- Metalworking & Fabrication

- Industrial Screen Printing Market

Industrial Screen Printing Market Size, Share, and Growth Forecast, 2026 – 2033

Industrial Screen Printing Market by Product Type (Manual Screen Printing Machines, Semi-Automatic Screen Printing Machines, Fully Automatic Screen Printing Machines), Printing Type (Screen Printing, Digital Printing, Flexography, Gravure, Others), End-User (Textile & Apparel Industry, Automotive Industry, Electronics & Electrical Industry, Packaging Industry, Consumer Goods Industry, Industrial Goods, Medical & Healthcare), and Regional Analysis for 2026-2033

Industrial Screen Printing Market Share and Trends Analysis

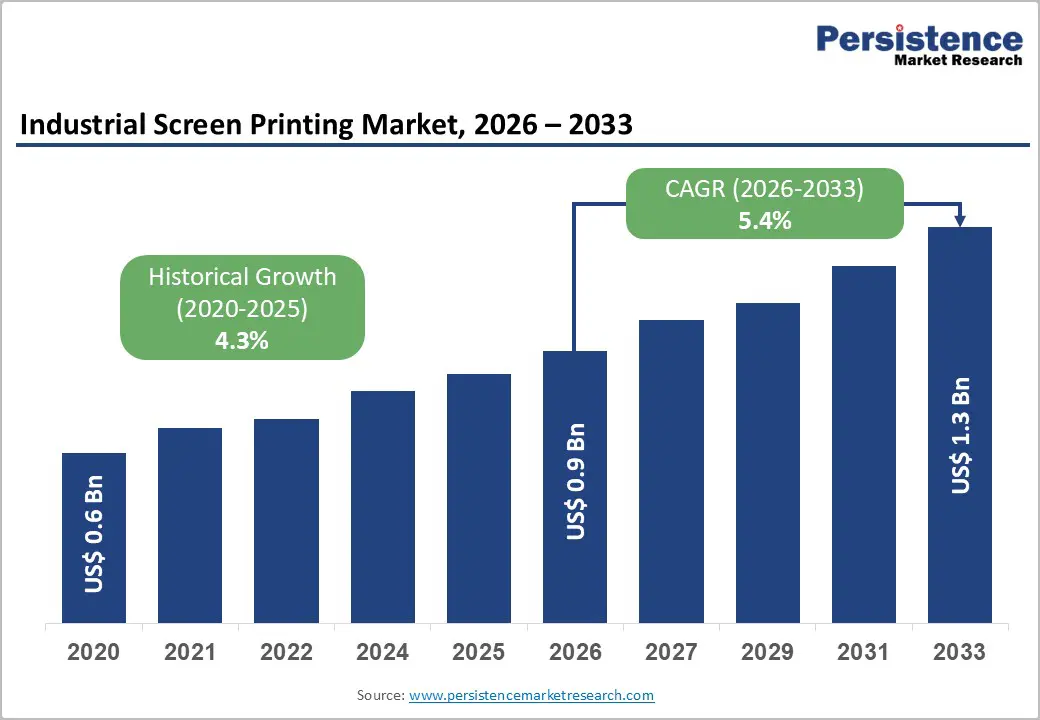

The global industrial screen printing market size is likely to be valued at US$ 0.9 billion in 2026, and is projected to reach US$ 1.3 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026−2033.

Market growth is being driven by increasing industrial automation and integration of digital technologies, which streamline production, improve precision, and reduce labor intensity. Rising demand across textile, automotive, and electronics sectors creates consistent adoption opportunities, as companies seek durable, high-quality printing solutions.

Regulatory emphasis on manufacturing standardization and quality compliance enhances the need for consistent, reliable printing processes. Technological advancements in semi-automatic and fully automated screen printing equipment facilitate scalability, operational efficiency, and resource optimization. Emerging markets with expanding industrial infrastructure present substantial capacity for new installations and modernization of existing systems.

Key Industry Highlights

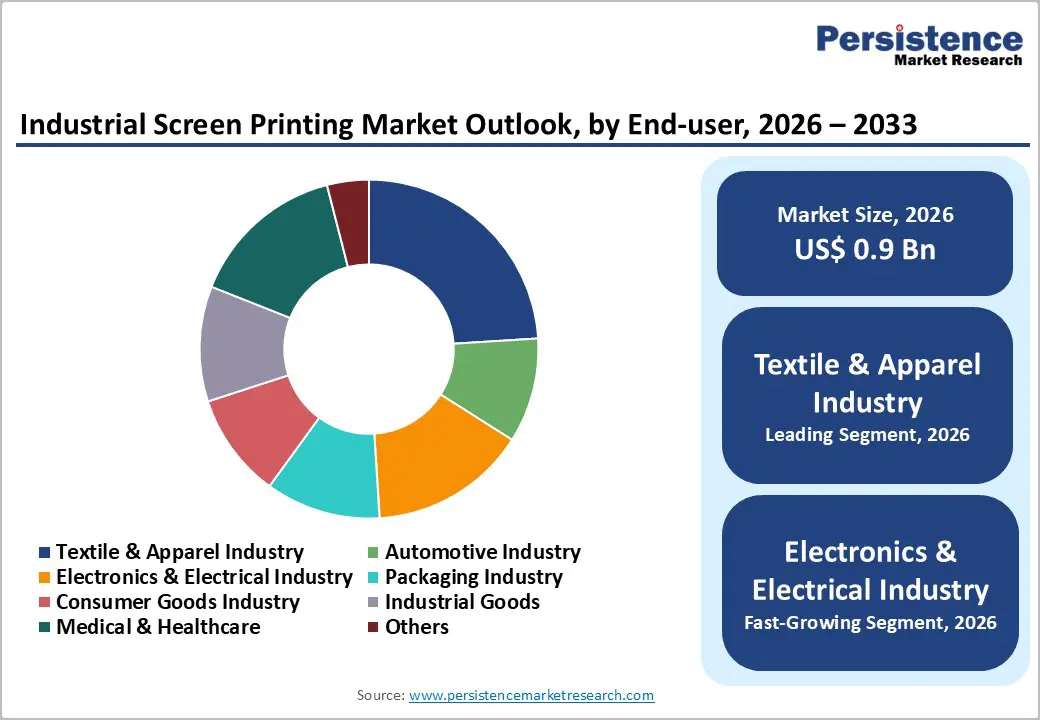

- Leading End-User: The textile and apparel industry is expected to lead with about 40% share in 2026, driven by high-volume fabric printing needs and stringent regulatory quality requirements.

- Fastest-growing End-User: The electronics and electrical industry is slated to grow the fastest between 2026 and 2033, fueled by rising demand for high-precision component printing.

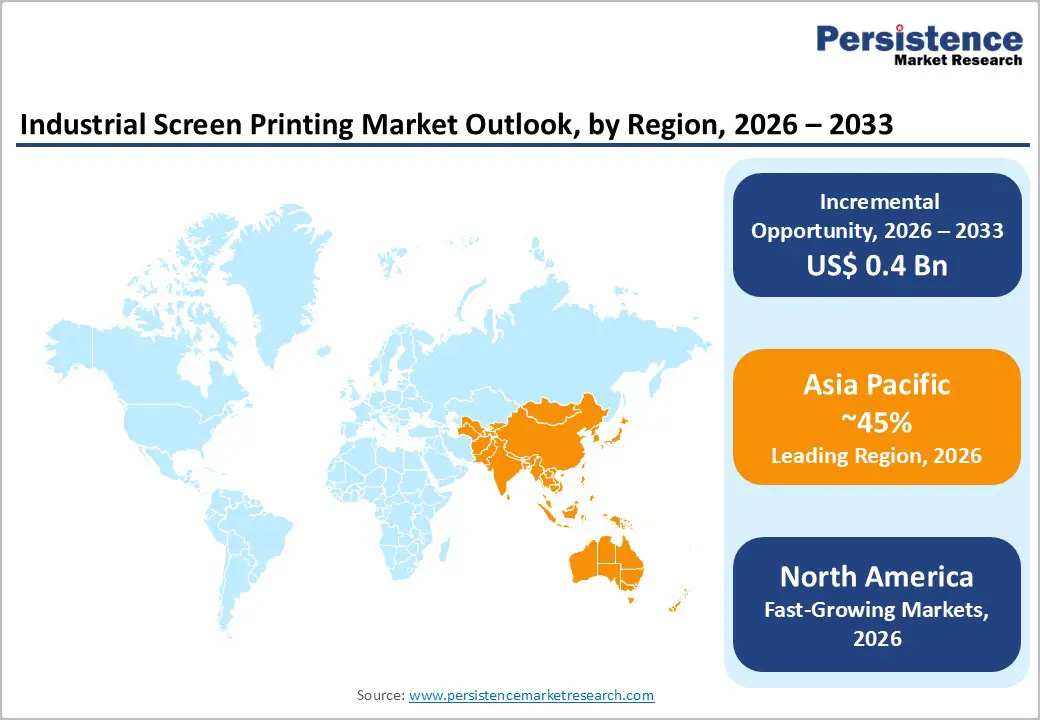

- Dominant Region: Asia-Pacific is set to dominate in 2026, with an estimated 45% share, supported by large-scale manufacturing and strong electronics and textile production.

- Fastest-growing Market: North America is projected to be the fastest-growing market through 2033, on account of advanced manufacturing adoption and high demand for high-precision customized printing.

- December 2025: Embee Group debuted its Sapphire and Emerald direct-to-fabric digital printers at ITMA Asia, along with a hybrid rotary-digital machine for versatile, sustainable textile production.

| Key Insights | Details |

|---|---|

| Key Insights | Details |

| Industrial Screen Printing Market Size (2026E) | US$ 0.9 Bn |

| Market Value Forecast (2033F) | US$ 1.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements in Screen Printing Equipment

Automation and digital integration in screen printing equipment has transformed production operations by improving throughput, quality consistency, and operational efficiency. Modern systems provide precise registration, uniform ink deposition, and real-time process monitoring, reducing manual setup and minimizing errors. Manufacturers achieve faster cycle times and higher equipment utilization, supporting lean production practices while lowering material waste.

Smart sensors and predictive maintenance functions enhance uptime and ensure continuous operation, enabling adherence to strict delivery schedules and exacting product specifications. These capabilities allow adaptation to diverse substrates and specialty applications, such as high-precision electronics and specialty industrial components, where repeatability and accuracy are critical. Software-driven controls ensure consistent output across large-scale runs, improving yield, reliability, and cost efficiency while supporting flexible production demands.

Advanced equipment also enables manufacturers to respond quickly to evolving market requirements and customized production requests. Enhanced automation reduces dependence on skilled labor for repetitive tasks, allowing teams to focus on quality assurance and process optimization. Process standardization, combined with real-time monitoring, strengthens operational control and minimizes the risk of defects or delays. Investment in modern equipment strengthens production resilience, scalability, and the ability to maintain consistent quality across multiple production lines. Precision, speed, and adaptability provided by these technologies make innovation in equipment design a central driver of operational performance and long-term competitiveness.

Availability of Substitute Technologies

The growing availability of substitute printing technologies poses a critical constraint on traditional screen-based printing methods, as these methods are less able to meet evolving customer and business needs. Alternative printing technologies such as digital inkjet and direct-to-garment (DTG)/direct-to-film (DTF) eliminate many inherent limitations of screen processes by minimizing setup time, reducing dependency on manual preparation and fixed screens, and enabling on-demand customization without the economies-of-scale barriers that have historically favoured analogue methods. In commercial applications where design complexity, rapid iteration and short runs are standard expectations, these substitutes can complete jobs with significantly less overhead and operational complexity, leading many buyers to favour them over older techniques.

From a strategic perspective, the presence of compelling substitutes reduces price flexibility and lengthens sales cycles for vendors reliant on screen processes. Buyers weighing the total cost of ownership now often prioritize throughput, flexibility, and lean-production alignment over legacy performance advantages.

Substitute technologies also align more closely with sustainability and lean principles by reducing waste, energy consumption and material use, which increasingly influence procurement decisions across sectors. Companies that do not differentiate their core offerings or transition portions of their portfolio face stagnating demand, weaker customer retention and intensified competitive pressure from digitally enabled entrants.

Adoption of Hybrid and Functional Printing Applications

The expansion of hybrid and functional printing applications is driven by the increasing demand for versatile production techniques that integrate multiple functionalities into a single process. Industries such as electronics, automotive, and packaging seek solutions that combine traditional decorative printing with conductive, protective, or sensor-enabled layers. This trend enables manufacturers to streamline operations, shorten production cycles, and achieve greater precision in product customization.

Functional printing enables the direct embedding of electronic circuits, smart sensors, and advanced coatings onto substrates, reducing reliance on separate assembly processes and supporting lean manufacturing principles. The ability to produce multifunctional components within a single workflow enhances operational efficiency while reducing material waste and energy consumption.

The shift toward hybrid approaches also aligns with the broader technological trend of miniaturization and intelligent product design. Companies are exploring ways to integrate electronic or responsive elements into everyday objects without increasing complexity or cost. The adaptability of hybrid printing supports experimentation with new materials, substrates, and inks, fostering innovation in product development. This approach provides a platform for rapid prototyping, shorter time-to-market, and scalable production of complex designs. Manufacturers leveraging these applications can respond more effectively to evolving customer demands for smart, multifunctional products while maintaining consistent quality standards and cost-effectiveness.

Category-wise Analysis

Product Type Insights

Fully automatic machines are poised to lead, with a forecasted 45% share of the industrial screen printing market revenue in 2026, owing to high-volume production capabilities, minimal labor requirements, and the integration of automation technologies. Precision alignment, reduced human error, and consistent output quality enhance suitability for electronics, automotive, and packaging applications. The segment’s ability to deliver scalable solutions aligns with industrial efficiency standards and operational compliance requirements. Adoption is further supported by long-term cost savings, compatibility with predictive maintenance, and compatibility with advanced inks and substrates.

Semi-automatic machines are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by moderate capital investment, flexible deployment, and ability to upgrade from manual systems. They bridge the gap between manual and fully automated solutions, enabling incremental automation adoption while maintaining production control. Industries with variable production-volume requirements benefit from operational versatility and reduced training requirements. Enhanced functionality, integration with digital controls, and adaptability to diverse substrate types position the segment for rapid adoption in emerging and mid-sized industrial facilities.

Printing Type Insights

Screen printing is expected to be the leading segment, with a projected 55% market share in 2026, due to its versatility, durability, and compatibility with diverse substrates, including textiles, plastics, and electronics. Its ability to maintain consistent print quality at high volumes positions it as a preferred method for industrial applications that require repeatable accuracy and robust visual appeal. The process supports a wide range of ink types and coatings, enabling production of both functional and decorative layers. Operational efficiency is reinforced by long-term reliability, minimal maintenance requirements, and compatibility with automated and semi-automated production lines, making it a trusted choice for industrial-scale manufacturing.

Digital printing is expected to grow the fastest between 2026 and 2033, driven by customization, short-run production efficiency, and integration with e-commerce-driven supply chains. The flexibility of digital platforms supports on-demand printing, allowing manufacturers to meet rapidly shifting consumer preferences and small-batch production needs without extensive setup times. Integration with automated workflow and computer-aided design platforms streamlines operations, reduces manual intervention, and optimizes material usage, supporting sustainability goals. This adaptability positions digital printing as a key enabler for fast-moving industries seeking agile production while maintaining high-resolution output and operational efficiency across diverse product lines.

End-User Insights

The textile & apparel industry is slated to hold a dominant position, with an anticipated 40% of market share in 2026, driven by high-volume demand for patterned fabrics, branding, and packaging solutions. Adoption is reinforced by the need to maintain consistent quality and meet regulatory standards for durability, colorfastness, and safety. Automated screen-printing equipment enhances production efficiency by reducing manual labor and enabling high-speed operations. Technological compatibility with a variety of inks, patterns, and substrates enables manufacturers to maintain repeatable precision across large-scale production runs.

The electronics & electrical industry is forecast to be the fastest-growing end-user segment between 2026 and 2033, driven by increased adoption of printed circuit boards, labeling, and component marking. Market adoption is driven by the demand for high-precision, fine-detail printing necessary for compact electronic components. Investment in automated and semi-automated machinery helps ensure compliance with strict safety and quality regulations while improving throughput.

Expansion is further supported by growth in consumer electronics, automotive electronics, and industrial electrical applications. Integration with advanced quality monitoring systems enhances consistency, optimizes material usage, and reduces operational risks, enabling scalable production while maintaining compliance and efficiency.

Regional Insights

North America Industrial Screen Printing Market Trends

North America is forecasted to be the fastest-growing regional market for industrial screen printing technologies between 2026 and 2033, stimulated by rapid adoption of advanced manufacturing technologies and increasing demand for high-precision, customized products. Growth is driven by the convergence of digital and hybrid printing platforms with automated production systems, enabling short-run manufacturing, rapid prototyping, and integration with e-commerce-driven supply chains. Electronics, medical devices, aerospace components, and specialty packaging increasingly require functional inks, fine-detail printing, and consistent high-resolution output, creating sustained demand for advanced screen printing solutions.

Investment in research and development fosters innovation in materials, substrates, and printing processes, while robust industrial clusters reduce implementation risk and accelerate technology deployment. Regulatory emphasis on environmental compliance, quality assurance, and product traceability reinforces adoption of automated and hybrid solutions.

The growth trajectory of the market here is further strengthened by the rising demand for smart and multifunctional products, which integrate sensors, conductive pathways, or protective coatings into printed components. Collaboration between manufacturers, technology providers, and standards organizations ensures compliance with industry-specific regulations while facilitating rapid adoption of innovative production methods. Workforce expertise, coupled with infrastructure investments in automation, robotics, and digital quality monitoring, reduces resource wastage, shortens lead times, and improves production reliability. Companies increasingly implement predictive maintenance and process optimization systems to ensure consistent output and operational continuity. Integration of industrial screen printing into advanced manufacturing ecosystems enables seamless alignment with electronics, medical, and consumer goods production.

Europe Industrial Screen Printing Market Trends

The market in Europe is foreseen to demonstrate significant growth in industrial screen printing, supported by strong emphasis on precision manufacturing, regulatory compliance, and sustainable production practices. Demand in electronics, automotive components, medical devices, and packaging drives adoption of high-resolution and functional printing technologies capable of delivering consistent quality across complex substrates. Advanced manufacturing hubs integrate automated and hybrid systems with digital workflow platforms, enabling rapid prototyping, small-batch production, and high-volume output without compromising accuracy or throughput. Investment in research and development encourages experimentation with conductive inks, sensor integration, and multifunctional coatings, facilitating innovation in smart electronics, wearable devices, and specialty packaging.

Government policies and industrial standards promoting environmental responsibility, safety, and product traceability reinforce adoption, ensuring operational processes meet both international compliance and customer expectations.

Growth is further driven by increasing demand for customization, short-run production, and lightweight, high-performance components in automotive, aerospace, and consumer electronics sectors. Industrial ecosystems benefit from collaboration between manufacturers, technology providers, and standards organizations, creating knowledge networks that accelerate adoption of advanced printing techniques and reduce implementation risk. Skilled workforce availability and infrastructure investments in automation and quality monitoring systems enhance production efficiency, minimize material waste, and ensure repeatable high-quality output. Integration of industrial screen printing into broader manufacturing systems supports supply chain optimization, predictive maintenance, and resource utilization, positioning Europe as a hub for high-precision, innovative, and sustainable printing applications across diverse industrial segments.

Asia Pacific Industrial Screen Printing Market Trends

In 2026, Asia Pacific is projected to hold approximately 45% of the industrial screen printing market share, driven by large-scale manufacturing capabilities and a diversified industrial base. Electronics production ecosystems, including printed circuit board assembly, component marking, and device integration, generate high-volume demand for precise and repeatable printing processes. The textile and apparel sector further contributes to adoption, integrating branding, functional printing, and patterning directly into fabrics and packaging. Competitive labor cost structures, dense supplier networks, and advanced infrastructure enable efficient deployment of automated and hybrid printing systems. Government initiatives promoting industrial modernization, export competitiveness, and technological adoption reinforce capacity expansion, while robust logistics and clustering effects facilitate rapid scaling of production across multiple industrial sectors.

Leadership in Asia Pacific is reinforced by alignment between industrial policy and global supply chain integration, encouraging high-value manufacturing, export-oriented electronics production, and textile innovation. Government-reported data indicates electronics production increased nearly sixfold, with exports rising eightfold over the last decade, reflecting growing industrial output and integration into international markets.

Advanced manufacturing clusters and technology adoption accelerate implementation of automated, hybrid, and functional printing applications, supporting fine-detail printing, compliance with safety standards, and scalable throughput. Concentration of skilled workforce, material availability, and innovation networks reduces operational risk, enhances cost efficiency, and strengthens structural advantage sustaining long-term market dominance in industrial screen printing.

Competitive Landscape

The global industrial screen printing market structure demonstrates moderate fragmentation, with leading players such as MHM Siebdruckmaschinen GmbH, M&R Companies, ATMA CHAMP ENT. CORP., and DEK Printing Machines Ltd. collectively accounting for approximately 45% of overall market share. These manufacturers differentiate through technological innovation, including high-precision printing systems, automated and hybrid platforms, and advanced functional printing capabilities. Investment in research and development allows these companies to deliver solutions tailored to electronics, textile, and specialty packaging sectors, while enhancing operational efficiency, repeatability, and throughput for industrial clients. Service offerings, including maintenance, training, and digital workflow integration, further strengthen customer retention and create competitive barriers for smaller suppliers.

Market concentration and competitive dynamics vary across different territories. Established manufacturers dominate industrial clusters in Europe and North America, where infrastructure, skilled workforce, and regulatory standards reinforce adoption of advanced screen printing systems. In contrast, Asia Pacific reflects a broader and more diverse vendor base, with emerging suppliers offering flexible, low-cost solutions alongside established players, fostering innovation and expansion of production capabilities.

Competitive strategies increasingly focus on automation, multi-functional printing integration, and after-sales service differentiation, enabling leading players to capture high-value industrial contracts while smaller vendors target specialized applications

Key Industry Developments

- In September 2025, researchers from the Technical University of Darmstadt and Karlsruhe Institute of Technology (KIT) developed fully screen-printed 3D thermoelectric generators (TEGs) using silver selenide and antimony telluride inks with carbon interlayers. The flexible devices deliver 1.22 mW from a 43 K gradient, enabling milliwatt-scale wearable/IoT power for scalable printing.

- In July 2025, Koala Paper launched a waterproof PET-based inkjet film for screen printing plate-making, featuring a microporous coating that absorbs water-based inks for quick-drying, smudge-free, high-density positives. The 140 g/m² film offers dimensional stability, 13±2 haze for contrast, and versatility for UV exposure, flexo/pad printing, and PCB imaging.

- In May 2025, Gallus Rotascreen unveiled a new rotary screen printing unit at the SPI Exhibition in Essen, Germany, offering retrofittable screen-printing capability for narrow-web presses and designed to enhance precision and integration in label production workflows.

Companies Covered in Industrial Screen Printing Market

- MHM Siebdruckmaschinen GmbH

- M&R Companies

- ATMA CHAMP ENT. CORP.

- DEK Printing Machines Ltd.

- Durst Group

- GrafcoAST

- Kammann Machines

- Serigraph Inc.

- SPGPrints B.V.

- Systematic Automation, Inc.

Frequently Asked Questions

The global industrial screen printing market is projected to reach US$ 0.9 billion in 2026.

High-volume industrial production demand, requirement for durable and high-precision printing on diverse substrates, increasing adoption of automation, and growing use of functional and hybrid printing applications are driving the market.

The market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Adoption of hybrid and functional printing applications, integration with automated manufacturing systems, expansion of electronics and textile production, and rising demand for customized industrial printing are creating new market opportunities.

Some of the key market players include MHM Siebdruckmaschinen GmbH, M&R Companies, ATMA CHAMP ENT. CORP., DEK Printing Machines Ltd.