- Specialty & Fine Chemicals

- Fatty Amides Market

Fatty Amides Market Size, Share, and Growth Forecast 2026 - 2033

Fatty Amides Market by Product Type (Erucamide, Oleamide, Stearamide, Behenamide), Product Form (Beads, Powder, Others), Application (Lubricants, Anti-Block Agents, Release Agents, Slip Agents, Dispersants, Others), Industry (Film Processing, Rubber, Ink, Others), and Regional Analysis for 2026 - 2033

Fatty Amides Market Size and Trend Analysis

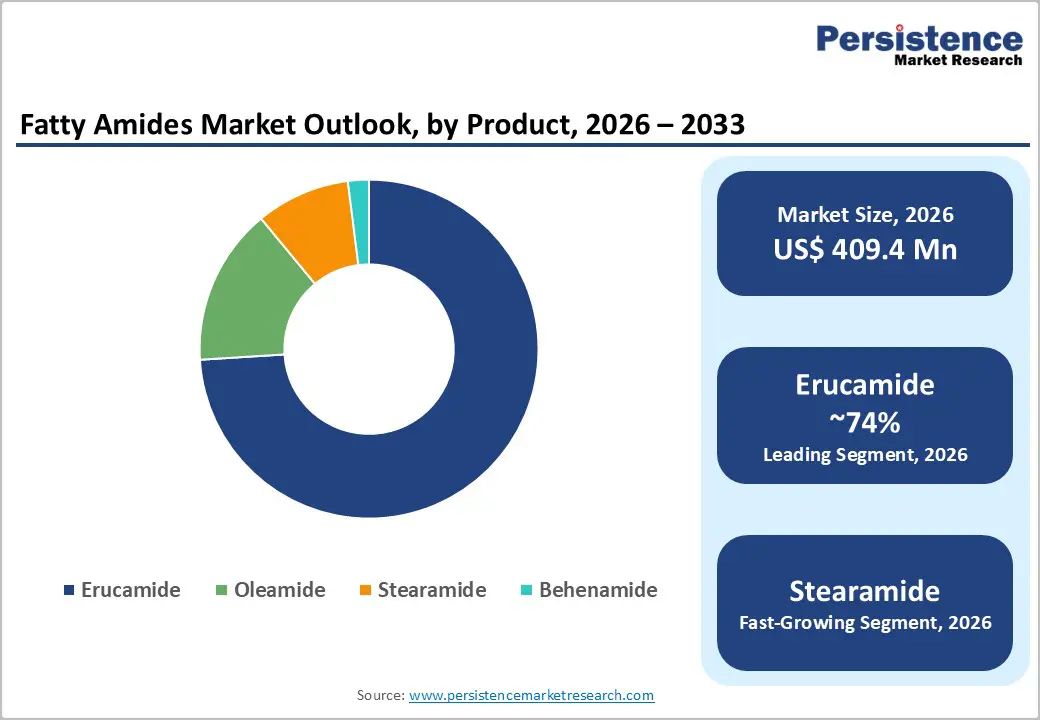

The global fatty amides market size is valued at US$ 409.4 million in 2026 and is projected to reach US$ 585.6 million by 2033, growing at a CAGR of 5.2% between 2026 and 2033. This consistent expansion is driven by accelerating global demand for flexible packaging films, the progressive shift toward bio-based oleochemical additives under sustainability-driven regulatory frameworks, and the expanding application of fatty amides as performance-enhancing slip and anti-block agents across polyolefin film processing industries.

The global flexible packaging industry, which is the primary end-use driver for fatty amide slip agents, is expanding at a sustained pace, supported by the Food and Agriculture Organization of the United Nations (FAO)-documented growth in packaged food consumption in emerging economies and the structural premiumization of consumer goods packaging in North America, Europe, and Asia Pacific.

Key Industry Highlights:

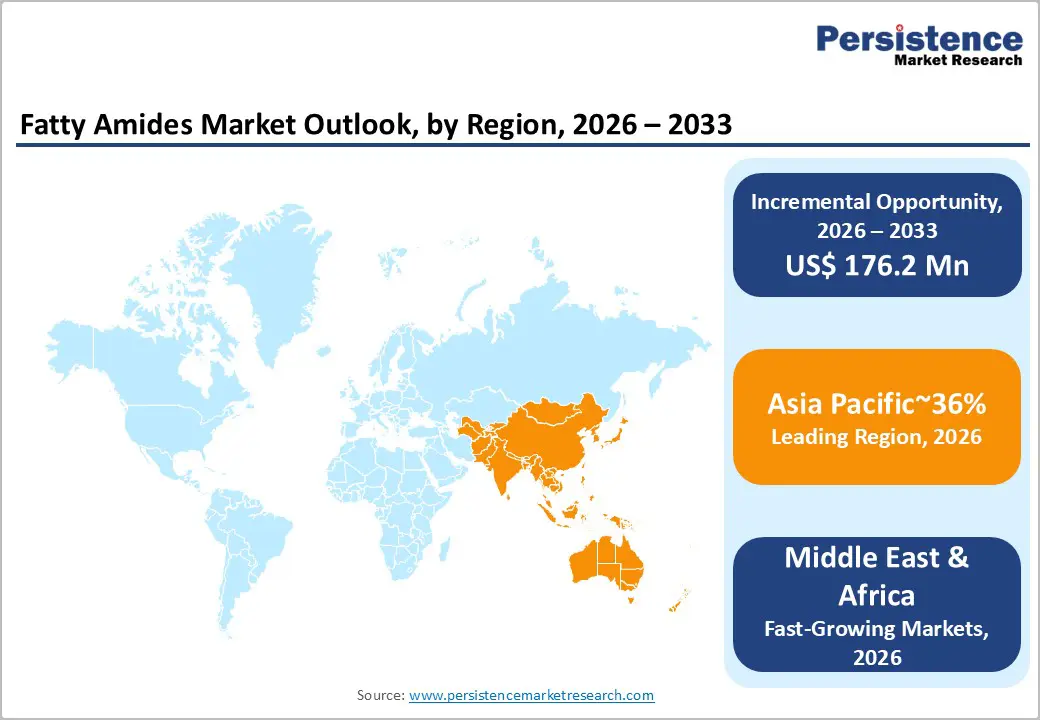

- Leading Region: Asia Pacific leads the global Fatty Amides market, anchored by China's e-commerce-driven packaging industry, valued at approximately US$ 2.2 trillion in 2024, and India's expanding domestic film conversion sector, with regional producers Fine Organic Industries, Sichuan Tianyu, and KLK Oleo sustaining the world's largest fatty amide manufacturing base.

- Fastest Growing Region: Asia Pacific is simultaneously the fastest-growing region, led by India's government-supported specialty chemicals expansion under the PLI scheme, Vietnam's rapidly growing flexible packaging export industry, and Indonesia and Malaysia's integrated palm oil-to-oleochemical production corridors providing competitive bio-based fatty amide feedstock advantages.

- Dominant Segment: Erucamide leads the Product Type category with approximately 74% of global Fatty Amides market revenue, driven by its irreplaceable role as the premier slip agent in polyolefin film formulations globally, with regulatory approval under FDA 21 CFR and EU Regulation 10/2011 cementing its dominant position across food-contact film applications worldwide.

- Fastest Growing Segment: The Printing Ink and Specialty Coatings sub-segment within Applications is the fastest-growing category, driven by the European Printing Ink Association (EuPIA) mandating bio-derived, food-contact-compliant wax and amide additives and the rapid expansion of flexible packaging printing capacity across China, India, and Vietnam, creating multi-year demand growth for micronized fatty amide powder dispersions.

- Key Market Opportunity: The global masterbatch industry's transition to RSPO and ISCC-certified bio-based additives, compelled by the EU's Single-Use Plastics Directive and brand owner sustainability commitments, creates a premium-priced, policy-guaranteed procurement opportunity for fatty amide producers with certified sustainable supply chains, enabling suppliers to access long-term preferred supplier contracts at above-market pricing through 2033.

DRO Analysis

Drivers - Booming Global Flexible Packaging Industry Driving Sustained Slip Agent Demand

The global flexible packaging industry is the single most important demand driver for fatty amide slip agents, particularly erucamide and oleamide, which are compounded into polyethylene (PE) and polypropylene (PP) films to reduce surface friction and improve machinability on high-speed packaging lines. According to the World Packaging Organization (WPO), flexible packaging accounts for approximately 25% of total global packaging output by value and is one of the fastest-growing packaging segments globally, driven by the convenience food, e-commerce, personal care, and pharmaceutical sectors.

Global plastic film production, the primary processing substrate for fatty amide slip agents, exceeded 80 million tons annually in recent years and continues to expand, particularly in Asia Pacific where rising middle-class consumption is stimulating rapid packaging industry growth.

The European Plastics Converters (EuPC) industry body confirms that polyolefin film converters across Europe consume fatty amide-based masterbatches as an essential non-negotiable processing additive for friction coefficient control. The functional irreplaceability of fatty amide slip agents in polyolefin film formulations, where typical loading levels range from 0.05% to 0.2% by weight, ensures a structurally stable and growing demand floor for the fatty amides market as global film output continues to expand through 2033.

Oleochemical Industry Expansion and Bio-Based Additive Mandates Amplifying Feedstock Accessibility

Fatty amides are synthesized through the amidation reaction of fatty acids, primarily erucic acid (from high-erucic acid rapeseed oil), oleic acid (from sunflower or palm oil), stearic acid (from animal tallow or vegetable sources), and behenic acid (from Ben oil or high-erucic rapeseed), with ammonia or amines. The expanding global oleochemical industry, anchored by the world's largest palm oil and rapeseed producing regions in Malaysia, Indonesia, and Europe, is providing progressively more accessible and price-competitive fatty acid feedstocks for fatty amide synthesis.

According to the Malaysian Palm Oil Board (MPOB), Malaysia produced 18.03 million tons of palm oil in 2024, sustaining a reliable supply of C18 fatty acid derivatives, including oleic and stearic acids, for oleochemical processing. Simultaneously, the European Commission's Farm-to-Fork Strategy and REACH regulation's preference for bio-based specialty chemicals over petroleum-derived counterparts is creating regulatory pull for fatty amide producers to expand bio-derived product portfolios.

Companies including Croda International, KLK Oleo, and Fine Organic Industries are investing in production capacity expansions aligned with bio-based oleochemical feedstock supply security, reinforcing the market's upstream cost competitiveness and sustainability credentials through the forecast period.

Restraints - Volatility in Vegetable Oil and Fatty Acid Feedstock Prices Squeezing Producer Margins

Fatty amide production costs are significantly influenced by the price dynamics of upstream oleochemical feedstocks, particularly high-erucic acid rapeseed oil (HEAR), palm kernel oil, and tallow, which are subject to substantial price volatility driven by agricultural yield variability, geopolitical trade disruptions, and competing biodiesel demand. The Food and Agriculture Organization (FAO) reported that vegetable oil prices experienced acute volatility between 2021 and 2023, with the FAO Vegetable Oil Price Index peaking at record levels in early 2022, driven by the Russia-Ukraine conflict disrupting sunflower oil exports, before moderating in 2023.

This feedstock price instability makes it structurally difficult for fatty amide producers to maintain consistent gross margins, particularly for smaller producers without long-term supply agreements or backward integration into oleochemical refining, constraining market pricing stability and suppressing investment confidence.

Regulatory Restrictions on Animal-Derived Tallow Feedstocks in Key End-Use Applications

Stearamide and certain grades of behenamide, relies on animal-derived tallow as a cost-effective stearic acid source. However, regulatory and commercial end-use restrictions on animal-derived ingredients are progressively limiting tallow-based fatty amide applicability. The European Union's REACH Regulation (EC No. 1907/2006) and food-contact material regulations, including EU Regulation 10/2011 on plastic materials in contact with food, impose strict substance restrictions and migration limit requirements that effectively exclude certain tallow-sourced fatty amide grades from premium food packaging applications.

The growing adoption of Halal and Kosher certification requirements in food packaging supply chains, particularly in Middle Eastern and Southeast Asian markets, further restricts tallow-based product acceptance, constraining the addressable application scope for animal-derived fatty amide grades and pressuring producers to invest in alternative vegetable-derived synthesis routes.

Opportunities- Sustainable Masterbatch and Bio-Based Polymer Additive Markets: A High-Growth Platform for Fatty Amide Integration

The global masterbatch industry's accelerating transition toward bio-based and sustainably sourced polymer additives presents a highly strategic commercial expansion opportunity for fatty amide manufacturers. Masterbatch compounders, who are the primary channel through which fatty amide slip and anti-block agents are delivered to film processors, are facing growing pressure from brand owners and retailers in Europe and North America to demonstrate bio-based content and environmental product declarations (EPDs) for their additive formulations.

The European Bioplastics Association projects that the global bioplastic and bio-additive industry will triple in capacity by 2028, driven by mandatory bio-content policies under the EU's Single-Use Plastics Directive and evolving Extended Producer Responsibility (EPR) frameworks across G20 economies. Fatty amides, being inherently bio-derived oleochemicals, are positioned as natural "green additive" alternatives to synthetic slip agents such as silicone-based compounds.

Producers that obtain credible RSPO (Roundtable on Sustainable Palm Oil)-certified or ISCC (International Sustainability and Carbon Certification)-compliant supply chain credentials for their fatty amide products can access the premium-priced sustainable masterbatch segment and secure preferred supplier status with multinational brand owners pursuing bio-content targets. Companies including Croda International and Fine Organic Industries are advancing sustainability-certified bio-based fatty amide grades for this purpose, establishing a blueprint for the industry's premium product evolution through 2033.

Expanding Printing Ink and Specialty Coating Applications Unlocking New Demand Verticals

Fatty amides, particularly erucamide and stearamide in micronized powder form, are gaining traction as multi-functional performance additives in printing inks, surface coatings, and specialty wax compounds, where they function simultaneously as slip modifiers, surface energy modifiers, dispersants, and rub-resistance enhancers.

The European Printing Ink Association (EuPIA) has confirmed that bio-derived additives compliant with EU food contact regulations are in growing demand among ink formulators serving the food and pharmaceutical packaging sectors. In Asia Pacific, the rapid expansion of commercial printing and flexible packaging industries, particularly in China, India, and Vietnam, is creating multi-year demand growth for fatty amide-based ink additives.

Producers such as FACI Group and Italmatch Chemicals are expanding their specialty wax and dispersion product ranges that incorporate fatty amide functionality for printing ink applications, reflecting the commercial maturation of this adjacent high-value market segment. Companies that develop tailored fatty amide grades optimized for UV and water-based ink systems will be well-positioned to capture premium market share in this fast-evolving specialty chemicals niche through 2033.

Category-wise Analysis

Product Type Insights

Erucamide is the dominant product type segment, accounting for approximately 74% of total global Fatty Amides market revenue. Erucamide, the amide of erucic acid (C22:1 cis-13-docosenoic acid) derived from high-erucic acid rapeseed oil (HEAR), dominates the market owing to its exceptional performance as a slip agent in polyolefin film applications, where it migrates progressively to the film surface to create a low-friction layer with a target coefficient of friction (COF) of approximately 0.1–0.2 at standard loading levels. Its relatively high melting point (~82°C) combined with a long-chain unsaturated structure gives it superior slip performance stability at processing temperatures encountered in blown and cast polyethylene film manufacturing.

Croda International, PMC Biogenix, and KLK Oleo are the leading global erucamide producers, with production capacities distributed across Europe, North America, and Asia Pacific. The global production of HEAR rapeseed, the primary feedstock, is concentrated in Germany, Poland, Canada, and China, where dedicated HEAR cultivation programs by agricultural bodies ensure a managed and traceable supply chain. Erucamide's technical performance leadership and established regulatory approval under EU food-contact material regulations and U.S. FDA 21 CFR cement its dominant market position through the forecast period.

Product Form Insights

Beads constitute the dominant product form segment, capturing approximately 63% of total global Fatty Amides market revenue. The bead form, comprising spherical or prilled solid particles typically 2–5 mm in diameter, is the preferred physical presentation for fatty amide delivery to masterbatch compounders and direct polyolefin compounders because it offers superior handling characteristics: low dust generation, accurate volumetric dosing, free-flowing bulk behavior, and minimized worker exposure compared to fine powder alternatives.

Bead-form fatty amides produced through prilling, flaking, or pastillation processes can be accurately incorporated into gravimetric dosing systems on high-speed compounding lines without clogging or segregation, a critical requirement for precision masterbatch production where additive loading consistency directly affects film COF performance.

Leading producers including Croda International and Fine Organic Industries supply the majority of their erucamide and oleamide production in prilled bead form to global masterbatch customers. The European masterbatch sector, represented by EuPC, specifies bead-form fatty amides as the standard input format in supplier qualification requirements, reinforcing this form's structural market leadership throughout the forecast period.

Application Insights

Slip Agents constitute the leading application segment, accounting for approximately 35% of total global Fatty Amides market revenue. Fatty amide slip agents, primarily erucamide and oleamide, are the technically preferred and most commercially established solution for reducing the coefficient of friction (COF) in polyolefin films used in flexible packaging, enabling smooth, high-speed passage of packaging materials through form-fill-seal (FFS), overwrap, and horizontal flow-wrap machines.

The performance advantage of fatty amide-based slip agents over alternative technologies, including silicone-based slip additives, lies in their bio-derived origin, competitive cost profile, and proven regulatory compliance under FDA 21 CFR and EU Regulation 10/2011 for food-contact packaging applications.

The Association of Plastics Manufacturers in Europe (PlasticsEurope) reports that polyolefin films account for the largest share of European plastic production, providing the structural demand base that sustains slip agent leadership. Fatty amide slip agents are consumed globally at average loading levels of 500–2,000 ppm by weight in final film formulations, translating to large absolute consumption volumes given the tens of millions of tons of polyolefin film produced annually worldwide.

Industry Insights

Film processing is the dominant Industry segment, accounting for approximately 38% of total global Fatty Amides market revenue. The film processing industry, encompassing blown film, cast film, and biaxially oriented film production lines for flexible food packaging, industrial films, agricultural mulch films, and consumer goods packaging, is by far the largest end-use consumer of fatty amides globally, given the functional necessity of slip and anti-block agents in virtually every commercial polyolefin film formulation.

PlasticsEurope's plastics production data confirms that polyolefin films collectively account for several million tons of annual plastic production in Europe alone, with the Asia Pacific region producing the largest absolute volumes globally. The relationship between fatty amide and film processing is particularly entrenched: erucamide and oleamide are specified in masterbatch formulations by all major film converters globally and are referenced in FDA, BfR (German Federal Institute for Risk Assessment), and EU food-contact positive lists, providing the regulatory certainty and formulatory stability that sustains long-term contractual demand from film processors.

Regional Analysis

North America Fatty Amides Trends & Insights

The United States is the largest market for fatty amides in North America holding nearly 84% share in the region, driven by one of the world's most extensive flexible packaging conversion industries and a well-established masterbatch additive supply chain concentrated in the Midwest and Southeast manufacturing corridors. The U.S. Flexible Packaging Association (FPA) confirms that flexible packaging is the largest and fastest-growing packaging segment in the United States, with annual shipments exceeding US$ 34 billion, directly sustaining fatty amide slip and anti-block agent demand across food, pharmaceutical, and personal care packaging applications.

PMC Biogenix, headquartered in Memphis, Tennessee, is the most significant North American fatty amide producer, supplying erucamide, oleamide, and stearamide grades to masterbatch producers and direct film converters across the continent. The U.S. FDA's 21 CFR regulatory framework provides clear compliance pathways for fatty amides in food-contact applications, supporting stable demand in regulated packaging segments.

Canada contributes through its large HEAR rapeseed cultivation base, a primary raw material source for erucamide synthesis, making it strategically significant in the global fatty amide supply chain as an upstream feedstock supplier. The Canola Council of Canada manages the country's rapeseed sector, which produces both food-grade canola and dedicated high-erucic rapeseed varieties for oleochemical industrial applications. North America's advanced regulatory infrastructure (EPA, FDA, and OSHA compliance frameworks), combined with the presence of globally leading fatty amide producers and formulators, including HB Chemical and Dyna Glycols, positions the region as both a significant consumption base and an innovation hub for advanced fatty amide product development.

Europe Fatty Amides Trends & Insights

Europe is the world's most sustainability-advanced region for fatty amide consumption, characterized by stringent regulatory requirements under REACH, EU food-contact material regulations, and the overarching European Green Deal framework, which collectively incentivize the adoption of bio-derived, sustainably sourced oleochemical additives in polymer processing. Germany is the largest European fatty amide market accounting 21% share of the market, underpinned by its highly developed plastics compounding, masterbatch, and film conversion industries, collectively among the world's most technically advanced.

The Industrieverband Kunststoffverpackungen e.V. (IK), Germany's plastics packaging industry association, cites slip and anti-block masterbatches based on bio-derived fatty amides as essential inputs for compliant food packaging production under EU Regulation 10/2011. Croda International plc, headquartered in East Yorkshire, UK, is the most globally influential fatty amide producer in Europe, supplying its Crodamide series of erucamide, oleamide, stearamide, and behenamide grades to masterbatch customers across the continent.

France and Spain together hold 19% and contributing through active flexible packaging and printing ink manufacturing sectors. The European Printing Ink Association (EuPIA) is driving adoption of EU-compliant bio-derived wax additives, including fatty amide dispersions, in printing inks serving food-contact flexible packaging.

The European Bioplastics Association's projection of tripling bio-additive capacity by 2028 is compelling European fatty amide producers to invest in RSPO-certified and ISCC-verified supply chain credentials, premium-positioning their product portfolios ahead of mandatory bio-content legislation expected under the EU Sustainable Product Regulation framework. Lamberti and FACI Group, both based in Italy, further reinforce Europe's position as a globally significant fatty amide supplier with diversified product portfolios serving specialty chemicals applications including lubricants, release agents, and dispersants.

Asia Pacific Fatty Amides Trends & Insights

Asia Pacific is the world's dominant fatty amide consumption region holds nearly 36% of the global market and the fastest-growing market, driven by the region's global leadership in flexible packaging film production, the world's largest concentration of polyolefin compounding and masterbatch manufacturing capacity, and advantaged access to palm oil and rapeseed fatty acid feedstocks from Malaysia, Indonesia, and China. China is both the largest consumer and producer of fatty amides in the region, with major domestic manufacturers including Sichuan Tianyu Oleochemical Co., Ltd. and Haihang Industries Co., Ltd. supplying erucamide and oleamide to the country's vast network of polyolefin film converters, masterbatch producers, and ink formulators.

India is the fastest-growing market growing with a 7.3% CAGR, supported by a rapidly expanding domestic flexible packaging industry and strong government manufacturing sector investment through the Production Linked Incentive (PLI) scheme for specialty chemicals. Fine Organic Industries Pvt. Ltd., one of the world's leading oleochemical additive producers, is headquartered in Mumbai, supplying a comprehensive range of fatty amide grades including erucamide, oleamide, stearamide, and behenamide to domestic and export markets. Mohini Organics Pvt. Ltd. and Pukhraj Additives LLP represent the growing tier of Indian specialty fatty amide producers serving domestic masterbatch and packaging needs.

Japan contributes through advanced application development, with Nippon Fine Chemical Co., Ltd. and Kao Corporation, both headquartered in Japan, supplying technically differentiated high-purity fatty amide grades for pharmaceutical, electronics, and specialty coating applications across the Asia Pacific premium segment. KLK Oleo, part of Malaysia's Kuala Lumpur Kepong Berhad (KLK), operates as a major regional oleochemical manufacturer with integrated palm-based fatty acid and fatty amide production, serving customers across Southeast Asia, China, and export markets globally.

Competitive Landscape

The global Fatty Amides market exhibits a moderately consolidated competitive structure, dominated at the premium tier by a small number of globally integrated oleochemical and specialty chemical companies, complemented by a broader set of regional producers in Asia and India. Croda International, PMC Biogenix, KLK Oleo, and Fine Organic Industries collectively command the majority of high-value erucamide and specialty amide supply in regulated food-contact and pharmaceutical applications.

Competitive differentiation is achieved through feedstock traceability and sustainability certification (RSPO, ISCC), product purity and regulatory compliance documentation (FDA, REACH, EU 10/2011), application technical support, and custom product development. Emerging competitive strategies include backward integration into HEAR rapeseed sourcing, development of vegan and tallow-free product grades, and partnerships with masterbatch compounders for co-development of high-performance multi-functional additive systems.

Key Developments:

- In 2024, Croda International plc expanded its bio-based fatty amide product line under the Crodamide brand, reinforcing its RSPO Mass Balance-certified supply chain credentials, targeting masterbatch producers and flexible packaging converters seeking verified sustainable oleochemical additive grades compliant with evolving EU packaging regulations.

- In 2024, Fine Organic Industries Pvt. Ltd. commenced expansion of its fatty amide production capacity at its Ambernath, Maharashtra plant in India, targeting growing domestic masterbatch and export demand for erucamide and oleamide from Southeast Asian markets.

- In 2023, KLK Oleo, subsidiary of Kuala Lumpur Kepong Berhad, received ISCC PLUS certification for its fatty acid-derived oleochemical additives including fatty amide grades, enabling it to supply certified bio-based inputs to European customers with mandatory sustainability documentation requirements.

Companies Covered in Fatty Amides Market

- Croda International Plc.

- PMC Biogenix Inc.

- Fine Organic Industries Pvt. Ltd.

- Nippon Fine Chemical Co. Ltd.

- Kao Corporation

- KLK Oleo

- FACI Group

- Italmatch Chemicals S.p.A

- Sichuan Tianyu Oleochemical Co., Ltd.

- Haihang Industries Co., Ltd.

- Mohini Organics Pvt. Ltd

- Pukhraj Additives LLP

- Dyna Glycols

- HB Chemical

- Lamberti

Frequently Asked Questions

The global Fatty Amides market is valued at US$ 409.4 Mn in 2026 and is projected to reach US$ 585.6 Mn by 2033, expanding at a CAGR of 5.2% during the forecast period.

The two primary drivers are: (1) the accelerating global flexible packaging industry, with the World Packaging Organisation confirming flexible packaging as one of the fastest-growing packaging segments globally, driving demand for erucamide and oleamide slip agents; and (2) the oleochemical industry's expansion in Malaysia, Indonesia, and India, where the Malaysian Palm Oil Board (MPOB) confirmed 18.03 million tons of palm oil production in 2024, sustaining competitive bio-based fatty acid feedstock supply for fatty amide synthesis.

Erucamide leads the Product Type segment with approximately 74% of global market revenue.

Asia Pacific leads the global Fatty Amides market, driven by China's world's largest e-commerce industry, valued at approximately US$ 2.2 trillion in 2024 per China's National Bureau of Statistics.

The most significant opportunity is the global masterbatch industry's mandatory transition to RSPO and ISCC-certified bio-based polymer additives, driven by the EU's Single-Use Plastics Directive and brand owner sustainability commitments. Fatty amide producers with certified bio-based supply chains, such as Croda International (RSPO Mass Balance certified) and KLK Oleo (ISCC PLUS certified), can command premium pricing and preferred supplier status from multinational masterbatch and film converter customers, unlocking a structurally higher-margin revenue stream through 2033.

The global fatty amides market is led by Croda International Plc., PMC Biogenix Inc., Fine Organic Industries Pvt. Ltd., KLK Oleo, Nippon Fine Chemical Co. Ltd., Kao Corporation, FACI Group, Italmatch Chemicals S.p.A., Sichuan Tianyu Oleochemical Co., Ltd., Haihang Industries Co., Ltd., Mohini Organics Pvt. Ltd., Lamberti S.p.A., Emery Oleochemicals, Baerlocher GmbH, HB Chemical, and Pukhraj Additives LLP, among others.