- Chipsets & Processors

- GaN RF Device Market

GaN RF Device Market Size, Share, and Growth Forecast, 2026-2033

GaN RF Device Market by Product Type (Discrete RF Components, Integrated RF Devices & Subsystems, Specialty RF Devices), End-Use (Telecom & Networking, Defense & Aerospace, Automotive & Mobility), Technology (GaN-on-Silicon Carbide (SiC), GaN-on-Silicon (Si), GaN-on-Diamond. Others), and Regional Analysis for 2026-2033

GaN RF Device Market Share and Trends Analysis

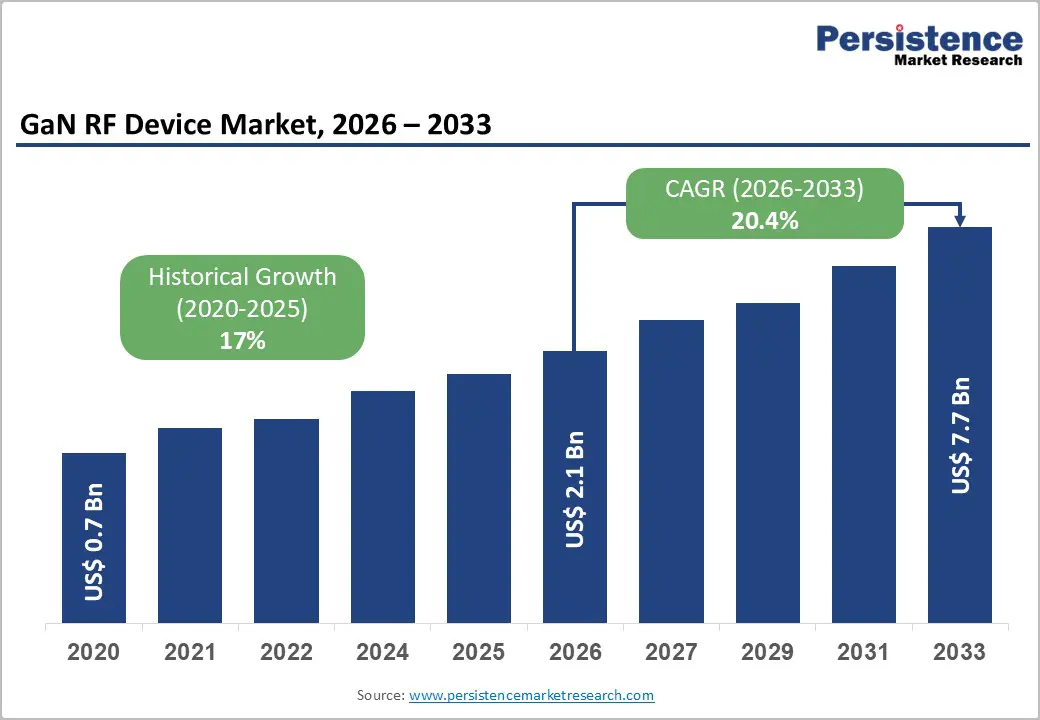

The global GaN RF device market size is likely to be valued at US$ 2.1 billion in 2026, and is projected to reach US$ 7.7 billion by 2033, growing at a CAGR of 20.4% during the forecast period 2026 – 2033.

Market growth is primarily driven by the rapid deployment of 5G infrastructure, which is increasing demand for high-performance radio frequency (RF) components across telecom networks. Simultaneously, heightened defense modernization programs and expanding automotive radar and mobility applications are requiring RF solutions with higher power, greater efficiency, and enhanced reliability. Innovations in wide bandgap semiconductor technologies, including gallium nitride (GaN) on silicon carbide (SiC) and GaN on Silicon platforms, are enabling significant performance improvements, such as higher power density, thermal efficiency, and frequency range. Strong regional commitments to advanced RF systems and increased capital expenditures by original equipment manufacturers (OEMs) are further accelerating adoption across telecom, aerospace, and automotive sectors.

Key Industry Highlights

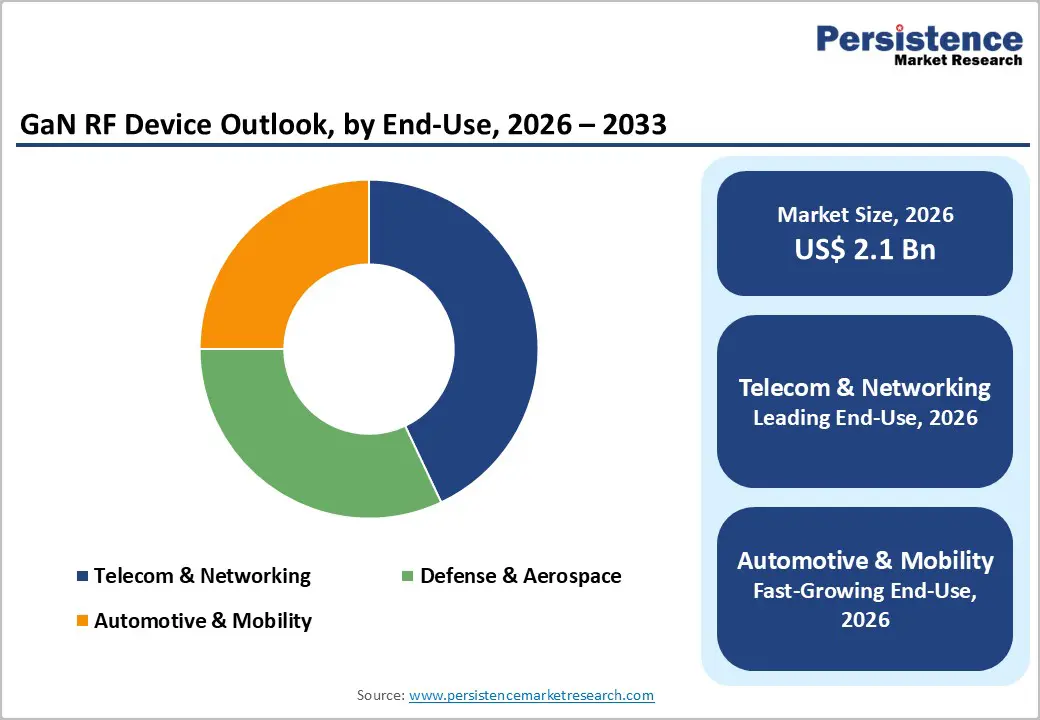

- Dominant End-Use: Telecom & networking is set to command around 43% of the revenue share in 2026, while automotive and mobility electronics are likely to grow the fastest at 22% CAGR through 2033, driven by 5G deployments and smart mobility adoption.

- Leading Device & Product Type: Discrete RF components are expected to lead with over 45% share in 2026, while integrated RF Devices are projected to be the fastest-growing device segment through 2033 due to lower manufacturing costs and expanding adoption.

- Technology Leadership: GaN on SiC is anticipated to dominate with an estimated 70% share in 2026, while GaN on Si is set to register the fastest growth at 12% CAGR through 2033, supported by efficiency and industrial scalability.

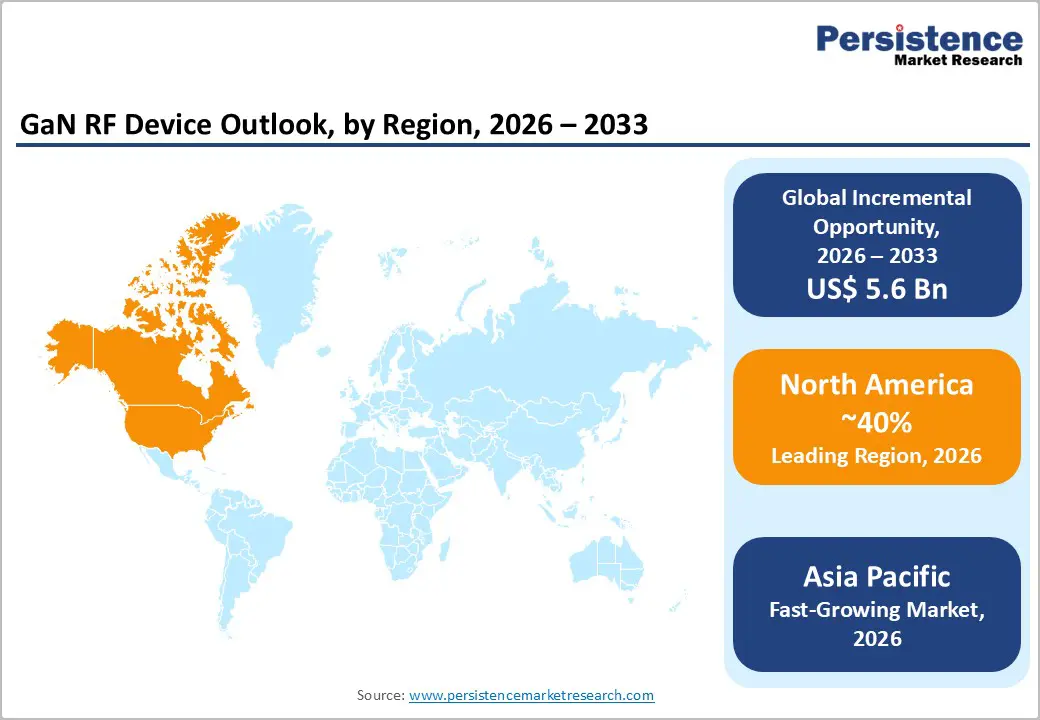

- Regional Leadership: North America is poised to dominate with an estimated 40% share in 2026 while Asia Pacific record the fastest growth through 2033, led by large-scale 5G rollout and investments in China, India, and Japan.

| Key Insights | Details |

|---|---|

|

GaN RF Device Market Size (2026E) |

US$ 2.1 Bn |

|

Market Value Forecast (2033F) |

US$ 7.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

20.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

17% |

Market Factors – Growth, Barriers, and Opportunity

Expansion of 5G and Advanced Wireless Networks

The rapid global rollout of 5G and next-generation wireless infrastructure continues to elevate demand for high-power RF devices designed for wide bandwidths and elevated frequency operation. Telecommunications authorities worldwide are auctioning new mid- and high-band spectrum, prompting network operators to accelerate base station deployments, small cell densification, and massive multiple-input and multiple-output (MIMO) expansion. In the United States, the Federal Communications Commission (FCC) expanded mid-band spectrum auctions in 2025 to support 5G growth and improve rural connectivity, reinforcing demand for advanced RF components.

In Asia, Japan’s Ministry of Internal Affairs and Communications announced accelerated mid- and millimeter-wave spectrum allocations in 2026 to support 5G-Advanced services and future 6G evolution, signaling strong government commitment to next-generation wireless infrastructure. South Korea and India have also fast-tracked spectrum policy reforms in 2025 to support private investment and network modernization. These policy actions are pushing telecom operators to invest in high-performance GaN solutions for network upgrades, sustaining structural demand and reinforcing telecom & networking as the dominant RF GaN application globally.

Defense, Aerospace, and Automotive Radar Modernization

Global defense modernization programs are expanding RF GaN demand as military systems upgrade radar, electronic warfare, and communication suites with higher performance requirements. The U.S. Department of Defense (DoD) announced in March 2025 increased funding for high-power GaN radar systems to support next-generation air and missile defense initiatives, reinforcing GaN adoption in mission-critical applications. NATO allies have similarly reaffirmed commitments to modernize air defense and communications capabilities in 2025–2026, strengthening demand for wide bandgap RF solutions.

At the same time, automotive regulatory and technology shifts are driving rapid adoption of advanced radar in mobility platforms. In 2025, the European Commission (EC) finalized new mandatory radar safety standards requiring enhanced object detection and collision avoidance systems in passenger vehicles by 2027, prompting automakers to accelerate deployment of high-frequency RF GaN radar modules. GaN’s performance advantages in thermal resilience and high-frequency signal integrity make it essential for autonomous driving and connected EV systems, aligning defense and mobility modernization with robust market growth across multiple high-value segments.

High Upfront Fabrication Costs and Material Complexities

The manufacturing complexity of gallium nitride RF devices on silicon carbide substrates continues to create significant cost barriers compared with alternative technologies. SiC substrates require intricate epitaxial growth, stringent quality control, and precision fabrication, contributing to elevated unit costs and extended lead times. These higher costs make it difficult for manufacturers to compete on cost-per-watt metrics in price-sensitive segments such as small cell telecom equipment and mid-tier automotive radar applications. Efforts to scale production to larger wafer formats are underway but have yet to fully eliminate price premiums due to yield and tooling challenges.

Recent industry developments have underscored cost pressures: several major semiconductor fabs reported significant increases in capital expenditures needed to support advanced node transitions, with complex tooling and precision fabrication requiring more layers, more mask steps, and higher energy input. Meanwhile, companies such as Wolfspeed are restructuring production to transition from 150 mm to 200 mm SiC wafer lines, a move expected to lower long-term unit costs but entail short-term underutilization costs and investment burdens. These dynamics amplify the cost experience in GaN RF device fabrication and underscore the financial hurdles that continue to constrain adoption beyond premium applications.

Supply Chain and Material Availability Risks

Global semiconductor supply chains remain fragile and highly exposed to geopolitical and corporate disruptions, posing material availability risks for GaN RF component manufacturing. Dependence on a limited number of substrate suppliers, concentrated equipment sources, and complex international logistics creates vulnerability when trade tensions escalate or corporate disputes disrupt production. Export controls, shifting regulatory policies, and regional supply mandates have increasingly fragmented supply chains, adding uncertainty to material flows and lead time reliability for advanced RF components.

Recent developments illustrate these risks at scale. In early 2026, China’s Ministry of Commerce warned of potential global chip shortages linked to the escalating dispute between Dutch chipmaker Nexperia and its Chinese subsidiary, which previously disrupted automotive and electronics production when export controls were imposed. Meanwhile, China has mandated that 50% of equipment for new chip capacity be domestically sourced, a policy that may bolster regional self-sufficiency but complicates global supply chain consistency as foreign tool access becomes more restricted. These events highlight structural supply disruptions that can constrain volume production ramps for GaN RF devices and deter investment in broader, price-sensitive markets.

Integration of mmWave and Next-Generation Wireless Technology

As wireless technologies evolve toward mmWave and early 6G standards, the demand for high-frequency, high-efficiency RF amplification and switching devices is expanding rapidly across next-generation network deployments. Governments and global telecom operators are exploring non-terrestrial networks (NTNs) and 6G testbeds to support ubiquitous broadband coverage, including satellite-terrestrial integration. In March 2025, collaborative industry demonstrations validated 5G NTN calls over low-Earth-orbit (LEO) channels, reaffirming technical feasibility for future 6G enhancements and broader RF requirements.

Telecom carriers are also planning space-based services to complement terrestrial 5G, such as Vodafone Idea’s satellite broadband initiative targeting a mid-2026 launch, signaling expanded service models that require advanced RF components. Emerging spectrum policies in Europe and Asia are allocating mmWave bands for 6G research, critical access, and urban infrastructure densification. These developments are creating a multi-billion-dollar opportunity for GaN RF solutions that enable high-frequency performance in both mmWave and early 6G ecosystems, especially where operators pursue ultra-low latency and enhanced throughput services.

Expansion in Aerospace, Satellite & Advanced Material Platforms

The proliferation of satellite constellation projects and advanced aerospace communications is creating significant new demand for GaN RF devices beyond traditional terrestrial networks. Government-backed initiatives such as the European Union’s IRIS² broadband satellite constellation, planned for deployment with hundreds of LEO and medium-Earth-orbit (MEO) satellites beginning in 2025, emphasize secure global connectivity and extended coverage requiring high-performance RF hardware.

Satellite operators are also forging strategic partnerships to accelerate service delivery, such as SES’s 2025 agreement with Impulse Space to expedite LEO satellite deployment, reducing transit time into operational orbits and expanding service capacity. These constellation efforts, combined with growing integration between 5G networks and satellite connectivity, are fueling demand for high-power, high-efficiency GaN amplifiers and front-end modules. As broadband, defense communication, and earth observation programs expand, this opportunity is strengthening GaN’s role in high-reliability aerospace and satellite ecosystems, offering a differentiated revenue stream beyond traditional telecom channels.

Category-wise Analysis

Product Type Insights

Discrete RF components are expected to remain the leading product type in 2026, capturing approximately 45% of the GaN RF device market revenue share, due to their extensive use in high-power transistors and HEMTs for telecom base stations and defense systems. Their modular design simplifies integration, maintenance, and system upgrades while ensuring robust performance under sustained high-power operation.

A notable 2025 development reinforcing this leadership was Mitsubishi Electric’s verification of a compact 7 GHz GaN power amplifier module (PAM) for 5G-Advanced base stations, demonstrating superior power efficiency and compact form factor for large-scale wireless deployments. This underscores discrete GaN’s critical role in enabling next-generation network and mission-critical systems.

Integrated RF devices & subsystems are slated to be the fastest-growing segment, expanding at an estimated 2026-2033 CAGR of 21%, backed by a huge demand for multifunction, compact modules that consolidate amplification, switching, and filtering functions from original equipment manufacturers (OEMs). These solutions reduce board footprint, improve calibration efficiency, and accelerate deployment across telecom and aerospace systems.

A key 2025–2026 example is Spain’s GIGaNTE project, led by Indra, which advanced GaN-based integrated circuits for radar and communications, supporting compact subsystem production and national semiconductor autonomy. Specialty RF devices in aerospace and satellite communications also benefit from this growth, enabling high-frequency, high-reliability applications in niche, premium markets.

End-Use Insights

Telecom & networking are likely to account for roughly 43% of the GaN RF device market share in 2026. GaN technology’s high power handling and efficiency make it ideal for 5G base stations, massive MIMO radios, and evolving 5G-Advanced infrastructures where performance and reliability are critical. In 2025, Mitsubishi Electric publicly verified a GaN power amplifier module optimized for 5G-Advanced base stations, confirming GaN’s role in powering next-generation wireless infrastructure with improved energy efficiency and compact form-factor integration. This real-world deployment highlights how telecom operators are integrating GaN RF solutions to meet rising bandwidth and network capacity requirements.

Automotive & mobility stands out as the fastest-growing application, with a 22% CAGR supported by the expanding use of advanced radar, lidar, and communications modules in vehicles. GaN’s ability to operate efficiently at high frequencies, critical for 77–79 GHz automotive radar bands, has accelerated interest from major OEMs and Tier-1 suppliers pursuing safer, high-resolution sensing systems. Meanwhile, the Defense & Aerospace segment continues steady expansion, illustrated by Europe’s GIGaNTE initiative in 2025, which advanced GaN circuit design for radar and secure communications, reflecting defense priorities for rugged, high-performance RF technologies across applications.

Regional Insights

North America GaN RF Device Market Trends

North America is expected to dominate with an approximate 40% of the GaN RF device market value in 2026, owing to substantial defense spending and early telecom migration in the region. The U.S. Department of Defense’s large allocations toward radar modernization and electronic warfare systems continue to stimulate GaN RF integration into mission-critical platforms, supporting sustained demand for high-power, wide-bandgap solutions. In 2026, major capacity expansions, such as Wolfspeed’s significant fabrication facility investments in North Carolina, underscore strategic scaling to meet defense and telecom requirements

Recent moves by major chip manufacturers to increase production capacity and R&D funding for advanced semiconductors, including GaN-focused research allocations, highlight the region’s strategic focus on supply chain resilience. For instance, GlobalFoundries boosted its overall chip investment plan in 2025, dedicating part of a substantial US$ 16 billion investment toward emerging semiconductor technologies that include gallium nitride for high-efficiency power and RF applications. These developments reinforce North America’s leadership in high-performance RF markets while expanding manufacturing infrastructure for next-generation communication systems.

Europe GaN RF Device Market Trends

The Europe GaN RF device market is anchored by coordinated defense, aerospace, and telecom investments across Germany, the U.K., France, and Southern European nations. National programs emphasize semiconductor autonomy and strategic value chains, with collaborative industry initiatives supporting GaN technology development for high-reliability radar and communication modules. In March 2026, Spain’s launch of a multi-year project to build autonomous GaN manufacturing capability underscores this trend toward European self-sufficiency in advanced RF technologies.

Although growth is more measured than in Asia Pacific, Europe’s regulatory harmonization, through defense funding mechanisms and cross-border R&D collaboration, supports steady adoption of GaN devices in premium applications. The region’s focus on compact, integrated RF modules for defense and secure communications continues to attract investment, bolstered by programs that strengthen semiconductor manufacturing and packaging ecosystems. These dynamics position Europe as a stable and innovation-focused market for GaN RF solutions with enduring strategic relevance.

Asia Pacific GaN RF Device Market Trends

Asia Pacific is poised to emerge as the fastest-growing market for GaN RF devices through 2033, driven by rapid 5G infrastructure expansion, semiconductor capacity growth, and strategic national investments in advanced electronics across China, India, Japan, and ASEAN markets. The region’s share is growing rapidly as carriers deploy GaN-based components in high-frequency base stations and automotive radar systems. In India, recent breakthroughs in indigenous GaN chip design by national laboratories illustrate deepening local capabilities in RF technology and defense electronics, reducing reliance on imports and building competitive advantage in strategic sectors.

China’s dominant position in global gallium supply chains underscores Asia Pacific’s pivotal role in supporting the manufacturing and deployment of GaN components worldwide, even as geopolitical policies fluctuate. A Reuters report noted temporary licensing relief on critical mineral exports, such as gallium, between China and Western partners in late 2025, easing short-term supply constraints in semiconductor ecosystems while highlighting the importance of regional supply resilience.

With aggressive infrastructure build-outs, government incentives, and cross-border partnerships boosting RF semiconductor output, Asia Pacific stands out as the fastest-expanding regional market with long-term volume growth potential.

Competitive Landscape

The global GaN RF device market structure is moderately consolidated, with a cohort of leading semiconductor companies commanding a significant portion of market revenue through broad product portfolios and strategic investments in wide-bandgap technology development. Key players such as Wolfspeed, Qorvo, MACOM, Sumitomo Electric, and Ampleon hold substantial market share due to their strength in GaN-on-SiC and GaN-on-Si manufacturing, aerospace and defense system integrations, and high-efficiency RF components for telecom infrastructure upgrades. These established vendors leverage deep engineering expertise and end-market relationships to maintain robust positions in high-power RF devices, particularly for 5G base stations, satellite links, and radar applications.

Market competition is shaped by vertical integration strategies, capacity investments, and wafer-scale technology roadmaps that aim to improve thermal performance, power density, and cost-effectiveness. Strategic partnerships and capacity expansions, both in GaN epitaxy and advanced packaging, are common as companies align to capture next-generation RF demand. Regional specialization also plays a role, with domestic players in Asia building localized supply chains to mitigate export control pressures.

While incumbent vendors maintain share through scale and breadth of offerings, emerging specialists and fabless innovators are gaining traction via design optimization and targeted segment focus, driving overall competitive intensity.

Key Industry Developments

- In February 2026, ROHM licensed TSMC’s 650V GaN process to its Hamamatsu facility, aiming for full in-house production by 2027, targeting AI servers and EV power systems while securing supply chains and strengthening its EcoGaN™ product line.

- In December 2025, Onsemi partnered with Innoscience and GlobalFoundries to scale GaN production and introduced Vertical GaN-on-GaN technology, supported by a US$ 6 billion share repurchase program to reinforce investor confidence and growth in AI and EV markets.

Companies Covered in GaN RF Device Market

- Wolfspeed, Inc.

- Qorvo, Inc.

- GaN Systems

- MACOM Technology Solutions

- Infineon Technologies AG

- Sumitomo Electric Device Innovations

- ROHM Semiconductor

- Navitas Semiconductor

- STMicroelectronics

- Aethercomm

- Hitachi, Ltd.

- Renesas Electronics

- NXP Semiconductors

- Bosch Semiconductor Solutions

- Mitsubishi Electric

Frequently Asked Questions

The global GaN RF device market is projected at US$ 2.1 billion in 2026.

Widening 5G deployment, defense modernization, and automotive radar adoption are driving market growth.

The market is poised to witness a CAGR of 20.4% from 2026 to 2033.

Opportunities exist in 5G infrastructure expansion, aerospace communication systems, and autonomous vehicle radar adoption.

Wolfspeed, Qorvo, MACOM, Sumitomo Electric, and Ampleon are some of the key players in the market.