- Industrial Machinery

- Industrial Stackers Market

Industrial Stackers Market Size, Share, and Growth Forecast, 2026 – 2033

Industrial Stackers Market by Product Type (Manual Stackers, Electric Stackers, Semi-Electric Stackers), Load Capacity (Light Duty, Medium Duty, Heavy Duty), Application (Warehousing & Logistics, Construction, Retail & Wholesale, Automotive, Food & Beverage, Pharmaceuticals, Others), and Regional Analysis for 2026-2033

Industrial Stackers Market Share and Trends Analysis

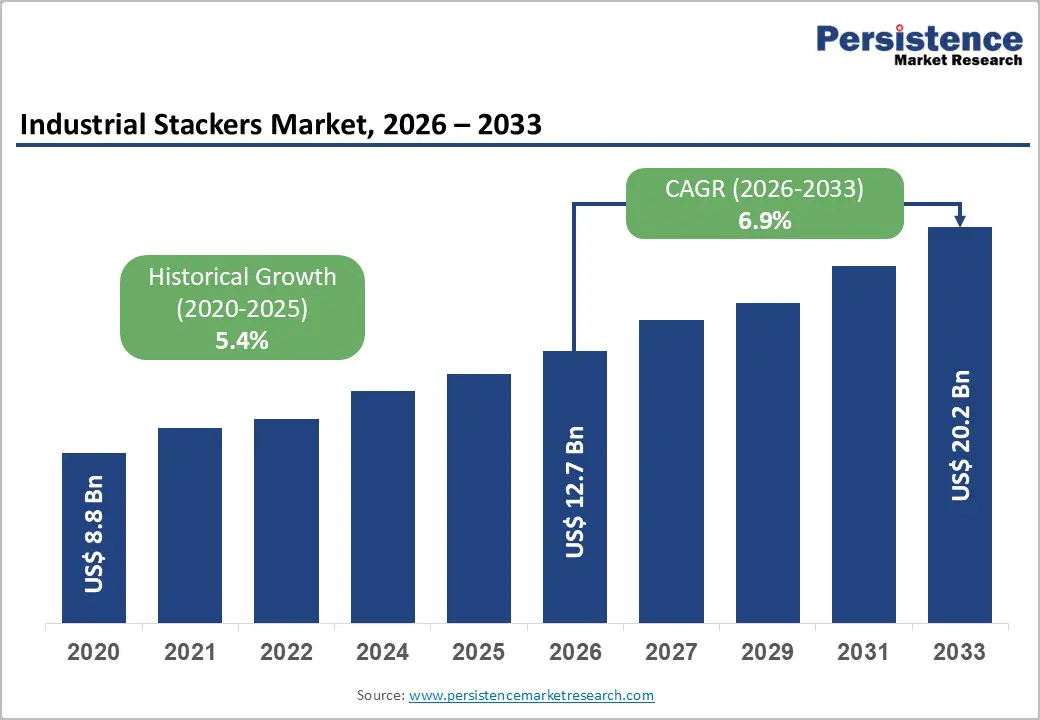

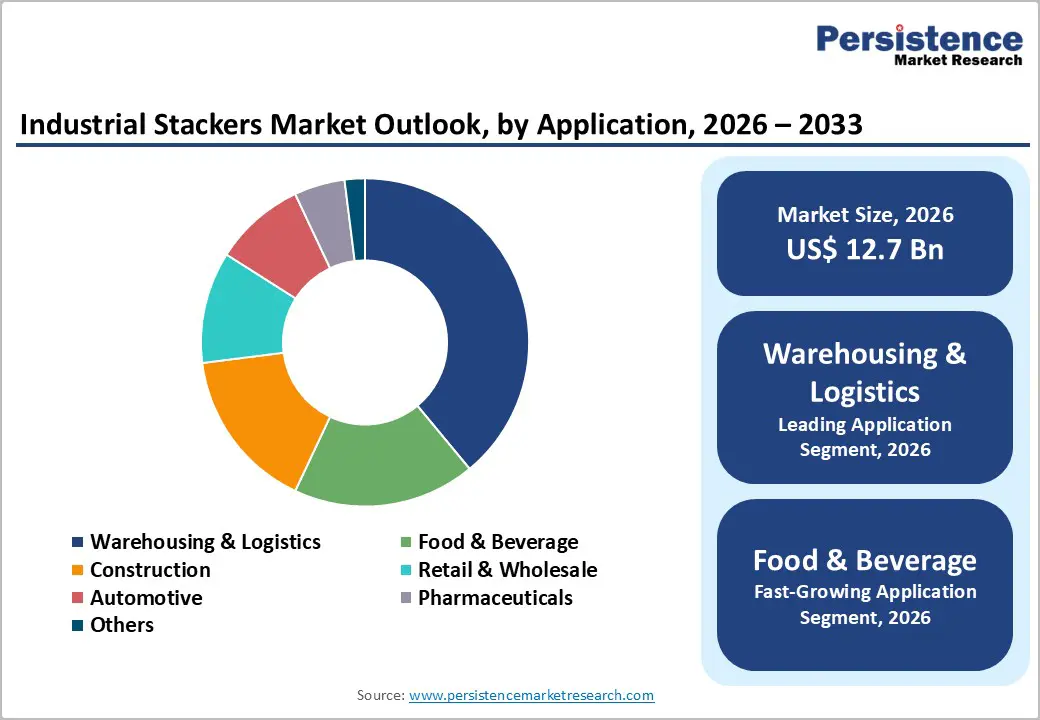

The global industrial stackers market size is likely to be valued at US$ 12.7 billion in 2026, and is projected to reach US$ 20.2 billion by 2033, growing at a CAGR of 6.9% during the forecast period 2026−2033.

The market growth is primarily driven by increasing demand for efficient material handling solutions across warehousing, logistics, and industrial sectors. Rapid expansion of e-commerce and automated warehouses has intensified adoption of stackers to optimize storage density and workflow. Integration of advanced technologies such as IoT-enabled monitoring and electric drive systems enhances operational efficiency, promoting broader deployment. Infrastructure modernization and industrial automation in emerging economies stimulate investment in mechanized handling solutions. Regulatory support for workplace safety and labor protection encourages the replacement of manual lifting with automated stackers. Urbanization and expansion of retail, construction, and manufacturing sectors create structural demand for scalable and flexible material handling equipment.

Key Industry Highlights

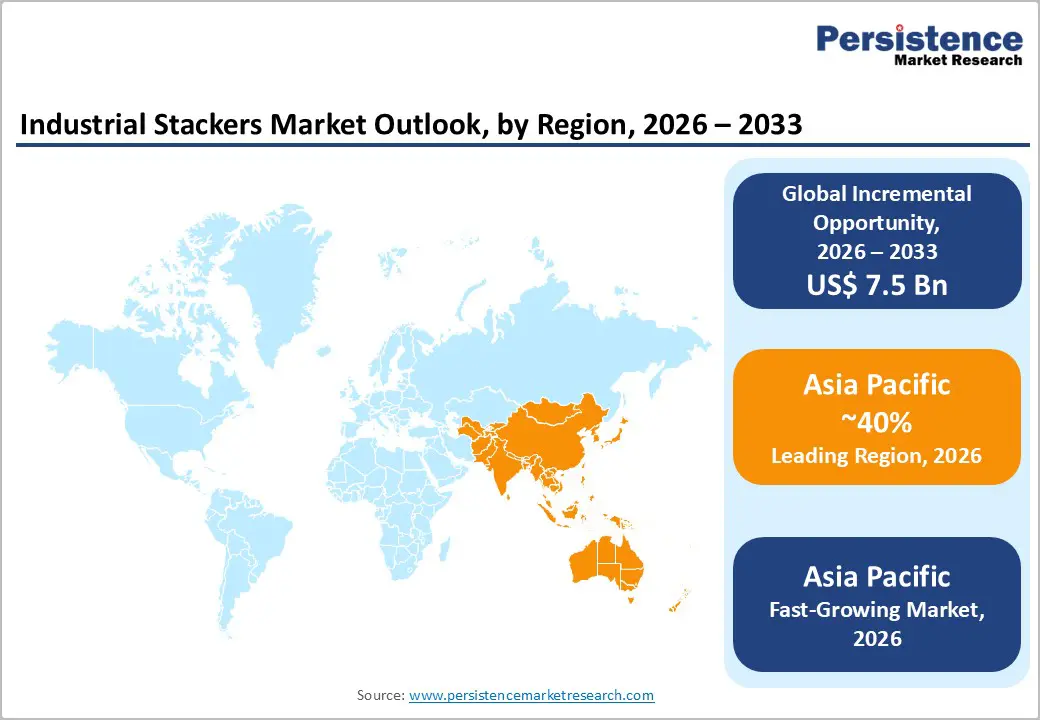

- Dominant Region: Asia Pacific is expected to lead with about 40% market share in 2026, powered by manufacturing growth in China and India.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market through 2033, fueled by e-commerce expansion and warehouse automation in Japan and South Korea.

- Leading Application: Warehousing & logistics is set to command nearly 39% revenue share in 2026, supported by warehouse automation and distribution center expansion.

- Fastest-growing Application: Food & beverage is expected to be the fastest-growing application between 2026 and 2033, driven by rising palletized food storage demand.

- February 2026: Big Joe Forklifts launched the WS25-40 lithium-ion walkie stacker designed for improved productivity in narrow warehouse aisles.

| Key Insights | Details |

|---|---|

| Industrial Stackers Market Size (2026E) | US$ 12.7 Bn |

| Market Value Forecast (2033F) | US$ 20.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Material Handling Equipment

Rapid innovation in material handling equipment has shifted operational priorities from manual labor toward smart, interconnected systems that deliver measurable performance improvements. Smart technologies such as sensors, automated guided systems, and data enabled controls enhance real time visibility of goods movement and reduce errors that previously drove rework and inefficiencies. These advanced tools improve throughput and accuracy in inventory processes, significantly lowering cycle times and error rates as digital workflows replace manual pen and paper practices. A US government safety guideline notes materials handling hazards relate to powered industrial equipment and robotics integration in warehousing, highlighting the need for updated equipment that aligns with evolving operational standards.

Wider adoption of technology also drives safety and compliance, which are increasingly linked to productivity and risk management strategies. Innovative systems such as autonomous mobile robots and advanced control software help minimize workplace injuries linked to heavy equipment movement, addressing key concerns documented by federal workplace safety agencies. As facilities automate more tasks, real time monitoring enables predictive maintenance and reduces unplanned downtime that traditionally eroded throughput and added cost pressures on operations. In an industry projection, U.S. warehousing employment reflects significant participation in warehousing and storage, underpinning the scale at which improved technologies can impact overall performance.

Automation and Labor Cost Pressures

Adopting automated systems for material handling operations directly responds to rising labor expenses while improving throughput and workforce efficiency. U.S. government data shows that nonfarm business sector labor productivity rose 1.9% in the third quarter of 2025 as output expanded faster than hours worked, indicating productivity gains from technology and process improvements alongside stable labor inputs. In practical terms, automation replaces repetitive manual tasks, compresses cycle times, and allows facilities to move goods continuously without incurring overtime or wage escalation, contributing to lower unit labor costs over time.

Labor markets in developed economies continue to exhibit tight employment conditions and skill shortages, elevating hiring difficulty and wage pressures for material handling roles. Employers increasingly allocate capital expenditure toward mechanization and robotics to maintain operational scalability and confront workforce constraints. Automation systems also reduce variability associated with human-driven processes, decrease workload intensity for remaining staff, and align throughput with just in time and high mix order profiles. With unit labor costs representing a meaningful proportion of operational budgets, leveraging automated stackers supports labor cost moderation and drives productivity improvements that align with macroeconomic productivity trends observed in recent government productivity and cost reports.

Competition from Alternative Equipment

Material-handling operations within warehouses and production facilities increasingly rely on a diverse range of equipment capable of performing lifting, transporting, and stacking tasks. Forklifts, pallet trucks, automated guided vehicles, and conveyor-supported systems provide broader operational flexibility across large facilities. Many logistics operators prioritize equipment that supports both vertical lifting and horizontal transportation within a single operational cycle. Such capability reduces operational steps and improves workflow continuity in high-volume environments. Advanced forklift models and automated vehicles integrate sensors, fleet management software, and navigation systems that support digital warehouse infrastructure. These technological capabilities attract enterprises focused on automation, productivity optimization, and integration with warehouse management systems.

Procurement decisions within industrial logistics environments emphasize operational efficiency, workforce productivity, and equipment versatility. Facilities managing bulk cargo, containerized shipments, or high-density racking structures prefer machinery capable of moving goods across extended warehouse zones while performing lifting operations. Multi-purpose material-handling machines reduce equipment fleet size and simplify operator training requirements. Rapid adoption of warehouse automation systems strengthens preference toward vehicles capable of autonomous navigation and integration with digital inventory systems. Modern forklifts and automated vehicles deliver higher load capacities, wider maneuvering capability, and compatibility with automated storage infrastructure. Such characteristics increase substitution potential within warehouses and manufacturing plants.

Stringent Safety and Regulatory Compliance

Workplace safety frameworks governing lifting and material-handling equipment impose strict operational requirements across warehouses, logistics hubs, and industrial facilities. Regulatory authorities mandate operator certification, structured safety training, routine equipment inspections, load-capacity monitoring, and documented maintenance schedules before equipment deployment within operational environments. Compliance procedures introduce administrative complexity for companies managing warehouse fleets and distribution infrastructure. Procurement cycles extend due to documentation verification, internal risk assessment, and legal liability evaluation associated with lifting operations.

Inspection programs conducted by national labor authorities reinforce strict regulatory oversight within industrial workplaces. Regulatory enforcement actions include workplace audits, equipment usage verification, and operational safety assessments across manufacturing plants and distribution facilities. Non-compliance exposure creates financial penalties, operational disruptions, or mandatory corrective actions, which increases risk perception among facility managers and logistics operators. Internal compliance teams often dedicate resources toward documentation management, operator recertification programs, and safety process reviews to maintain regulatory alignment.

Rental and Leasing Models for Flexible Deployment

Flexible equipment access through rental and leasing structures creates a strong opportunity in material-handling operations where warehouse throughput, seasonal demand, and contract-based logistics projects require rapid capacity adjustments. Logistics providers, retail distributors, and third-party fulfillment operators often manage fluctuating order volumes driven by e-commerce cycles, infrastructure projects, or short-term supply contracts. Under such conditions, capital-intensive equipment ownership limits operational agility and ties financial resources to long-term assets. Leasing arrangements support short deployment cycles, enabling operators to scale lifting capacity during peak inventory movement and release equipment once demand stabilizes.

Rapid expansion of warehousing networks and contract logistics facilities strengthens the relevance of temporary equipment deployment models. Public logistics development programs and regulatory frameworks support modernization of storage infrastructure, encouraging private investment in distribution centers and integrated supply chain hubs. Newly established facilities often operate under pilot phases, short-term logistics contracts, or regional distribution trials, which create demand for flexible equipment solutions rather than permanent procurement. Rental fleets enable operators to equip these facilities quickly while maintaining financial flexibility and operational responsiveness.

Shift to Sustainable and Hybrid Technologies

Operational sustainability objectives and tightening environmental regulations are accelerating the transition toward cleaner material-handling technologies across industrial facilities. Manufacturing plants, logistics hubs, and distribution centers increasingly prioritize equipment that aligns with carbon-reduction frameworks and workplace environmental standards. Electrified and hybrid stacker systems support this transition through low-emission operation, reduced noise levels, and improved energy efficiency compared with conventional fuel-driven machines. Such characteristics enable deployment in enclosed warehouse environments, food processing facilities, and pharmaceutical storage areas where air-quality compliance remains critical.

Corporate decarbonization strategies and energy-efficiency programs are strengthening investment interest in hybrid and battery-powered material-handling equipment. Industrial operators increasingly integrate sustainability targets within procurement frameworks, leading to preference for equipment platforms capable of lowering fuel consumption and operational emissions. Hybrid drive systems combine electric propulsion with energy-efficient auxiliary power, enabling flexible operation in facilities that require extended duty cycles while maintaining reduced environmental impact. Energy-efficient stacker designs contribute to lower operating costs through reduced fuel expenditure, simplified maintenance cycles, and improved lifecycle efficiency.

Category-wise Analysis

Product Type Insights

Electric stackers are likely to be the leading segment with nearly 46% revenue share in 2026, due to increasing demand for energy-efficient warehouse equipment and improved operational productivity. Electric stackers enable efficient pallet lifting and transportation with minimal manual effort, supporting high-throughput warehouse environments. Integration of battery-powered drive systems improves lifting precision, load stability, and operator control across distribution centers and manufacturing facilities. Industrial operators prioritize electric equipment due to reduced physical strain on workers and improved operational efficiency compared with manual alternatives. Energy efficiency initiatives within logistics facilities further strengthen demand for electric models.

Semi-electric stackers are expected to witness the fastest growth between 2026 and 2033, as industrial operators seek cost-efficient equipment that balances automation benefits with moderate capital investment. Semi-electric stackers combine manual mobility with electrically powered lifting systems, enabling improved operational efficiency without the higher acquisition cost associated with fully electric models. Small and medium-sized warehouses frequently adopt semi-electric equipment due to budget constraints and moderate handling requirements. Operational flexibility further supports growth. These stackers operate effectively in warehouses where pallet transportation distances remain limited but vertical lifting assistance is required.

Application Insights

Warehousing & logistics is positioned as the leading segment, capturing nearly 39% of the industrial stackers market revenue share in 2026, supported by increasing warehouse automation and expanding distribution infrastructure. Modern logistics networks require efficient pallet handling systems capable of supporting inventory storage, order fulfillment, and goods transportation within distribution centers. Industrial stackers play a critical role in vertical pallet stacking operations and storage optimization within warehouse environments. Growth of third-party logistics providers strengthens equipment demand. Distribution centers handling goods for multiple manufacturers require flexible handling equipment capable of supporting diverse pallet sizes and weight categories.

Food & beverage is expected to emerge as the fastest-growing segment between 2026 and 2033, driven by increasing demand for efficient palletized product storage within food processing and distribution facilities. Food supply chains require organized pallet handling across storage warehouses, refrigerated facilities, and packaging plants. Industrial stackers support safe pallet movement while maintaining operational hygiene standards required for food storage environments. Growth of packaged food distribution networks increases palletized goods transportation across warehouses and cold storage facilities. Stackers enable efficient vertical storage of packaged food products, improving space utilization within temperature-controlled warehouses.

Regional Insights

North America Industrial Stackers Market Trends

North America maintains strong demand for advanced warehouse lifting equipment supported by large distribution networks and a highly organized retail logistics ecosystem. Extensive supply chains serving retail, e-commerce, food distribution, and automotive manufacturing require efficient pallet handling systems within storage and fulfillment facilities. High warehouse throughput and large inventory volumes increase the need for compact stacking equipment capable of supporting vertical storage and rapid pallet movement. The United States represents a major logistics hub with widespread distribution centers linked to highway freight networks and container ports that facilitate high product flow across domestic supply chains.

Warehouse automation initiatives and rapid expansion of fulfillment infrastructure continue strengthening equipment deployment across logistics facilities. Large distribution campuses developed by online retail platforms operate high-density storage systems that rely on electric stacking equipment for internal pallet movement and space optimization. Third-party logistics providers invest heavily in advanced warehouse layouts designed to support fast order fulfillment and multi-channel distribution operations. Industrial sectors including food processing, pharmaceuticals, aerospace manufacturing, and consumer goods production depend on reliable pallet handling systems to maintain efficient internal material flow between production zones and storage facilities.

Europe Industrial Stackers Market Trends

Europe demonstrates strong demand for energy-efficient warehouse equipment supported by environmental sustainability policies and industrial safety standards. Strict workplace emission regulations and operational safety guidelines encourage adoption of electric and low-noise material-handling equipment across logistics facilities and manufacturing plants. Industrial sectors including automotive engineering, machinery manufacturing, pharmaceuticals, and packaged food production rely on structured pallet storage systems that require compact stacking equipment for efficient vertical storage and internal logistics operations. Organized supply chains and advanced warehouse infrastructure strengthen equipment utilization within distribution centers handling high product volumes.

Rapid transformation of warehouse infrastructure further supports equipment demand across logistics networks and industrial supply chains. E-commerce fulfillment hubs, parcel distribution centers, and cross-border logistics facilities operate high-density pallet racking systems that require reliable stacking equipment capable of functioning in narrow-aisle warehouse layouts. Digital warehouse management platforms, automated storage systems, and real-time inventory tracking technologies improve coordination between lifting equipment and supply-chain operations. Industrial operators increasingly prioritize electrified warehouse fleets equipped with lithium-ion batteries and energy-efficient drive systems in order to reduce operational emissions and improve energy efficiency within indoor logistics environments.

Asia Pacific Industrial Stackers Market Trends

Asia Pacific is expected to lead with an estimated 40% of the industrial stackers market share in 2026, supported by a vast industrial production base and rapidly expanding warehousing infrastructure across manufacturing and distribution sectors. Large-scale production of electronics, automotive components, consumer appliances, and packaged goods generates continuous pallet movement across factory floors and logistics facilities. China and India represent major industrial manufacturing centers with extensive factory networks and large distribution systems that require efficient pallet-handling equipment for internal logistics operations. Strong manufacturing output and expanding export trade reinforce warehouse equipment utilization across industrial corridors and port-connected logistics hubs.

Asia Pacific is forecasted to be the fastest-growing regional market for industrial stackers between 2026 and 2033, fueled by rapid expansion of e-commerce fulfillment infrastructure and rising investment in automated logistics facilities. Online retail platforms continue to establish large fulfillment centers designed to manage high-volume product movement, strengthening the requirement for pallet stacking and vertical storage solutions. Japan and South Korea focus on technologically advanced warehouse operations supported by robotics, digital inventory systems, and high-efficiency storage architecture. Expansion of cold-chain logistics, pharmaceutical distribution centers, and food processing warehouses further strengthens demand for reliable warehouse lifting equipment designed for precision material handling and continuous operational efficiency.

Competitive Landscape

The global industrial stackers market structure is moderately fragmented, characterized by the presence of multinational equipment manufacturers and specialized material-handling solution providers. Large companies operate extensive product portfolios that include electric, semi-electric, and manual stackers designed for warehousing, manufacturing, and logistics applications. Competitive positioning focuses on equipment reliability, lifting capacity, energy-efficient drive systems, and long operational life cycles that reduce maintenance requirements in high-volume warehouse environments. Leading manufacturers such as Toyota Industries Corporation, Jungheinrich AG, KION GROUP AG, Crown Equipment Corporation, and Hyster-Yale, Inc. maintain strong global distribution systems supported by dealer networks, service centers, and regional manufacturing facilities.

Competition within the industry also involves a large group of mid-sized manufacturers and regional equipment suppliers that address localized logistics requirements through flexible production capacity and cost-competitive product offerings. These companies supply stackers for small and medium warehouse operators, retail distribution centers, and industrial storage facilities where affordable material-handling solutions remain important for operational efficiency. Dealer-based sales channels and equipment leasing programs play a major role in expanding market access, enabling logistics operators to adopt material-handling equipment without large upfront capital expenditure.

Key Industry Developments

- In November 2025, Konecranes launched a fully electric reach stacker designed for high-intensity container handling operations, delivering up to 16 hours of performance on a single charge and expanding the company’s electrified lift-truck portfolio.

- In August 2025, Toyota Material Handling introduced a new lineup of electric heavy-duty stackers, including walkie reach, walkie straddle, and counter-balanced models designed for warehouse productivity with load capacities ranging from 2,000 to 4,000 pounds and lift heights up to 189 inches.

- In August 2025, SANY Group unveiled the world’s first 50-ton energy-storage reach stacker, designed for handling large energy-storage containers with a 512 kWh swappable battery system enabling more than seven hours of continuous operation.

Companies Covered in Industrial Stackers Market

- Toyota Industries Corporation

- Jungheinrich AG

- KION GROUP AG

- Crown Equipment Corporation

- Hyster-Yale, Inc.

- MITSUBISHI LOGISNEXT CO.LTD.

- Hangcha Forklift

- Bobcat Company.

Frequently Asked Questions

The global industrial stackers market is projected to reach US$ 12.7 billion in 2026.

Expansion of warehouse infrastructure, rising e-commerce logistics activity, and increasing demand for efficient pallet handling in manufacturing and distribution operations are driving the market.

The market is poised to witness a CAGR of 6.9% from 2026 to 2033.

Adoption of electric and hybrid stackers, warehouse automation expansion, and increasing investment in sustainable logistics infrastructure are creating key market opportunities.

Some of the key market players include Toyota Industries Corporation, Jungheinrich AG, KION GROUP AG, Crown Equipment Corporation, and Hyster-Yale, Inc.