- LED & Lighting (Optoelectronics)

- UV Curing Lamps Market

UV Curing Lamps Market Size, Share, and Growth Forecast, 2026 – 2033

UV Curing Lamps Market by Product Type (Mercury Vapor Lamps, LED Lamps, Arc Lamps, Others), Application (Printing, Coating, Adhesive, Others), End-User (Automotive, Electronics, Healthcare, Industrial, Others), and Regional Analysis for 2026-2033

UV Curing Lamps Market Share and Trends Analysis

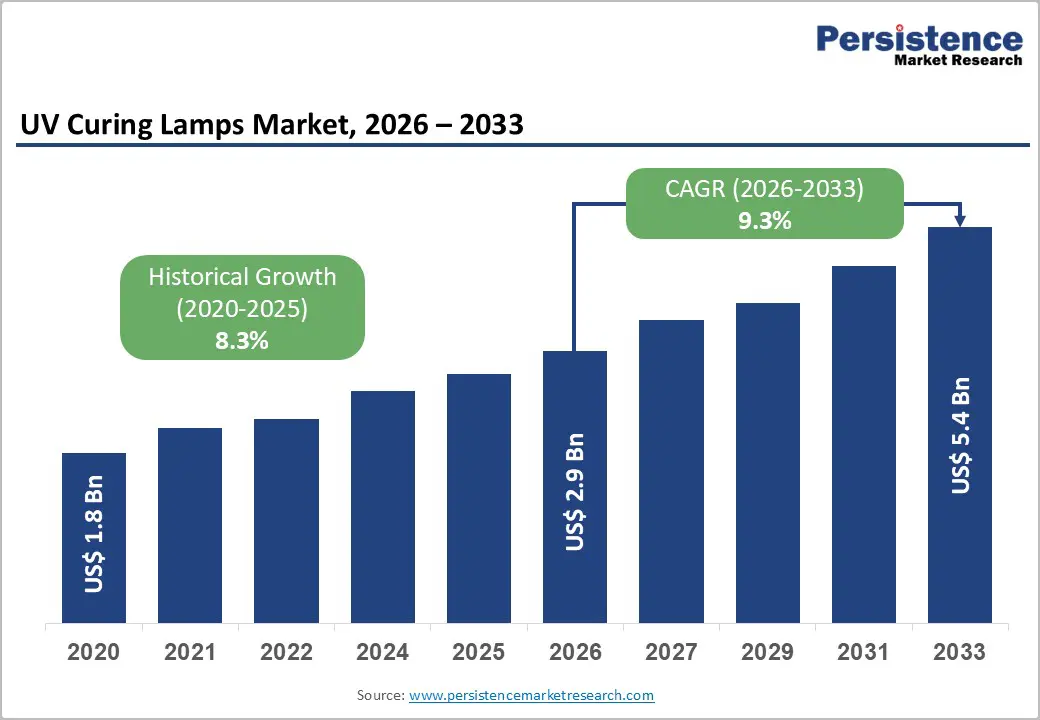

The global UV curing lamps market size is likely to be valued at US$ 2.9 billion in 2026, and is projected to reach US$ 5.4 billion by 2033, growing at a CAGR of 9.3% during the forecast period 2026−2033.

The market demonstrates strong structural growth momentum due to accelerating industrial process optimization and sustainability-driven manufacturing transformation. Adoption expands as manufacturers prioritize faster curing cycles, reduced energy consumption, and improved production throughput across printing, coating, electronics, automotive, and healthcare manufacturing environments. Rising regulatory emphasis on volatile organic compound emission reduction directly supports transition from solvent-based curing systems toward ultraviolet (UV)-based curing technologies, creating a cause–effect pathway between environmental policy enforcement and equipment investment decisions. Technological integration represents a central growth catalyst. Advancements in light-emitting diode (LED) ultraviolet systems enable precise wavelength control, extended operational lifecycles, and lower thermal output, encouraging replacement of conventional mercury vapor systems in sensitive production settings.

Key Industry Highlights

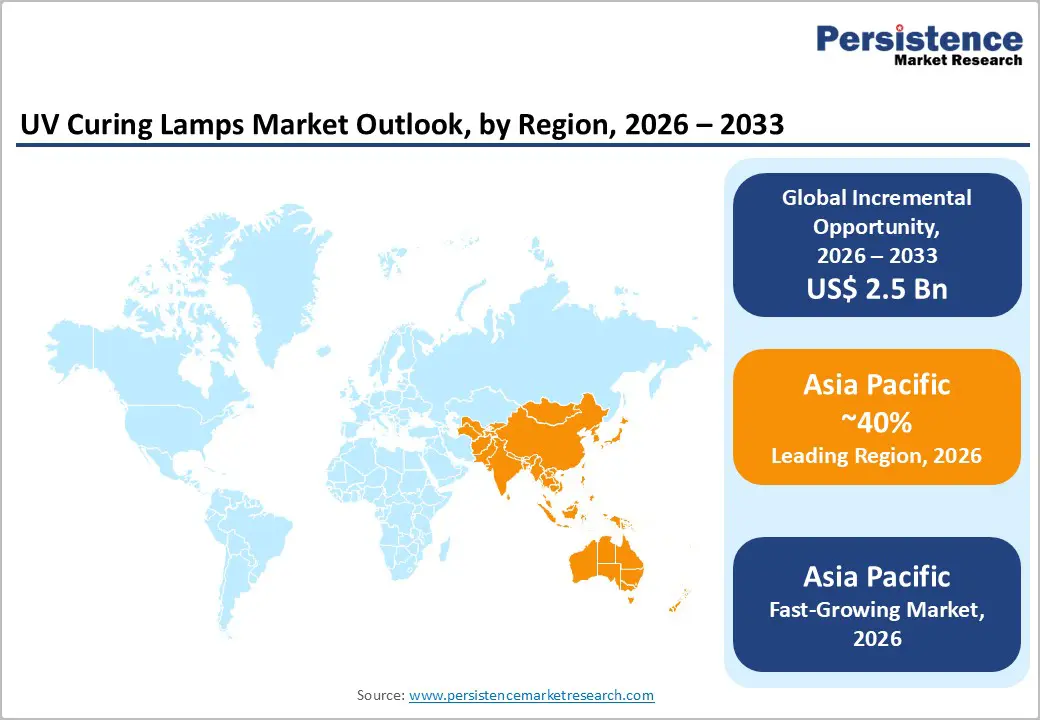

- Dominant Region: Asia Pacific is projected to hold about 40% market share in 2026, driven by concentrated high-output manufacturing hubs and extensive industrial adoption of ultraviolet curing.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market during 2026–2033, propelled by precision manufacturing expansion and electronics miniaturization.

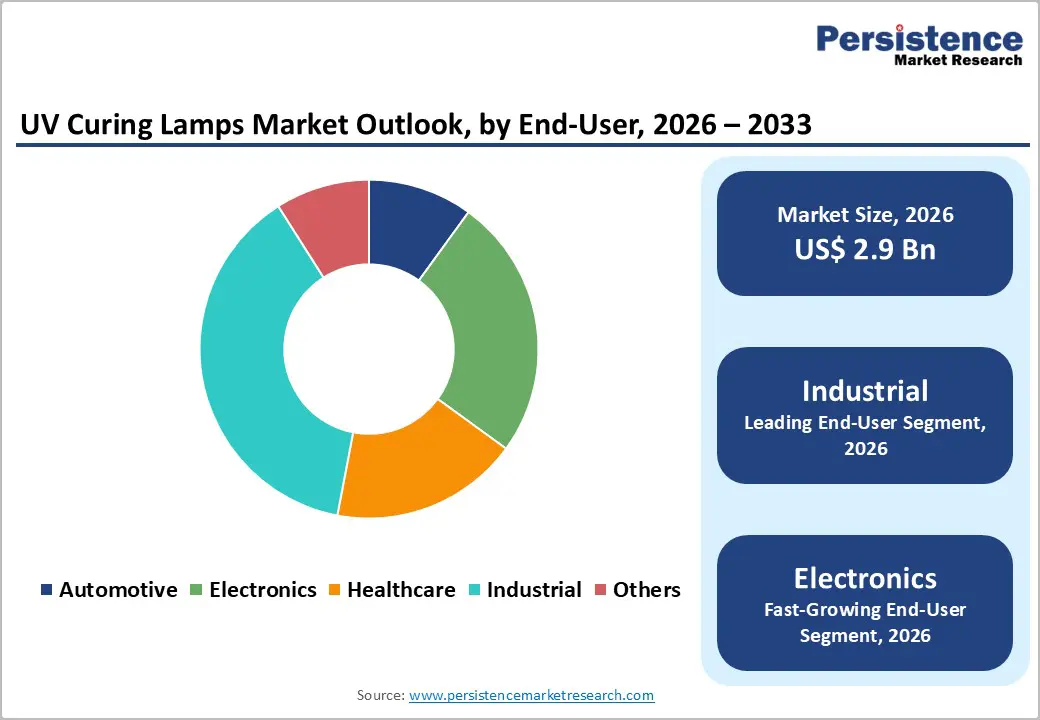

- Leading End-User: Industrial manufacturing is set to account for about 38% share in 2026, owing to the alignment of UV curing lamps with quality certification frameworks and their automation compatibility.

- Fastest-growing End-User: Electronics is expected to be the fastest-growing segment through 2033, driven by miniaturization, precision assembly needs, and cleanroom-compatible low-temperature curing.

- January 2026: IST METZ announced development of the LEDcure NX water-cooled LED UV system targeting industrial curing applications with high energy efficiency, modular integration, and improved operational reliability.

| Key Insights | Details |

|---|---|

|

UV Curing Lamps Market Size (2026E) |

US$ 2.9 Bn |

|

Market Value Forecast (2033F) |

US$ 5.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

8.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Shift toward High-Efficiency and Low-Emission Manufacturing

Rising emphasis on operational efficiency and emission reduction reshapes manufacturing investment priorities across energy-intensive industries. Policy frameworks increasingly link production approvals, environmental clearances, and fiscal incentives to measurable reductions in air pollutants and energy intensity. Regulatory authorities promote process technologies that minimize volatile organic compound release, shorten production cycles, and lower thermal losses, aligning industrial output with national clean-manufacturing objectives. In India, for example, regulatory guidance under the Environment (Protection) Act sets stringent air-quality compliance expectations, where pollution control systems used in manufacturing lines must demonstrate up to 95% destruction and removal efficiency for volatile organic compounds, as cited on official government regulatory portals in 2025.

Operational economics further reinforces this shift toward efficiency-driven production models. Energy-intensive drying and curing stages traditionally generate high operating costs, maintenance burden, and emission management overhead. Low-emission manufacturing systems support faster throughput, reduced floor-space utilization, and stable quality outcomes, strengthening return on capital investment. Government-led environmental audit mechanisms introduced in 2025 require structured disclosure of emission performance and energy usage, increasing transparency across industrial facilities and supply chains. Compliance readiness now influences supplier qualification, export eligibility, and long-term contract allocation in regulated sectors such as electronics, automotive components, packaging, and medical devices.

Advancement of LED UV Technology and Automation Integration

Industrial production priorities increasingly emphasize energy efficiency, process reliability, and compatibility with advanced materials. Light-emitting diode ultraviolet systems align with these priorities through stable wavelength delivery, instant activation, and limited heat generation, which supports precise curing across sensitive substrates and high-speed lines. These characteristics improve throughput predictability and reduce thermal distortion risks in coatings, inks, and adhesives. Evidence from 2025 published by the U.S. Department of Energy (DOE) confirms that light-emitting diode lighting uses at least 75 percent less energy and achieves operating lifetimes up to 25 times longer than conventional lighting technologies, validating the efficiency and durability advantages that influence capital allocation decisions in industrial environments. Energy performance and longevity together strengthen operational cost control and asset utilization metrics valued in large-scale manufacturing.

Automation integration reinforces the value proposition through alignment with digitally managed production systems. Automated ultraviolet curing enables synchronized control of exposure time, intensity, and line speed within connected manufacturing architectures. This integration supports consistent quality output, minimizes human intervention, and improves repeatability across batch and continuous processes. Real-time monitoring and data capture enable process optimization and early fault identification, which supports yield stability and compliance requirements. UV systems designed for automation fit these objectives by functioning as controlled, software-driven process units rather than standalone equipment.

High Initial Capital Investment and Retrofit Complexity

Industrial UV curing systems require significant upfront equipment expenditure and extensive line modifications to integrate into existing production environments. Many plants must invest in specialized UV lamps, power supplies, safety shielding, and ventilation and control systems before the technology can be operational. For smaller manufacturers this represents a large fixed cost that competes directly with other capital needs, delaying internal return on investment and cash flow recovery. Supply and installation of high-intensity UV emitters and associated infrastructure often require facility downtime, structural changes to support electrical loads and trained technical personnel for commissioning. These factors collectively increase project complexity, extend implementation timelines and require careful planning for compatibility with existing processes such as conveyors or spray booths. Retrofitting can necessitate line stoppages that interrupt production targets and require detailed process control validation before full-scale operation is resumed.

In addition to the capital burden, adapting existing manufacturing lines to UV curing involves material handling, control integration and operator training. Production lines originally configured for thermal or solvent-based drying may need reengineering to effectively accommodate high-intensity UV light sources, affecting fixture positions, shielding to protect workers from exposure and synchronization with application equipment. Process engineers and operators must develop new standard operating procedures and safety protocols, increasing training costs and lengthening the learning curve as teams gain experience with UV chemistry and energy dosing.

Material Compatibility Constraints and Safety Compliance Burdens

Industrial adoption is constrained by incompatibilities between ultraviolet curing lamps and many existing substrates, coatings or adhesives. A broad range of materials used in production lines do not transmit or react efficiently to ultraviolet wavelengths, which forces formulation redesign, extended cycle times or additional surface preparation steps to achieve effective curing. These requirements drive up development and capital expenditures, dilute operational throughput and restrict flexibility in process selection when standardization of curing processes would otherwise improve efficiency. The need to tailor materials and processes for specific lamp outputs can also create deeper supply chain complexity as firms must validate compatibility and performance across multiple material families and curing technologies to avoid yield losses.

Regulatory and safety obligations create further operational cost pressures in industrial environments where ultraviolet radiation is present. Government health guidance indicates that atmospheric processes absorb approximately 90% of UV-B radiation before it reaches the surface, highlighting inherent biological risks associated with ultraviolet exposure at higher intensities than natural background levels, which informs workplace protections and controls. Organizations must develop engineering controls, shielding, personal protective equipment and comprehensive training to mitigate risks of eye injury and skin damage from artificial ultraviolet sources, and these measures must be documented and maintained under occupational safety frameworks. Compliance activities extend product qualification timelines and require ongoing investment in monitoring and validation to satisfy regulators and protect personnel.

Expansion of Electronics, Medical Device, and Advanced Materials Manufacturing

Growth in electronics, medical device, and advanced materials manufacturing creates a strong opportunity for UV curing technologies through structural shifts in production methods and quality expectations. Electronics manufacturing increasingly prioritizes miniaturization, high circuit density, and fast cycle times, which elevates demand for curing solutions that deliver precision without thermal stress. UV curing supports rapid bonding, encapsulation, and coating of sensitive components while maintaining dimensional stability and process consistency. Public-sector manufacturing programs focused on semiconductor fabrication, electronics assembly, and localized supply chains reinforce capital investment in automated, high-throughput production lines where UV curing integrates seamlessly with robotics and inline inspection systems.

Medical device and advanced materials manufacturing further reinforce this opportunity through strict regulatory frameworks and performance-driven material selection. Medical device production relies on clean, repeatable curing processes for adhesives and coatings used in catheters, implants, diagnostic equipment, and wearable health technologies. UV curing enables controlled polymerization, low volatile emissions, and consistent surface properties that support compliance and traceability objectives. Advanced materials manufacturing, including functional coatings, engineered polymers, and composite structures, depends on precise curing to achieve targeted mechanical, optical, and chemical characteristics. UV-based systems support energy-efficient processing, reduced waste generation, and scalable production of high-value materials.

Replacement Cycle Acceleration and Transition toward Mercury-Free Solutions

Regulatory pressure and environmental compliance priorities are reshaping equipment investment decisions across industrial UV applications. Governments are enforcing stricter controls on mercury usage in manufactured products, supported by public health and environmental protection mandates. These frameworks create defined end-of-use horizons for mercury-containing lamps, prompting organizations to reassess installed systems earlier than traditional depreciation cycles. Compliance planning now aligns with regulatory calendars rather than asset lifespan, which compresses replacement timelines. Procurement teams increasingly favor technologies that eliminate regulatory exposure, reduce hazardous material handling, and simplify audit readiness.

Operational efficiency and asset optimization further reinforce accelerated replacement behavior. Mercury-free UV solutions deliver consistent output stability, reduced maintenance frequency, and simplified waste management processes compared with legacy systems. These attributes support lean manufacturing objectives, uptime optimization, and sustainability reporting commitments that are now embedded in corporate governance frameworks. Capital expenditure decisions increasingly factor lifecycle efficiency, energy management alignment, and environmental risk mitigation. Equipment replacement is therefore positioned as a value-protection initiative rather than a discretionary modernization effort.

Category-wise Analysis

Product Type Insights

Mercury lamps are anticipated to secure around 45% of the UV curing lamps market revenue share in 2026, reflecting widespread installed base presence across printing, coating, and industrial curing applications. Established reliability, broad wavelength output, and compatibility with diverse ink and coating formulations support continued usage in high-volume production environments. Many manufacturers retain mercury vapor systems due to existing process qualification, workforce familiarity, and integration with legacy production lines. Replacement cycles remain gradual where regulatory enforcement timelines allow continued operation. Operational robustness and consistent curing performance reinforce adoption in applications requiring deep penetration and uniform exposure. Service networks and component availability further strengthen market position, particularly in regions with mature industrial infrastructure.

LED lamps are expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by energy efficiency, extended operational lifespan, and mercury-free compliance alignment. Precise wavelength targeting enhances curing efficiency while reducing thermal stress on substrates. These advantages expand applicability across electronics, healthcare, and advanced material processing. Provider preference shifts toward light-emitting diode systems due to reduced maintenance requirements and predictable output stability. Innovation in power density and modular system design improves scalability across production formats. Accessibility improves as system costs decline through manufacturing scale-up and component standardization.

End-User Insights

Industrial manufacturing is likely to dominate with a projected 38% of the UV curing lamps market share in 2026 owing to the broad application of UV curing lamps across coatings, printing, and assembly processes. Adoption is reinforced by alignment with industrial quality certification frameworks that emphasize consistency, traceability, and defect reduction across high-volume production lines. Ultraviolet curing enables rapid cycle times and uniform curing outcomes, supporting throughput optimization in automated environments. Integration with robotics and conveyor-based systems strengthens process reliability while minimizing rework rates. Energy efficiency and reduced downtime enhance operating cost control, making ultraviolet curing a preferred solution for manufacturers focused on productivity, compliance adherence, and scalable production performance.

Electronics is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by miniaturization trends, high-precision assembly requirements, and contamination-sensitive production environments. Ultraviolet curing supports low-temperature processing, which preserves component integrity in compact circuit designs and advanced semiconductor packaging. Compatibility with cleanroom standards and digital manufacturing platforms strengthens relevance across smart devices and high-density electronics. Equipment integrators and automation specialists play a central role in accelerating adoption through system-level integration and validated process designs. Customizable curing configurations align with diverse electronics formats, supporting rapid innovation cycles and high-yield manufacturing outcomes.

Regional Insights

North America UV Curing Lamps Market Trends

North America demonstrates strong strategic relevance for UV curing solutions, anchored in advanced manufacturing maturity and regulatory-driven technology upgrades. Industrial sectors such as aerospace, automotive, medical devices, and high-performance packaging emphasize precision, reliability, and compliance, creating sustained demand for curing systems that deliver consistent output under controlled conditions. Ultraviolet curing aligns with stringent product quality frameworks and validation protocols, supporting repeatable manufacturing outcomes and traceable process control. Corporate focus on operational efficiency and energy optimization accelerates replacement of legacy thermal and solvent-based curing methods. Environmental compliance initiatives and hazardous material reduction policies reinforce transition toward mercury-free technologies, influencing capital expenditure planning across large manufacturing enterprises.

Growth momentum is shaped by automation intensity, reshoring initiatives, and expansion of high-value manufacturing rather than volume-led industrial expansion. Smart factory adoption increases reliance on curing systems compatible with digital controls, real-time monitoring, and predictive maintenance platforms. Ultraviolet curing supports these priorities through instant response, precise energy delivery, and minimal thermal stress on sensitive components. Demand from electronics assembly, additive manufacturing post-processing, and advanced composites introduces new application complexity that favors high-specification curing technologies. Investment incentives tied to clean manufacturing, energy efficiency, and productivity enhancement encourage modernization of production assets.

Europe UV Curing Lamps Market Trends

Europe plays a significant role in the UV curing lamps market landscape due to a blend of regulatory rigor, established industrial bases, and emphasis on sustainability. Strong environmental policies and chemical restrictions have encouraged early adoption of mercury-free and energy-efficient curing technologies across manufacturing sectors such as automotive, aerospace, and high-precision coatings. Legislative frameworks push manufacturers to exceed minimum compliance, adopting cleaner technologies ahead of mandatory timelines. This proactive stance reduces operational risk, improves life-cycle performance metrics, and aligns with corporate sustainability commitments that influence capital allocation decisions. High output precision industries in this market favor ultraviolet curing for its ability to deliver consistent quality with minimal waste and rapid cycle times.

Growth dynamics are shaped by technological modernization and demand diversification rather than sheer volume expansion. Integration of ultraviolet curing systems with digital quality assurance and predictive maintenance tools enhances productivity and supports lean production models. Manufacturers focusing on bespoke products, limited runs, and high-value applications find value in customizable curing configurations that minimize thermal impact and support material innovation. Investment trends reflect a shift toward automation-ready systems that can be validated within stringent quality management frameworks, enabling manufacturers to balance flexibility with repeatability. Collaborative technology development between equipment suppliers and end users drives incremental improvements in curing efficiency, spectral control, and system uptime. Demand from specialty coatings, optical bonding, and advanced adhesive applications creates pockets of accelerated uptake. Financial incentives tied to energy savings and reduced waste further reinforce investment decisions.

Asia Pacific UV Curing Lamps Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 40% of the UV curing lamps market share, propelled by dense concentration of high-output manufacturing hubs and deep integration of ultraviolet curing within electronics, automotive, packaging, and industrial coatings production lines. Manufacturing ecosystems across China, Japan, South Korea, and India operate on scale-driven efficiency models where rapid curing, inline processing, and defect minimization are operational priorities. Ultraviolet curing supports short production cycles, consistent surface performance, and automation compatibility, aligning with throughput-focused factory design. Export-oriented manufacturing amplifies adoption, as global buyers enforce strict quality and sustainability benchmarks that favor advanced curing solutions. Local availability of equipment suppliers, system integrators, and component manufacturers shortens procurement cycles and reduces deployment risk. Industrial policy emphasis on manufacturing modernization and cleaner production technologies accelerates transition toward energy-efficient and mercury-free systems, reinforcing replacement demand.

Asia Pacific is also poised to be the fastest-growing market for UV curing lamps during the 2026–2033 forecast period, driven by rapid expansion of precision manufacturing, electronics miniaturization, and adoption of advanced materials across high-value industrial applications. Growth momentum reflects increasing complexity of production processes that require low-thermal, high-accuracy curing to protect sensitive components and multilayer assemblies. Ultraviolet curing supports digitalized manufacturing workflows through instant on-off capability, process repeatability, and compatibility with automated inspection systems. Rising investment in electric mobility components, semiconductor packaging, and high-performance coatings creates new application intensity rather than incremental volume demand. Government-backed industrial upgrading initiatives encourage deployment of energy-efficient production tools that enhance export competitiveness and operational resilience. Expansion of local engineering expertise and customization capabilities improves system fit across diverse production formats, lowering adoption barriers for mid-scale manufacturers.

Competitive Landscape

The global UV curing lamps market structure is characterized by moderate fragmentation, with leading players collectively accounting for approximately half of global revenue. This structure reflects a balance between established multinational technology providers and specialized solution developers focused on niche applications. Competitive intensity is shaped less by pricing leverage and more by capability depth across wavelength control, energy efficiency, system integration, and regulatory alignment. Customers prioritize performance reliability, process consistency, and long-term service support, which elevates the importance of engineering expertise and application knowledge. As a result, competitive positioning favors companies that deliver tailored curing solutions aligned with specific production requirements rather than standardized, volume-driven offerings.

Service capability plays a critical role, as customers value installation support, system validation, and lifecycle optimization to protect capital investments. Application-specific customization enables differentiation in segments such as electronics assembly, medical device manufacturing, and specialty coatings, where curing requirements vary significantly. Strategic partnerships with equipment integrators and materials suppliers further strengthen competitive positioning. Key players shaping this landscape include Heraeus Covantics, Phoseon Technology, IST METZ GmbH & Co. KG., Excelitas Technologies Corp., Dymax, and Panasonic Industry Co., Ltd. These companies compete through technology leadership, system-level expertise, and solution adaptability, reinforcing a market environment where innovation, reliability, and customer alignment define competitive success rather than scale alone.

Key Industry Developments

- In December 2025, Polymatech Electronics unveiled a breakthrough high-power UV LED platform engineered for ultra-fast industrial curing that enables sub-one-second curing for UV-sensitive inks, coatings, and adhesives while eliminating mercury and reducing energy consumption.

- In December 2025, Fujifilm’s AQUAFUZE water-based coating technology has won the RadTech Europe Innovation Award 2025 for advancing sustainable UV cure systems with reduced volatile organic compound (VOC) emissions and enhanced performance.

- In May 2025, Kyocera launched a new air-cooled UV LED light source G7A Series designed for compact industrial curing applications, delivering high irradiance performance and eliminating the need for water-cooling systems to enhance manufacturing efficiency and space utilization.

Companies Covered in UV Curing Lamps Market

- Heraeus Covantics

- Phoseon Technology.

- IST METZ GmbH & Co. KG.

- Excelitas Technologies Corp.

- Dymax

- Panasonic Industry Co., Ltd.

- Nordson Corporation.

- BW Converting

- Hoenle AG

- Ushio Inc.

Frequently Asked Questions

The global UV curing lamps market is projected to reach US$ 2.9 billion in 2026.

Rising adoption of rapid, energy-efficient, and mercury-free curing technologies across industrial manufacturing, electronics, printing, and advanced materials processing drives growth.

The market is poised to witness a CAGR of 9.3% from 2026 to 2033.

Expansion of mercury-free UV LED systems, accelerated equipment replacement cycles, and growing demand from precision manufacturing and automation-driven production environments are creating new opportunities.

Some of the key market players include Heraeus Covantics, Phoseon Technology, IST METZ GmbH & Co. KG., and Excelitas Technologies Corp.