- Food Packaging

- Food Oil Absorbing Sheet Market

Food Oil Absorbing Sheet Market Size, Share, and Growth Forecast, 2026 - 2033

Food Oil Absorbing Sheet Market by Material Type (Reed Oil Absorbing Paper, Cellulose-Based, Others), Product Type (Square, Round, Others), Distribution Channel, Application, and Regional Analysis for 2026 - 2033

Food Oil Absorbing Sheet Market Size and Trends Analysis

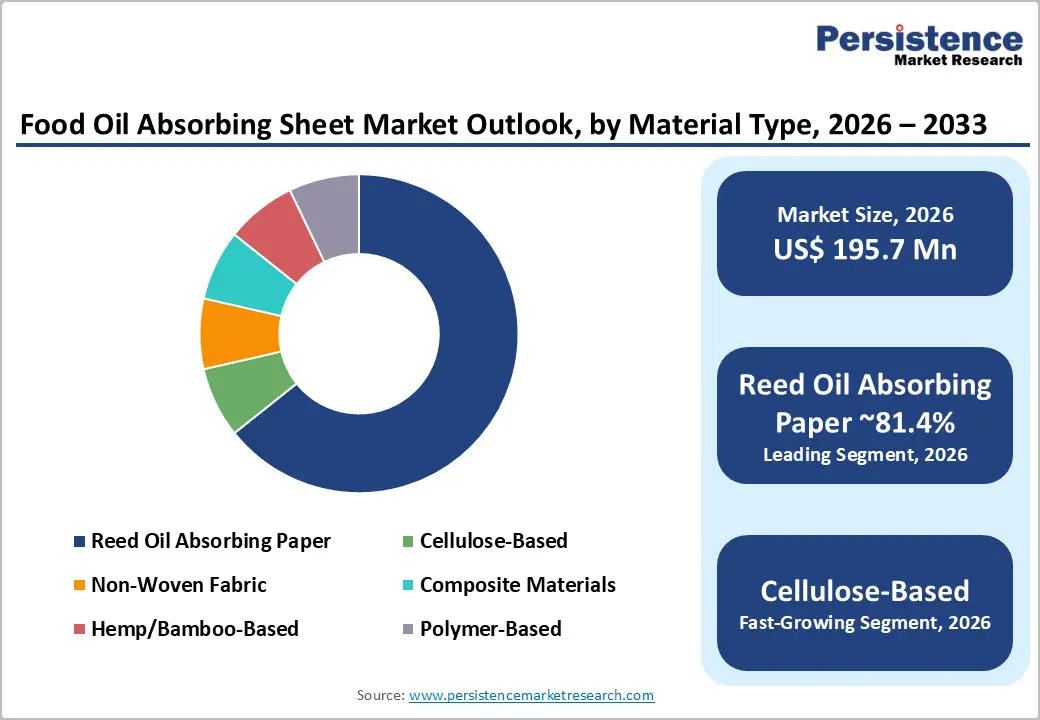

The global food oil absorbing sheet market size is likely to be valued at US$ 195.7 million in 2026 and is expected to reach US$261.0 million by 2033, growing at a CAGR of 4.2% between 2026 and 2033, driven by increasing consumer health awareness, expansion of quick-service restaurant chains, and growing processed food production.

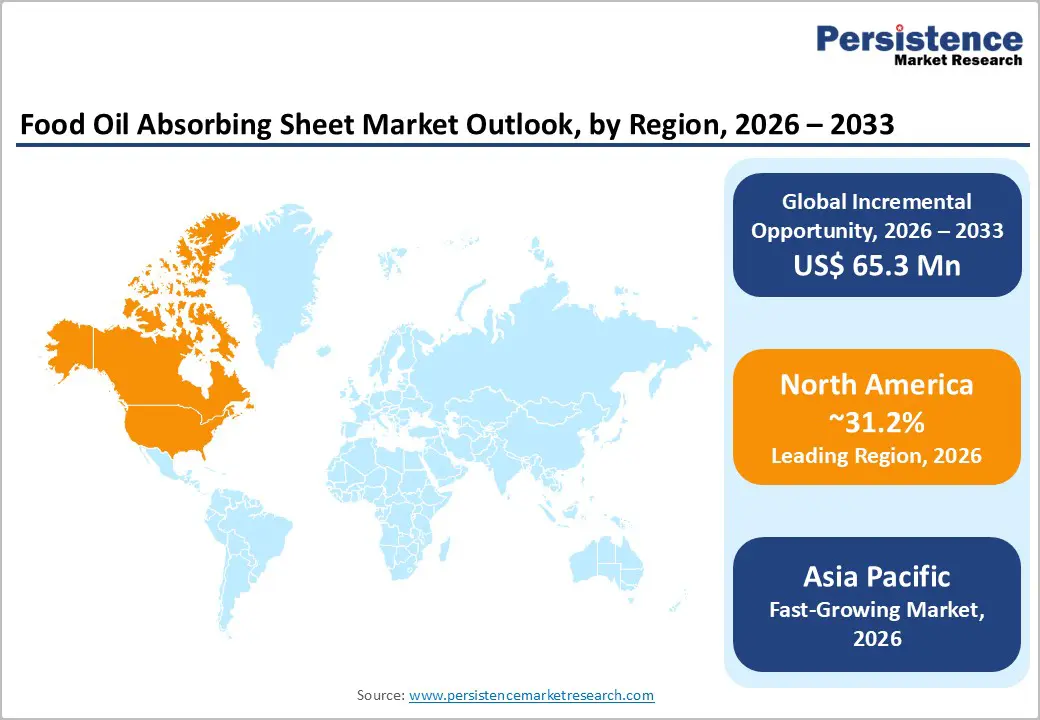

North America accounts for approximately 31.2% of the global market share, while Asia Pacific represents the fastest-growing regional market. Commodity price trends in pulp and vegetable oils continue to influence cost structures and procurement strategies.

Key Industry Highlights:

- Leading Region: North America is projected to lead with approximately 31.2% share, supported by high quick-service restaurant density, strong supermarket penetration, and established food-contact compliance standards.

- Fastest-Growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid urbanization, QSR expansion, and rising disposable incomes across China, India, Japan, and ASEAN markets, contributing the highest projected CAGR through 2033.

- Investment Plans: Manufacturers are investing in automated converting lines, high-GSM creping technologies, and biodegradable cellulose R&D, while retailers expand compostable SKUs to meet sustainability targets. Capacity expansion in Asia and private-label scale manufacturing in North America remain strategic priorities.

- Dominant Material Type: Reed oil-absorbing paper is projected to account for 81.4% of the market in 2026, reflecting established procurement standards, cost efficiency, and widespread use across household and commercial applications.

- Leading Product Type: Square sheets are projected to account for 52.3% of the market in 2026, driven by standardized sizing, retail-friendly packaging formats, and strong supermarket distribution.

| Key Insights | Details |

|---|---|

| Food Oil Absorbing Sheet Market Size (2026E) | US$195.7 Mn |

| Market Value Forecast (2033F) | US$261.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Health and Hygiene Awareness Driving Product Adoption

Growing consumer awareness regarding dietary fat intake and food presentation standards is increasing demand for oil-management solutions. Households and foodservice operators are actively reducing visible oil residue in fried and packaged foods to align with wellness trends. Global edible oil production remains substantial, sustaining high levels of frying and oil-based food preparation worldwide. This structural consumption pattern underscores the ongoing demand for oil-absorbing materials. Adoption is particularly strong in packaged snack manufacturing, quick-service restaurants, and retail foodservice counters, where visual quality and perceived freshness directly influence purchasing decisions. As health-conscious behavior grows, oil-absorbing sheets offer a low-cost solution to enhance product appeal and hygiene standards.

Expansion of Foodservice and Commercial Kitchens

The global expansion of restaurants, quick-service outlets, cloud kitchens, and food-delivery platforms has increased demand for disposable, food-contact consumables. Oil-absorbing sheets are widely used for plating, takeaway packaging, and batch frying operations. Commercial kitchens prioritize materials that reduce oil carryover, prevent sogginess, and maintain food texture during transit.

As urbanization accelerates in emerging economies and new restaurant outlets continue to open in developed markets, procurement volumes for foodservice consumables rise correspondingly. Institutional buyers prefer standardized materials that improve presentation consistency and reduce customer complaints. This institutional demand stabilizes manufacturers' revenue streams and supports long-term supply contracts.

Sustainability and Material Innovation

Sustainability initiatives across the retail and foodservice sectors are accelerating demand for biodegradable and cellulose-based oil-absorbents. Regulatory scrutiny of packaging waste and single-use plastics is driving a transition toward compostable fiber solutions. Innovations in high-GSM cellulose composites, hemp-based blends, and bamboo-derived materials improve oil absorption efficiency while maintaining structural integrity. T

hese advancements reduce sheet usage per serving and lower total waste output. Retailers increasingly require environmental certifications for shelf placement, creating a competitive advantage for suppliers offering validated eco-credentials. Material innovation, therefore, enables both premium pricing strategies and alignment with corporate sustainability commitments.

Barrier Analysis - Raw Material and Input Cost Volatility

Paper pulp, specialty cellulose fibers, and polymer binders are subject to commodity price fluctuations. Variability in global pulp markets and supply chain disruptions can increase production costs. Manufacturers operating in price-sensitive retail environments may struggle to pass cost increases to end customers. Annual input cost swings of 10-20% can significantly compress margins, particularly in commodity-grade reed oil-absorbing paper. Smaller producers with limited procurement leverage face greater exposure to raw material volatility, which affects profitability and long-term capital planning.

Substitution and Private-Label Competition

Oil-absorbing sheets compete with alternatives such as paper towels, greaseproof liners, and advanced fryer filtration systems. Large retailers and quick-service restaurant chains frequently source private-label absorbent sheets in bulk, exerting downward pressure on branded pricing. Manufacturing fragmentation in Asia intensifies cost competition, limiting differentiation in commodity segments. Mid-tier brands must justify premium pricing through performance validation, sustainability certifications, and distribution reach. Without clear differentiation, the risk of commoditization remains significant.

Opportunity Analysis - Premium Biodegradable Cellulose Products

Growing preference for compostable and environmentally responsible materials presents a scalable premium opportunity. If 5-10% of existing polymer-based volume transitions to cellulose-based alternatives by 2030, incremental revenue growth could add several percentage points above baseline forecasts. Biodegradable sheets allow suppliers to secure long-term contracts with environmentally conscious retailers and foodservice operators. Manufacturers that can provide third-party compostability certifications and consistent performance metrics can command higher average selling prices and improve profit margins.

E-Commerce and Direct-to-Consumer Expansion

Online sales currently account for 20-25% of the distribution share and are the fastest-growing channel. Subscription models, value multipacks, and bundled kitchen consumables support margin expansion and brand loyalty. If online penetration increases beyond 30% in urban markets, manufacturers may benefit from improved pricing control and customer data analytics. Even a 5% shift in supermarket volume to direct online sales could materially enhance gross margins for leading brands. Digital marketing also enables targeted promotion of premium, eco-certified formats.

Category-wise Analysis

Material Type Insights

Reed oil-absorbing paper is expected to hold an 81.4% market share in 2026, due to its established presence across household and foodservice applications. Produced primarily from high-GSM cellulose and creped fiber structures, reed-based sheets deliver reliable oil uptake, structural strength, and cost efficiency. Large supermarket chains in North America and Europe continue to stock reed-based absorbent sheets under both branded and private-label offerings, reinforcing procurement standardization. Quick-service restaurant operators favor reed paper for fried chicken, tempura, and snack plating due to its consistent absorption rate and compliance with food-contact safety standards. Manufacturers utilizing advanced creping, embossing, and pore-structure control technologies achieve uniform absorption performance, making reed paper suitable for high-volume institutional kitchens and packaged snack producers.

Cellulose-based and biodegradable materials represent the fastest-growing material category and are anticipated to gain incremental market share by 2033 as sustainability regulations tighten globally. Retail sustainability commitments and compostability mandates are accelerating the adoption of alternatives derived from bamboo pulp, hemp fiber, and recycled paper blends. Premium grocery chains are increasingly highlighting compostable oil-absorbing sheets in eco-friendly product sections, particularly in Western Europe and Japan. Performance advancements in multilayer cellulose composites now allow absorption levels comparable to those of conventional reed paper while reducing the environmental footprint. Although unit prices remain higher, foodservice operators benefit from improved oil retention efficiency that reduces sheet usage per serving. As packaging waste directives expand and corporate ESG targets become procurement criteria, cellulose-based materials are positioned for sustained above-average growth.

Product Type Insights

Square sheets are projected to account for 52.3% of the product type share in 2026, owing to their standardized dimensions and operational flexibility. Their uniform shape fits common trays, fryer baskets, takeaway boxes, and retail packaging formats, making them the default choice across supermarkets and foodservice outlets. Mass production through roll-to-sheet conversion systems ensures cost efficiency and supply consistency.

Large grocery retailers frequently offer square sheets in multipacks for household frying, while quick-service restaurants procure bulk cartons for high-volume operations. The format’s simplicity supports private-label expansion, particularly in North America and the Asia Pacific. Its compatibility with automated dispensing systems in commercial kitchens further strengthens its continued dominance.

Tempura paper and specialty round sheets are expected to be the fastest-growing product category and are anticipated to expand their share in premium and cuisine-specific foodservice applications. These formats are closely associated with Japanese and Korean culinary practices, where presentation aesthetics and precise oil control are critical. The rising global popularity of sushi bars, ramen outlets, and fusion cuisine restaurants has increased demand for authentic tempura paper.

Specialty round sheets are also gaining traction in gourmet burger chains and bakery outlets where visual plating quality influences customer perception. The rapid growth of air-fryer usage in households further supports demand for niche absorbent formats tailored to smaller cooking appliances. With higher average selling prices and stronger brand differentiation, specialty formats are emerging as a profitable growth segment within the broader product portfolio.

Regional Insights

North America Food Oil Absorbing Sheet Market Trends - QSR-Driven Demand, FDA Compliance, and Private-Label Volume Expansion

North America is projected to hold approximately 31.2% of the market share in 2026. The U.S. drives regional demand due to its dense quick-service restaurant network and highly organized grocery retail infrastructure. According to the U.S. Census Bureau and the National Restaurant Association, U.S. foodservice sales continue to expand annually, supporting consistent consumption of disposable absorbent food-contact paper products. Canada contributes a stable secondary demand, particularly in urban retail clusters such as Ontario and British Columbia. Several structural drivers shape the regional outlook. First, the U.S. quick-service and fast-casual restaurant segment continues to invest in packaging quality and control over presentation.

Large chains such as McDonald’s and Chick-fil-A have publicly reported packaging optimization initiatives to improve oil control and food appearance, indirectly supporting demand for absorbent liners and sheets. Second, major retail chains, including Walmart and Kroger, continue expanding private-label kitchen consumables, reinforcing high-volume procurement of square-format oil-absorbing sheets.

Regulatory oversight significantly influences product development timelines. The U.S. Food and Drug Administration regulates food-contact paper materials under Title 21 CFR, requiring compliance for absorbent sheets used in direct food contact. Compostability standards such as ASTM D6400 certification also influence procurement decisions, particularly for retailers that have announced sustainable packaging targets.

For example, Whole Foods Market continues to expand its compostable and FSC-certified paper product assortments, encouraging suppliers to incorporate recycled or biodegradable fibers. Investment activity in the region focuses on automation and material innovation. Companies such as Georgia-Pacific and Hoffmaster Group have invested in advanced converting technologies that improve creping precision and absorption uniformity. Hoffmaster’s expansion of sustainable tabletop and foodservice paper products reflects broader regional demand for eco-compliant alternatives. Private-label consolidation among grocery retailers also increases bargaining power, creating margin pressure for smaller converters while benefiting scaled producers with integrated pulp sourcing.

Europe Food Oil Absorbing Sheet Market Trends - EU Circular Economy Mandates and Sustainable Fiber Innovation

Europe represents a mature yet innovation-driven market for food oil-absorbing sheets, supported by structured retail systems and regulatory harmonization within the European Union. Germany and the U.K. serve as primary consumption centers due to high per-capita foodservice spending and strong supermarket penetration. France and Spain demonstrate incremental demand driven by tourism-related restaurant activity, particularly in urban hospitality hubs. EU-wide packaging and waste directives significantly shape material selection.

The EU Packaging and Packaging Waste Directive (PPWD) and national circular-economy action plans encourage reduced plastic use and increased adoption of compostable paper. This regulatory environment accelerates demand for cellulose-based and FSC-certified absorbent sheets. Retailers such as Tesco (UK), Carrefour (France), and Edeka (Germany) have implemented sustainability roadmaps that prioritize recyclable or biodegradable food-contact paper products, influencing supplier portfolios.

Germany’s strong base of converting and specialty paper manufacturing supports regional production. Companies such as Metsä Tissue and Sappi Europe continue to expand sustainable fiber sourcing and lightweight specialty paper technologies, thereby indirectly benefiting adjacent categories, such as absorbent food liners. In 2024, Metsä Group announced continued investment in fiber innovation and resource efficiency at its tissue and specialty paper facilities, reinforcing Europe’s focus on lower-carbon pulp solutions. These developments improve supply reliability and sustainability credentials for downstream converters producing oil-absorbing sheets. The U. K’s Extended Producer Responsibility (EPR) scheme for packaging, implemented in stages through 2024 and 2025, further pressures brands to demonstrate recyclability and waste reduction. As a result, foodservice operators increasingly shift toward unbleached and compostable absorbent sheets to align with compliance requirements. Premium organic retail chains such as Bio Company in Germany and Planet Organic in the U.K. actively promote eco-certified kitchen consumables, stimulating demand growth in higher-margin biodegradable segments.

Asia Pacific Food Oil Absorbing Sheet Market Trends - Rapid QSR Expansion and Cost-Competitive Paper Manufacturing Growth

Asia-Pacific is likely to exhibit the highest growth rate globally, driven by rapid urbanization, expanding middle-class populations, and accelerated growth in the restaurant sector. China and Japan provide a strong baseline consumption due to established culinary traditions involving fried and tempura-style foods. India and ASEAN economies deliver significant incremental growth potential as organized retail and quick-service restaurant chains expand. China’s large-scale foodservice sector supports consistent demand for absorbent paper products.

According to data from China’s National Bureau of Statistics, catering industry revenues have shown sustained recovery and expansion following pandemic disruptions, reinforcing institutional demand. Domestic manufacturers benefit from cost-efficient pulp processing and extensive converting networks in provinces such as Zhejiang and Guangdong. Companies such as Hengan International and APP China continue investing in paper production capacity, strengthening raw material availability for absorbent sheet manufacturing.

India and Southeast Asia are experiencing high-growth trajectories, supported by international QSR expansion. Brands such as KFC, Jollibee, and Domino’s Pizza continue adding outlets across urban centers, increasing institutional procurement of absorbent liners and sheets. Organized supermarket chains, including Reliance Retail in India and Central Group in Thailand, are expanding private-label kitchen consumables, enhancing product visibility and accessibility. Environmental regulations across the Asia Pacific are tightening incrementally. China’s phased plastic-reduction policies and India’s single-use plastic restrictions encourage the use of paper-based alternatives in food applications. While cost sensitivity remains high in commodity segments, investments in converting capacity and export-oriented production strengthen regional competitiveness.

Competitive Landscape

The global food oil absorbing sheet market exhibits moderate fragmentation. Mid-sized manufacturers and private-label suppliers account for significant volume, while numerous regional converters serve local demand. Competitive positioning splits between cost-focused commodity producers and innovation-driven premium brands. Scale, sustainability certification, and supply chain integration differentiate leading players.

Key strategies include sustainability-led innovation, cost optimization through regional manufacturing, channel diversification, and certification-driven differentiation. Market leaders focus on securing institutional contracts and strengthening online presence, while emerging players emphasize niche premium formats.

Key Industry Developments

- In June 2025, BiOrigin Specialty Products launched “BioGuard™”, a 100% food-safe, oil- and grease-resistant paper designed for improved absorption and sustainability, expanding high-performance options for foodservice and packaging applications.

Companies Covered in Food Oil Absorbing Sheet Market

- Huhtamaki Oyj

- Berry Global Inc.

- Mondi Group

- Amcor plc

- Brady Corporation

- Purajan Co., Ltd.

- Tikusan Co., Ltd.

- Shenzhen Beite Purification Technology Co., Ltd.

- Weifang MayShine Imp & Exp Co., Ltd.

- Ningbo Riway Industrial Co., Ltd.

- Mudanjiang Hengfeng Paper Co., Ltd.

- Georgia-Pacific LLC

- Ahlstrom

- Duni Group

- Nordic Paper Holding AB

- Hoffmaster Group, Inc.

- Fujimori Kogyo Co., Ltd.

- Oji Holdings Corporation

Frequently Asked Questions

The global food oil absorbing sheet market size is projected to be valued at US$195.7 million in 2026.

By 2033, the food oil absorbing sheet market is expected to reach US$261.0 million.

Key trends include rising demand for biodegradable and cellulose-based materials, expansion of quick-service restaurants globally, increasing private-label penetration in supermarkets, growth of online sales channels, and premiumization through specialty formats such as tempura and round sheets.

By material type, reed oil absorbing paper leads with an anticipated 81.4% market share, while by product type, square sheets dominate with 52.3% share due to standardized dimensions and broad retail distribution.

The food oil absorbing sheet market is expected to grow at a CAGR of 4.2% between 2026 and 2033.

Major companies include Huhtamaki, Berry Global Inc., Mondi Group, Purajan Co., Ltd., and Brady Corporation.