- Chemicals and Materials

- Foot Orthopedic Insoles Market

Foot Orthopedic Insoles Market Size, Share, and Growth Forecast, 2026 - 2033

Foot Orthopedic Insoles Market by Product Type (Customized, Prefabricated), Material (Ethyl-Vinyl Acetate (EVA), Thermoplastics, Composite Carbon Fibers, Foams, Others), Application (Medical, Sports & Athletics, Personal Comfort, Others), and Regional Analysis for 2026-2033

Foot Orthopedic Insoles Market Share and Trends Analysis

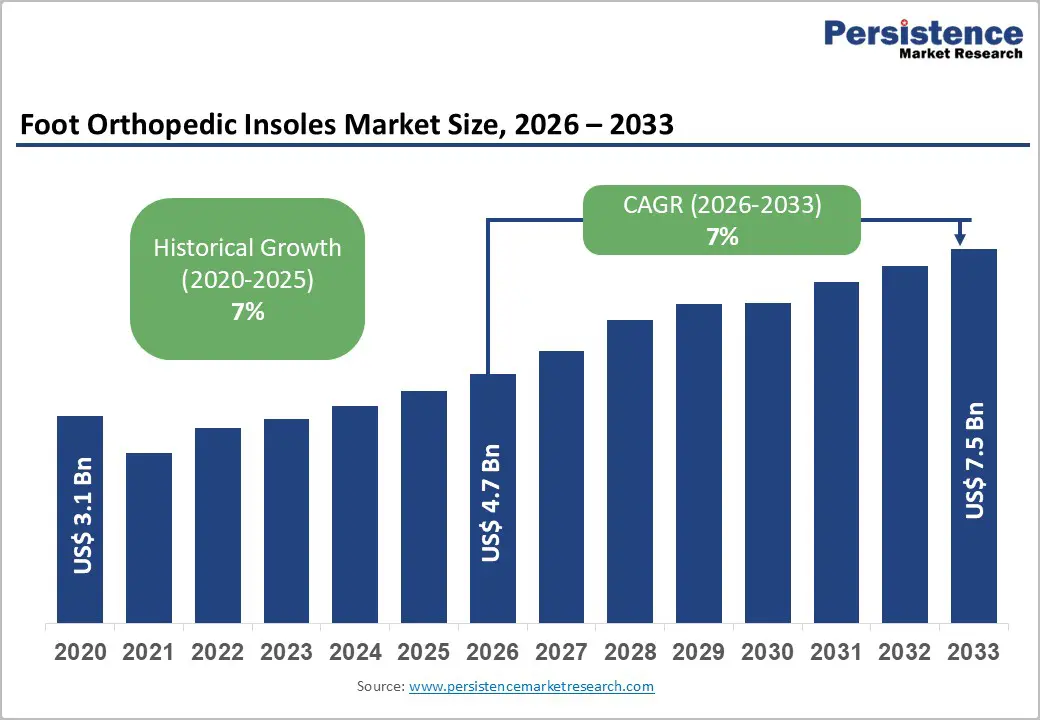

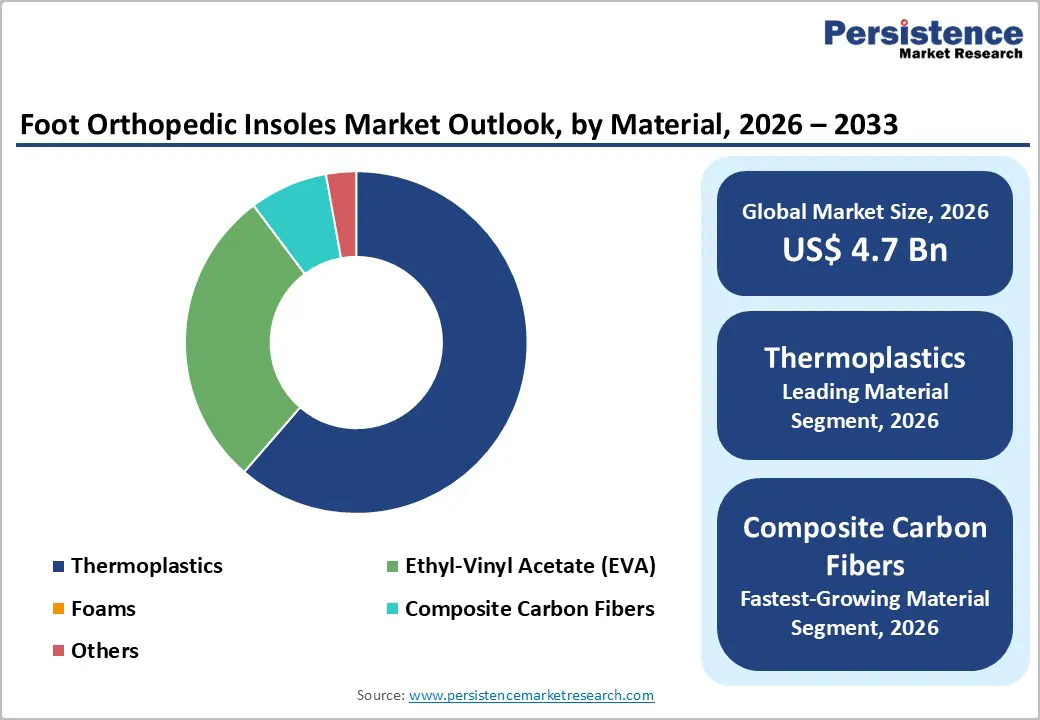

The global foot orthopedic insoles market size is likely to be valued at US$ 4.7 billion in 2026, and is estimated to reach US$ 7.5 billion by 2033, growing at a CAGR of 7% during the forecast period 2026−2033.

The market is being propelled by converging demographic trends, including rapid aging of global populations and rising prevalence of metabolic diseases, particularly diabetes, affecting over 530 million adults worldwide, according to the International Diabetes Federation (IDF). Technological advancements in additive manufacturing, 3D foot scanning, and biomechanical pressure mapping is reducing production timelines for custom insoles from weeks to days, addressing a structural healthcare gap in preventive foot care.

Healthcare systems across developed economies are increasingly recognizing the cost-benefit proposition of clinical-grade orthotics, which reduce emergency room visits for foot-related complications in diabetic populations. Together, these macroeconomic, technological, and clinical factors is creating a sustained demand for orthopedic insoles across clinical and medical environments managing chronic foot disorders, performance-focused consumers seeking competitive advantage, and mass-market consumers addressing daily comfort needs through retail channels.

Key Industry Highlights

- Dominant Product Type: Customized insoles are likely to capture an estimated 51.8% of the market revenue share in 2026, as 3D scanning adoption accelerates.

- Material Leadership: Insoles made from composite carbon fibers are likely to exhibit the highest CAGR of 9.3% through 2033 owing to the expansion of athletic footwear with professional sports franchise adoption.

- Dominant Region: North America is poised to lead with approximately 40.6% market share in 2026, supported by broader Medicare coverage and the integration of 3D scanning technology.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing regional market, expected to register a 2026-2033 CAGR of 9.4%, on account of increasing diabetes prevalence in India and China.

- Competitive Trends: Strategic M&A acceleration by large conglomerates is aimed at establishing precedent for consolidating specialized products and diversifying portfolios.

- August 2025: Orpyx Medical Technologies launched a sensory insole program to prevent diabetic foot complications by tracking plantar pressure, temperature, steps, and wear time, syncing to a mobile app and cloud platform.

| Key Insights | Details |

|---|---|

| Foot Orthopedic Insoles Market Size (2026E) | US$ 4.7 Bn |

| Market Value Forecast (2033F) | US$ 7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Digital Manufacturing and Customization Accelerating Clinical Adoption

Additive manufacturing is transforming the production and distribution of orthopedic insoles by enabling faster, more precise customization. Advanced scanners now capture biometric data in real-time, allowing software algorithms to generate patient-specific arch contours, pressure-redistribution zones, and material density maps within minutes. This approach has proven particularly effective for diabetic foot management, as clinical studies show that AI-optimized pressure mapping reduces peak plantar pressure by 18–22% compared to traditional manual molding.

Leading orthopedic institutions have reported that scan-to-production pipelines have reduced fabrication time significantly, enabling same-week delivery and improving patient compliance. Digital workflow automation has also lowered per-unit labor costs sizably, making mid-tier manufacturers more competitive against established brands.

European manufacturers, especially those in the Netherlands, are pioneering the use of flexible carbon-fiber matrices that combine 3D computer-aided design (CAD) optimization with aerospace-grade materials. Clinical data from sports podiatry centers demonstrate that carbon-optimized insoles increase standing long-jump distance by 1.6 inches and elevate output among athletic users.

The sector has attracted significant investment, with venture capital funding for digital orthotic platforms reaching. This technological shift is drawing new entrants, such as Stride Soles, which was founded in 2024 by German podiatrists and technologists. The company has showcased rapid market-readiness for remote-first orthotic delivery models.

Supply Chain Constraints and Material Cost Volatility Impacting Market Growth

The orthopedic insole industry has been experiencing structural instability due to fluctuating polymer outlays and sourcing risks. Ethylene vinyl acetate (EVA), which is a core material for making insoles, has derived its feedstock from petroleum-based intermediates that remain sensitive to crude oil volatility. Resin pricing for this substance has surged since early 2024, creating significant fiscal pressure for firms that have relied on legacy formulations. Although producers have been transitioning toward carbon-negative alternatives, such as bio-EVA, this eco-friendly option carries a hefty premium.

Thermoplastics have represented bulk of recent market earnings, but virgin synthetics such as polypropylene (PP) and polyetheretherketone (PEEK) have sustained notable inflation. High-margin solutions including carbon-fiber composites have also encountered competition from the aerospace and automotive sectors. Furthermore, inventory concentration threats have intensified as specialized foams comprising Poron or Sorbothane have depended on lone-origin providers. These compounding expenditures have triggered a sizeable margin shrinkage, which has forced several regional companies in Asia Pacific to reconsider their operational strategies. Price-sensitive segments are likely to face restricted expansion, as manufacturers will not be able to pass these elevated costs onto consumers without losing volume.

Integration of Smart Insoles with Wearable Health Devices

Orthopedic insoles have been converging with wearable health technology and digital biometric ecosystems, creating a value-added opportunity that differs from traditional positioning. Integrated pressure sensors, inertial measurement units (IMUs), and real-time data transmission to smartphone applications have enabled continuous gait analysis, biomechanical feedback, and personalized coaching. This convergence has transformed static insoles into dynamic platforms for injury prevention and performance optimization.

For example, Striv's sensor-embedded insoles transmit real-time data via Bluetooth, providing athletes with metrics such as cadence, ground contact time, pressure distribution, and movement symmetry. The platform's machine learning engine generates personalized coaching recommendations to reduce the risk of anterior cruciate ligament (ACL) re-injury.

This capability has extended beyond athletic applications into clinical settings. Continuous gait monitoring has enabled early detection of progression in conditions such as Charcot foot or emerging neuropathy, triggering intervention before complications develop. Integration with broader wearable ecosystems, including Apple Watch, Garmin, and Oura Ring, has enabled data-rich user experiences that foster sustained engagement and generate recurring monetization opportunities.

However, realizing this opportunity will require infrastructure investment in secure data architectures, regulatory compliance for medical-grade sensors, clinical evidence generation, and ecosystem partnerships with health platforms. These requirements can concentrate market share among well-capitalized players and technology-enabled startups backed by venture capital, making the opportunity geographically and demographically concentrated within tech-forward, affluent-consumer segments in North America and Western Europe.

Category-wise Analysis

Product Type Insights

Prefabricated insoles are predicted to command around 48.2% of the market revenue share in 2026. Cost accessibility ranges from US$ 25–US$ 95 per pair versus US$ 200–US$ 600 for customized alternatives. Their immediate availability is ensured through retail and e-commerce channels, with established brands serving mass-market segments effectively. For instance, Dr. Scholl's has secured the largest retail footprint with distribution through over 75,000 pharmacy and supermarket locations worldwide, enabling impulse purchases.

Similarly, Superfeet's performance line has captured significant athletic retail share through point-of-sale demonstrations and athlete endorsements. Product differentiation remains moderate across applications such as dress insoles, athletic performance, diabetic-specific solutions, and daily comfort. However, the growth of this segment is expected to decelerate, as consumers are increasingly perceiving prefabricated insoles to have limited clinical benefits compared to their customized counterparts.

Customized insoles are set to chart the highest growth trajectory at roughly 9.8% CAGR from 2026 to 2033. This segment is likely to capture 51.8% of market revenues in 2026, signaling a structural shift toward personalized healthcare. Digital manufacturing has reduced production costs of customized insoles by a considerable margin since 2020. Clinical evidence has demonstrated superior outcomes of these products for diabetic neuropathy, chronic plantar fasciitis, and post-surgical rehabilitation.

Three-dimensional (3D) foot scanning adoption has rapidly expanded, with leading manufacturers having scaled digital capacity aggressively. Bauerfeind, for instance, has established cloud-based computer-aided design (CAD) platforms for remote clinician access, while direct-to-consumer (DTC) platforms such as Stride Soles have widened their consumer base through remote scanning and algorithmic optimization.

Material Insights

Thermoplastics are poised to command an estimated 54.1% of the foot orthopaedic insoles market revenue share in 2026. Superior processability, durability, and established supply chains have sustained this dominance. Materials such as PE, PEEK, and polyurethane (PU) formulations have delivered competitive advantages. Excellent thermoformability has enabled precise custom molding to individual foot contours, while compression resistance has exceeded foam alternatives.

Established manufacturing workflows have required minimal process re-engineering, with orthopedic clinics extensively utilizing semi-rigid and rigid thermoplastic shells for custom orthotics. Key suppliers including Lorica, Superflex, and Hapco have secured leading positions through proprietary formulations that optimize flexibility, durability, and cost. Thermoplastics have also excelled in diabetic foot care and pediatric applications requiring structural support.

Composite carbon-fiber materials are expected to register the fastest growth during the 2026–2033 forecast period, owing to performance positioning in athletic segments and emerging clinical applications. Premium pricing, improved energy return, vertical jump gains, and running enhancement are the key features driving the adoption of foot orthopaedic insoles made from composite carbon fibers. Professional basketball and soccer franchises have anchored demand, creating consumer pull-through among recreational athletes.

Material innovation has further accelerated with flexible carbon-fiber fabrics enabling mid-foot hinge behavior. Manufacturers such as SOLE and Superfeet performance lines have integrated carbon-fiber components into their premium custom offerings. Even though supply constraints have limited faster scaling due to specialized equipment and skilled labor requirements, capital deployment has accelerated in these materials.

Application Insights

Medical applications are expected to account for around 58.4% of revenue share in 2026, driven by strong clinical demand from patients with foot disorders, chronic diseases, and post-surgical rehabilitation for conditions such as plantar fasciitis, diabetic foot complications, flat feet, and pes planus. Clinician-prescribed purchasing behavior characterizes this category, with reimbursement eligibility sustaining demand volume. High clinical-evidence requirements differentiate medical applications from consumer segments, with patients with diabetes leading the way.

Management of diabetic neuropathy and plantar ulceration has driven orthotic prescription volume to exceed medical segment volume in developed markets. Orthopedic surgeons and podiatrists have increasingly positioned custom orthotics as foundational elements of conservative treatment pathways before surgical intervention. Healthcare economic data have demonstrated orthotic effectiveness in reducing emergency department visits for diabetic foot complications.

Sports and athletics applications are slated to post the highest CAGR between 2026 and 2033, backed by performance positioning, consumer lifestyle aspiration, and integration with fitness ecosystems. Mass-market fitness and recreational activities have accelerated the growth of this segment. Professional sports franchises have outfitted rosters with custom performance orthotics.

Collegiate athletic training programs are also increasingly prescribing athlete-specific insoles for injury prevention, creating demand-pull dynamics for this segment. While recreational athletes have sought to replicate elite configurations, the integration of wearable technology has accelerated the growth of this segment. For example, smart insoles with embedded pressure sensors and gait analytics have generated recurrent sales avenues.

Regional Insights

North America Foot Orthopedic Insoles Market Trends

North America is anticipated to dominate in 2026, holding around 40.6% of the foot orthopaedic insoles market share on the back of a mature podiatric infrastructure supports widespread clinical delivery. Medicare and private insurance have established reliable reimbursement pathways, strongly aided by consumers demonstrating improving awareness of preventive foot care. The United States generates the majority of regional revenue, followed by Canada and Mexico.

Key states such as California, Florida, Texas, and New York lead the market in terms of volume due to population density, higher incomes, and health-conscious demographics. The regional market has shown resilience during economic disruptions, including the pandemic period. Average selling prices here have remained the highest globally for both custom and prefabricated solutions, reflecting consumer willingness to invest in quality and reimbursement support.

North American manufacturers lead in digital infrastructure adoption. Podiatric clinics are integrating 3D foot scanning and AI-enabled biomechanical analysis into routine practice. For example, the Aetrex Albert 2 Pro platform standardizes biometric capture across specialty clinics. Medicare has continued to expand coverage for diabetic orthotics and age-related foot conditions. Private insurers have standardized custom orthotic reimbursement with defined patient cost-sharing.

Changing demographics in the region have amplified demand, as aging populations grow alongside rising diabetes and obesity prevalence. The U.S. Food and Drug Administration (FDA) classifies insoles as Class I or Class II devices, enabling streamlined market entry for innovative manufacturers. Competition is consolidating around clinical specialists, retail brands, and emerging D2C platforms.

Europe Foot Orthopedic Insoles Market Trends

Europe is likely to be the second-largest regional market for foot orthopaedic insoles owing to robust healthcare standards and advanced regulatory frameworks. The region demonstrates leadership in sustainability and environmental innovation, with manufacturers pioneering bio-based and recycled materials such as bio-EVA and recycled thermoplastics. The European Union (EU) Circular Economy Action Plan and Extended Producer Responsibility directives have created competitive advantages for producers committed to sustainable supply chains.

Leading Dutch manufacturers have reported increased average selling prices following bio-EVA adoption, while enabling retailers to meet environmental, social, & governance (ESG) reporting requirements. The expansion of the National Health Service (NHS) and tightening of diabetic foot care commissioning standards have incentivized podiatric practices to prescribe custom orthotics, expanding clinical volume. Universal health insurance systems in Germany and the Nordic countries have increased reimbursement for orthotic devices, stabilizing regional demand.

In Europe, orthopedic insoles are classified as Conformité Européenne [CE]-marked medical devices, requiring compliance with EU Medical Device Regulation 2017/745. This regulatory environment demands rigorous clinical evidence and post-market surveillance, elevating market entry barriers and compliance costs. Established manufacturers such as Bauerfeind AG, Sidas, and Foot Science International maintain strong clinical relationships and NHS partnerships, controlling a significant share of the market.

North American and Asian competitors are increasing penetration through strategic partnerships and localized manufacturing. With investment capital targeting sustainable materials innovation and clinical evidence generation, European venture capital is shifting toward deep-tech applications, including advanced polymer formulations, flexible carbon-fiber manufacturing automation, and digital biomechanics analysis platforms.

Asia Pacific Foot Orthopedic Insoles Market Trends

Asia Pacific is poised to emerge as the fastest-growing regional market for foot orthopedic insoles, forecasted to register a 2026-2033 CAGR of 9.4%, on account of large patient pools and rising health awareness. Aging populations have skyrocketed the need for daily health support solutions, while chronic disease management has been pushing more patients into preventive foot care pathways.

Mature markets such as Japan have sustained steady replacement demand through clinical and specialty retail networks, while developing markets such as India and Indonesia have been expanding the addressable base as consumers have shifted from basic comfort purchases to condition-led solutions. Diabetes prevalence and the risk of diabetic foot ulcers have been reinforcing this shift, and multinational suppliers have been adapting their portfolios toward medically credible products that still fit local price expectations.

Regional market growth is accelerating in tandem with the improvements witnessed in digital distribution and public health capacity. D2C models have been scaling through smartphone-led assessment and telehealth fulfillment, which has been reducing reliance on limited specialist density in many cities and secondary regions. Governments have also been modernizing health systems and piloting stronger chronic-care programs, which will expand reimbursement pathways for selected orthotic use cases in several countries.

Regulatory environments have remained fragmented across the region, allowing companies to benefit from building country-specific compliance roadmaps and flexible manufacturing footprints that can efficiently serve multiple approval regimes. Competitive intensity has been increasing across price tiers, with domestic brands defending value segments and international players focusing on premium performance and clinically positioned offerings.

Competitive Landscape

The global foot orthopedic insoles market structure has remained moderately fragmented, with a large mix of multinational brands, regional manufacturers, and digital-first entrants competing across channels. No single supplier has dominated, which has resulted in companies strengthening their foothold through sharper positioning and stronger execution of market-entry strategies. Established clinical manufacturers have been protecting their share by tightening clinical relationships, improving evidence generation, and strengthening workflow integration in podiatry and orthopedic practices.

Mass-market retail brands have been defending distribution reach and brand familiarity, but they have been facing slower growth as consumers have been shifting toward personalized options and direct purchasing. Telehealth platforms and D2C models have been expanding quickly because they have been controlling the customer relationship and using data-led onboarding to drive conversion and retention.

Clinical specialists such as Aetrex Worldwide, Inc., Bauerfeind AG, and Sidas SAS have been differentiating through proprietary assessment systems and outcome tracking, but they have been needing to keep building digital pathways that will have reduced friction for patients and clinicians over time. Retail-led players such as Dr. Scholl’s have been strengthening product tiering and merchandising, while they have been building D2C capabilities to protect margins and capture first-party demand signals.

Digital challengers such as Stride Soles have been using remote assessment and direct shipping to widen access, and this approach has been pressuring incumbents to improve speed, transparency, and service design. Materials and component leaders have been expanding influence through sustainability and supply-chain integration, reinforcing the strategic value of premium insole materials in footwear and orthotics ecosystems.

Key Industry Developments

- In August 2025, PioCreat introduced a 3D printing system that enables clinics to produce custom orthotic insoles in 35 minutes. The IPX2 printer and FS A002 scanner integrate scanning, gait analysis, and multi-material printing for faster, precise production.

- In August 2025, Superfeet unveiled the Sport Ultralight insole, engineered 25% lighter than traditional models with SuperRev™ supercritical foam and EVOLyte™ carbon-fiber cap. The ultralow-profile design fits tight footwear such as soccer cleats and gym trainers, delivering responsive energy return and stability for athletes.

- In July 2025, Sengkang General Hospital (SKH) in Singapore piloted in-house 3D-printed custom insoles for diabetic foot care, reducing delivery time from two months to one week. Collaboration with Singapore General Hospital's 3D printing center has improved pressure distribution by 52.7% and peak pressure reduction by 28.5%.

Companies Covered in Foot Orthopedic Insoles Market

- Dr. Scholl's Wellness Co.

- Bauerfeind AG

- Superfeet Worldwide, Inc.

- Aetrex Worldwide, Inc.

- Otto Bock SE & Co. KGaA

- Sidas SAS

- Foot Levelers, Inc.

- Spenco Medical Corporation

- Powerstep

- SOLE Laboratories, Inc.

- Birkenstock

- Implus Corporation Vionic Group

- Asics Corporation

- Profoot, Inc.