- Food Ingredients & Additives

- Food-Based Essence Market

Food-Based Essence Market Size, Share and Growth Forecast, 2026-2033

Food-Based Essence Market by Source (Vegetable Essence, Fruit Essence), Form (Liquid, Powder), Application (Beverages, Bakery & Confectionery, Dairy & Frozen Desserts, Savory & Snacks, Processed & Convenience Foods, Specialty & Functional Nutrition), and Regional Forecast for 2026-2033

Food-Based Essence Market Share and Trends Analysis

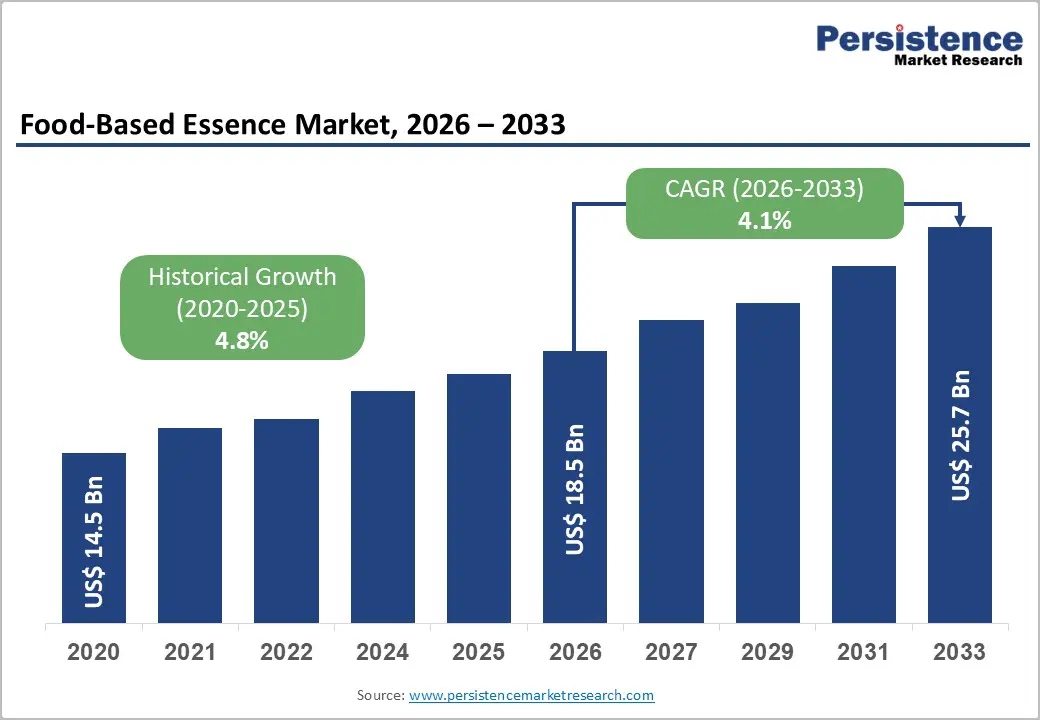

The global food-based essence market size is likely to be valued at US$ 18.5 billion in 2026, and is projected to reach US$ 25.7 billion by 2033, growing at a CAGR of 4.8% during the forecast period 2026-2033. This trajectory is supported by a sustained demand for natural taste solutions as consumers have increasingly favored recognizable ingredients over synthetic flavorings in everyday products.

Rising consumption of processed and convenience foods has continued to create a broad volume base, while fruit- and vegetable-derived essences are gaining share in beverages, dairy alternatives, and functional nutrition formats that promise both flavor and added benefits. For brand owners, this shift has created an opportunity to reposition legacy ranges with more transparent labels while using concentrated essences to maintain cost control and formulation flexibility. Regulatory encouragement for clean-label formulations has also reinforced the use of food-based essences, as authorities and standard-setting bodies have promoted plant-origin ingredients and clearer disclosure practices. At the same time, advances in extraction, encapsulation, and stabilization technologies are allowing manufacturers to protect volatile notes, extend shelf life, and retain performance under challenging processing conditions such as high heat or low pH.

Key Industry Highlights

- Dominant Source: Fruit-based essences are expected to hold around 60% market revenue share in 2026, due to their extensive usage in beverage and bakery products.

- Leading Form: Liquid essences are projected to dominate with 70% share in 2026, driven by ease of blending, with powdered forms growing at about 5.6% CAGR, owing to their shelf stability.

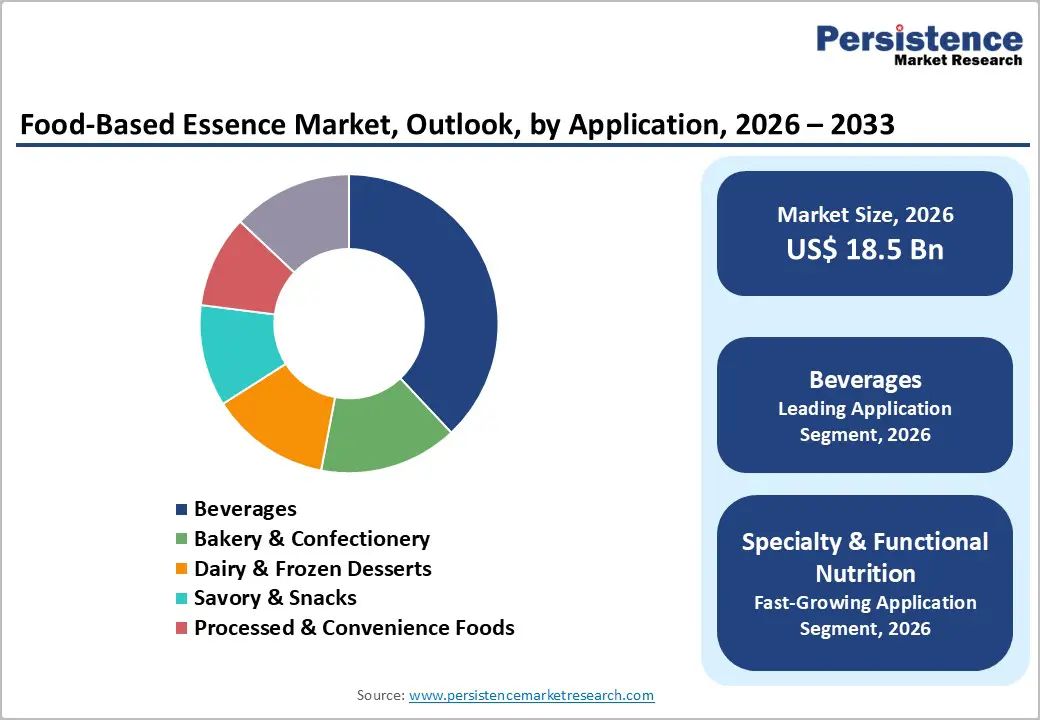

- Primary Application: Beverages are likely to lead with 38% share in 2026, reflecting high-volume functional drink consumption, while specialty & functional nutrition registering about 6.4% CAGR through 2033, driven by health-focused product innovation.

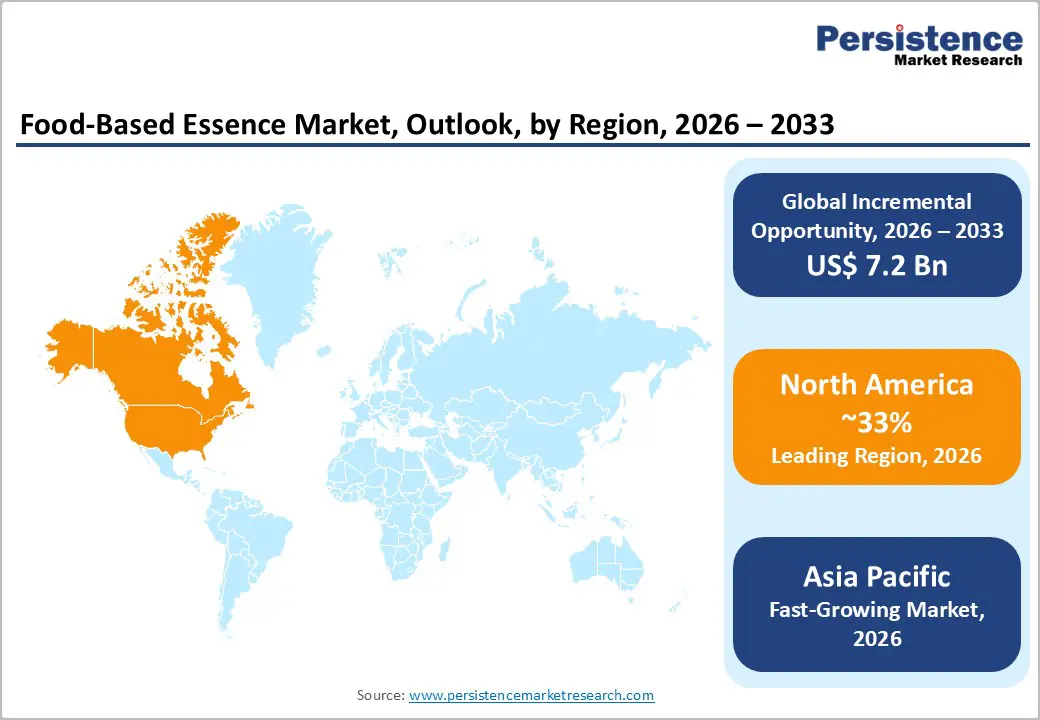

- Regional Leadership: North America is set to lead with an estimated 33% share due to an advanced food processing infrastructure, whereas the Asia Pacific market is expected to grow the fastest at nearly 6% CAGR through 2033, fueled by rapid expansion of food manufacturing.

- Competitive Dynamics: Competition is increasingly shaped by natural extraction innovation, capacity expansion, and regional localization strategies, with leading players prioritizing Asia-focused investments.

- April 2025: Corbion launched Verdad® Essence WH100, a cultured wheat-based natural mold inhibitor for clean-label bakery products, paired with an enhanced predictive Natural Mold Inhibition Model.

| Key Insights | Details |

|---|---|

| Food-Based Essence Market Size (2026E) | US$ 18.5 Bn |

| Market Value Forecast (2033F) | US$ 25.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Shift towards Natural, Scalable, and Technology-Enabled Flavor Solutions

Consumer preferences have moved decisively toward natural and clean-label food ingredients, driven by growing awareness of ingredient transparency and increasing regulatory scrutiny of artificial additives. Regulatory guidance from the U.S. Food and Drug Administration (FDA) and European Food Safety Authority (EFSA) has accelerated reformulation across beverages, dairy, and bakery categories, pushing manufacturers to prioritize plant-based flavor sources. As a result, fruit essences such as apple, grape, and berry, along with vegetable essences including carrot, cucumber, and tomato, are witnessing sustained demand. Industry observations also indicate that clean-label product launches continue to outpace conventional alternatives in developed markets, reinforcing premiumization trends and long-term demand stability for food-based essences.

Rampant urbanization, higher workforce participation, and evolving dietary habits are fueling global growth in processed and convenience foods, particularly in Asia Pacific and Latin America, as highlighted by the Food and Agriculture Organization (FAO). Food-based essences enable manufacturers to maintain consistent taste profiles at scale while optimizing formulation costs, making them essential in bakery & confectionery, savory snacks, and ready-to-eat meals. Technological advances in cold extraction, solvent-free processing, and microencapsulation have further improved flavor retention, solubility, and shelf life. Evidence shows these technologies significantly enhance stability, reduce wastage, and expand application potential in functional nutrition and dairy products, strengthening overall return on investment for food manufacturers.

Supply Chain Volatility and Regulatory Fragmentation

Food-based essences rely heavily on agricultural raw materials, making the market structurally exposed to climate variability, crop yield fluctuations, and geopolitical trade disruptions. The World Bank and FAO have documented that fruit and vegetable supply chains are becoming increasingly unstable due to extreme weather events, including droughts, floods, heatwaves, and unseasonal rainfall, combined with disruptions in global trade flows. These factors reduce crop yields, affect harvest quality, and create irregular supply cycles, resulting in frequent price fluctuations and sourcing uncertainty. For food-based essence manufacturers, such instability directly impacts the availability and cost of raw materials, raising procurement risks and complicating long-term production planning, particularly for smaller producers without secured contracts.

The regulatory compliance adds another layer of complexity, as standards vary significantly across regions. Agencies such as the FDA, EFSA, and regulators across Asia Pacific enforce differing requirements for labeling, solvent usage, and residual content. Navigating these multi-jurisdictional rules increases product development timelines and certification costs. Smaller suppliers face higher entry barriers, while multinational companies must adapt formulations for regional acceptance, limiting economies of scale and slowing broader market expansion.

Expanding Demand across Functional, Regional, and Shelf-Stable Applications

The global shift toward health-conscious diets has driven strong demand for food-based essences in functional beverages, protein supplements, and fortified foods. Flavored electrolyte drinks and plant-based protein shakes, enhanced with natural fruit essences such as cranberry, banana, and black raspberry, are gaining popularity for their improved taste and nutritional integrity. Powdered essences are increasingly incorporated into bakery mixes, snack seasonings, and instant beverages, supporting longer shelf life, operational efficiency, and flavor consistency, enabling food manufacturers to command higher margins and premium positioning.

Developing economies are rapidly becoming major hubs for both food-based consumption and production. Government-backed initiatives, such as expanded food processing parks in India, new flavor production facilities in China, and Indonesia’s US$ 22 billion investment in agricultural processing infrastructure, are supporting local ingredient production. Regional extraction and blending facilities help reduce logistics costs, tailor products to local taste preferences, and provide scalable solutions for global brands. As functional and shelf-stable products gain traction, these developments are expected to accelerate adoption and long-term growth across high-volume and premium food categories.

Category-wise Analysis

Source Insights

Fruit-based essences are expected to be the leading source segment, accounting for approximately 65% of global revenue in 2026, driven by broad application across beverages, dairy, and bakery products. Apple, grape, and banana essences dominate as preferred flavors due to universal consumer acceptance and formulation flexibility. For example, PepsiCo’s flavored fruit juice variants and Danone’s fruit-infused yogurt lines leverage fruit essences to enhance taste profiles while aligning with consumer clean-label preferences. Their consistent use in high-volume products enables stable long-term supply contracts and large-scale production planning. These essences also support brand differentiation through recognizable fruit notes in mainstream portfolios.

Vegetable essences are projected to be the fastest-growing source segment, projected to expand at a CAGR of 6.1% through 2033, supported by demand for savory and plant-forward products. Cucumber, carrot, and tomato essences are increasingly incorporated in health beverages, cold-pressed vegetable juices, soups, and plant-based meal solutions, enhancing natural flavor profiles. Companies such as Nestlé and Unilever have introduced vegetable-forward product lines that incorporate these essences to meet clean-label and health-focused consumer demand. The rising consumer acceptance of vegetable flavor profiles in mainstream food applications is strengthening adoption across developed and emerging markets.

Product Form Insights

Liquid essences are likely to be the dominant product form, estimated to hold 70% of market revenues in 2026, due to their ease of blending, rapid flavor dispersion, and suitability for beverages and dairy applications. Major beverage manufacturers, such as Coca?Cola with its fruit-infused sparkling water variants and Keurig Dr Pepper in flavored coffees and teas, rely on liquid formats to ensure consistent flavor dosing and efficient line throughput. The format’s versatility allows smooth integration into both hot and cold applications and maintains flavor clarity across product ranges. Additionally, liquid essences help beverage producers optimize formulation processes and minimize production variability.

Powdered essences are expected to be the fastest-growing product form, with a 5.6% CAGR through 2033, supported by expanding applications in bakery mixes, instant beverages, and snack seasonings. Powdered fruit and vegetable essences are increasingly used in products such as Mondelez International’s flavored snack lines and General Mills’ instant breakfast cereals for enhanced shelf life and operational efficiency. These essences offer advantages in logistics and storage while integrating seamlessly into dry formulations. Growing demand in emerging markets, particularly for convenience foods, underpins the accelerated adoption of powdered formats.

Application Insights

Beverages are projected to be the leading application segment, projected to account for 38% of the food-based essence market revenue share in 2026, driven by strong consumption volumes and continuous product innovation. Fruit essences play a central role in flavored water, juices, smoothies, and functional drinks, reflecting consumer preference for familiar, refreshing flavor profiles. For example, Nestlé’s flavored bottled waters and Red Bull’s fruit-enhanced energy drinks utilize fruit essences to balance taste with functional benefits. Beverage product portfolios continue to expand with novel flavor releases that appeal to younger, health-conscious consumers seeking both taste and value.

Specialty and functional nutrition is anticipated to be the fastest-growing application, anticipated to register a CAGR of 6.4% through 2033, backed by increasing consumer focus on health, wellness, and taste optimization in nutraceutical products. Food-based essences are widely used to improve palatability in protein shakes, fortified meal replacements, and vitamin-enriched beverages without compromising nutritional integrity. Companies such as Abbott Nutrition and Herbalife Nutrition incorporate natural essences in their functional formulations to enhance consumer compliance and product appeal. The combination of rising demand for health-oriented products and premiumization is accelerating adoption in both developed and emerging markets

Regional Insights

North America Food-Based Essence Market Trends

North America is forecasted to hold approximately 33% of the food?based essence market share in 2026, driven by strong demand for natural ingredients and clean?label products. The United States dominates, supported by advanced food processing infrastructure, robust R&D ecosystems, and early adoption of innovative formulations. Kraft Heinz has introduced vegetable?enhanced sauces using natural essences, while Dr Pepper Snapple Group continues to expand flavored beverage offerings with fruit essences in mainstream and niche categories. Regulatory oversight by the FDA encourages transparent labeling, reinforcing consumer trust and reformulation toward plant?based flavor solutions.

The competitive landscape in North America is defined by strategic investment in extraction technologies and flavor optimization. For instance, Campbell Soup Company has reformulated select ready?to?serve soups with cold?pressed vegetable essences to appeal to health?oriented consumers. PepsiCo North America continues to increase the use of natural fruit essences across its juice and hydration portfolios to meet evolving tastes. Partnerships between food processors and ingredient suppliers focus on accelerating new flavor introductions, improving production efficiency, and expanding capacity to support both beverage and specialty nutrition segments.

Europe Food-Based Essence Market Trends

Europe represents a mature and sophisticated market for food-based essences, holding a considerable share of the market, supported by harmonized regulatory frameworks and consumer preference for quality. Key markets such as Germany, the U.K., France, and Spain are at the forefront, with strong uptake in premium bakery and dairy applications. Nestlé Europe has incorporated natural fruit essences into its yogurt and dairy beverage lines, while Danone Europe has expanded the use of plant-based vegetable essences in chilled soups and sauces. Regulatory alignment under EFSA promotes consistent quality standards, supporting wider adoption of natural ingredient usage across product portfolios.

European manufacturers also emphasize traceability and sustainability, aligning with consumer expectations for responsibly sourced food components. For example, Arla Foods has integrated sustainable fruit essences in its organic milk and flavored milk products to differentiate offerings in health?centric segments. In addition, Unilever Europe continues to scale plant?based meal solutions and premium sauces that leverage botanical essences for enhanced flavor. Growing investment in organic and minimally processed flavor solutions, paired with strategic collaborations between food producers and ingredient innovators, reinforces Europe’s significant role in the global food?based essence landscape.

Asia Pacific Food-Based Essence Market Trends

Asia Pacific is projected to be the fastest?growing regional market for food-based essences, projected to register a 6% CAGR through 2033, driven by rapid expansion of food and beverage manufacturing, rising disposable incomes, and shifting dietary patterns. China, India, and ASEAN countries are key contributors, with growing middle?class demand for flavored and convenience foods. Ting Hsin International Group in China has expanded its instant noodle and sauce offerings using both fruit and vegetable essences to meet local taste preferences. In India, ITC Foods has introduced flavored snack segments that utilize vegetable essences to appeal to health?oriented consumers.

Government support for food processing investments and ingredient localization further amplifies growth opportunities. For example, Malaysia’s agrifood processing incentives have encouraged companies such as QSR Brands to incorporate locally sourced natural essences into ready?to?eat sauces and beverages. Kerry Group Asia Pacific continues to invest in regional manufacturing hubs to improve supply chain efficiency and tailor flavor solutions for local markets. As global players deepen their presence and local innovators respond to culturally specific tastes, the accelerating growth trajectory of the Asia Pacific market remains a key strategic opportunity for businesses.

Competitive Landscape

The global food-based essence market is moderately consolidated, with leading players such as Givaudan, IFF, Symrise, Firmenich, and Mane collectively holding over 50% of revenue. These companies leverage strong client networks in beverages, bakery, dairy, and convenience foods, and invest in R&D for natural extraction, microencapsulation, and clean-label solutions. Proprietary technologies allow them to deliver high-stability, functional flavors that meet regulatory standards and evolving consumer preferences.

Regional and niche players, including Takasago, Kancor Ingredients, and Kerry Group, focus on specialty flavors, botanical extracts, and local taste profiles. Market entry barriers include raw material volatility and complex formulation requirements, but advances in powder processing and shelf-stable delivery formats enable smaller players to participate. Market consolidation is expected as global leaders acquire regional firms and form strategic partnerships to expand portfolios and geographic reach.

Key Industry Developments

- In January 2026, Juicy Marbles launched its whole-food Umami Burger in 225 U.K. Tesco stores, blending sunflower protein, fermented koji barley, quinoa, flax seeds, seitan, and miso for a versatile veggie patty. It bridges hyper-realistic meat alternatives and simple veggie burgers, offering savory flavor, springy texture, and an original or spinach-Mediterranean variant. The move taps demand among U.K. consumers for less processed plant-based options amid ultra-processing concerns.

- In November 2025, PepsiCo introduced its new “Simply NKD” line featuring Doritos and Cheetos variants free of artificial colors and flavors, aligning with rising clean?label consumer demand. The products retain classic taste profiles while using natural ingredients. This initiative positions PepsiCo toward healthier snack alternatives and expands its portfolio with additive?free options.

- In May 2025, Suntory Global Spirits launched -196™ vodka seltzer nationwide, featuring a new permanent Strawberry flavor alongside Lemon, Grapefruit, and Peach. The formulations have been crafted via Japanese Freeze Crush Infusion at -196°C for bold, whole-fruit taste with premium vodka and 3g sugar.

Companies Covered in Food-Based Essence Market

- Givaudan

- International Flavors & Fragrances

- Symrise

- Firmenich

- Kerry Group

- Sensient Technologies

- Takasago

- Mane

- Robertet Group

- Döhler Group

- Frutarom

- Blue Pacific Flavors

- Flavorchem

- Huabao International

Frequently Asked Questions

The global food-based essence market is projected to reach US$ 18.5 billion in 2026.

Key drivers include rising consumer preference for natural and clean-label ingredients, growth in processed and convenience foods, and technological advancements in extraction and encapsulation methods.

The market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Opportunities include functional and specialty nutrition products, expanding manufacturing hubs in Asia Pacific, and rising adoption of powdered essences for shelf-stable applications

Few of the leading companies in the market include Givaudan, IFF, Symrise, Firmenich, Mane, and Takasago.