- Industrial Machinery

- Industrial Foam Guns Market

Industrial Foam Guns Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Foam Guns Market by Foam Type (Closed-cell, Open-cell), Material (Aluminum, Plastic, PTFE-Coated), Application (Manufacturing, Aerospace & Defense, Others), and Regional Analysis 2026 - 2033

Industrial Foam Guns Market Size and Trends Analysis

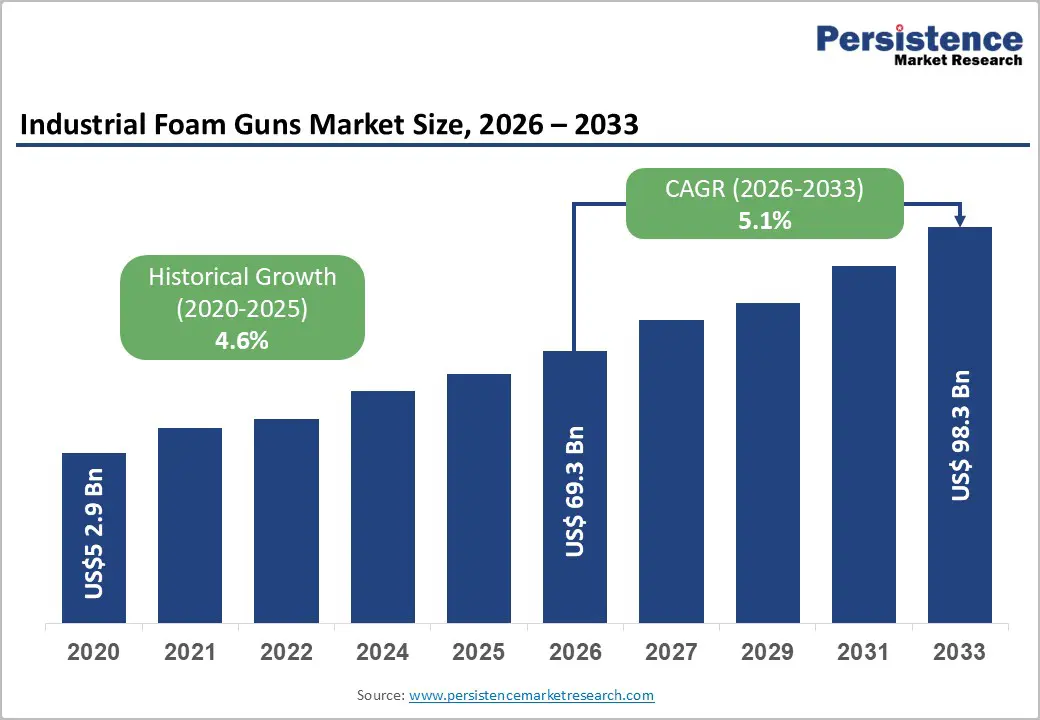

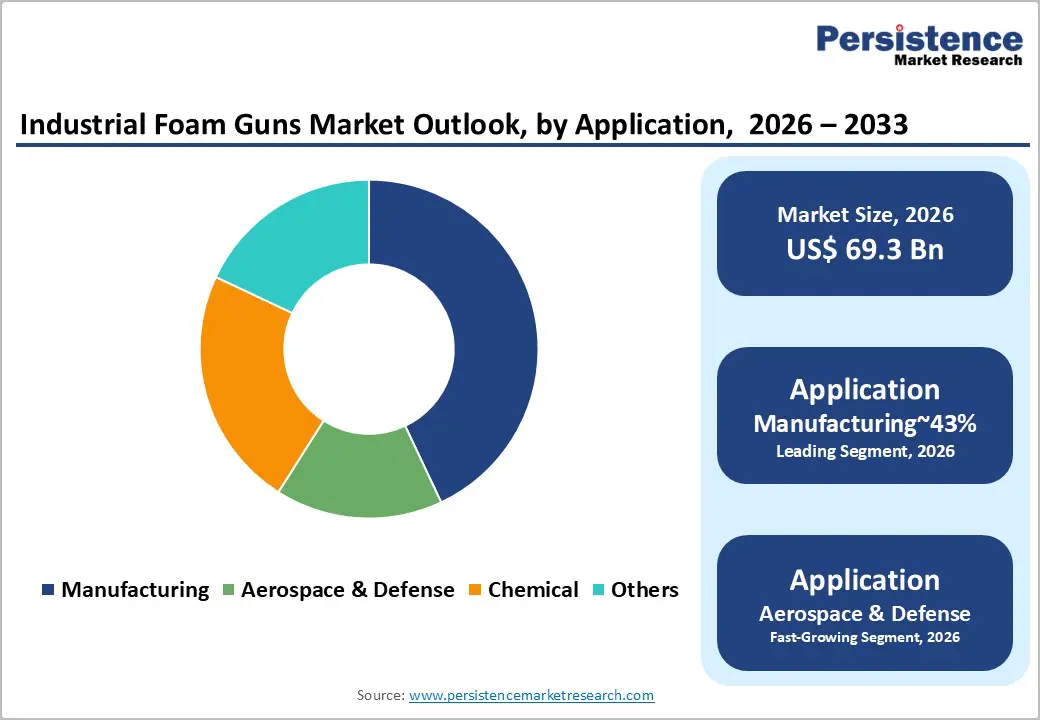

The global industrial foam guns market size is likely to be valued at US$69.3 billion in 2026 and is expected to reach US$98.3 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by the rising demand in manufacturing for precision sealing and insulation, alongside aerospace lightweighting needs.

The market expands via automation in manufacturing and regulatory pushes for energy-efficient insulation. Primary growth factors include expanding construction activities, driven by urbanization and infrastructure development, and usage in insulation applications. Technological advancements in gun designs, such as improved ergonomics and automation integration, have enhanced efficiency, reducing material waste in manufacturing settings.

Key Industry Highlights:

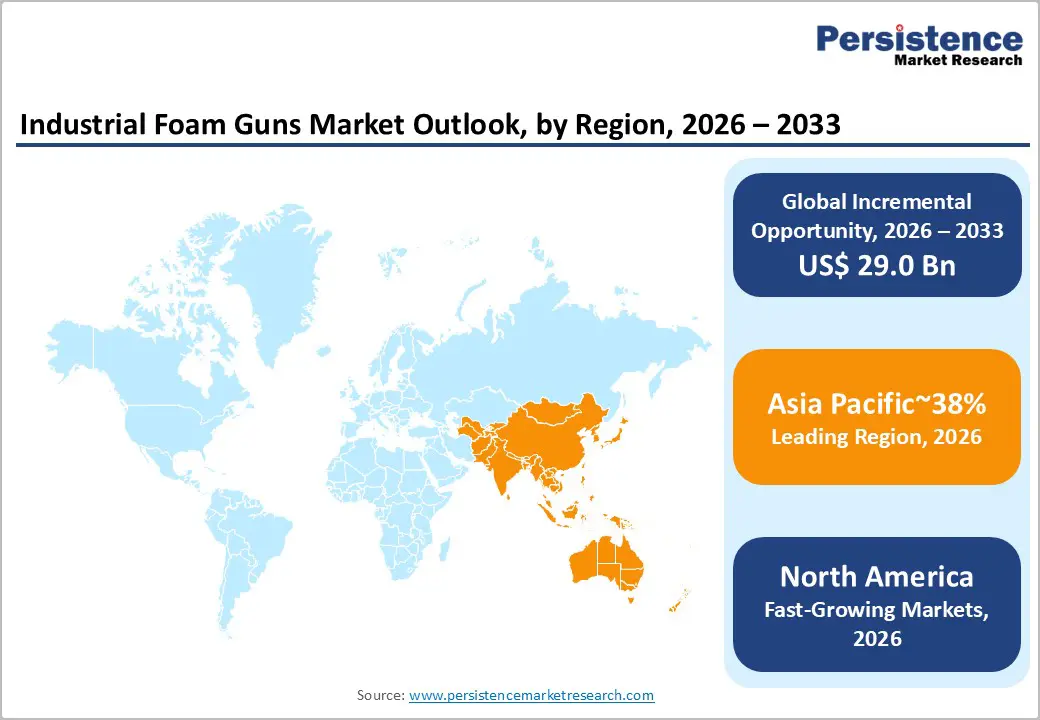

- Leading Region: Asia Pacific is projected to lead with approximately 38% of the global market share in 2026, due to deep manufacturing penetration, advanced automation adoption, and a robust industrial ecosystem.

- Fastest-Growing Region: North America is anticipated to grow fastest due to industrial expansion, supportive policy frameworks, and technology-driven adoption across construction, aerospace, and automotive sectors.

- Leading Material: Aluminum is projected to dominate the material segment for simplicity, durability, adoption, and functional use across key sectors, holding approximately 52% of market demand in 2026.

- Leading Application: Manufacturing is expected to lead, accounting for approximately 42% in 2026, through industrial adoption, automated throughput, quality control, and high-value applications in appliances, electronics, and industrial machinery production.

| Key Insights | Details |

|---|---|

|

Industrial Foam Guns Market Size (2026E) |

US$69.3 Bn |

|

Market Value Forecast (2033F) |

US$98.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Manufacturing Automation

The expansion of manufacturing automation is structurally increasing demand for industrial foam guns across production facilities globally. Automation initiatives in high-volume manufacturing enhance precision in sealing, bonding, and insulation applications, creating consistent requirements for controlled foam dispensing equipment. Industrial foam guns enable optimized material usage, directly reducing waste and improving process efficiency, while aligning with cost containment and lean production frameworks. This trend is particularly pronounced in complex assembly lines where repeatability and accuracy are critical for maintaining product quality and operational throughput. Regulatory standards for occupational safety and environmental compliance further reinforce the adoption of automated dispensing solutions, as precise foam application minimizes exposure to hazardous chemicals and reduces emissions associated with overuse of polymer-based materials.

Automated foam dispensing influences upstream material procurement and downstream operational planning by reducing excess inventory requirements and lowering scrap management costs. Integration of foam guns with robotics and programmable logic systems enhances workflow synchronization, enabling factories to achieve higher productivity without proportional labor increases. Regional adoption patterns reflect concentrated investment in Asia Pacific manufacturing hubs, where automation-driven efficiency gains are directly linked to competitive industrial positioning. The synergy between automation and foam gun utilization is creating a stable and technically sophisticated market expansion pathway.

Technological Advancements in Dispensing Systems

Rapid technological evolution in foam dispensing systems is significantly shaping the industrial foam gun market dynamics. Innovations such as IoT-enabled foam guns allow real-time monitoring of material usage, optimizing consumption and reducing operational waste across manufacturing and aerospace applications. Integration with automated production lines enhances precision in sealing, bonding, and insulation processes, aligning with regulatory standards for efficiency, safety, and environmental compliance. These advancements address labor shortages and skill gaps by reducing dependence on manual operations, while simultaneously improving throughput and product consistency. The convergence of sensor technology, data analytics, and programmable logic control reinforces process reliability and supports cost-efficient operations across complex assembly environments.

The adoption of smart dispensing systems influences upstream procurement strategies, as precise material usage minimizes excess inventory and mitigates supply chain variability. Downstream, reduced waste and enhanced repeatability lower operational costs and improve margins, particularly in high-precision sectors such as aerospace and automotive manufacturing. Regional disparities in skilled labor availability further drive adoption, with developed markets leveraging automation to offset workforce shortages, while emerging economies benefit from enhanced productivity. These technological improvements are establishing a structurally efficient, precision-oriented demand trajectory for industrial foam guns.

Barrier Analysis - Health and Safety Risks

The application of industrial foam in manufacturing and construction introduces significant occupational health and safety challenges, particularly due to exposure to isocyanates. These chemical compounds are associated with respiratory sensitization, skin irritation, and other long-term health effects, creating regulatory pressure for stringent handling protocols. Compliance with regional safety standards requires extensive training, monitoring, and investment in protective measures, including high-grade personal protective equipment, fume extraction systems, and controlled work environments. Such regulatory and operational obligations increase the cost of adoption, affecting procurement decisions across cost-sensitive industrial facilities and limiting rapid market penetration.

The health and safety constraints influence both upstream material selection and downstream operational workflows. Manufacturers must invest in specialized storage, dispensing infrastructure, and maintenance routines to mitigate chemical exposure, which can reduce overall process efficiency. Regulatory enforcement varies across regions, creating uneven adoption patterns and impacting cross-border supply chain strategies. Additionally, insurance requirements and liability considerations further embed cost and compliance burdens, constraining growth in markets where safety expenditures are prohibitive. Occupational health risks remain a persistent barrier to widespread foam gun integration.

Economic Sensitivity in Construction

The industrial foam gun market is materially influenced by economic cycles, particularly within the construction & building segment, which represents a substantial portion of overall demand. Fluctuations in interest rates and financial conditions directly affect project financing, causing delays or cancellations of infrastructure developments. Slowdowns in real estate activity reduce the deployment of foam-based sealing, insulation, and bonding applications, constraining procurement volumes and disrupting production schedules for manufacturers. Regional disparities in economic stability further exacerbate adoption variability, with emerging markets more vulnerable to investment deferrals, while developed markets exhibit moderated but persistent sensitivity to cyclical construction spending.

The economic pressures influence upstream material procurement, inventory management, and logistics planning. Manufacturers face reduced throughput requirements during market contractions, leading to underutilized capacity and heightened cost-per-unit pressures. Project deferrals also impact downstream contractors and integrators, limiting workflow continuity and creating intermittent demand patterns for precision dispensing systems. Collectively, macroeconomic volatility introduces structural uncertainty into market expansion projections, emphasizing the dependence of industrial foam gun consumption on broader construction investment trends and fiscal policy stability.

Opportunity Analysis - Transition to Smart Dispensing Systems

The industrial foam gun market is increasingly positioned to benefit from the integration of IoT and AI-enabled dispensing technologies, which offer substantial operational efficiencies across high-precision sectors. Smart foam guns enable real-time monitoring of material usage, predictive maintenance scheduling, and automated flow regulation, ensuring consistent bead thickness and application accuracy. These capabilities are particularly critical in aerospace and automotive manufacturing, where uniformity, weight optimization, and compliance with engineering tolerances are essential. Regulatory frameworks emphasizing process safety, environmental compliance, and material conservation further reinforce adoption, as smart systems reduce waste and support adherence to stringent production standards.

The integration of IoT and AI transforms upstream procurement and inventory management by facilitating data-driven forecasting and reducing material overstocking. Downstream operations benefit from reduced rework, enhanced process repeatability, and lower labor dependency, while analytics platforms provide actionable insights for continuous process improvement. Regional adoption is influenced by industrial automation maturity, with developed markets leading in early implementation and emerging economies gradually integrating these technologies. Mutually, the shift toward smart dispensing establishes a structurally efficient, technology-driven growth trajectory for industrial foam guns.

Rise of Modular and Prefabricated Construction

The transition toward modular and prefabricated construction is structurally increasing demand for automated foam dispensing solutions within controlled factory environments. Prefabricated components produced off-site require precise, repeatable application of sealing and bonding materials, which robotic foam dispensing arms can deliver efficiently. This evolution enables manufacturers to integrate industrial foam guns directly into automated assembly lines, supporting consistent quality, faster throughput, and reduced material waste compared with traditional on-site application methods. Regulatory and safety frameworks also favor controlled factory-based operations, minimizing occupational exposure to isocyanates and improving compliance with environmental and workplace standards.

Modular construction reshapes upstream design and procurement processes, emphasizing compatibility between foam guns and robotic systems while optimizing material flow. Downstream, adoption of plug-and-play gun heads supports scalability and flexible production scheduling, reducing labor dependence and improving operational predictability. Regional construction trends, particularly in developed markets with high modular adoption, create early demand for technologically advanced dispensing equipment, while emerging markets gradually follow as prefabrication infrastructure expands. The dynamics establish a significant, technology-driven opportunity for industrial foam gun manufacturers targeting automated construction workflows.

Category-wise Insights

Material Insights

Aluminum is expected to lead, accounting for approximately 52% share in 2026, underpinned by its superior durability, chemical resistance, and structural stability across high-pressure manufacturing and professional industrial workflows. Adoption remains anchored by operational precision, long service life, and ease of maintenance, with enterprises prioritizing workflow integration and consistent throughput in heavy-duty applications. Ongoing platform evolution, advanced alloy formulations, and modular rod systems continue to reinforce replacement cycles and utilization intensity. Leading manufacturers such as Graco, Soudal, and ITW Dynatec leverage these platforms to lock in enterprise workflows and optimize performance across demanding chemical, aerospace, and construction applications. This combination of mature infrastructure, proven reliability, and predictable material compatibility sustains the segment’s dominance within structured industrial deployment models.

Plastic is expected to be the fastest-growing segment in the Industrial Foam Gun market, driven by emerging needs for lightweight, corrosion-resistant tools and semi-disposable workflows across portable and chemical-intensive applications. Growth is being catalyzed by advanced polymer engineering, ergonomic designs, and enhanced non-stick surfaces, which materially improve operator comfort, speed, and adaptability in high-volume and DIY scenarios. Accelerating adoption is supported by integration with cartridge systems, automation-friendly manifolds, and modular designs that lower operational friction for first-time adopters. Leading brands such as Bostik, Fischer, and Würth are introducing new product lines that capture early-cycle demand, embedding switching costs, while industrial validation and workforce familiarity further reinforce uptake.

Application Insights

Manufacturing is anticipated to lead, accounting for approximately 42% share in 2026, underpinned by its entrenched role in high-volume assembly lines and automated production workflows. Adoption remains anchored by operational efficiency, precision in sealing and bonding, and integration with robotic dispensing systems, with enterprises prioritizing throughput consistency and standardized quality control across appliances, electronics, and industrial machinery production. Leading manufacturers such as Graco, Soudal, and ITW Dynatec provide high-spec guns tailored for form-in-place gaskets, vibration dampening, and thermal insulation, locking in enterprise workflows and sustaining professional adoption. This combination of mature infrastructure, repeatable process integration, and controlled operational environments ensures the dominance of manufacturing applications in industrial foam gun deployment.

The aerospace & defense segment is projected to be the fastest-growing segment, driven by emerging needs for lightweighting, fuel efficiency, and high-precision foam applications across commercial and military aircraft. Growth is being catalyzed by advanced high-R polyurethane and polyimide foams, automated dispensing systems, and portable high-viscosity guns, which materially improve operational speed, accuracy, and component performance. Accelerating adoption is supported by integration with specialized MRO workflows, stealth and ballistic foam applications, and cabin retrofit programs, lowering operational friction for first-time adopters. Leading brands such as Bostik, Würth, and Fischer are introducing new platforms optimized for aerospace compliance standards, while global defense modernization programs reinforce early-cycle demand.

Regional Insights

Asia Pacific Industrial Foam Guns Market Trends

Asia Pacific is expected to remain the leading regional market for industrial foam guns, accounting for approximately 38% of global revenue in 2026, supported by deep manufacturing penetration, large-scale infrastructure expansion, and a robust industrial ecosystem. The region’s dominance is underpinned by high-volume manufacturing in China, India, and Japan, where automation adoption, cost-efficient labor, and advanced production workflows drive sustained demand for precision foam dispensing. Integration of IoT-enabled and AI-driven “smart” guns, robotic automation in automotive assembly lines, and high-volume low-pressure (HVLP) systems reinforces operational efficiency and material optimization. Leading manufacturers such as Sheela Foam Ltd., Nitto Denko, Roughneck, Hilti, and Asahi Suna provide advanced metal-body, PTFE-coated, and high-pressure solutions, ensuring enterprise lock-in, consistent quality control, and alignment with regional technological evolution.

China anchors the Asia Pacific market, likely accounting for approximately 40% of regional demand, shaping the broader growth trajectory through concentrated industrial output and infrastructure investments. Regulatory frameworks, including GB/T energy efficiency standards and chemical compliance measures, channel procurement toward environmentally compliant, high-performance equipment. Vendor strategies in China increasingly focus on IoT-enabled monitoring, robotic dispensing integration, and ergonomic designs to reduce labor intensity, while FDI inflows accelerate technology transfer and production scale. This combination of industrial depth, regulatory alignment, and platform innovation positions China to sustain Asia Pacific’s leading market share.

North America Industrial Foam Guns Market Trends

North America is expected to register the fastest growth trajectory in the industrial foam gun market, supported by a dynamic construction and manufacturing ecosystem, regulatory incentives, and technology-driven adoption. The U.S. anchors demand through EPA energy codes, FAA F3 regulations, and federal programs such as ENERGY STAR and Safer Choice, which collectively encourage high-performance insulation and eco-friendly foam usage. The region’s growth is reinforced by automation adoption across industrial lines, robotic dispensing in aerospace and automotive applications, and integration of IoT-enabled guns for real-time monitoring and predictive maintenance. Leading vendors such as Graco, Hilti, Huntsman, Dow, and PMC provide advanced metal-body and PTFE-coated guns with touchscreen interfaces, closed-cell foam compatibility, and low-GWP system support.

The U.S. serves as the regional anchor, shaping North America’s momentum through construction, aerospace, and EV manufacturing. Boeing’s deployment of closed-cell foam guns for 737 composite lightweighting demonstrates a high-value industrial application, while regulatory mandates such as the AIM Act drive transitions to low-GWP HFO systems. Vendor strategies increasingly emphasize automation, smart IoT tools, and equipment retrofits to comply with energy efficiency and chemical standards. Combined with venture capital-backed innovation and infrastructure modernization, these factors position the U.S. to propel North America’s rapid growth, reinforcing its leadership in high-precision, sustainable, and technology-enabled foam dispensing solutions.

Europe Industrial Foam Guns Market Trends

Europe is expected to remain a mature and structurally stable market for industrial foam guns, supported by a well-established construction and manufacturing ecosystem, harmonized regulatory frameworks, and advanced technological adoption. The region’s stability is reinforced by compliance with the EU Green Deal and the Energy Performance of Buildings Directive, which drive large-scale retrofitting and high-performance insulation adoption. Industrial modernization, including digital integration and Industry 4.0 workflows, sustains demand for precision dispensing solutions in automotive and manufacturing sectors. Leading vendors such as Hilti, BASF, Covestro, Forvia, and Continental provide advanced metal-body, PTFE-coated, and sensor-enabled guns, ensuring consistent quality, predictive maintenance capabilities, and alignment with circularity and sustainability mandates.

Germany anchors the European market, shaping regional momentum through its leadership in automotive manufacturing, construction standards, and energy efficiency initiatives. Passivhaus projects and EV battery thermal management programs require precise foam gun applications to achieve airtightness and NVH optimization. Regulatory enforcement under REACH, F-Gas, and PPWR directives accelerates the adoption of low-GWP and recyclable foams, prompting vendors to deploy eco-friendly, high-performance dispensing technologies. Germany’s industrial hubs leverage digital and IoT-enabled guns for predictive maintenance, operational efficiency, and modular construction integration, sustaining consistent procurement while guiding regional technology standards and platform adoption across Europe’s mature industrial landscape.

Competitive Landscape

The global industrial foam guns market is moderately fragmented, with leadership concentrated among global suppliers such as Graco, Hilti, Huntsman, Dow, and PMC, reflecting a mix of high-performance product specialization and broad geographic reach. These leading players exert functional influence through precision-engineered dispensing systems, advanced metal and PTFE-coated designs, and IoT-enabled monitoring, shaping procurement decisions and operational standards across construction, manufacturing, and aerospace applications. Competitive positioning is defined by horizontal differentiation in application-specific solutions, vertical integration of proportioning and cartridge systems, and niche specialization in low-GWP or smart foam technologies. Industry behavior reflects ongoing consolidation through strategic M&A, platform evolution toward automation and predictive maintenance, and service-led models emphasizing lifecycle support and operator safety.

Key Industry Developments:

- In December 2025, BASF launched WALLTITE® RSB, a sustainable spray foam insulation system made from recycled and bio-based materials, boosting demand for industrial foam guns compatible with low-carbon resin formulations.

- In February 2025, Carlisle Companies Inc. acquired ThermaFoam, an expanded polystyrene manufacturer, advancing its "Vision 2030" strategy and expanding its presence in the South Central U.S.

- In May 2024, Huntsman International LLC introduced the Icynene Series spray polyurethane foam insulation, driving the need for advanced industrial foam guns for precise application and top-tier insulation performance.

Companies Covered in Industrial Foam Guns Market

- Graco Inc.

- 3M

- Hilti

- Dow Inc.

- BASF SE

- Covestro AG

- Huntsman

- Carlisle Fluid Technologies

- Fuji Spray

- Demilec Inc.

- Makita

- TriTech Industries

- Rhino Linings

- Premier Building Solutions

- J.H. Fletcher & Co.

- Zhejiang Chaoyu Tools

Frequently Asked Questions

The global industrial foam guns market is projected to be valued at US$69.3 billion in 2026 and is expected to reach US$98.3 billion by 2033, driven by demand in manufacturing, aerospace lightweighting, and energy-efficient insulation applications.

Automation enhances precision in sealing, bonding, and insulation processes across high-volume manufacturing lines, reducing material waste, improving operational efficiency, and supporting integration with robotic and IoT-enabled dispensing systems.

The industrial foam guns market is forecast to grow at a CAGR of 5.1% from 2026 to 2033, reflecting the adoption of smart dispensing systems, modular construction, and high-precision manufacturing applications.

Asia Pacific is the leading regional market, supported by deep manufacturing penetration, infrastructure expansion, high adoption of automation, and integration of smart foam guns in automotive, aerospace, and construction sectors.

The industrial foam guns market is moderately fragmented, with leading players including Graco Inc., Hilti, Huntsman, Dow Inc., BASF SE, Covestro AG, 3M, Carlisle Fluid Technologies, Fuji Spray, Demilec Inc., Makita, TriTech Industries, Rhino Linings Corporation, Premier Building Solutions, J.H. Fletcher & Co., and Zhejiang Chaoyu Tools. These companies compete through advanced dispensing technology, IoT integration, and application-specific solutions.