- Processed Food

- Prepared Meals Market

Prepared Meals Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Prepared Meals Market By Product Type (Frozen Meals, Chilled Meals, Others), Distribution Channel (Supermarkets & Hypermarkets, Others), End-user, and Regional Analysis for 2025 - 2032

Prepared Meals Market Size and Trends Analysis

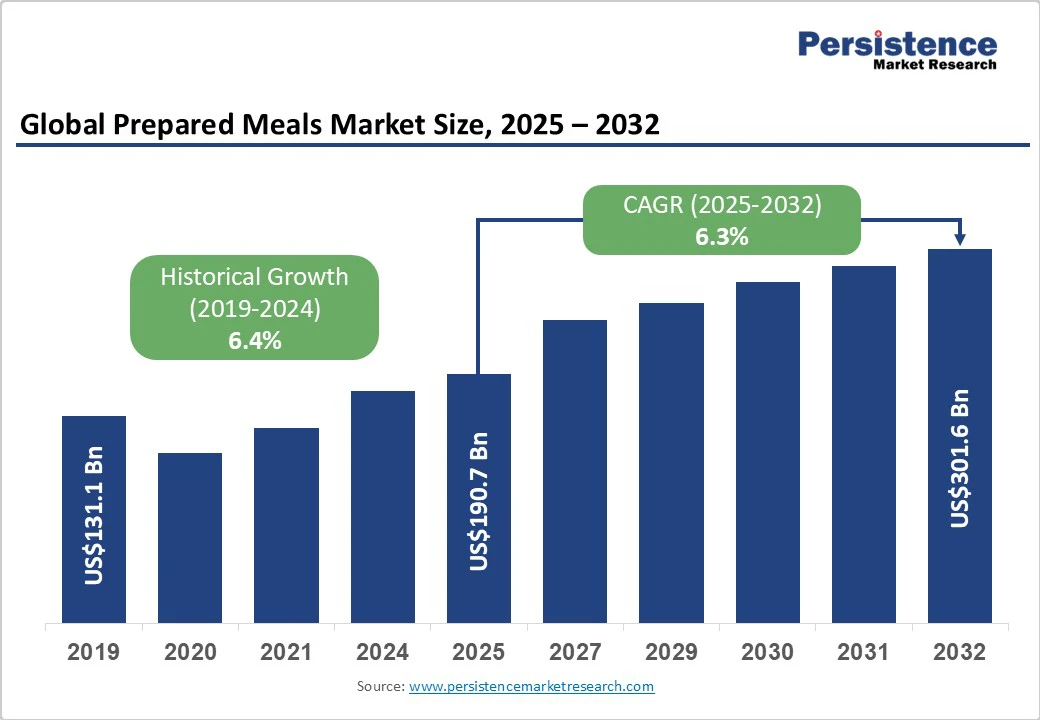

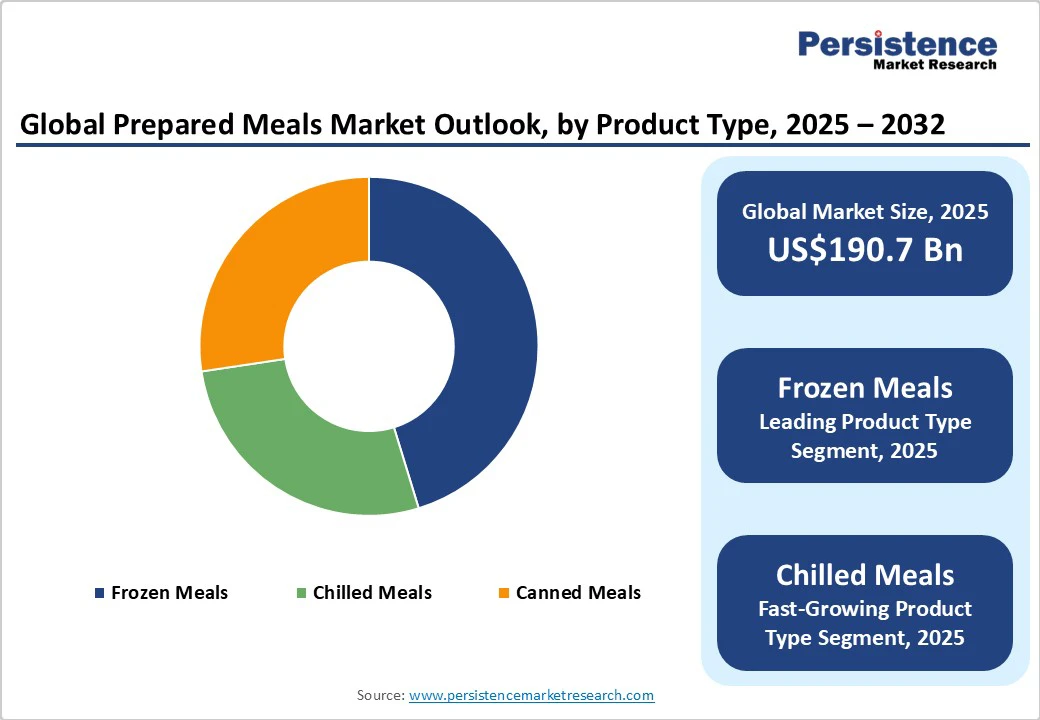

The global prepared meals market size is likely to be valued at US$190.7 Billion in 2025 and is expected to reach US$301.6 Billion by 2032, growing at a CAGR of 6.3% during the forecast period from 2025 to 2032, driven by rising consumer demand for convenient and time-saving food solutions, expansion of frozen and chilled product portfolios, and increased adoption of online retail and subscription-based meal delivery channels.

Key Industry Highlights:

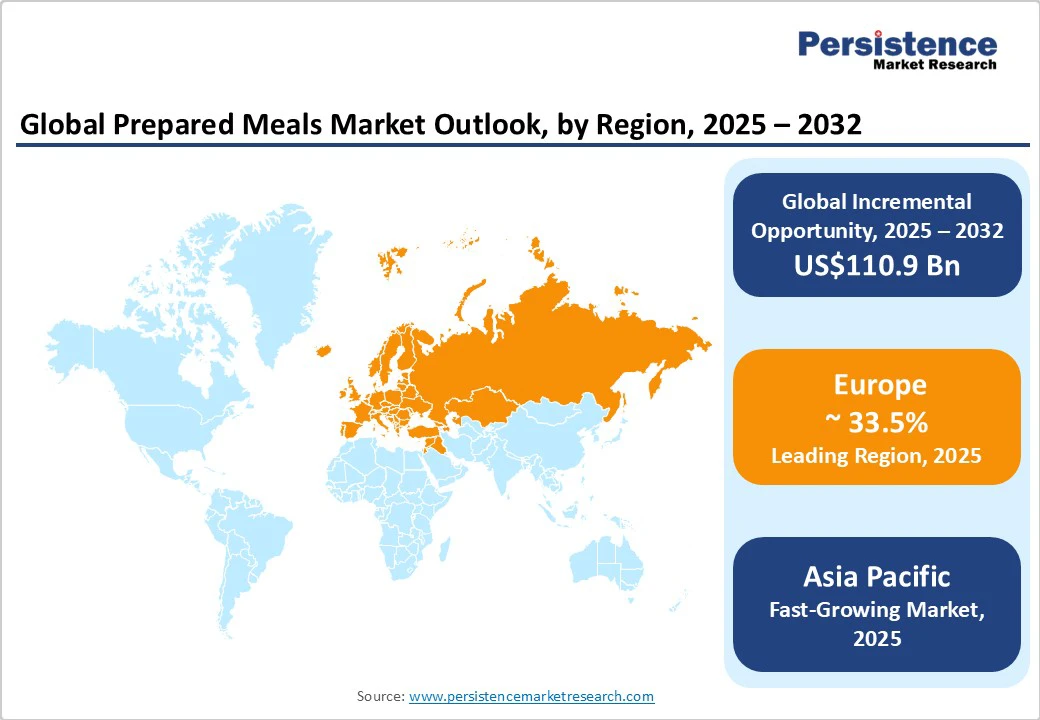

- Leading Region: Europe, accounting for approximately 33.5% share in 2025, supported by high urbanization, strong retail penetration, and evolving consumer demand for convenience and premiumization.

- Fastest-Growing Region: Asia Pacific, projected CAGR above 7% between 2025 and 2032, driven by urbanization, e-grocery adoption, and rising disposable incomes.

- Investment Plans: Expansion of cold-chain infrastructure, automation, plant-based and premium chilled meal facilities; notable developments include Ajinomoto’s China frozen meal kits (2024) and McCain’s new India production facility.

- Dominant Product Type: Frozen meals account for 42.6%, leading by value due to their extended shelf life, which accounts for 42% of retailer penetration and widespread consumer familiarity.

- Leading Distribution Channel: Supermarkets & hypermarkets hold a 54.8% share, contributing the largest revenue globally due to high shopper frequency, refrigerated aisle availability, and trusted brand presence.

| Key Insights | Details |

|---|---|

|

Prepared Meals Market Size (2025E) |

US$190.7 Bn |

|

Market Value Forecast (2032F) |

US$301.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Convenience & Demographic Changes

Rising urbanization, higher female workforce participation, and evolving household structures have significantly boosted demand for prepared meals. In the U.S., ready-meal sales grew approximately 6–7% annually between 2019 and 2023. Consumers are increasingly shifting their purchases from foodservice to retail and e-commerce channels. Manufacturers are expanding SKUs across healthy, plant-based, and premium offerings to capture frequency and wallet share. The sustained demand for convenience presents a measurable opportunity for revenue growth and product diversification.

Technology and Shelf-Life Innovations

The adoption of High-Pressure Processing (HPP), modified-atmosphere packaging, and automated cook-chill systems has extended shelf life without the need for high preservative use. Advances in refrigeration and packaging have improved food safety and distribution efficiency. These innovations reduce barriers for national and regional product rollouts, particularly for chilled and fresh-frozen Stock Keeping Units (SKUs). They enable brands to launch premium, clean-label meals while maintaining quality, minimizing shrinkage, and capturing higher margins.

Channel Shift: E-commerce & Direct-to-Consumer Models

Online retail and subscription meal delivery are among the fastest-growing channels. Although starting from a modest base, these channels offer higher average selling price (ASP) potential and consumer data insights. Investments in omnichannel capabilities, cold-chain logistics, and subscription retention mechanics allow brands to maximize customer lifetime value. This channel growth also requires careful evaluation of cost-to-serve and strategic assortment of SKUs.

Barrier Analysis - Cold-Chain and Input Cost Pressures

Rising energy, packaging, and refrigerated transport costs create margin pressures, particularly for smaller manufacturers with limited scale. Cold-chain infrastructure increases working capital requirements and break-even volumes. Operators must optimize logistics, negotiate long-term contracts, and adjust packaging strategies to mitigate volatility and protect profitability.

Regulatory and Nutrition Scrutiny

Prepared meals are subject to stringent nutrition labeling, allergen management, and front-of-pack disclosure regulations. Reformulation and relabeling efforts can increase per-SKU development costs and delay time-to-market by several months. Proactive investment in regulatory intelligence and flexible reformulation processes is crucial for remaining compliant and market-ready.

Opportunity - Premium Healthy & Functional Meals

Demand for nutritious, low-preservative prepared meals continues to rise. High-protein, plant-based, and low-sodium options are gaining traction rapidly. Premium and healthy SKUs could represent a significant incremental opportunity by 2030 if they capture 8–12% of volume growth within the broader market. Verified health claims and clean-label positioning can enable higher ASP and retailer placement.

Emerging Markets & Regional Manufacturing

APAC countries, such as China, India, Japan, and ASEAN nations, are experiencing a rapid adoption of prepared meals due to urbanization and modern retail growth. Establishing local manufacturing reduces landed costs, accelerates market entry, and enables competitive pricing for premium SKUs. Regional production also allows faster response to local taste preferences and regulatory requirements.

Category-wise Analysis

Product Type Insights

Frozen meals continue to dominate the prepared meals category, accounting for 42.6%, due to several structural advantages. Frozen meals enjoy strong demand due to their long shelf life, minimal spoilage, and ease of inventory management. High retailer penetration and prime shelf placement in supermarkets drive visibility. North America and Europe lead consumption, with brands such as Lean Cuisine, Healthy Choice, and Birds Eye contributing significantly. Private labels from Tesco, Walmart, and Carrefour also contribute to boosting market share. Versatile formats—from family packs to single-serve meals- ensure high repeat purchases, making frozen meals a high-volume, high-value segment.

Chilled meals are experiencing the fastest growth across mature markets due to premiumization trends and increasing consumer preference for fresh, clean-label products. Technological advancements, such as Modified Atmosphere Packaging (MAP), high-pressure processing (HPP), and enhanced cold-chain logistics, have extended the shelf life of chilled products without compromising their quality or nutritional integrity. Examples include Bakkavor’s fresh meal bowls in the U.K. and Greencore’s ready-to-eat salads, which target health-conscious consumers seeking convenience with freshness. The higher perceived value allows brands to command premium prices (ASP uplift of 10–20%), positioning chilled meals as a margin-enhancing, high-growth category. Retailers are also expanding shelf space for chilled SKUs, further accelerating adoption.

Distribution Channel Insights

Brick-and-mortar retail remains the largest channel by value, supported by strong shopper frequency, wide product assortment, and trust in established brands. Supermarkets and hypermarkets provide the infrastructure for refrigerated and frozen product displays, allowing consumers to purchase meals alongside other grocery items conveniently. Leading chains such as Walmart, Kroger, Tesco, Carrefour, and Sainsbury’s dominate the segment, offering both national brands and private-label alternatives. The channel’s prominence also ensures consistent visibility for new product launches and seasonal or promotional SKUs, reinforcing repeat purchases.

Online retail, including e-commerce platforms and subscription meal delivery services, is the fastest-growing channel for prepared meals. Growth is driven by increasing consumer adoption of e-grocery, cold-chain logistics improvements, and changing shopping behavior among millennials and Gen Z. Brands such as HelloFresh, Factor, and Blue Apron in the U.S., and Gousto and Mindful Chef in the U.K., are leveraging direct-to-consumer (D2C) models to provide personalized meal plans, premium options, and convenience. Online channels offer higher margins, detailed consumer insights, and opportunities for cross-selling premium or functional SKUs, while also enabling rapid geographic expansion without the need for traditional retail infrastructure.

Convenience stores, vending machines, and on-the-go outlets cater to immediate consumption or impulse purchases. Brands such as 7-Eleven Ready Meals and Lawson’s Bento Boxes in Japan exemplify success in urban, high-traffic environments. Although smaller in revenue share than supermarkets or online channels, convenience formats are critical for capturing urban commuters, single-person households, and emergency food purchases.

End-user Insights

Household consumers are the largest end-user segment, representing the majority of prepared meal consumption globally. Dual-income households, urbanization, and the increasing need for time-saving solutions drive growth. Products targeting household consumption range from single-serve frozen dinners to family-size ready meals. Brands such as Lean Cuisine, Stouffer’s, and Birds Eye cater to family and individual needs. Retail private labels also play a significant role, offering cost-effective alternatives that retain strong shelf space. Household adoption ensures consistent demand, forming the backbone of the prepared meals market.

Foodservice and delivery partnerships are emerging as the fastest-growing end-user segment, driven by cloud kitchens, meal kits, and grocery-linked prepared meal programs. Companies such as McCain Foods and Nestlé are partnering with cloud kitchens or restaurant chains to offer ready-to-eat meals, thereby expanding their distribution without incurring heavy capital expenditures. These partnerships enable hybrid B2B2C models, delivering convenience to end consumers while maximizing operational efficiency. The segment is particularly attractive for innovation in ethnic cuisine, functional meals, and premium offerings, providing both revenue and margin growth opportunities for brands expanding beyond retail channels.

Regional Insights

Europe Prepared Meals Market Trends - Premiumization, Sustainability & Chilled Meal Growth

Europe holds the largest share of the market, accounting for approximately 33.5% of revenue. Germany, the U.K., France, and Spain are key contributors, supported by high urbanization, strong retail penetration, and evolving consumer demand for convenience and premiumization. Regulatory harmonization across the EU ensures consistent food safety, allergen labeling, and nutritional disclosure, while sustainability mandates are driving the adoption of eco-friendly packaging. Leading players include Bakkavor, Nomad Foods, and Greencore, complemented by extensive private-label programs with major retailers such as Tesco, Carrefour, and Lidl.

Recent developments include Nomad Foods’ acquisition of a chilled ready-meal facility in Germany in 2024, enabling faster product rollouts, and Greencore’s expansion of plant-based meal offerings in the U.K. in 2025. Country insight: Germany shows the highest consumption of chilled premium meals, whereas the U.K. market demonstrates rapid growth in online and subscription meal channels. Investment priorities focus on sustainable packaging, premium chilled offerings, and expanding cold-chain logistics for omnichannel distribution.

North America Prepared Meals Market Trends - Frozen Meal Dominance & D2C Expansion

North America, led by the U.S., represents a highly mature and influential market for prepared meals, with per-capita consumption among the highest globally. The region has witnessed robust growth across frozen, chilled, and meal-delivery channels, driven by urbanization, busy lifestyles, and increased adoption of convenience foods. Regulatory oversight is stringent, with FDA labeling requirements, FSMA food safety compliance, and calorie/nutrition disclosure regulations ensuring consumer safety and transparency.

The competitive landscape is dominated by multinationals such as Nestlé, Conagra, General Mills, and Kraft Heinz, while major retailers like Walmart and Kroger continue to expand their private-label offerings. In recent developments, Nestlé launched a plant-based frozen meal line in 2024, targeting health-conscious consumers, while Blue Apron expanded its U.S. delivery network in 2023, reflecting the growing interest in direct-to-consumer (D2C) models. In the U.S., frozen meals account for over 40% of total prepared meal retail sales, whereas subscription meal kits are capturing younger, tech-savvy demographics. Investments focus on automation, cold-chain infrastructure, and co-packing to enhance operational efficiency and scale.

Asia Pacific Prepared Meals Market Trends - Urbanization-Driven Surge & Localized Production

The Asia Pacific is the fastest-growing region for prepared meals, driven by urbanization, rising disposable incomes, and the expansion of modern retail. China leads adoption, supported by increasing e-grocery penetration, busy urban lifestyles, and rapid growth of ready-to-eat options. Japan and India are notable for premium and convenience-focused meals, while ASEAN countries are emerging markets for both retail and foodservice segments. Local manufacturing is a key strategy for cost competitiveness and faster market entry, often implemented through joint ventures or contract manufacturing arrangements. Recent developments include Ajinomoto Co., Inc. launching frozen meal kits in China in 2024 and McCain Foods opening a new production facility in India in 2023 to serve urban centers.

Chilled and frozen formats dominate China’s prepared meals market, while Japan emphasizes ready-to-eat convenience and functional nutrition products. Growth drivers include single- and two-person households, online retail expansion, and increasing e-grocery infrastructure, creating opportunities for both global and regional players to capture high-volume urban markets.

Competitive Landscape

The global prepared meals market combines scale-driven multinationals with fragmented private-label and regional operators. Leading players hold single-digit to low-teens market shares by region, with concentration higher in North America and Europe and more fragmented in APAC. Strategic positioning spans cost leadership, premiumization, and innovation in packaging and formulations.

Key strategies include product innovation (clean-label, functional), channel diversification (online, D2C), regional manufacturing to reduce costs, and sustainability initiatives. Leading companies leverage scale for cost efficiency while pursuing premium offerings and collaborating with retailers.

Key Industry Developments:

- In August 2025, Fresh Prep Foods, a major meal kit delivery service in Canada, launched Zero Waste Kit to make meal kits more sustainable. These kits vastly reduce the need for single-use plastics, saving 22,851 kg of single-use plastic waste from entering the environment in 2024 alone.

- In September 2025, Hamburger Helper introduced a new line of breakfast meal kits, marking its first expansion beyond dinner offerings. Available nationwide at retailers such as Walmart and Kroger, the breakfast lineup offers both at-home and on-the-go options designed to provide convenient and affordable morning meals.

- In September 2025, Tesco launched a new line of "restaurant-quality" ready meals called the Finest Chef's Collection, available in 160 stores across the U.K. Developed by Tesco’s in-house chefs, the collection features 12 premium dishes inspired by Italian, Indian, and British cuisines, designed to serve two people.

Companies Covered in Prepared Meals Market

- Nestlé S.A.

- General Mills, Inc.

- Conagra Brands, Inc.

- The Kraft Heinz Company

- Tyson Foods, Inc.

- McCain Foods Limited

- Nomad Foods Limited

- Bakkavor Group plc

- Greencore Group plc

- Ajinomoto Co., Inc.

- Campbell Soup Company

- Kellanova (Kellogg spin-off)

- Orkla ASA

- MTR Foods Pvt. Ltd.

- Hormel Foods Corporation

- Bonduelle S.A.

- Pinnacle Foods (Conagra subsidiary)

- Ready Pac Foods, Inc.

- Freshly, Inc.

- Blue Apron Holdings, Inc.

Frequently Asked Questions

The prepared meals market size was valued at US$190.7 Billion in 2025.

The prepared meals market is projected to reach US$301.6 Billion by 2032.

Key trends include premiumization of chilled meals, growth of online retail and D2C channels, plant-based and clean-label product launches, expansion of cold-chain infrastructure, and increased adoption of frozen meals in emerging markets.

The frozen meals segment leads by value, accounting for approximately 42.6% of total product sales in 2025, driven by extended shelf life, retailer penetration, and strong consumer familiarity.

The prepared meals market is expected to grow at a CAGR of 6.3% between 2025 and 2032.

Major players include Nestlé S.A., General Mills, Inc., Conagra Brands, Inc., The Kraft Heinz Company, and Bakkavor Group plc.