- Specialty & Fine Chemicals

- Fatty Amines Market

Fatty Amines Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Fatty Amines Market Analysis By Product Type (Primary Fatty Amines, Secondary Fatty Amines, Tertiary Fatty Amines), Source (Petrochemical‑based, Oleochemical‑based), Form (Liquid, Solid), Application, End-use and Regional Analysis 2025 - 2032

Fatty Amines Market Share and Trends Analysis

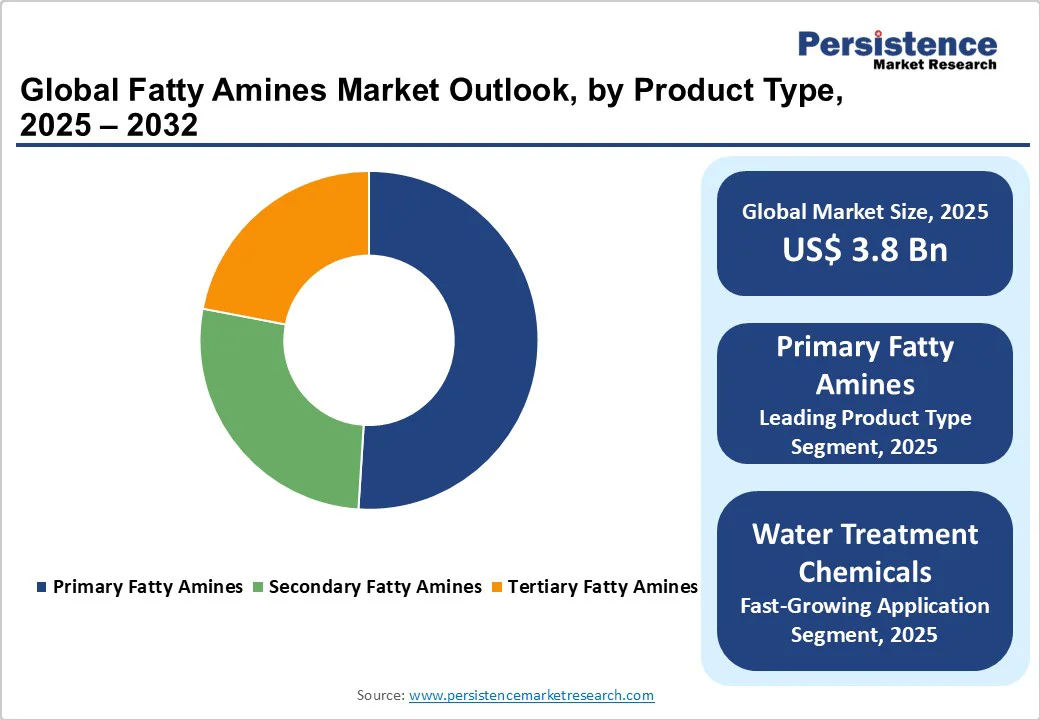

The global fatty amines market size is likely to value at US$ 3.8 Bn in 2025 and is projected to reach US$ 5.9 Bn by 2032, growing at a CAGR of 6.7% between 2025 and 2032. Growth is propelled by intensifying agrochemical usage for yield improvement and pest control, rising industrial and municipal water treatment investments, and expanding use of cationic surfactants and amine oxides in household and industrial cleaning.

Key Market Highlights

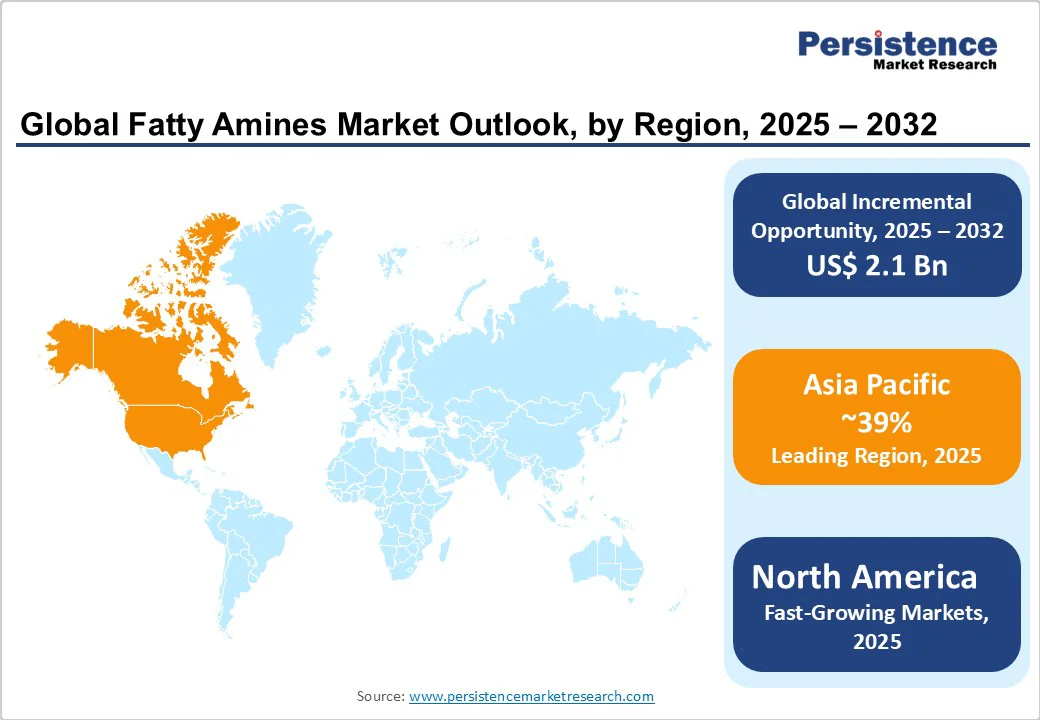

- Leading region: Asia Pacific leads on manufacturing scale, cost advantages, and broad end use demand across agrochemicals, water treatment, and construction chemicals, supported by ongoing capacity expansions and technology localization.

- Fastest growing region: North America is set for robust growth on the back of high performance cationic surfactants in cleaning and investments in industrial water management, under strong regulatory and innovation ecosystems.

- Dominant segment: Primary Fatty Amines hold the largest product share near 51%, underpinned by their indispensable role as intermediates and direct agents in anti caking, flotation, and corrosion inhibition.

- Fastest growing segment: Water Treatment Chemicals show accelerated adoption given stricter discharge standards, reuse targets, and industrial utility upgrades, with fatty amines used as biocides and corrosion inhibitors.

- Key market opportunity: Bio based and mass balance certified amines unlock premium positioning for personal care, cleaning, and regulated applications by improving lifecycle metrics while retaining performance.

| Key Insights | Details |

|---|---|

|

Fatty Amines Market Size (2025E) |

US$ 3.8 Bn |

|

Market Value Forecast (2032F) |

US$ 5.9 Bn |

|

Projected Growth CAGR (2025-2032) |

6.7% |

|

Historical Market Growth (2019-2024) |

5.4% |

Market Dynamics

Drivers - Heightened reliance on agrochemical performance enhancers

Global food security needs and pest pressures are pushing adoption of efficient formulations, where fatty amines function as emulsifiers, dispersants, and wetting agents that improve active ingredient delivery. Fertilizers and crop-protection products increasingly incorporate fatty amines and derivatives as anti-caking and adhesion aids, sustaining double-digit volume needs in peak seasons. Fatty amines support anticaking of fertilizer granules and stability of herbicide emulsions, with water repellent properties especially valued in fertilizers and agrochemical intermediates. Parallel growth in adjacent value chains, such as the Fatty Alcohol Market and Dimer Fatty Acid Market, reinforces integrated oleochemical sourcing and downstream formulation innovation.

Growing Investments in Water Treatment and Hygiene

Industrial and municipal water treatment demand has intensified, driven by stricter discharge norms, heightened public health vigilance, and infrastructure upgrades. Fatty amines act as biocides, disinfectants, and corrosion inhibitors across treatment trains, contributing to measurable adoption gains. Industry sources highlight fatty amines’ role as powerful bacteria killing agents and corrosion inhibitors; the water treatment industry uses nearly a quarter of global fatty amines output by value share in recent assessments. In parallel, cationic surfactant derivatives of fatty amines are central to advanced cleaning and disinfection regimes in institutional and household applications, complementing the broader Industrial Water Treatment Chemicals ecosystem.

Restraint - Feedstock Price Volatility and Supply Uncertainty

Key raw materials, most notably ammonia and ethylene oxide, exhibit cyclical price swings tied to natural gas and ethylene markets. Elevated energy prices and competing demand in petrochemical chains can compress margins and disrupt planning cycles. Long running ammonia price variability and persistent ethylene oxide tightness both of which raise the cost base for amine synthesis and tertiary amine routes. Such volatility often triggers pass through pricing and can delay downstream demand in cost sensitive applications.

Regulatory scrutiny and substitution pressure in selected uses

Regional frameworks governing chemical safety, emissions, and residues (e.g., environmental and occupational exposure controls) can increase compliance costs and spur reformulation. While regulators in Canada have assessed several alkanolamine and fatty alkanolamide substances as low risk at typical exposures, ongoing global oversight and product specific migration limits in contact applications necessitate stewardship, testing, and documentation that elevate time to market and cost burdens. In commoditized segments, availability of alternative chemistries may cap pricing power.

Opportunities - Bio based and Lower impact Amines Across Home & Personal Care and Industrial Use

Sustainability commitments are accelerating a shift toward bio based routes and mass balance certified feedstocks. Advances in heterogeneous catalysis for bio amines and biomass balance certification models in the chemical industry provide credible decarbonization pathways and identical performance drop ins for existing formulations. Producers that scale bio naphtha/bio ethanol pathways or adopt green ammonia inputs can differentiate on lifecycle metrics while meeting rising brand-owner requirements in Personal Care & Cosmetics and Household & Industrial Cleaning end markets.

Capacity Expansions and Asia Manufacturing Optimization

Leading suppliers are expanding specialty amine capacity closer to demand centers to secure feedstock availability, cut logistics costs, and tailor grades to fast growing applications. Notably, capacity additions and site upgrades in China broaden portfolios and enhance cost positions for global players, aligning with long term demand in polyurethane, epoxy, water treatment, agrochemicals, and construction chemicals. Such brownfield and greenfield moves create supply optionality and support customized amine derivatives for high value segments. The momentum mirrors growth seen in related markets like the Fatty Amide Market and Fatty Acid Supplements Market, underscoring multi product synergies.

Category wise Insights

Product Type Analysis

Primary Fatty Amines lead with an estimated value share near 51%, reflecting their role as foundational intermediates for producing secondary and tertiary amines and their direct use as flotation agents, anti caking agents, and corrosion inhibitors. Market evaluations identify primary fatty amines as the dominant product class owing to their versatility across agrochemicals, water treatment, asphalt additives, and cationic surfactant precursors. Their centrality in synthesizing downstream amines helps stabilize utilization rates across cycles and underpins continuous demand from fertilizer conditioning and mineral processing.

Source Analysis

Oleochemical based amines command an estimated majority share of about 55%, anchored by ample availability of natural oils (palm, tallow, coconut/palm kernel) and established hydrolysis and hydrogenation routes in the oleochemicals sector. Industry literature indicates that a limited set of fats and oils contributes to the bulk of fatty acid production globally, feeding downstream amide and amine chains and supporting sustainability branding and certification programs. The visibility of large integrated oleochemical producers in Asia and Europe supports predictable sourcing and competitive cost curves relative to purely petrochemical based chains.

Form Analysis

Liquid form accounts for approximately 60% share, driven by ease of handling, blending, and dosing in surfactant, agrochemical, and water treatment formulations. Liquids facilitate inline emulsification and rapid incorporation into concentrates and finished goods, reducing processing steps and enabling tighter specification control for cationic surfactants, amine oxides, and corrosion inhibitor packages used across oilfield chemicals, cleaning, and industrial water systems. Solid forms remain important for logistics efficiency and certain downstream syntheses but trail liquids in multi sector versatility.

Application Analysis

Water Treatment Chemicals represents a leading application with around 24% utilization share, as fatty amines serve as biocides, disinfectants, flocculants, and corrosion inhibitors across municipal and industrial circuits. Rising investments in wastewater reuse, cooling water efficiency, and stricter discharge thresholds in Europe and North America sustain premium formulations, while industrialization across Asia grows baseline volume needs. Emulsifiers and Surfactants & Detergents are also significant, supported by fatty amine derivatives that stabilize emulsions and deliver cationic conditioning in home and personal care value chains.

Industry Analysis

Agrochemicals lead end use with an estimated 32% share, leveraging fatty amines in herbicide/emulsion systems and as anti caking agents in fertilizers to maintain flowability, reduce dusting, and enhance field performance. Sectoral growth aligns with population driven food demand and the need for resilient yields amid climate and pest pressures. Oil & Gas, Water Treatment, and Household & Industrial Cleaning collectively provide diversified downstream exposure, ensuring relative demand resilience and providing avenues for specialty grade premiums.

Regional Insights

North America Global Fatty Amines Market Trends

The U.S. anchors regional demand through a mature cleaning products ecosystem and a broad base of industrial water treatment applications. Tertiary amines for cationic surfactants and amine oxides remain critical in household and institutional cleaning, while oilfield and process water chemicals sustain industrial uptake. Regulatory oversight from agencies such as the U.S. Environmental Protection Agency (EPA) drives continuous improvements in product stewardship across applications.

Innovation trends emphasize greener chemistry and tighter impurity controls, supporting reformulations in home care and potential future qualification for sensitive industrial processes. Regional suppliers benefit from proximity to ethylene and ammonia feedstocks, though energy price swings warrant hedging strategies and selective long term contracting.

Europe Global Fatty Amines Market Trends

Germany, France, the U.K., Spain, and the Netherlands show persistent demand anchored in water treatment and advanced manufacturing. Compliance with EU REACH and sector specific regulations sustains the need for traceable, lower impact chemistries, with coordinated controls on migrating substances in food contact materials underscoring product testing rigor. The regional focus on wastewater reuse, corrosion management in district heating and industrial utilities, and sustainability aligned personal care formulations favors high purity amines and certified feedstock models.

Producers and distributors emphasize lifecycle transparency, environmental labeling, and mass balance certifications—progress that aligns with brand owner sustainability commitments in detergents and cosmetics. Continuous investment in wastewater and industrial water technologies supports steady consumption of amine based treatment packages.

Asia Pacific Global Fatty Amines Market Trends

China, Japan, India, and ASEAN economies combine manufacturing scale, cost advantages, and growing domestic demand in agrochemicals, construction, and water treatment. National and provincial projects in industrial wastewater management, alongside agricultural modernization programs, are key consumption pillars. Market reviews highlight China as a prominent demand and production hub with steady ~4.0% growth noted in recent analyses, supported by infrastructure and industrial development.

Capacity expansion and portfolio localization-illustrated by Evonik’s specialty amines investment in Nanjing with green electricity sourcing-enhance supply chain resilience and product customization for regional customers. India’s low cost manufacturing base and skilled workforce add to the region’s export competitiveness, while rising domestic use of anti caking agents and agrochemical intermediates further lifts fatty amine demand.

Competitive Landscape

The fatty amines market is moderately consolidated among integrated chemical and oleochemical players with global footprints. Leaders differentiate via feedstock integration, sustainability certifications, application know how in agrochemicals and water, and proximity capacity in Asia. Strategies include specialty grade development, debottlenecking and greenfield capacity in China and the U.S., and collaboration with Ag tech ecosystems to optimize agrochemical performance packages. Price management amid feedstock volatility, plus formulation support for regulatory compliance in North America and Europe, remains a core competitive lever.

Key Market Developments:

- In November, 2024 Evonik Industries AG broke ground to expand specialty amine production in Nanjing, enhancing portfolio breadth and access to cost effective raw materials, with operations ramping from 2026.

- In May 2022: Kao Corporation announced a new tertiary amine facility in Texas with about 20,000 tons annual capacity, targeted to commence operations by 2025.

- In September 2018: Indo Amines Ltd. merged Mains Organics and Core Chemicals subsidiaries to improve product breadth and profitability.

Companies Covered in Fatty Amines Market

- Akzo Nobel N.V.

- Evonik Industries AG

- Kao Corporation

- Clariant AG

- Arkema S.A

- Solvay S.A

- E.I. du Pont de Nemours & Co

- Albemarle Corporation

- Procter & Gamble Company

- Lonza Group Ltd

- Eastman Chemical Company

- Indo Amines Ltd

- Sterling Auxiliaries Pvt. Ltd.

- Nouryon

- Wuxi Zhufeng Fine Chemical Co., Ltd.

- NOF CORPORATION

Frequently Asked Questions

The fatty amines market is valued at US$ 3.8 Bn in 2025 and projected to reach US$ 5.9 Bn by 2032, reflecting a 6.7% CAGR over 2025–2032; historical CAGR during 2019–2024 is 5.4%.

Agrochemical performance enhancement and expanding water treatment investments are core drivers; fatty amines act as anti‑caking agents, emulsifiers, biocides, and corrosion inhibitors in these applications.

Primary Fatty Amines lead with about 31% share due to their role as intermediates for downstream amines and direct use in flotation, anti‑caking, and corrosion inhibition.

Asia Pacific leads on manufacturing scale and diversified end‑use demand; capacity expansions and localization by global players strengthen supply and cost positions.