a CAGR of 6.6% during the forecast period 2026–2033.

The growth of the market is driven by the rising incidence of neonatal jaundice, increasing demand for dermatological phototherapy treatments, and wider adoption of light-emitting diode (LED) phototherapy technology in healthcare facilities. Hospitals and NICUs rely on phototherapy as a first-line treatment for neonatal hyperbilirubinemia, which affects a large percentage of newborns globally. Dermatologists also recommend UV phototherapy for chronic skin conditions such as psoriasis, vitiligo, and eczema. Clinical guidelines from pediatric and dermatology associations reinforce the role of light-based therapeutic devices in treatment protocols. Meanwhile, growing awareness of home-based phototherapy devices and advances in energy-efficient LED light sources are expanding access to phototherapy treatments worldwide.

Key Industry Highlights

- Leading Applications: Neonatal jaundice treatment is set to command around 43% revenue share in 2026, while dermatological phototherapy treatments are likely to grow the fastest through 2033, driven by rising prevalence of skin disorders.

- Dominant Technology: LED phototherapy lamps are projected to hold approximately 42% revenue share in 2026, while fiber-optic systems are expected to grow the fastest at 7.9% CAGR through 2033, supported by improved neonatal comfort.

- Leading End-Users: Neonatal intensive care units (NICUs) are anticipated to lead with 44% market share in 2026, while homecare settings are likely to register the fastest growth through 2033, fueled by adoption of portable home phototherapy devices.

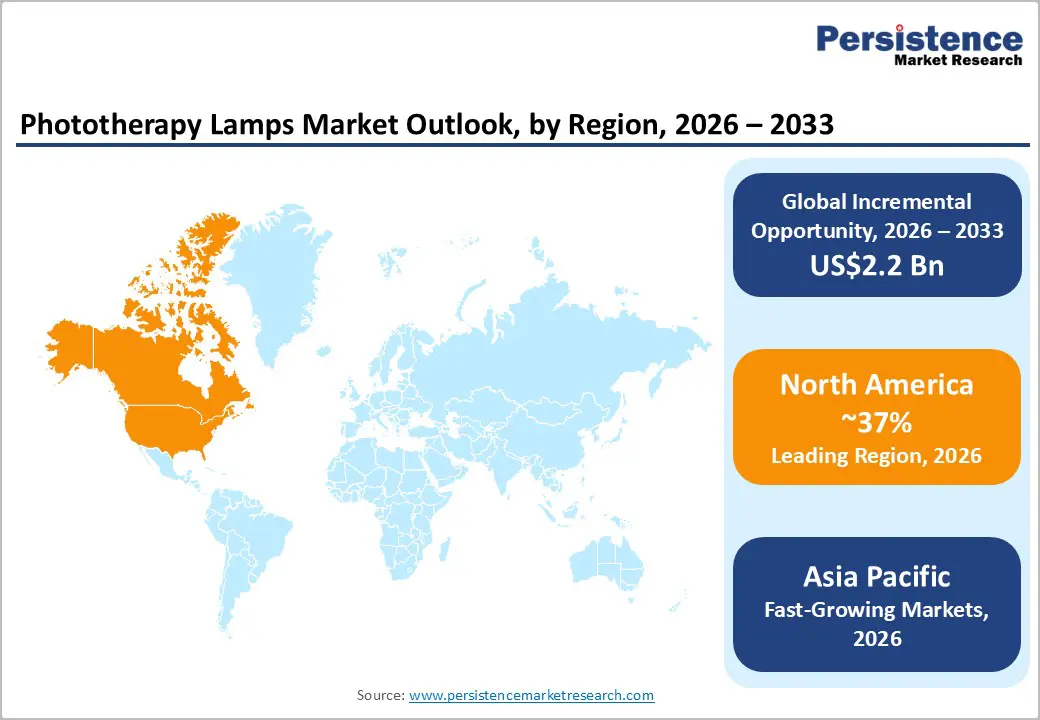

- Regional Leadership: North America is likely to lead with nearly 37% market share in 2026, while Asia Pacific is expected to grow at the fastest pace with a 7.3% CAGR through 2033, driven by expanding healthcare infrastructure.

- Competitive Environment: Market dynamics center on LED technology innovation, portable home phototherapy systems, and expansion into emerging markets, strengthening distribution networks and clinical adoption globally.

| Key Insights | Details |

|---|---|

| Phototherapy Lamps Market Size (2026E) | US$ 3.9 Bn |

| Market Value Forecast (2033F) | US$ 6.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Incidence of Neonatal Jaundice and Expanding Clinical Phototherapy Adoption

One of the primary drivers of the phototherapy lamps market is the increasing global prevalence of neonatal jaundice. Studies indicate that approximately 60% of full-term newborns and nearly 80% of preterm infants develop jaundice during their first week. Severe hyperbilirubinemia is a major cause of hospitalization, especially in emerging economies. Neonatal intensive care units rely on phototherapy lamps to reduce bilirubin levels and prevent complications such as kernicterus. The American Academy of Pediatrics recommends phototherapy as the standard treatment for moderate to severe neonatal jaundice. Rising birth rates in regions such as Asia and Africa continue to support strong clinical demand.

Hospitals are increasingly investing in LED-based neonatal phototherapy systems due to their efficiency and precision. These lamps offer longer lifespans, reduced energy consumption, and lower heat emission compared to traditional fluorescent or halogen devices. Adoption is driven by the need for reliable treatment that ensures infant safety and clinical effectiveness. Expanding healthcare infrastructure, especially in public hospitals and private neonatal units, is accelerating procurement of advanced phototherapy lamps. This trend also aligns with initiatives to improve neonatal care quality while maintaining cost-effectiveness. As a result, NICUs remain the leading end-user segment driving sustained market growth.

Expanding Dermatological Applications and Technological Advancements

The increasing prevalence of chronic skin disorders is another major growth driver for the phototherapy lamps market. Globally, skin diseases affect nearly 900 million people at any given time, including conditions such aspsoriasis, vitiligo, eczema, and acne. These conditions often require long-term management through controlled ultraviolet phototherapy treatments, particularly in dermatology clinics and specialty centers. Narrowband UVB phototherapy is recognized as a standard therapy for moderate to severe cases, promoting clinical adoption. As patient awareness rises and clinics expand treatment offerings, demand for technologically advanced phototherapy systems is steadily increasing.

The shift to LED phototherapy technology has further strengthened the market. LED systems deliver precise wavelengths, longer operational lifespans (20,000–30,000 hours), and lower heat output, improving treatment safety and efficiency. Hospitals and dermatology centers are prioritizing LED devices due to reduced maintenance costs and better energy efficiency. These advancements also allow for more accurate dosing, enhancing treatment outcomes for both neonatal and dermatological applications. As healthcare providers increasingly focus on reliable, cost-effective, and safe solutions, LED-based phototherapy lamps are becoming the preferred technology worldwide.

Barrier Analysis - High Costs and Regulatory Constraints

The phototherapy lamps market continues to face upward pressure from high capital costs associated with advanced LED based equipment. LED systems typically cost 20–40% more than traditional fluorescent units, requiring significant investment from hospitals and specialty clinics, particularly in rural and emerging market settings. Budget constraints slow replacement cycles and delay technology upgrades, even as newer systems offer improved efficiency and safety. This cost barrier affects procurement decisions and limits the pace at which providers adopt next generation devices across care settings.

Regulatory compliance adds another layer of complexity. Devices must meet stringent medical safety standards from bodies such as the U.S. Food and Drug Administration (FDA) and European Union (EU) Medical Device Regulation (MDR), which extend development timelines and increase pre market expenditures. Compliance with such strict regulatory standards, including the IEC 62471 photo biological safety guidelines, increases product development timelines and costs. Smaller manufacturers may find it difficult to meet these requirements, slowing the introduction of innovative phototherapy devices into the market

Competition from Alternative Treatments

The phototherapy lamps market is also affected by rising competition from alternative treatment options, particularly in dermatology. For conditions such as psoriasis and eczema, biologics and targeted systemic therapies are increasingly used, reducing reliance on phototherapy in some clinical pathways. These alternatives are often perceived as more convenient or efficacious for severe disease, especially in health systems where reimbursement supports such therapies. As a result, dermatology clinics may prioritize non light based treatments, limiting growth potential for phototherapy devices.

Moreover, news reports in early 2026 have highlighted ongoing challenges in dermatology service continuity due to equipment downtime. For instance, the Jersey General Hospital dermatology service saw its phototherapy provision suspended for several years, delaying treatment access for patients with skin conditions until a replacement machine arrives, illustrating how operational and alternative therapy adoption barriers intersect. This real world disruption underscores that even when phototherapy remains clinically important, logistical constraints and competing treatment pathways can constrain its utilization.

Expansion of Home-Based Phototherapy, Remote Care, and Cosmetic Applications

The growth of home healthcare and remote dermatology treatments is creating strong opportunities for phototherapy lamps. Portable devices for conditions such aspsoriasis and vitiligo allow patients to receive care without frequent clinic visits. Properly supervised home phototherapy delivers outcomes comparable to hospital treatments, supporting wider adoption among patients and providers. In 2025, the Centers for Medicare & Medicaid Services (CMS) in the U.S. expanded reimbursement for remote therapeutic devices, enabling broader access to home-based phototherapy. Telemedicine tools allow clinicians to monitor therapy adherence, adjust protocols remotely, and ensure safety. These trends encourage development of user-friendly, connected devices for home care. Manufacturers can leverage this shift to expand their market reach globally.

Phototherapy is also gaining traction in the beauty and wellness sector, targeting skin rejuvenation, acne management, and anti-aging. In 2025, Lumenis launched a home-use LED device designed for cosmetic skin improvement, highlighting consumer adoption beyond clinical care. Beauty clinics increasingly integrate light therapy into non-invasive treatment portfolios. This opens new revenue channels alongside traditional medical applications. Patient interest in at-home cosmetic therapies complements clinical adoption. Manufacturers can leverage clinical credibility to capture both medical and wellness markets, creating a dual-market growth strategy. This trend broadens the overall adoption potential for phototherapy systems globally.

Healthcare Infrastructure Expansion and Smart Phototherapy Technologies

Global healthcare infrastructure expansion is driving demand for neonatal and dermatology phototherapy devices. Investments in maternal and child health facilities are prompting procurement of advanced phototherapy systems. For example, projects such as, a US$ 3.2 billion hospital in Adelaide and a US$ 1.8 billion worth hospital in Perth, Australia for women and babies includes expanded NICU and dermatology units, reflecting infrastructure-driven demand. Also, philanthropic initiatives such as the Beginnings Fund with a support neonatal care access and improve treatment outcomes in underserved regions. Hospitals are upgrading equipment to enhance clinical performance and patient safety. These developments highlight the importance of phototherapy devices in modern healthcare. The trend positions phototherapy lamps as essential in both hospital and specialty clinic settings worldwide.

Smart phototherapy systems with integrated sensors, automated dosage, and digital monitoring capabilities are increasingly adopted. Hospitals favor devices capable of real-time therapy tracking and electronic health record (HER) integration, which improve treatment precision and patient safety. The demonstrations of next-generation LED systems showcased remote monitoring and analytics features, highlighting technological advancements. These systems reduce risks of under- or over-treatment while improving clinical efficiency and operational workflow. Manufacturers developing smart, connected phototherapy devices can gain a significant competitive advantage. Adoption is expected to accelerate across both developed and emerging healthcare markets. Smart system integration is emerging as a key differentiator for manufacturers globally.

Category-wise Analysis

Technology Insights

LED phototherapy lamps are expected to be the market leader, to hold approximately 42% of the revenue share in 2026, due to their energy efficiency, precise spectral output, and extended operational life, supporting consistent neonatal and dermatology care. Hospitals and specialty centers increasingly prefer LED solutions for neonatal and dermatological applications that require consistent intensity and minimal heat emission. In 2025, a next-generation LED phototherapy device developed by LumenTech Health was launched, featuring adaptive multi-wavelength control and automated intensity adjustment, optimizing skin treatment effectiveness while avoiding UV exposure, highlighting a significant technological advancement for clinical adoption. This evolution underscores LED lamps’ ability to deliver customizable therapy across indications.

Fiber-optic phototherapy systems are projected to represent the fastest-growing technology with a projected CAGR of approximately 7.9% through 2033, driven by their flexible light delivery mechanisms that improve patient comfort and treatment precision. A new portable fiber-optic phototherapy pad developed by MedTech Innovate with embedded real-time monitoring sensors was introduced, enabling clinicians to tailor light intensity and exposure time based on real-time feedback. Hospitals are adopting fiber-optic systems where patient comfort and mobility are priorities, particularly in neonatal care. These advanced capabilities enhance clinical effectiveness while reducing risk of over-exposure.

Application Insights

Neonatal jaundice is poised to capture around 43% of the phototherapy lamps market revenue share in 2026, as phototherapy continues to serve as the standard intervention for bilirubin reduction in newborns. Clinicians rely on robust phototherapy systems that provide precise and consistent light output. The launch of a next-generation neonatal LED phototherapy unit developed by BrightCare Technologies with built-in therapy tracking and automated intensity adjustment was reported in leading healthcare news, demonstrating how device innovation is improving clinical workflow and treatment accuracy. These systems help ensure optimal dosing without excessive heat or infant discomfort. Advances in real-time monitoring support better care coordination between clinical staff. Such innovations reinforce neonatal phototherapy’s clinical efficacy.

Dermatological phototherapy is projected to emerge as the fastest-growing application through 2033, fueled by expanded use for conditions including psoriasis, vitiligo, and eczema. Light-based therapy is increasingly integrated into treatment regimens as a non-invasive alternative to systemic medications. In 2026, a new smart UVB phototherapy cabinet developed by DermalTech Systems equipped with automated dose calibration and patient usage analytics was showcased by a major European hospital system, illustrating how digital intelligence is enhancing patient safety and therapeutic outcomes. This tech enhancement reduces manual adjustments and ensures consistent, reproducible treatments. As clinics adopt systems that integrate data-driven dosing and treatment logging, dermatological phototherapy becomes more efficient and scalable.

Regional Insights

North America Phototherapy Lamps Market Trends

North America is expected to hold an estimated 37% of the phototherapy lamps market share in 2026, driven by advanced healthcare infrastructure, high neonatal screening rates, and strong adoption of LED phototherapy systems in hospitals and dermatology clinics. The United States accounts for most demand, supported by American Academy of Pediatrics guidelines for neonatal jaundice and widespread use in dermatology care. The Maternal and Child Health Program of the Health Resources and Services Administration (HRSA) invests in neonatal intensive care equipment, enabling hospitals to procure advanced LED phototherapy devices. FDA regulations ensure high-quality standards, fostering clinician confidence in new systems. Hospitals adopt multi-wavelength LED panels and connected devices to improve patient outcomes. Home healthcare adoption of portable phototherapy systems also expands outpatient care capabilities.

The region benefits from strong medical device R&D and hospital-academic collaborations, enabling rapid commercialization of innovative phototherapy technologies. Telemedicine-enabled systems allow remote monitoring and treatment adjustments, supporting both neonatal and dermatological care. NICUs increasingly deploy devices with real-time intensity tracking and automated dosing to optimize patient safety. Dermatology clinics adopt smart LED systems for outpatient care, improving efficiency and treatment reproducibility. Reimbursement support further drives adoption of advanced phototherapy lamps. Public and private healthcare facilities continue prioritizing energy-efficient, connected devices. These trends reinforce North America’s leadership and innovation in the global phototherapy market.

Europe Phototherapy Lamps Market Trends

Europe represents a mature but steadily growing market for phototherapy lamps. Germany, the United Kingdom, France, and Spain drive regional demand with broad access to dermatological and neonatal care facilities supported by public healthcare systems. Hospitals and clinics are investing in LED and fiber optic phototherapy systems that offer precise dosing, energy efficiency, and improved patient comfort. Regulatory harmonization under the EU MDR ensures consistent safety across member states, promoting adoption of advanced devices with robust clinical evidence. Hospitals expand outpatient phototherapy programs, particularly for chronic skin conditions, aligning with public health initiatives.

A € 1 million OP Zuid stimulus program award supported development of a next generation full body blue light phototherapy system for atopic dermatitis that can be used in home settings, highlighting Europe’s drive toward connected, patient centric devices. This development underscores the region’s focus on next generation LED, blue light, and home enabled phototherapy technologies that broaden clinical and consumer use cases. European dermatology clinics are early adopters of connected treatment systems with automated dose calibration and analytics, enhancing safety and efficiency. Public healthcare systems in the U.K. and Germany continue to integrate phototherapy care into broader chronic disease management strategies, reinforcing the region’s commitment to technology driven solutions. Continued collaboration between device manufacturers, clinical networks, and regulatory bodies fosters innovation and supports Europe’s role as a key market for advanced phototherapy devices.

Asia Pacific Phototherapy Lamps Market Trends

Asia Pacific is projected to be the fastest-growing regional market for phototherapy lamps, with a projected CAGR of 7.3% through 2033, driven by large birth populations, expanding healthcare infrastructure, and rapid adoption of smart medical technologies. Major contributors include China, Japan, and South Korea, where energy-efficient LED phototherapy lamps and fiber-optic systems are increasingly used in neonatal and dermatology care. The World Health Organization (WHO) and the UN Children’s Fund (UNICEF) launched the Regional Roadmap for the Elimination of Mother-to-Child Transmission, strengthening maternal and neonatal healthcare services and guiding public hospitals in upgrading neonatal care equipment, including advanced phototherapy devices. Dermatology clinics in urban centers are adopting portable, customizable phototherapy systems to increase outpatient treatment capacity. Public-private collaborations promote telemedicine integration and remote monitoring. .

Technological innovation is a key catalyst in the region’s growth trajectory. Manufacturers and service providers are integrating smart, app enabled controls, real time usage tracking, and remote compliance monitoring into phototherapy systems to meet rising demand. Patient preference for non invasive, efficient treatments for chronic skin conditions drives adoption beyond hospital settings. Hospitals across Asia Pacific are investing in integrated digital platforms that enhance device interoperability with electronic health records, supporting care continuity. Regional growth is further bolstered by expanding local device manufacturing, which lowers costs and accelerates adoption across emerging economies.

Competitive Landscape

The global phototherapy lamps market structure is moderately consolidated, with top players such as Philips Healthcare, GE Healthcare, Dräger, Natus Medical, and Koninklijke DSM holding over 50% of revenue share. These companies leverage strong hospital and clinical relationships, regulatory expertise, and integrated device-software platforms. Heavy investments in LED efficiency, multi-wavelength control, and smart monitoring technologies strengthen clinical adoption, while expansion into portable and home-use devices broadens their market presence. Their focus on energy-efficient, long-life systems also reduces operational costs for hospitals, enhancing competitiveness.

Regional and niche players, including BiliLux, LightWell Technologies, and DermalTech Systems, focus on specialized applications such as neonatal care, dermatology clinics, and homecare settings. Regulatory standards, clinical safety requirements, and precise device calibration limit new entrants, but connected and telemedicine-enabled phototherapy devices open opportunities for innovation. Market consolidation is expected as global leaders acquire smaller players to expand geographically and technologically, while strategic partnerships with digital health firms accelerate development of smart, integrated phototherapy solutions.

Key Industry Developments

- In February 2026, Natus Sensory expanded its newborn care portfolio by acquiring TheraB Medical, including the FDA-cleared SnugLit™ wearable phototherapy system. This swaddle-style device allows infants to be held during treatment, enhancing family-centered care and enabling hospital and home-based neonatal jaundice management.

- In September 2025, Alcon strengthened its retinal therapy offerings by acquiring LumiThera’s Valeda Light Delivery System (LDS), the first FDA-authorized photobiomodulation device for early to intermediate dry age-related macular degeneration (AMD). The system delivers non-invasive, low-level light therapy to support retinal cell health, expanding Alcon’s clinic-based treatment capabilities.

- In April 2025, iSMART Developments received FDA clearance for its handLITE device, the first non-UV light therapy system approved to treat hand dermatitis using red and near-infrared wavelengths. Clinical data show significant symptom improvement, with most patients reporting reduced severity and itching, positioning the device as a safe, non-invasive alternative to traditional treatments.

Companies Covered in Phototherapy Lamps Market

- GE HealthCare

- Natus Medical Incorporated

- Philips Healthcare

- Phoenix Medical Systems

- Drägerwerk AG

- Atom Medical Corporation

- Waldmann Medical Division

- National Biological Corporation

- Daavlin

- UVBioTek

- Nice Neotech Medical Systems

- Ibis Medical Equipment

- Herbert Waldmann GmbH & Co. KG

Frequently Asked Questions

The global phototherapy lamps market is projected to reach US$ 3.9 billion in 2026.

Increasing neonatal jaundice incidence, growing dermatology phototherapy demand, and widening adoption of energy-efficient LED systems are driving the market.

The market is poised to witness a CAGR of 6.6% from 2026 to 2033.

Expansion of home-based phototherapy devices and investments in smart, connected hospital systems offer major growth potential.

Philips Healthcare, GE Healthcare, Dräger, Natus Medical, Koninklijke DSM, BiliLux, LightWell Technologies, and DermalTech Systems are some of the key market players.